Hunting small caps | Turnarounds | Capital cycle | Special sits. Professionally managing capital.✍️ Deep dives • Articles • Portfolio upd. Not investment advice

Joined November 2023

- Tweets 1,991

- Following 528

- Followers 1,258

- Likes 4,930

505 Photos and videos

Pinned Tweet

May 18

Semapa may be making moves toward another attempt to go private.

Three clues:

1️⃣ With the sale of Secil, the holding sits on €761M in net cash (40% market cap)

2️⃣ Despite the cash position, the company has maintained last year's dividend.

3️⃣ At the AGM on May 28th, a buyback of 10% of shares will be voted on and approved.

Many Spanish value investors like @HolyFinance @JRuizRuiz @JRDA85 @GustavoBolsa have been following this holding for years. The catalysts may finally be aligning.

Full article on the blog.

🔗in next comment.

$SEM $NVG

4

7

19

4,208

Jun 13

Yesterday, someone acquired a 4% stake in Foraco, with volume surging to 24x the average daily volume. Something is moving. The short-term catalysts are there. We'll see.

$FAR.TO $FAR $MDI.TO $MDI

Apr 30

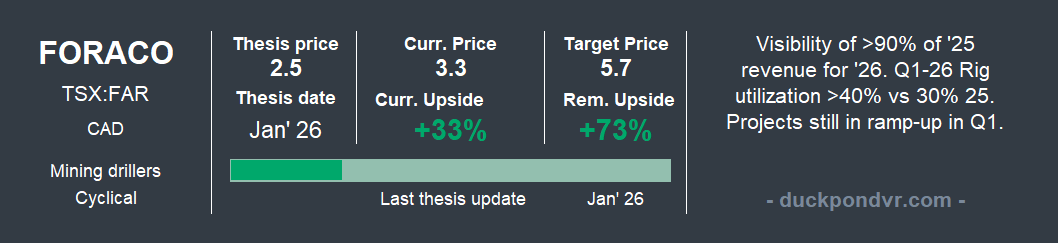

Foraco (TSX: FAR) — Q1 results

Sales $66.3 ( 20.4%), GM 10.7% (-340bps), EBIT margin 3.1% (-220bps), Net Profit $0.1m. Net debt $90.9m. KPIs: Rig utilization 40% (vs 30%)

🔍Drivers: Solid Mining ( 30%), NA ( 39%) & SA ( 98%). Soft Water (-18%) & APAC (-31%) due to contract phasing. Lower-margin cause og ramp-up phases of new long-term contracts.

📅Outlook: Highly favorable, underpinned by a record $404 m backlog secured at year-end.

✍️Write-ups

Ene'26 - Full thesis (Buy🎯: CAD 5.70)

$FAR.TO $FAR

1

2

287

Jun 12

SpaceX: $1.8T valuation, cash flows decades away, Macaulay Duration through the roof. That's the liquidity degradation playbook. Probably one of the worst retail scams (at short-term).

2

5

227

The Value Pond retweeted

Jun 3

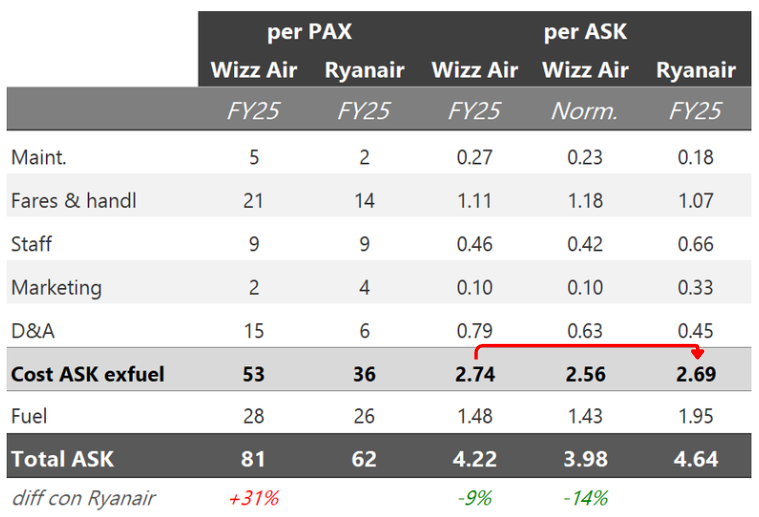

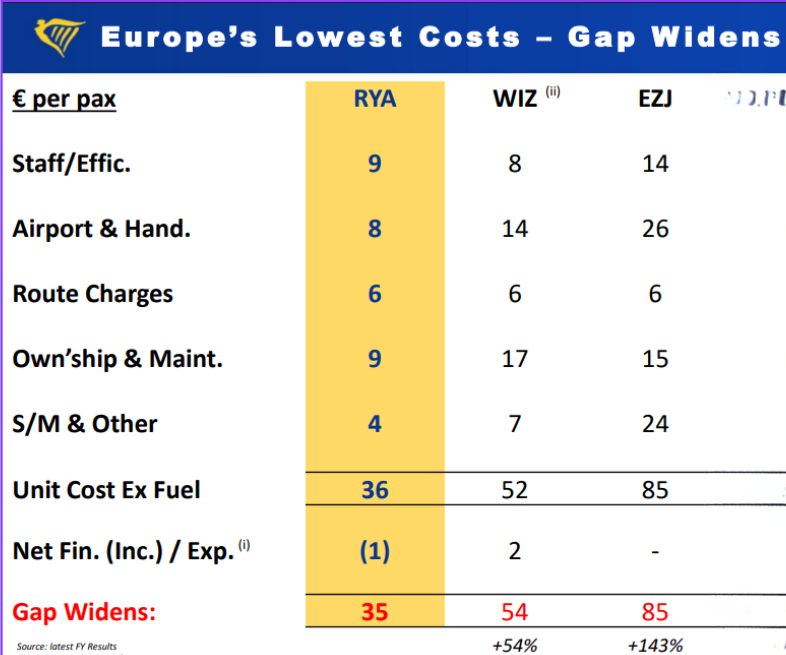

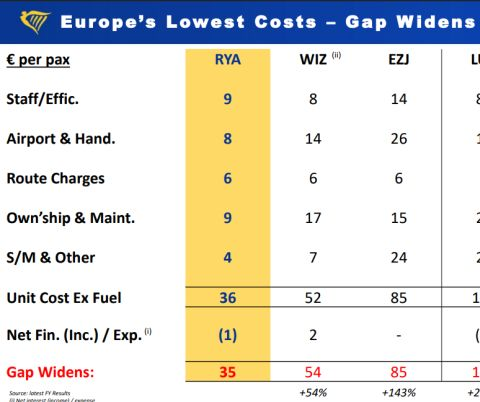

✈️ This slide is widely repeated in Ryanair earnings presentations, claiming a wide cost leadership gap over rivals. But does it hold up?

❗The table contains one inaccuracy (1️⃣) , one nuance worth mentioning (2️⃣), and one rather cheeky omission (3️⃣). Let's go. 🧵 (1/)

$WIZZ $WIZZ.L $RYA $RYAAY

1

2

8

854

Jun 3

Hey Mr. Market. What about ForvIA? They were on IA before.

1

1

3

313

The Value Pond retweeted

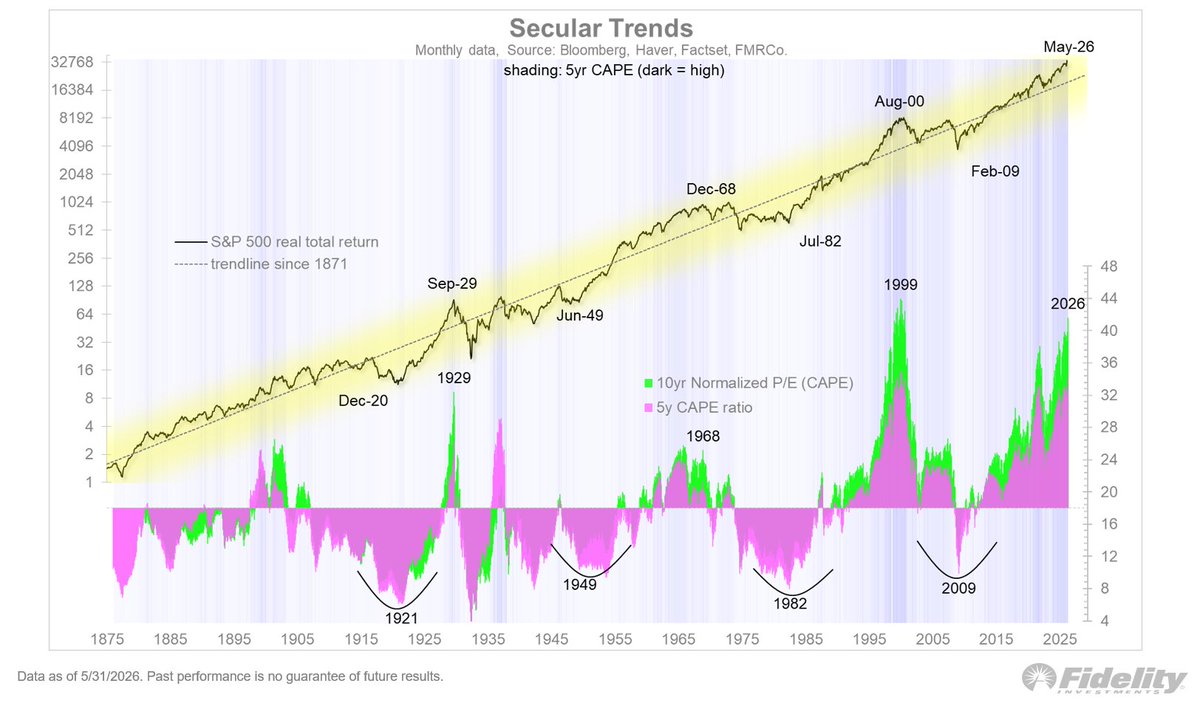

Those starting points are further confirmed by valuation via the 5-year CAPE ratio, as shown below. By that measure, the P/E bottoms that line up with the above are also 1921, 1949, 1982, and 2009. /END

4

5

53

8,352

The Value Pond retweeted

Jun 3

Combining effects 1️⃣ and 3️⃣, Wizz Air's unit costs are ~9% lower. Normalising for effect 2️⃣, they are ~14% lower.

The conclusion is clear: Wizz Air is Europe's real cost leader.

⚠️ this is not an attack on Ryanair. Ryanair sustains higher load factors, charges more per seat by flying higher-income routes, and has real advantages in areas like ground handling. It is an exceptionally well-run company with strong margins. (6/)

1

1

5

223

Jun 3

IFF’s new CEO has purchased $20 million in shares. This comes shortly after IFF announced the sale of its Food Ingredients business, leaving three segments: Scent and Taste (closer to Givaudan’s model) and Health & Biosciences (similar to Novozymes).

It has taken six years to digest the merger with DuPont’s Nutrition & Biosciences business, forcing the company to divest quality assets like Lucas Meyer Cosmetics and divisions such as Pharma Solutions.

After all this, it’s a company in a sector I really like. It underpins consumer staples, operates as a NIMBY-style oligopoly with high barriers to entry, and its products represent a very low percentage of the final product's total cost.

$IFF $GIVN $GIVNY $NSIS $NVZMY

2

397

Jun 3

✈️ This slide is widely repeated in Ryanair earnings presentations, claiming a wide cost leadership gap over rivals. But does it hold up?

❗The table contains one inaccuracy (1️⃣) , one nuance worth mentioning (2️⃣), and one rather cheeky omission (3️⃣). Let's go. 🧵 (1/)

$WIZZ $WIZZ.L $RYA $RYAAY

1

2

8

854

Jun 3

📖 I published a full thesis and an update on Wizz Air: fuel crisis, demand signals, sale & leaseback mechanics, and the full Excel model for paid subscribers.

Read it at duckpondvr.com 🦆

$WIZZ $WIZZ.L (8/)

1

2

277

Jun 3

Sometimes the numbers tell a different story.

If you found this useful, like and repost the first tweet. It helps more people see the analysis.

Follow @TheValuePond for deep dives on overlooked companies. 🦆

Jun 3

✈️ This slide is widely repeated in Ryanair earnings presentations, claiming a wide cost leadership gap over rivals. But does it hold up?

❗The table contains one inaccuracy (1️⃣) , one nuance worth mentioning (2️⃣), and one rather cheeky omission (3️⃣). Let's go. 🧵 (1/)

$WIZZ $WIZZ.L $RYA $RYAAY

2

163

The Value Pond retweeted

Dejo algunas cuentas interesantes dentro del mundo de la inversión:

@HolyFinance

@LuisMiguelValue

@TorrasLuis

@TheValuePond

@ASESOREFA

@Gestiprudent

@dapreal4

@creandocartera

@foso_defensivo

@MartaEscribanoL

@marcgarrigasait

@dantelriv

@Carlos_MoraM

Me dejo muchas, perdonadme.

3

1

14

2,262

Jun 2

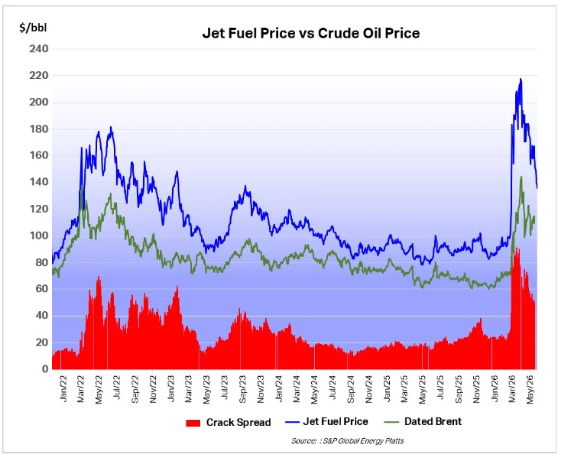

Jet fuel prices dropped 11% over the week but are still up 60% year-on-year in Europe.

3

226

The Value Pond retweeted

Jun 2

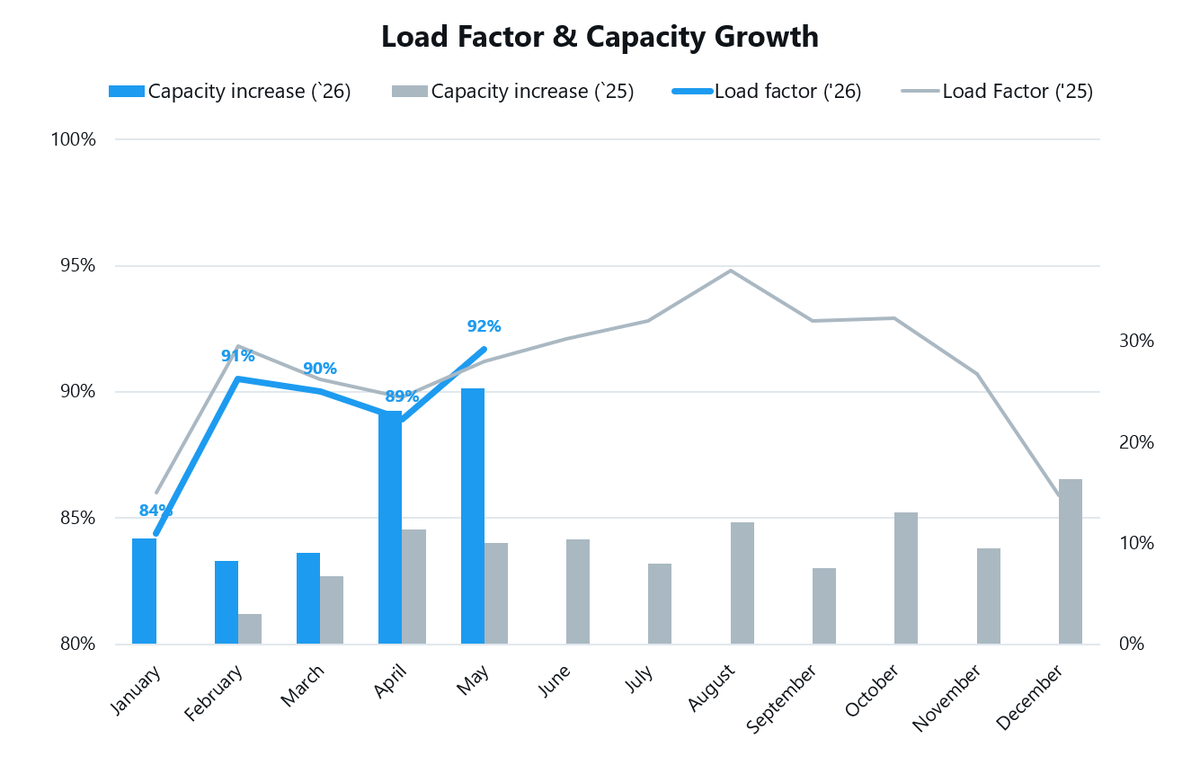

Wizz Air🛫May traffic statistics:

👤 26% passengers in May despite war.

✅91.7% load factor ( 50 bps) despite 25% capacity increase.

⛽️Lower CO2 per passenger/km, less fuel consumption. 70% of jet fuel is hedged around US$720/MT for the key part of the year.

Strong metrics in a key month, with operational fleet size up approximately 18% compared to Q2 2026.

In case you missed, should read this thread 👇 x.com/TheValuePond/status/20… $WIZZ $WIZZ.L

May 4

Michael O'Leary, Ryanair's CEO, recently said about Wizz Air: "If oil stays at these levels, two or three European airlines in October or November could go bankrupt, like Wizz Air."

A great CEO. But always provocative. And in this case, wrong.

A thread. 🧵(1/12)

$WIZZ $WIZZ.L $RYA $RYAAY

1

3

9

2,902