Joined August 2017

- Tweets 8,031

- Following 375

- Followers 1,906

- Likes 28,943

501 Photos and videos

Florian Buschek retweeted

$AVAV out with a new backpackable UGV:

"""

Designed for mobile exploration, mission-accompanying reconnaissance, explosive threat disposal, and operational support, TOM 50 RE enables dismounted forces, explosive ordnance disposal (EOD) teams, and special operations units—including SWAT—to rapidly deploy robotic capability wherever the mission demands.

The announcement was made at Eurosatory 2026, a global event for defence and security held in Paris.

“The introduction of TOM 50 RE reflects AV’s commitment to delivering robotic systems that directly address the realities of modern ground combat and explosive threat environments,” said Wahid Nawabi, Chairman, President, and Chief Executive Officer of AV. “Today’s operators need systems that move with them, adapt to multiple missions, and provide immediate intelligence while reducing risk to human life. TOM 50 RE delivers that capability in a highly portable form factor built for the tactical edge.”

Weighing less than 10 kilograms (22 pounds) and compact enough to be carried by a single operator, TOM 50 RE enables rapid deployment in confined and complex terrain, while its tracked design, stair-climbing flipper system, and dedicated mobility attachments allow it to overcome obstacles, navigate stairs and uneven terrain, and operate inside structures, delivering up to five hours of endurance and supporting payloads of up to five kilograms without compromising mobility.

With state-of-the-art onboard simultaneous localization and mapping (SLAM) capability, TOM 50 RE autonomously generates detailed maps of interior spaces, including multi-level buildings and global positioning system (GPS)-denied environments such as underground structures and dense urban terrain. Operators can identify and record points of interest directly within the digital map and export mission data immediately following operations, accelerating intelligence exploitation, supporting informed decision-making, and enabling more effective follow-on planning.

Equipped with four integrated high-resolution wide-angle cameras with infrared capability, TOM 50 RE delivers persistent 360-degree situational awareness in day, night, and degraded visual environments. Its advanced internet protocol (IP)-mesh radio architecture provides secure, resilient communications while enabling the system to function as a mobile repeater, extending connectivity for forces operating deep inside structures or complex terrain.

Its modular architecture, enabled by the Mission Module Interface (MMI) or an adapter supporting Telerob’s Universal Component Interface (UCI), allows operators to integrate mission-specific payloads, including advanced camera systems and disruptors, and tailor the system to evolving operational requirements.

“TOM 50 RE was designed to deliver immediate robotic capability at the point of need, where operators face the greatest uncertainty and risk,” said Florian Gruener, Managing Director of Telerob and Product Line General Manager for Uncrewed Ground Vehicles. “Its ability to rapidly conduct these missions in complex terrain allows forces to gain critical situational awareness, mitigate threats, and make faster, more informed decisions—while keeping personnel out of harm’s way.”

Controlled through AV_Halo™ Command running on the Tomahawk Grip family of systems or the Robo Command Control System, operators can seamlessly manage TOM 50 RE alongside other uncrewed systems, enabling coordinated robotic operations and enhancing situational awareness across the mission.

The Four Missions

> For mobile exploration, TOM 50 RE provides immediate situational awareness in unknown or high-risk environments, allowing operators to scout structures, confined spaces, and urban terrain without exposing personnel to danger.

> In mission-accompanying reconnaissance, the system’s integrated simultaneous localization and mapping (SLAM) capability enables it to navigate multi-story buildings, generate detailed interior maps, and identify and mark hazards or points of interest for follow-on forces.

> In defusing missions, TOM 50 RE supports the safe neutralization of improvised explosive devices and explosive hazards through modular disruptor and drop-charge payloads, allowing operators to mitigate threats from a safe distance.

> In its support role, in cooperation with the telemax EVO family of products, the system can serve as a mobile communications relay, extend operational reach, provide additional viewing angles, and enhance coordination between robotic and human elements across distributed teams.

TOM 50 RE expands AV’s portfolio of intelligent, mission-ready ground robotic systems supporting defence, security, and public safety forces worldwide.

"""

1

7

819

🚨$ABVX just quietly dropped new slides again!

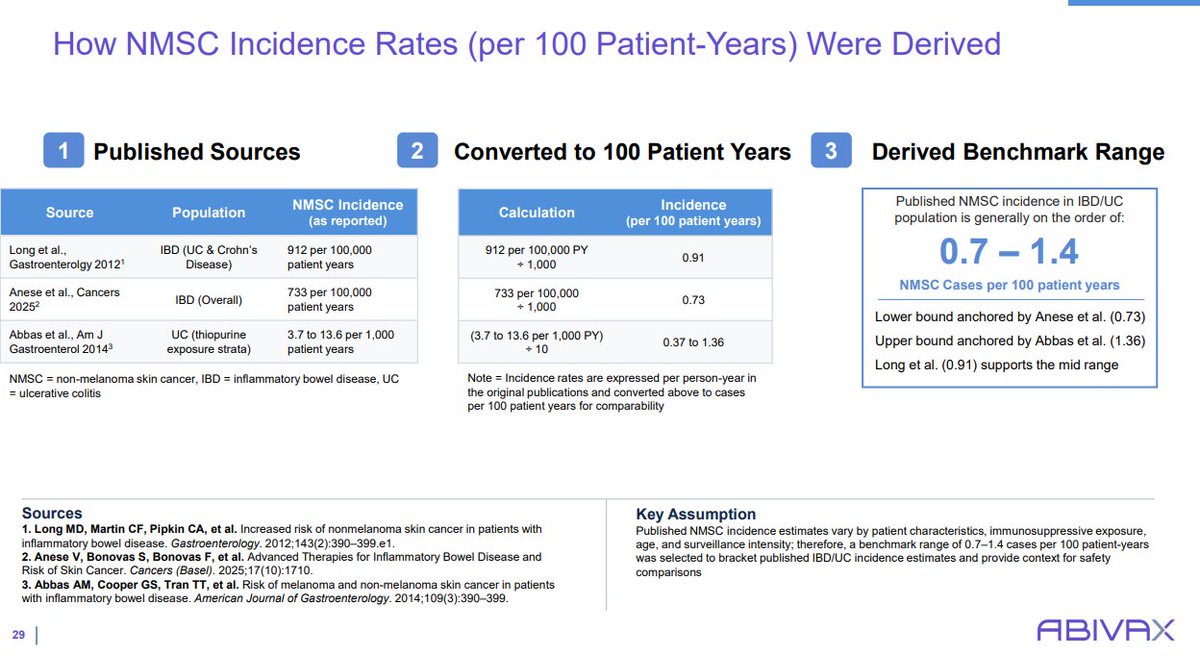

Aside from showing a much better/clearer discussion of data/expectations and a clear goal to handhold the market with the upcoming part 2 dataset, these slides give us another key insight: $ABVX is finding the same expected background nNMSC/NMSC rates as @deathtouch2k and I have discussed.

nNMSC/100PY expected range: 0.3-0.7

↪️Obe's rate so far: ~0.59

NMSC/100PY expected range: 0.7-1.4

↪️Obe's rate so far: ~0.79

And those are just for the 50mg doses...the Obe rates get further diluted massively if you were to include the 25mg dose levels, suggesting that the overall population is likely on the low end of expected cancer incidence. (Note the the calculations can change slightly once we get exact numbers of PY of exposure).

So, even just looking at the 50mg dosing patient years, and not including the Part 2 data that might further reinforce safety, $ABVX is getting the word out that their EXISTING cancer event rates are ALREADY well within EXPECTATIONS...the market is clearly waiting for the Part 2 data before coming to this conclusion...but I personally don't see why we need to wait. These data are very clear.

I continue to see no evidence of a "cancer signal" here, and I find the double digit stock price to be an absolute STEAL. $ABVX would very likely (IMO) have at least temporarily cracked $200/share on their absolutely unprecedented maintenance update without this (bogus?) "cancer scare".

Those of us in the weeds have been able to see that the "cancer scare" was noise from the beginning...the company of course will be slower in reaching the market to get that word out and make people understand it, but IMO that's where we are heading. I would predict that stock price will follow!

22

16

183

25,010

These new $ABVX slides come from an entirely new presentation called "ABTECT Maintenance Part 2 Primer".

Clearly management is going to be doing a much better job of presenting the new data within the appropriate context to show a jumpy market how to appropriately interpret safety data.

This whole mess (and resultingly depressed stock price) could have probably been avoided if they'd done this from the start, but in the end I think the final result (and much healthier stock price) will still be the same.

This time in between where we find ourselves now is what I'd call "opportunity".

4

3

52

5,617

Florian Buschek retweeted

$TRIP Tripadvisor is selling TheFork to American Express for $700M cash. At a ~$1.4B market cap, that is almost half the current equity value being unlocked from an asset the market was clearly not giving full credit for inside the consolidated company.

This is exactly why I, following @FBuschek's lead about a month ago, bought $TRIP as a special situation.

The Fork did roughly $232M LTM revenue and $28M adjusted EBITDA, so AMEX is paying about 3x revenue / 25x EBITDA. That is a very credible strategic valuation. Even more important: the company expects minimal tax leakage, meaning net proceeds should be close to gross proceeds.

The question now becomes capital allocation. If $TRIP uses the proceeds for a large buyback at these levels, the math gets very interesting quickly. $700M of proceeds against a ~$1.4B market cap is not a small lever. It is a balance-sheet event.

I still don’t think this is a clean compounder. Legacy Tripadvisor has real issues. AI search disruption is real. Viator needs to prove the March weakness was temporary. And management has to prove it will use proceeds intelligently.

But the bear case that “there is no hidden value here” just took a major hit. To me, this moves $TRIP from “interesting activist/SOTP idea” to “validated special situation with a clear next catalyst.”

I am not selling the pre-market pop just because the first asset sale got announced. I want to see what they do with the cash. Base case still looks like mid-to-high teens if proceeds are used well and Viator stabilizes. Bull case is higher if this is the first step in a broader simplification - breakup - sale process.

Disclosure: I am long $TRIP and may add, reduce, or sell at any time without notice. Not investment advice. Do your own work. Small caps and special situations are volatile and can be illiquid.

2

6

4,470

$TRIP TripAdvisor is selling TheFork, its online restaurant reservation and mgmt. platform in Europe, to AXP (American Express) for $700MM in cash ($700MM is about 50% of TRIP’s entire market cap).

1

1

2,244

Florian Buschek retweeted

$TRIP TripAdvisor is selling TheFork, its online restaurant reservation and mgmt. platform in Europe, to AXP (American Express) for $700MM in cash ($700MM is about 50% of TRIP’s entire market cap).

1

5

1,373

Florian Buschek retweeted

Jun 13

Great call

Looks like sentiment is changing pretty quickly on this one

Its still extremely cheap relative to other names tied to mega-infra, nuclear, and data centers

Plus has idiosyncratic value drivers with what is happening with their M&A

$DRX.TO

Apr 21

I recently bought $DRX.TO - ADF Group, a Canadian fabricator of complex structural steel. They have 2 fabrication facilities in Quebec and 1 in Montana.

The stock recently sold off on near-term margin noise tied to steel tariffs and their LAR acquisition, creating what I think is a really good entry point

Why It's exciting:

1. Trades under 4x depressed EBITDA with a clean net cash balance sheet

2. Backlog has more than doubled in a year from $300m to $650M , with strong bidding activity continuing.

3. Beneficiary of the "Build Canada" Thematic

4. A recent acquisition I believe will look like a no-brainer in hindsight

ADF is one of the best-positioned names to play the 'Build Canada' theme. They stand to benefit from a wave of infrastructure spend: airports, Ontario nuclear, hydro expansion in Quebec, BC, and Newfoundland, and energy/industrial buildout in the west. A "Buy Canadian" mandate further improves their competitive position and will spur industria/constructionl projects

Historically, they were 90% US, 10% Canada. However, with last year's tariffs, the company has aggressively pivoted its backlog which now sits at 60% Canadian and 40% US with a good chunk of the work segregated between the two countries. I expect Canada to make-up a bigger percentage of the mix overtime.

The most exciting part of the story is the LAR Group acquisition. Historically, ADF Group did primarily industrial & commercial projects. Think airports, warehouses, bridges and some industrial plants. LAR was a distressed, over-levered steel fabricator for the hydro sector. A specific contract blew them up and ADF stepped in as the white knight through a reverse vesting order approved by the government. It allowed them to acquire LAR's assets while having all liabilities extinguished, BUT keeping all certifications intact.

ADF is now certified to operate in both the hydro AND nuclear markets two of the most infrastructure-intensive sectors in Canada's near-term pipeline, in addition to potentially bidding for some of the big 'nation-building' projects the Canadian government has proposed.

The near-term overhang: LAR is working through a tail of low-margin legacy projects, which weighed on Q4 results. LAR currently runs ~10% gross margins vs. ADF's mid-20s. Management doesn't expect margins to deteriorate further from here, but the meaningful inflection only comes in H2 2026 and into 2027, as ADF deploys ~$35M to automate LAR's facilities. LAR is understood to be the preferred vendor for virtually all Hydro-Québec projects and so I expect more work to come their way. And let's not forget the government of Quebec approved the CCAA proceeding at record speed. Clearly Hydro-Quebec was pretty desperate to have ADF acquire LAR group as there aren't many companies capable of doing that type of work.

The second near-term overhang is the recent US steel tariff changes which puts a 10% tariff on the total value of steel transformed outside of US, but that uses US Steel. For some jobs, it made economical sense to ship US steel to Terrebonne and then ship it. It will impact their Q1/Q2 results, which caused last week's sell-off.

The market is focused on near-term headwinds but It's missing the forest for the trees.

Canada is entering one of the largest infrastructure build cycles in its history and ADF is one of a handful of Canadian companies capable of fabricating the complex steel structures these projects demand:

=> Hydro-Québec: $35–45B capex plan over the next decade

=> BC Hydro: $36B in regional investments over the next decade

=> Ontario & Atlantic provinces ramping hydro capacity

=> Ontario nuclear: plant refurbishments, SMRs, and Bruce Power expansion

And none of that includes the 15 'nation-building' projects the federal government has fast-tracked or the hundred of projects that will emerge from Canada's defense spend goal of 5% of GDP.

Despite the headwinds, the company expects to have stable gross margin, with a much bigger revenue number. There is a clear path here for the company to achieve 15% EBITDA margin on potentially over $500m of revenue which would get me to a target price of $17 at 6x EBITDA over the next 2-3 years.

2

3

16

3,224

Florian Buschek retweeted

Still think $CBR.V offers one of the best R/Rs around when measured over the next 12-24 months. Hard to see much downside even if gold pukes.

1

2

8

2,183

Florian Buschek retweeted

Jun 14

If Comrade Balding wants to influence the debate (and not just provide snark from the peanut gallery) he might try writing a few white papers of his own. As it stands he is sitting on the sidelines & missing an important evolution in how Europe is thinking about China.

2/2

1

3

22

5,199

Florian Buschek retweeted

Jun 14

14

21

193

31,499

100% this would a seriously unstoppable combination. Once daily oral combination WITH NO INITIATION LABS (*all* other IL-23s of non-optional TB screening requirement). People severely severely severely underestimate the significance of NO INITIATION LABS. You can sample these patients in office and have them take their first dose in the parking lot. Labs are not just an extra (unpaid) hassle for prescribers but also delay treatment initiation. EVERYTHING else requires labs and/or IV infusion clinic scheduling to get started.

JNJ can buy $ABVX and absolutely dominate IBD ($ABBV should be very scared if $JNJ pulls this off) or they can let their next big drug (Icotyde) be dominated by obefazimod in IBD. 180 turn either way they choose to go.

I see absolutely *zero* scenario where icotyde monotherapy efficacy even approaches $ABVX obefazimod efficacy - at least in maintenance.

Idk if JNJ is the most *likely* buyer of $ABVX, but I have zero doubt that JNJ makes the most strategic sense. Just my 2 cents

8

7

136

28,525

Florian Buschek retweeted

Jun 11

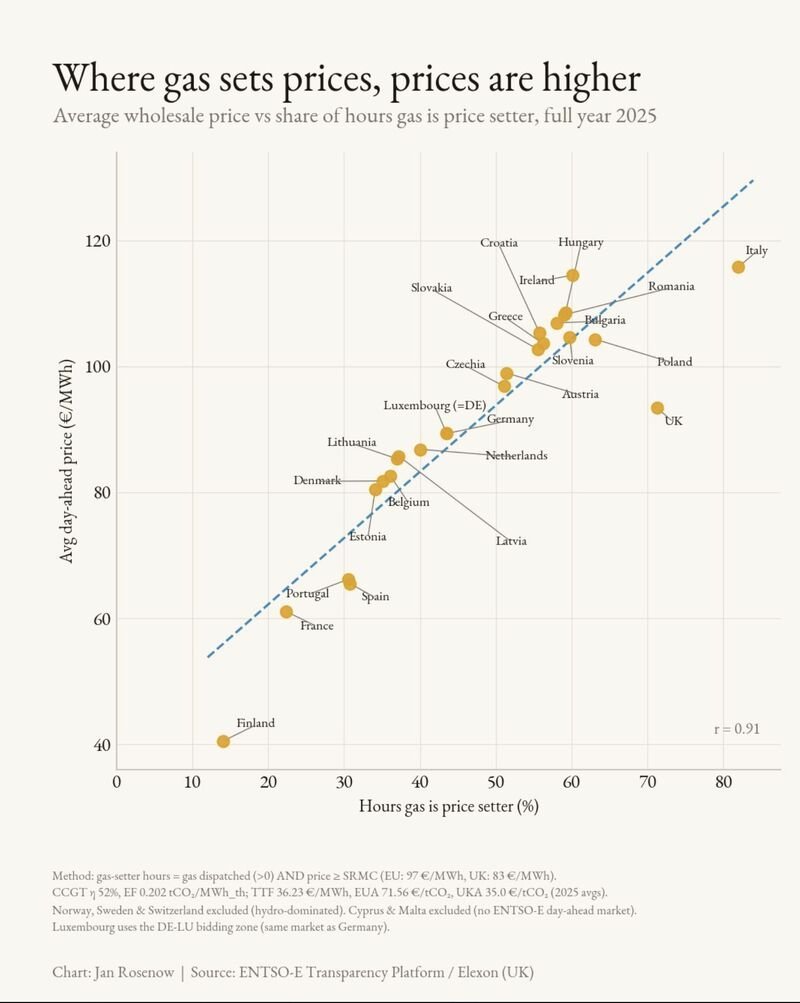

🇪🇺"Do renewables make power cheaper or more expensive?"

Wrong debate.

the below chart settles what actually drives European electricity prices and it isn't the share of wind and solar.

It's how often GAS sets the price.

🔸How pricing works?

in power markets, the most expensive plant needed in any hour sets the price for EVERYONE in that hour even if 80% of supply is cheap wind, hydro or nuclear.

So the question isn't "how much gas do you burn?" It's "how many hours is gas the marginal unit?"

The spread is brutal:

Finland: gas sets the price 14% of hours → €40/MWh.

Italy: gas sets the price 82% of hours → €116/MWh.

Nearly 3x the price, on the same continent, in the same year.

Note the outliers UK and Poland pay less than their gas-hours suggest.

And the broader finding is that more renewables shows NO clear effect on retail prices, but meaningfully LOWER industrial prices.

Renewables don't cut prices by existing they cut prices by pushing gas off the margin.

19

71

193

24,105

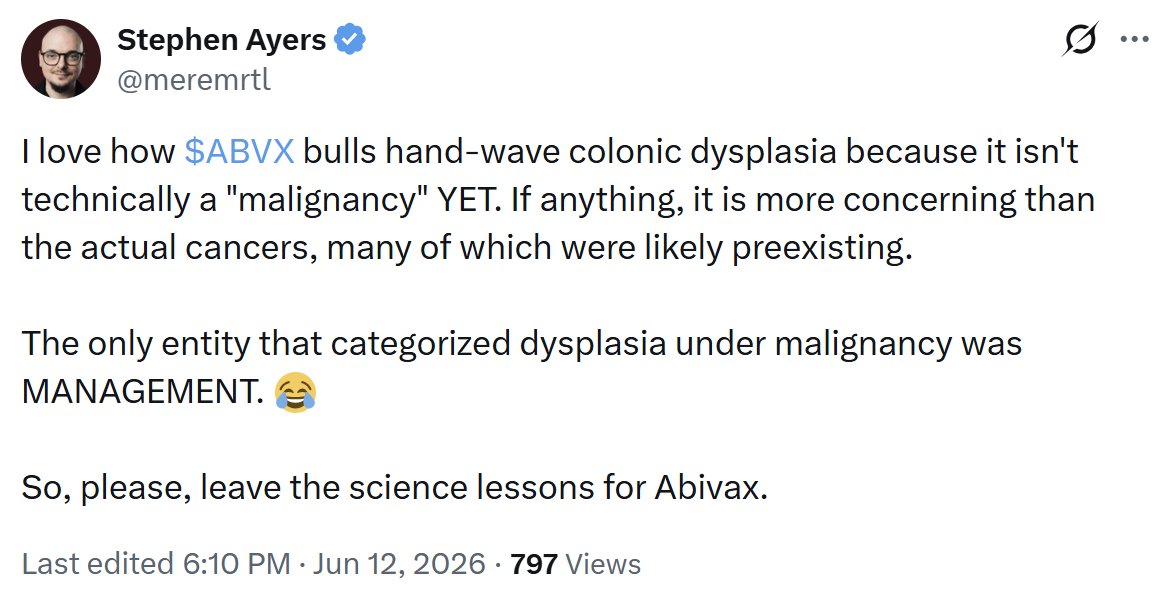

I'd respond to @meremrtl in his post directly, but he blocked me for politely disagreeing with him on $NKTR. There's something VERY important that he is VERY wrong about that I'd like to highlight.

It's funny that he recognizes that the 2 solid tumor cases in the $ABVX trial are mere bad luck/noise. I agree with him that the latency argument for solid tumors argues that these cancers pre-dated the $ABVX study given that they were slow-growing cancer types identified far too early (6-8 months) to be due to $ABVX's drug. These are the cases the market has been freaking out about, so...good to see you're an $ABVX bull, Stephen!

Now the point he is making about colonic dysplasia is very, very (very very very) stupid. He is trying to say that the single case of colonic dysplasia is the worrisome finding in the $ABVX study. I'll provide data to show you that his take is objectively stupid, so that he doesn't whine about me saying so. I'm not being mean - I'm calling a spade a spade, and of course very smart people can make very stupid points sometimes😉

There was 1 case of colonic dysplasia in the entire P2-P3 program for $ABVX.

In P3 we have ~310 patient years of exposure across arms (388 patients x ~80% 1 year completion rate). In reality 310 is a slight underestimate as we don't know when the other 20% discontinued, but it wasn't day 0. Still, let's be conservative.

In P2, we have ~130 patients treated across 5-7 years in the long term open label extension. Let's be overly conservative here too, and say 100 patients for 5 years = 500 more patient years.

So, very conservatively, we have ~810 patient years of obefazimod exposure.

1 case of colonic dysplasia. 810PY. That makes the colonic dysplasia event rate 0.12/100 Patient-Years on Obefazimod so far.

What Stephen (very very stupidly) fails to ask is: "What is the expected rate of colonic dysplasia in this patient population at baseline?".

The answer is ~1.77/100PY. ~15x higher than what $ABVX is showing.

Yeah, the expected background rate of colonic dysplasia in this population (long-term UC patients with median age in the 40s) is ~1.77/100PY, FIFTEEN TIMES HIGHER THAN WHAT IS BEING SEEN IN THE $ABVX TRIALS.

Colonic dysplasia is actually a relatively common (nonmalignant) event in general, but it is especially common in ulcerative colitis patients because their chronically inflamed colons are at a high risk of accumulating DNA mutations and immune dysfunction that leads to carcinogenesis.

What we are seeing in the $ABVX trials is actually a DRAMATICALLY lower than expected rate of colonic dysplasia, which is suggestive of A DECREASED RISK OF COLONIC DYSPLASIA AND COLON CANCER due to high levels of disease control.

Really, it's very simple...UC patients have a high risk of colon dysplasia/cancer because their colons are so severely inflamed...$ABVX's obefazimod stops that inflammation, LOWERING their risk of developing it. Not only is this mechanistically supported...the DATA support it as well.

What Stephen is highlighting as the big scary AE for $ABVX is actually an objective POSITIVE for the company if you have the brain and objectivity to analyze the data. However, some people (like Stephen) are just here to stir the pot! Oh well. The data are very clear, and they are bullish for $ABVX.

But hey, even Stephen signed off on the "real cancers" as not being a concern! Maybe he is coming around to be an $ABVX bull himself!

Source data: journals.lww.com/ajg/fulltex…

28

8

183

54,512

$ABVX

1) random chance

2) the placebo arm had ~half the adverse event capture of the drug arm because 2/3s of the placebo arm patients quit the study early (and thus were no longer surveilled for cancer).

Factoring in point 2 makes point 1 even more clear cut. If you double the capture of the placebo arm you would (by simulation obviously) turn 1 case into 2. Now it’s a 2:1 random chance skew instead of 4:1.

2

2

71

10,467

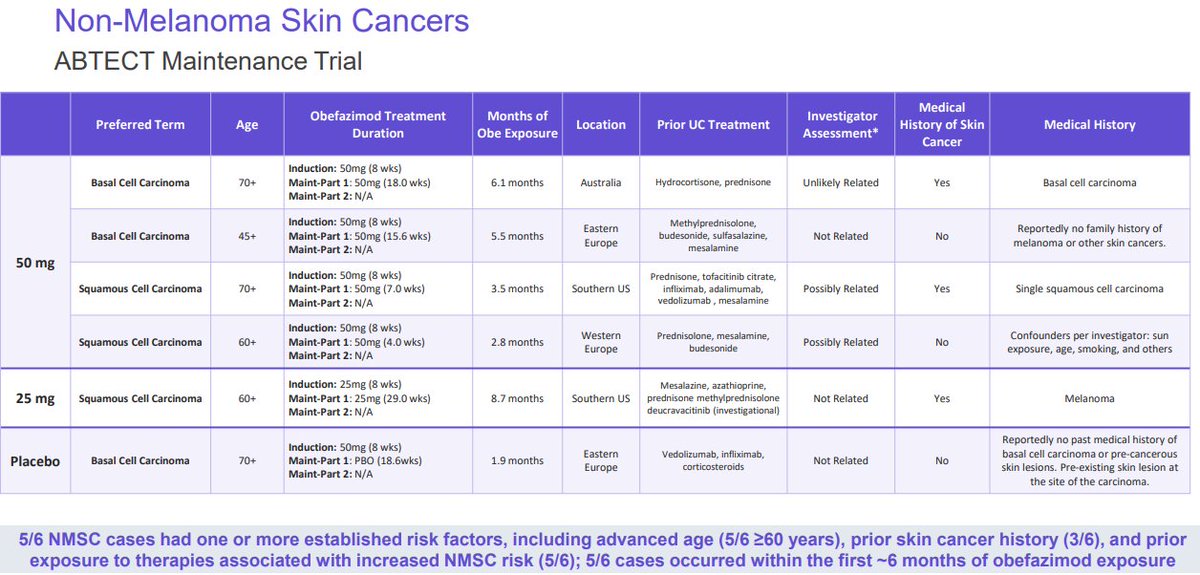

$ABVX seems to have (in the last hour or so?) quietly released a new corporate deck with 3 important slides at the end. All, in my opinion, providing strong new information showing that these cancer cases were unrelated to drug and equivalent to expected background noise.

Most important is the slide on the 2 non-nonmelanoma skin cancers. BOTH of these were more indolent, low/intermediate subtypes of their respective cancer (prostate and breast). Not only does this mean that the cancers are less threatening, it also means that THEY ARE SLOWER GROWING CANCERS. Why is this particularly important? Because it means that the development of the cancers very (very) likely PREDATES THEIR ENROLLMENT IN THE TRIAL. Look into the doubling times of grade 2 (Gleason 7) prostate cancer and grade 2 NST breast carcinoma. These are slow-growing tumors that very likely existed before these patients ever even had a dose of obefazimod.

That relates to another key finding on this slide - the prostate cancer case was identified via PSA screening at 8.5 months into the study (remember earlier is better). In the Guggenheim conference they had said it was confirmed at day 367...they must have been referring to the biopsy confirmation of the subtype, not PSA confirmation of the prostate cancer diagnosis. This new information speaks to an earlier diagnosis. The breast cancer patient was diagnosed even earlier than that! Only 6.8 months of Obe exposure.

Also, these new slides give us actual information on the prior drug exposures - before this afternoon we knew that they were on some prior treatments, but we didn't know what...THE PROSTATE CANCER WAS PREVIOUSLY EXPOSED TO ***5*** DRUGS WITH LABELED CANCER WARNINGS BEFORE ENROLLING IN THE STUDY! 3 OF THEM HAD ***BLACK BOX WARNINGS*** FOR CANCER RISK!

-Humira (black box)

-Infliximab (black box)

-Rinvoq (black box)

-Entyvio (warnings and precautions)

-Stelara (warnings and precautions)

We also just got new info on the NMSC cases (which matter far less but which spooked the market anyway).

How you can look at the details of these skin cancer cases and think they are related to the drug is beyond me (but then again, these details just got released - quietly, for some reason).

First of all, ***ALL OF THE 4 50MG CASES OF NMSC OCCURED IN 6 MONTHS OR LESS!!! Again, too rapid to be reasonably assumed drug-related. The fact that they all happened in the first half of this study is actually extremely exculpating evidence for $ABVX.

Other details:

-4/5 were 60 years old (STRONGLY associated with skin cancer risk)

-3/5 had PRIOR SKIN CANCER ALREADY(!!!!!)

-4/5 had prior exposure to other drugs that are known to increase skin cancer risk.

Finally, they also added a slide discussing that some studies have shown the elevated risks of these cancers for UC patients at baseline.

-~5x higher risk of prostate cancer in IBD patients

-~2x higher risk of breast cancer in IBD patients

Why did $ABVX add these 3 slides to the corporate deck randomly, silently, on a Friday afternoon? IDK. Legitimately good news in those slides! I'd have pressed released this info as soon as I had it, because the details really help alleviate the (already statistically misguided) concern that these cancers could've been caused by Obefazimod.

Here's the link: ir.abivax.com/static-files/e…

30

33

281

82,274

Florian Buschek retweeted

$NOW.V I was surprised by this too this morning. We will likely know more next week. I hope the company updates the market in more detail.

app.tracktacle.com/publicati…

1

1

15

3,424

Florian Buschek retweeted

Jun 11

Another solid pod from @JackFarley96, this one focused on energy supply with Kepler’s Matt Smith.

The big question: given the epic supply disruption, why isn’t crude higher? There are a bunch of factors here (US supply, decreased demand from China, among them).

But what if crude isn’t higher because of Trump? Getting too long risks being on the wrong side of a tweet that’s good for a 5% (or greater) rally. Jack suggests that Trump has imposed sort of a forward guidance impact on prices. It’s clear he’s looking for the off-ramp and that’s likely on the price.

Here’s the problem that I see: The lack of signal from price removes the urgency to end the conflict. If crude were at 150 and a gallon of gas at 7, the onslaught of media coverage and, perhaps, an even worse expected outcome for the Republicans at the midterms would motivate de-escalatory action. But gas is down 43 cents from the peak.

The “oil vigilantes” can’t motivate Trump via price because he himself can cause these same prices to reverse via a single tweet. If they run up too much, he panics and imposes a rally.

The issue, however, as Matt Smith does a great job of walking through, is that time is the enemy. Price isn’t telling us about the fast worsening supply backdrop. But fast worsening it is.

It’s framed as potentially “sleepwalking into a crisis”.

This isn’t a perfect analogue at all, but monetary policymakers and IMF types epically misread a VIX of 10 in 2006 as a sign of safety and resilience in the system, rather than the opposite.

Is today’s lower than expected level of crude vulnerable to a similar misread? It certainly dissuades action from Trump. Crude vol - way down from its peak - similar disregards the potential for a spike in prices.

podcasts.apple.com/us/podcas…

5

23

4,988

Florian Buschek retweeted

Jun 11

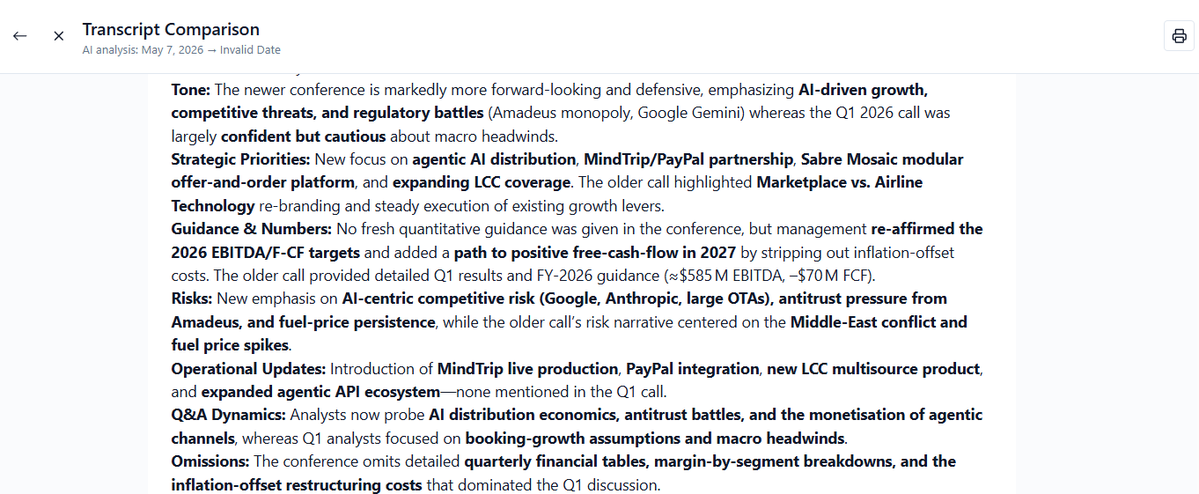

1/12 $SABR | Q1 2026 Call vs BofA TMT Conference

We broke down exactly how Sabre’s corporate narrative shifted across the 7 distinct sections of our latest Tracktacle transcript comparison. Let's walk through the exact changes section by section.

app.tracktacle.com/publicati…

1

3

10

1,481