Wannabe small and micro-cap investor in transition with plenty of ground to cover.

Joined November 2021

- Tweets 956

- Following 343

- Followers 53

- Likes 3,631

1 Photos and videos

MyMoneyMyMistakes retweeted

May 7

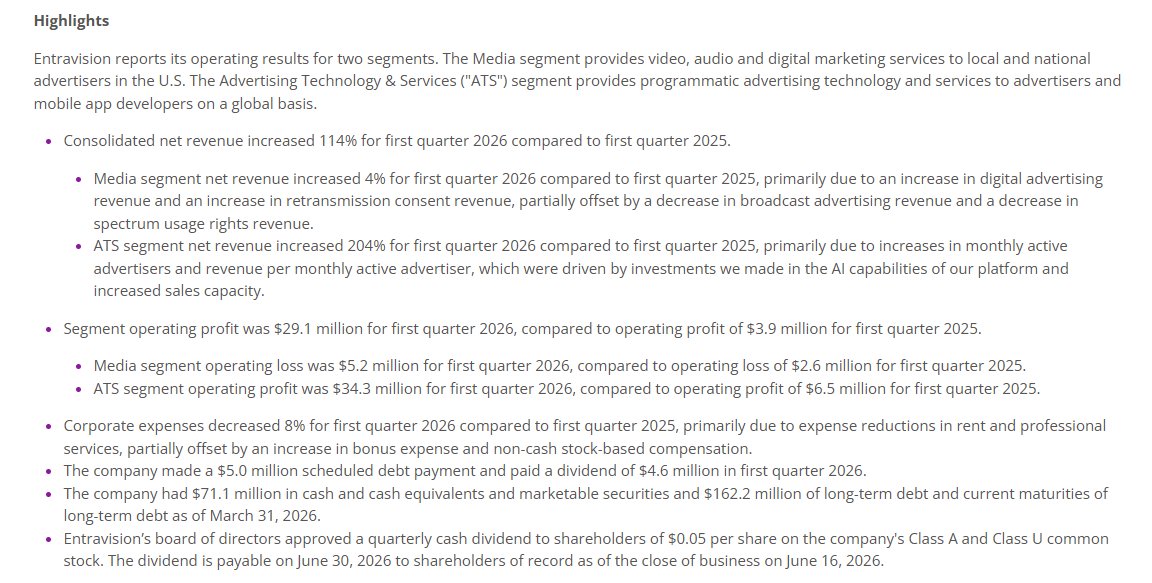

Medical Facilities Corporation Announces 2026 First Quarter Results prn.to/4uwhRQC | $DR.TO $MFCSF #buyback #NCIB #earnings #healthcare #TSX

2

5

1,573

MyMoneyMyMistakes retweeted

May 5

For myself

Life is a bit like the stock market. In the short run, randomness dominates, people can treat you unfairly, and outcomes can be disconnected from effort. But over the long run, there’s a stronger pull toward deserved results on average.

As late Munger put it “The world is not yet a crazy enough place to reward a whole bunch of undeserving people.”

2

6

719

MyMoneyMyMistakes retweeted

Das beliebte Quartalsupdate steht an und getreu dem Motto "Never change a running system" ist auch Patrick Schmidt wieder mit dabei. Bei beiden Schmidts gab es einen verhaltenen Start ins Börsenjahr und Christian hat sich nach dem...

youtube.com/watch?v=fqS1gebc…

1

4

30

6,371

MyMoneyMyMistakes retweeted

Excited to share that the Special Situations Digest has moved to a new home.

If you want a free month of paid access (Pro), just do the following: retweet this, drop a comment below, and send me a DM with your email, and I will give you complimentary access.

57

62

90

33,207

MyMoneyMyMistakes retweeted

Mar 24

Before travelling to Stockholm, we also met with $CSU.TO Jamal Baksh. Just received the green light from him, so our report on our meeting will be published at the end of this week at tresorcapitalnieuws.nl. Be sure to subscribe (it's free!).

We also discussed $TOI.V and $SABR, among others.

Mar 24

The RedEye serial acquirer conference videos are now live on their website. We met up with the team of Chapters Group $CHG.DE and several other serial acquirers. Read our report here:

tresorcapitalnieuws.nl/en/de…

4

8

128

18,916

MyMoneyMyMistakes retweeted

Mar 11

$SABR receives plenty of hate. My timeline is full of people calling it a shitco.

Investors who don’t understand $CSU.TO probably don’t get the $SABR story either.

Yes, SABR may lag the market leader $AMADY and its biggest competitor. But almost all revenue is recurring — meaning profitability could be much higher than it is today.

Many expenses could likely be cut without harming the top-line. Even a legacy business behind the leader could operate at similar margins as $AMADY for years.

Imo, this is a cost-cutting story, not about making SABR the #1 GDS or airline IT business.

Milk the cow and move on.

7

7

91

14,751

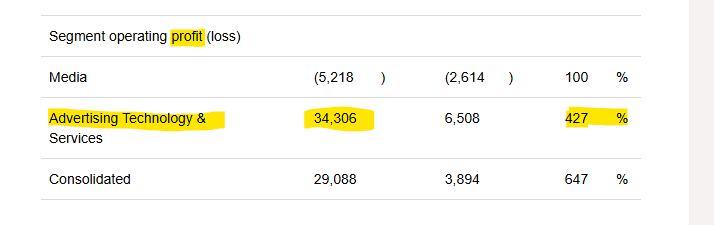

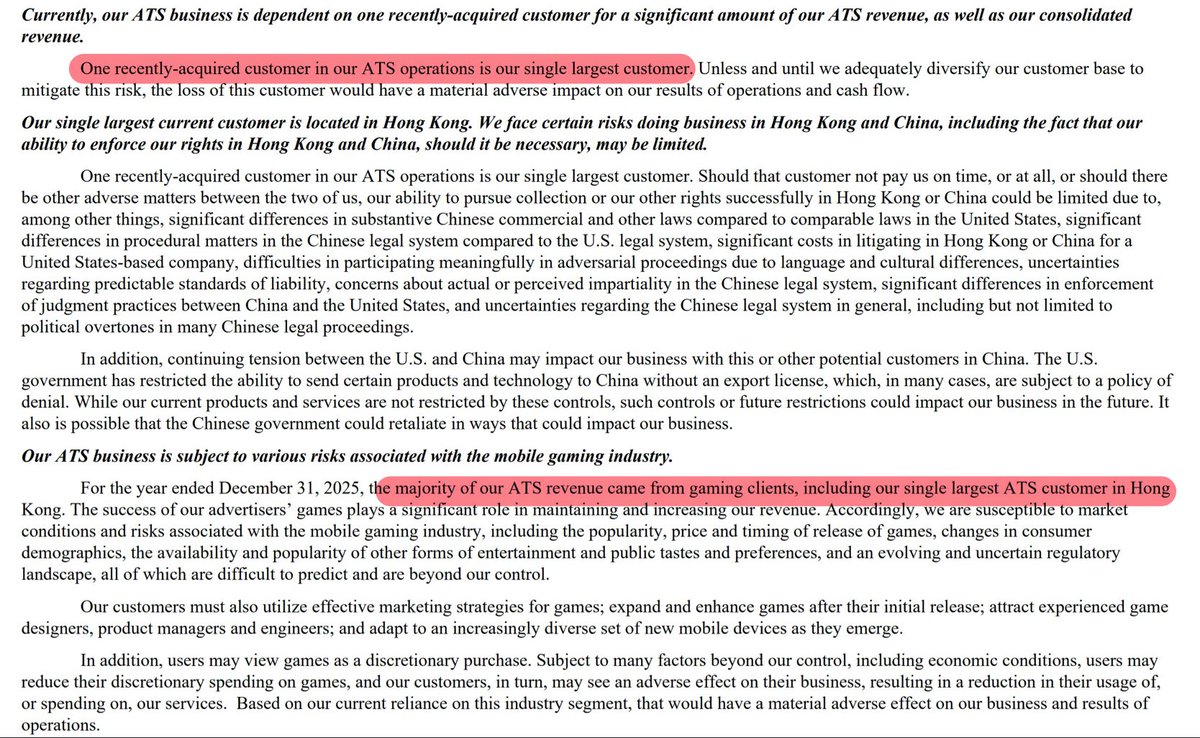

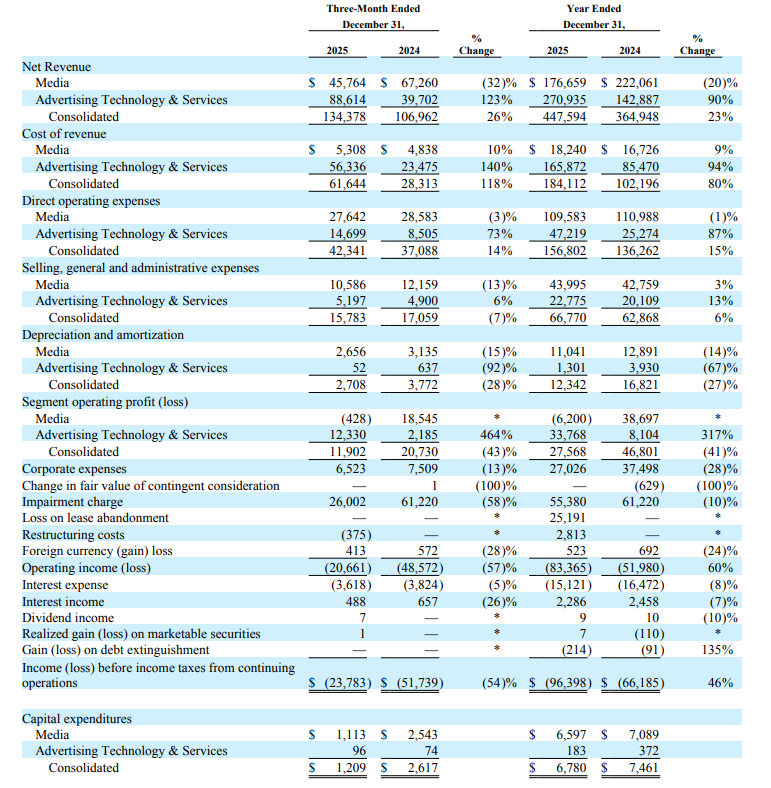

49% for Q4 and 61% FY.

And excl. the whale client, ATS operating margin is still up ~350% year over year.

This reaction is absurd.

$EVC

Mar 10

Here's my take on $EVC's China risk. Mgmt noted one customer = 9% of group revenue in 3Q25 and FY25. Excluding them entirely, ATS still grew 49% y/y. Meanwhile Liftoff is eyeing an IPO at 27x EBIT on 32% growth with $1.85B in NIBD. Selloff seems completely overblown imo.

1

1

2

389

MyMoneyMyMistakes retweeted

Mar 10

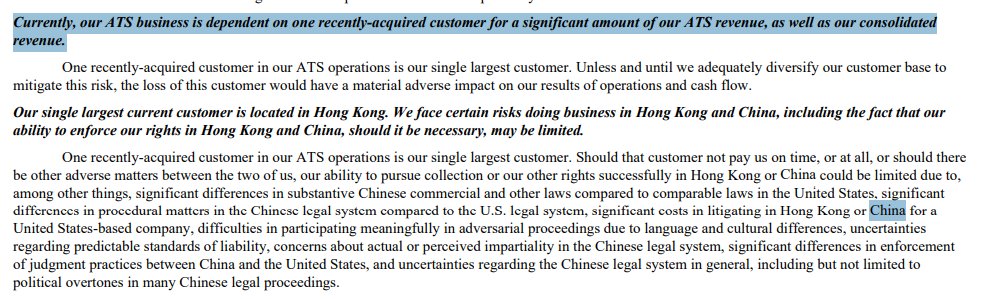

Before someone reads “customer concentration from 🇨🇳” and immediately clicks sell, I think a few things are worth considering:

1/ What percentage of the company’s total revenue that concentration actually represents

2/ What kind of growth the AdTech segment and Smadex would have posted this year/quarter if $EVC hadn’t added that major customer

3/ Whether the market is actually pricing in high growth at the current valuation

4/ Where Smadex is headquartered, whether it sells a product or a service (or even whether the customer is actually Chinese or Hong Kong–based)

5/ What landing one large customer (the first of this profile for the AdTech segment) typically implies about the chances of landing another somewhere down the line

It’s definitely not SaaS, but I also don’t think “not sticky” is a valid concern. Once a programmatic DSP onboards a client and establishes the relationship, the spend should be fairly recurring. Unless Smadex gets outcompeted on ROAS over time or customers stop valuing high level of support they currently receive. (which is another thing to consider)

I don’t want to make an example out of @MallardResearch, but I’ve seen too many investors overblow this concern and miss the big picture not to comment on it.

Customer concentration always scares me.

$EVC Entravision’s concentration with a Chinese gaming company? Even more so.

Unlike much hated SaaS, revenue is likely not sticky. A large partner helps, but still deserves a discount.

Cheap? Probably. But hard to size large.

2

2

27

6,066

MyMoneyMyMistakes retweeted

Mar 10

Here's my take on $EVC's China risk. Mgmt noted one customer = 9% of group revenue in 3Q25 and FY25. Excluding them entirely, ATS still grew 49% y/y. Meanwhile Liftoff is eyeing an IPO at 27x EBIT on 32% growth with $1.85B in NIBD. Selloff seems completely overblown imo.

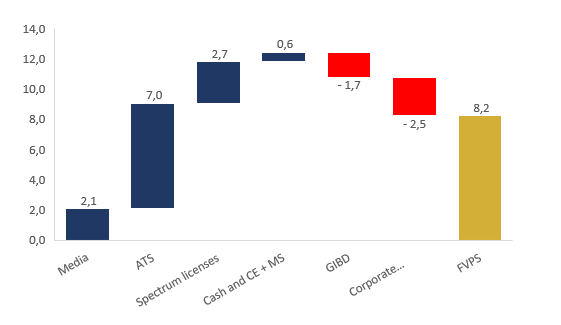

Shocked $EVC isn't up more. ATS rev 123% y/y ( 16% seq.), $12.3m EBIT (~14% margin) while investing heavily in AI & sales. ATS alone could be worth ~$740m at 15x EBIT run rate. Add midterm tailwinds, spectrum licenses worth ~$300m, if not more, and this is close to a 3x

2

2

24

4,143

MyMoneyMyMistakes retweeted

1/4 In der heutigen Folge befindet sich erstmals ein Gast direkt bei Christian vor Ort. @FBuschek war bereits schon einmal im Podcast vertreten und hat uns dieses Mal eine Aktie aus einem Sektor mitgebracht, der bislang noch gar nicht...

open.spotify.com/episode/2jc…

2

6

28

1,926

MyMoneyMyMistakes retweeted

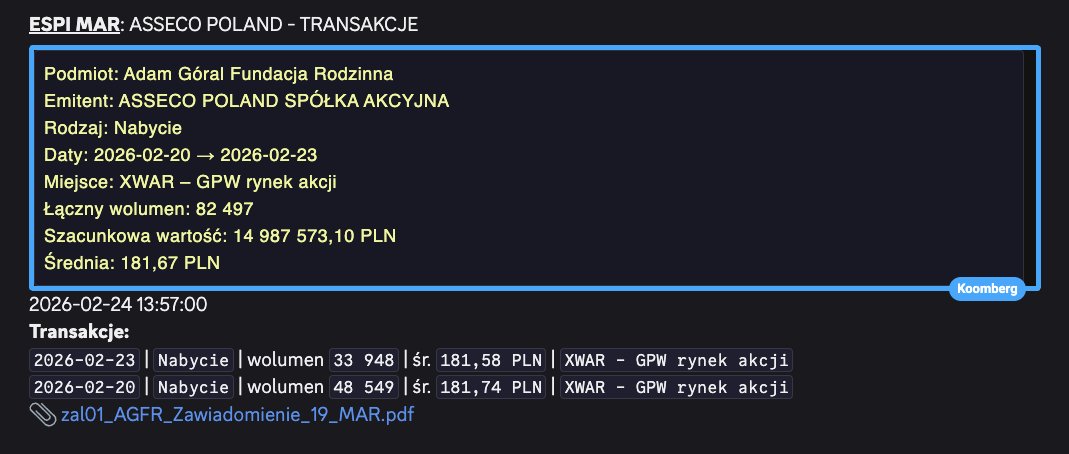

Feb 24

ASSECO POLAND - TRANSAKCJE

$ACP.WA

Szacunkowa wartość: 14,988 mln

8

2

49

10,263

MyMoneyMyMistakes retweeted

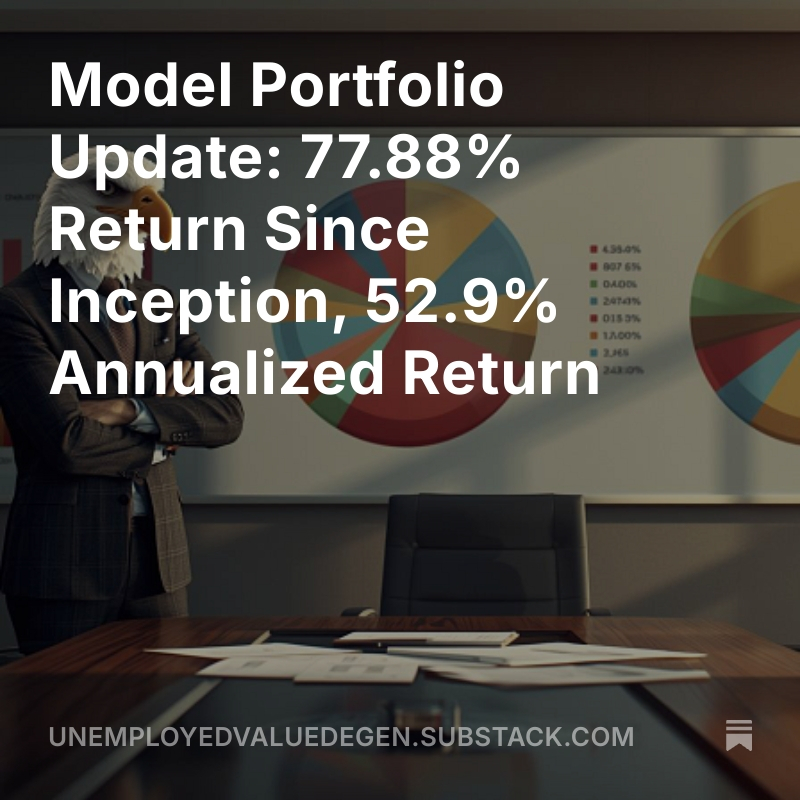

Model Portfolio Update: 77.88% Return Since Inception, 52.9% Annualized Return

I will be giving away an annual subscription at random to an account that retweets this post.

8

80

116

447,671

MyMoneyMyMistakes retweeted

Jan 23

$ACP.WA letter to shareholders

inwestor.asseco.com/en/about…

2

51

11,930

MyMoneyMyMistakes retweeted

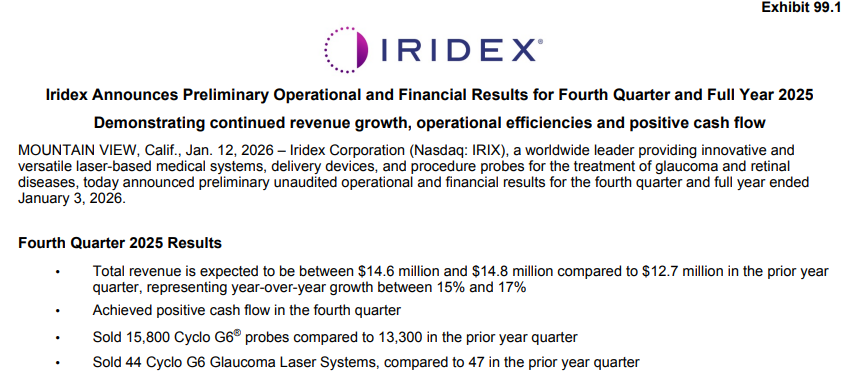

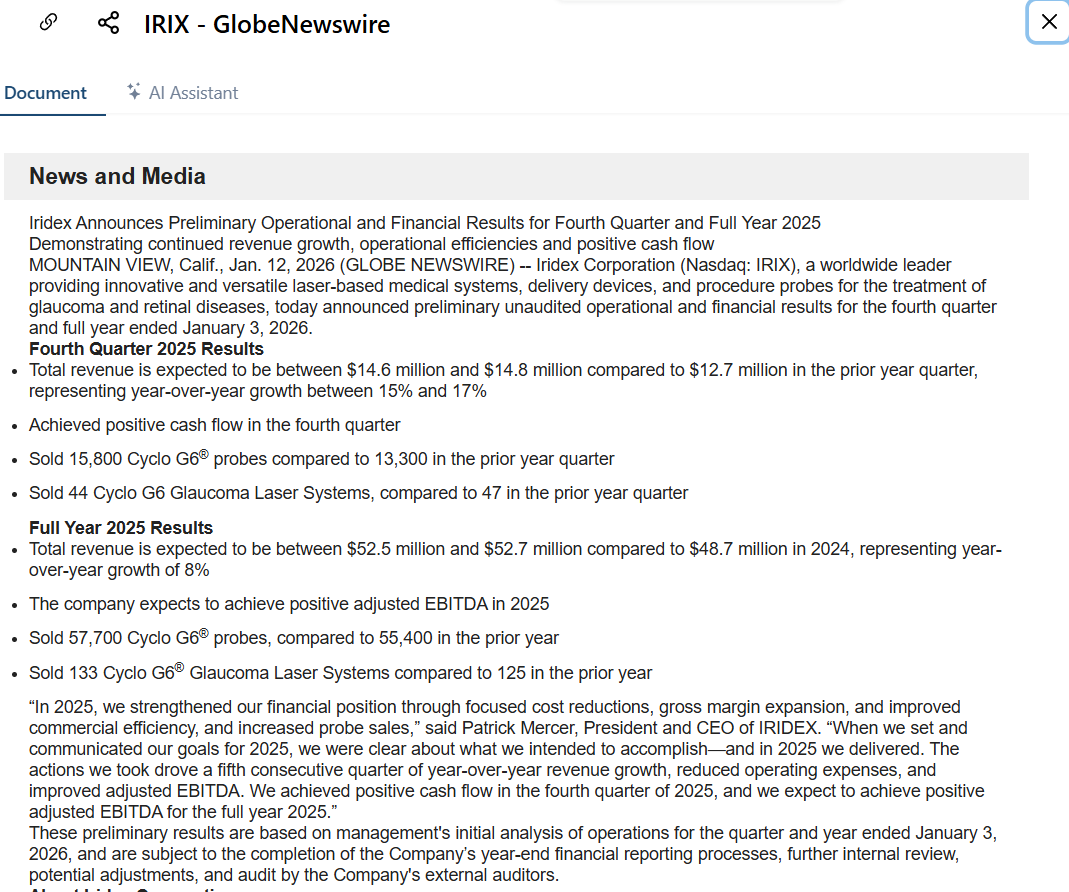

$IRIX I just remembered a statement from the BI interview. Growth in 26 should be in the same range as the growth seen in Q4, which would imply revenue growth of roughly 15-17% for 26. This is not formal guidance, but it is still a promising indication.

youtu.be/27bz1atjq6I?si=hDH0…

1/5 $IRIX At first glance, outstanding results, at least regarding growth in revenue and probes. It seems their efforts around probe growth are bearing fruit and are consistent with their recent comments in presentations.

Regarding...

app.tracktacle.com/publicati…

1

1

18

3,796

MyMoneyMyMistakes retweeted

1/5 $IRIX At first glance, outstanding results, at least regarding growth in revenue and probes. It seems their efforts around probe growth are bearing fruit and are consistent with their recent comments in presentations.

Regarding...

app.tracktacle.com/publicati…

2

3

18

7,127

MyMoneyMyMistakes retweeted

31 Dec 2025

Every microcap multi-bagger is the result of a management team that strung together two or more great quarters in a row. Small stocks need momentum to reach escape velocity. The more quarters they string together the higher the stock goes.

It's like dominos. Two great quarters in a row and the stock is probably a double. Three great quarters a triple. If a management can string together four to six great quarters and investors believe the momentum will continue - this is a 10-bagger.

The hard truth is the momentum usually runs out before we think. Microcap companies reach a ceiling in leadership, opportunity or both. Only a select few can backfill appropriately with talent, processes, and execution to continue the momentum and reach new highs.

microcapclub.com/how-long-wi…

6

12

115

15,543