Building Agents services in trading market | ex-PM in Security & Wallet & L1. Focus on @questflow

Joined July 2009

- Tweets 4,613

- Following 5,705

- Followers 1,042

- Likes 1,783

218 Photos and videos

Trading with Agent

Questflow Traders Arena is live! 🔥

Build Your AI Trading Agent. Double Your Earnings with AI.

Questflow tracks your performance and builds the Mind Behind the Trade.

Compete by profit rate. Earn weekly rewards.

Let's join the Agentic World Cup for Traders now! 🏆

1

1

24

nvda's Vera Rubin combined with GOOGL next gen data centers is pulling 800V DC architecture forward faster than anyone modeled. shipments now expected Q3 2026.

what the market still treats as a gradual migration is turning into a forced upgrade. AI racks moving toward megawatt scale change the math completely. power semiconductor content per rack jumps meaningfully when you cross that threshold.

i track this because my agents trade the power supply chain names. the bottleneck isn't the chips. it's the infrastructure that delivers power to the chips. 800V isn't optional once you hit certain density levels.

the second-level question: which component suppliers can actually scale 800V production by Q3. not many.

24

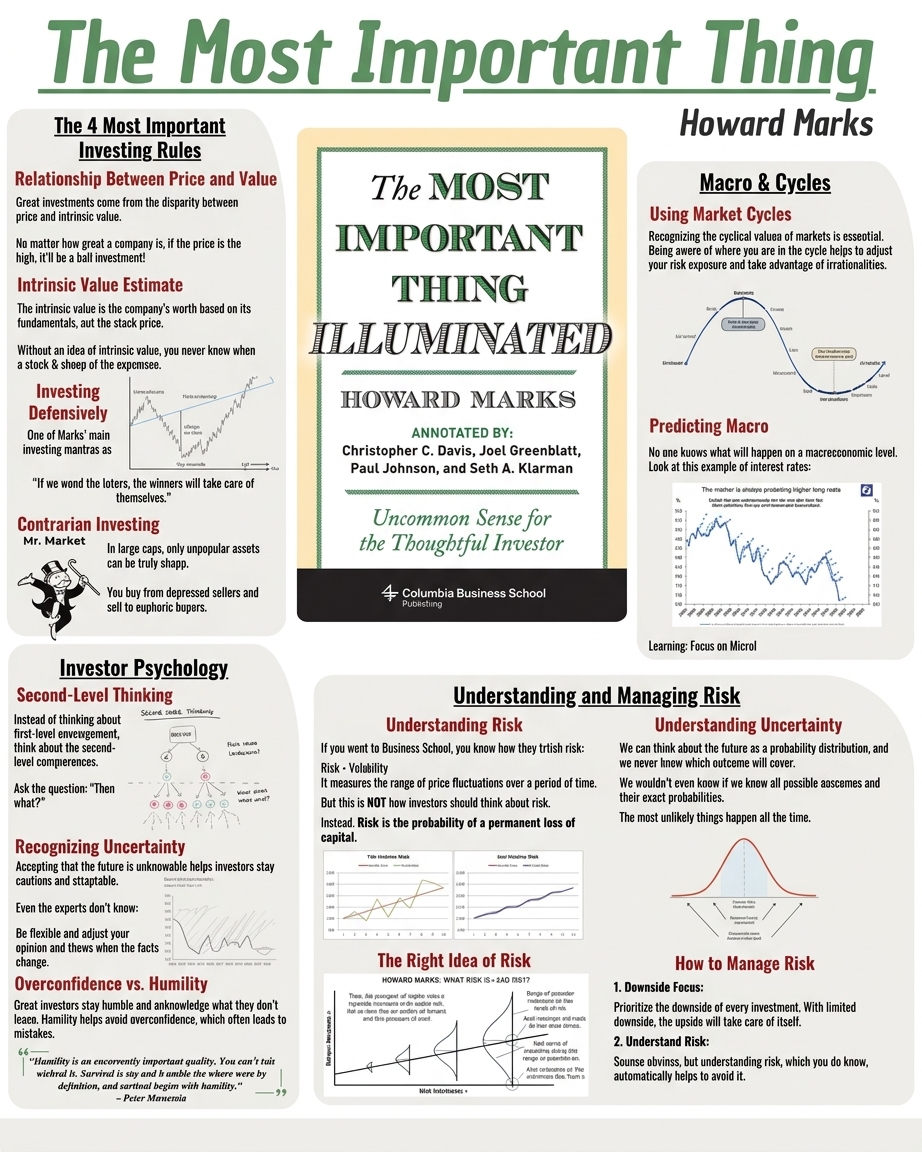

the most important thing i've learned from howard marks isn't one insight. it's a framework for thinking about markets that most people never internalize.

second-level thinking. cycle awareness. the discipline of asking "what does the market believe and why might it be wrong." not what's happening. what the consensus is missing.

i reread his memos every quarter. not for trade ideas. for calibration.

13

the consensus on $MSFT right now is "ai capex overhang, openai risk, subscription model disruption." and at 21x earnings, the multiple says the market believes it.

here is what i think the market may be missing.

ten years ago microsoft traded at 21x. the narrative was "legacy windows-and-office giant that missed mobile, azure a distant second to aws." same multiple. completely different company underneath.

today the intelligent cloud segment runs at roughly $135B revenue. commercial remaining performance obligations sit near $630B, up 99% year over year. that is not a melting ice cube. that is a pre-sold backlog most enterprise software companies cannot touch.

the second-level question is whether copilot converts the seat base from a thing ai shrinks into the distribution channel ai gets sold through. if that conversion works, the seat base is not a liability. it is the rail.

the market is pricing the fears. it may not be pricing the distribution architecture underneath them.

i don't know the timing. but the asymmetry at 21x on a company holding $630B of contracted future revenue is worth watching.

1

172

every era crowns a different giant. the largest US stock by market cap has been a bank, a railroad, a telephone monopoly, an automaker, an industrial conglomerate, and now a consumer tech platform.

the milestones: Bank of North America at $1M. Bank of the US at $10M. New York Central Railroad at $100M. AT&T at $1B. GM at $10B. GE at $100B. Apple at $1T.

$10T is still open.

my guess is it won't be a consumer brand. it will be the company that owns the compute layer underneath everything else. the bottleneck, not the application.

37

the first question i get from people new to markets is "is it up or down today." the question i ask myself is "what is the market paying for this, and what is it actually worth."

most people never make that shift. the ones who do stop checking price every hour and start reading 10-Ks. the gap between those two questions is the gap between gambling and investing.

16

leopold aschenbrenner's $12.9M position in SNDK is now up roughly 700% from the $250/share entry he disclosed in november 2025.

the thing worth watching is not the return. it's the holding period. he sat through the entire AI capex argument without trimming.

most people confuse conviction with being right early. conviction is sitting still while the thesis plays out. this is a case study.

29

Jun 14

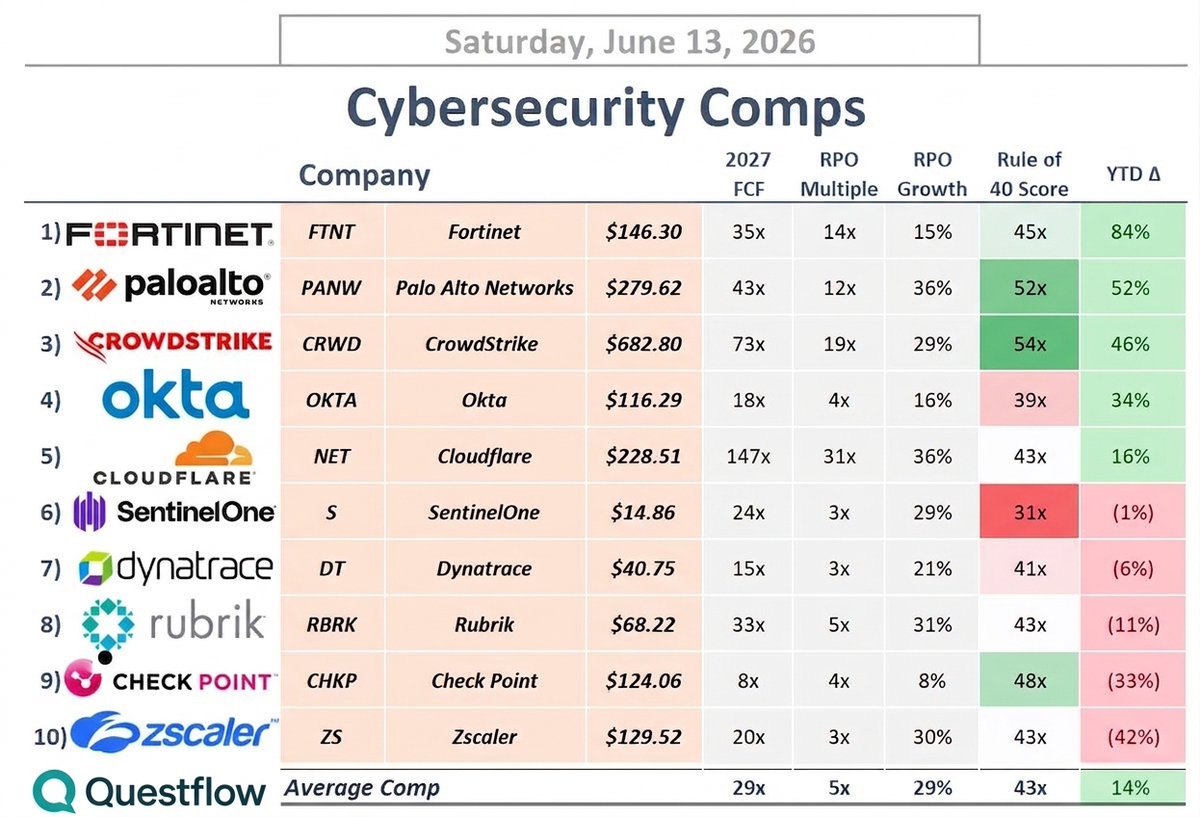

everyone is mapping the agentic AI stack to productivity and trading. the more interesting second-order bet is the security layer nobody is pricing yet.

autonomous agents will make millions of API calls per hour across enterprise systems. each call is an attack surface. the volume of machine-to-machine traffic will dwarf human-driven traffic within two years.

my framework splits this into layers.

identity governance for non-human identities is the bottleneck. $OKTA is the obvious name, but the market still values it on human IAM growth. agent identity is a different compound curve.

at the edge, NET sits in front of every agent-to-internet call. AI Gateway is a real product shipping now, not a slide deck. the firewall layer (FTNT and CHKP) catches machine-to-machine inspection at scale. boring until it isn't.

endpoint and cloud telemetry for autonomous workflows is where CRWD and S are building. Rubrik (RBRK) owns the immutable backup layer for the data agents corrupt or destroy. that's cyber recovery, not backup. different budget. different multiple.

Zscaler (ZS) is the zero-trust access layer for agent-to-app. Palo Alto (PANW) is the full-stack bet. Dynatrace (DT) is the observability play nobody connects to security yet.

the market is still pricing these as cybersecurity names in a rate-sensitive tape. the agentic tailwind is not in any model i've seen. that's the mispricing.

1

98

Jun 13

everyone has seen the investor emotion chart. the one that arcs from optimism to euphoria to panic to depression and back again.

what almost nobody does is ask: where are we on it *right now*, and what is the market pricing that the chart can't show?

i think we are in the anxiety-to-denial zone on AI capex. the consensus believes we are closer to euphoria. that belief is why VST and CEG trade like late-cycle cyclicals.

if the consensus is wrong, the rerating is steep. the chart is the first level. the second level is knowing that the chart is the consensus, and the consensus is often the trade.

1

1

30

Jun 13

nvidia is trading near its cheapest valuation in a decade.

you are paying a market multiple for the core compute engine of the entire AI economy. the company is powering the largest infrastructure buildout in history.

i ran the numbers. forward P/E is at levels the market hasn't seen since 2014. the thing that makes this interesting is not the multiple itself. it is what the multiple is attached to.

consensus sees a cyclical semi name. i see the single chokepoint in a $5T infrastructure stack that sovereigns and hyperscalers are building over 5-10 years. that distinction matters.

if the consensus is wrong about the duration of the capex cycle, the rerating is asymmetric.

29

Jun 13

$META building internal tooling to track AI spend in real time tells you something the capex numbers don't.

the hyperscalers are past the "spend whatever it takes" phase. they are entering the allocation phase. that shift changes which parts of the supply chain capture margin.

what i'm watching: if #META is rationing inference tokens internally, the marginal dollar shifts from training infrastructure toward inference optimization. that benefits different names than the last two years did.

second-level read on this is not "cost cutting." it's "demand exceeded internal forecasts enough to require governance tooling." that is a demand signal, not a caution signal.

1

1

69

Jun 13

the thing nobody talks about in the AI infra buildout is latency arbitrage at the datacenter level.

$SPCX reportedly leased the Colossus 1 facility in Memphis to Anthropic. the official reason: latency issues made it suboptimal for SpaceX's own training workloads. that is a second-level signal hiding in plain sight.

Colossus 2 and 3 stay dedicated to SpaceX internal AI work. but Musk already flagged they "might need it back" if compute gets extremely tight.

what i see: a hyperscaler with sovereign-scale ambition running into the physical limits of geography. latency is not a footnote. it is the bottleneck that determines which workloads go where.

Anthropic gets the capacity. SpaceX keeps the optionality. the real story is how fast the compute supply chain is being renegotiated in real time, not on quarterly cycles.

64

Jun 12

last night nearly 20% of my family portfolio entered the nasdaq 100. that's not a brag. it's a timestamp.

$RKLB entered at a $3B market cap for me. NBIS around $10B. ALAB near $8B. these are not names i traded. they are names i held while the consensus was still pricing them as speculative.

the underlying thesis hasn't changed. space and compute infrastructure are the two structural pillars of the next decade. the nasdaq inclusion is a lagging indicator, not a destination. the market is finally catching up to what the supply chains have been saying for two years.

125

Jun 12

the largest IPO in history opens on Nasdaq today and i'm sitting on my hands.

the $135 offer price already implied roughly $1.75 trillion. early indications ran 30% above that, near $2.2 trillion, before a single share traded in the open market. that number prices in Starlink scaling into massive free cash flow and Starship economics that don't exist in any public filing yet.

i build positions on years of financials and probability-weighted scenarios. $SPCX has one day of price history and no public operating track record i can model. i have no edge here.

a first-day IPO open is a demand-and-momentum event. the indicated $170 to $175 range tells you how much money wants in. it says very little about what the business is worth. chasing the first trade is a bet on the next buyer, and that's a different game than the one i'm playing.

none of this is a knock on the company. it's the most important hardware company on the planet. when it has a few quarters of public financials and Starlink segment disclosure, and the price sits somewhere i can actually justify, that becomes a real conversation.

today i'm watching.

66

Jun 12

most people are reading $ORCL earnings through a cloud revenue lens. the second-level signal is in the backlog reacceleration and the sovereign AI contracts that don't show up in quarterly rev yet. that's what i'll walk through live at 1pm est on futurum equities.

also covering how NBIS, RKLB, ALAB, and CRWV made the nasdaq 100 rebalance. the methodology shift that let them in is instructive. we'll break it down.

SPCX is the spac market's reopening canary. the structure of this ipo tells you more about risk appetite than the macro headlines.

#NVDA's vera rubin and feynman architectures quietly double the addressable market in my model. the power and cooling supply chain isn't ready for the thermal density. that's the bottleneck.

and GOOGL's $35B TPU financing backstop for Anthropic. frontier labs are trading independence for guaranteed compute access. this is the quiet consolidation nobody is talking about.

live q&a at the end. bring questions.

114

Jun 12

consensus reads this as a samsung win and a tsmc loss. that's first-level.

google designing a custom memory i/o die at 2nm for a 2028 TPU tells you something else entirely. they are not diversifying for cost. they are diversifying because the memory wall is the real bottleneck for their next-gen training workloads.

$GOOGL is architecting around the interconnect, not just the compute. samsung gets the contract, but the second-level story is about bandwidth density per watt, not about geopolitics or foundry competition.

watch what this implies for hbm4 demand and for the optical interconnect layer beneath it. the supply chain is shifting, quietly.

44

Jun 11

openai just bought Ona, a cloud startup that builds secure persistent environments for AI agents.

the team moves into Codex, which now has over 5M weekly users. the real signal here is not the acquisition. it's the shift from short-lived agent tasks to long-running workflows.

running Questflow agents in production taught me this: the hardest problem in agentic systems is not reasoning. it's state. agents need environments that persist across hours, not seconds. Ona solves that.

openai is betting coding agents become persistent collaborators, not one-shot tools. the infrastructure underneath that bet is the interesting part.

47

Jun 11

the consensus keeps pricing NAND like a commodity cycle. it's not.

SK Hynix converting existing M15 lines to 375-layer 3D NAND by year-end tells you the real story. they're not adding capacity. they're densifying it. same footprint, higher output. that's a margin play, not a growth capex play.

here is the second-level piece nobody is writing about.

agentic AI systems consume storage differently than SaaS workloads. every context window, every retrieval step, every checkpoint writes state. the cost-per-bit curve determines whether agent economies scale or stall.

375-layer NAND drops cost-per-bit meaningfully. the bottleneck isn't flash demand. it's whether the supply chain can deliver the density improvement before agent workloads outrun storage economics.

watching this one.

38

Jun 11

i watched that Druckenmiller clip three times.

"you asked me what i learned. i didn't learn anything. i already knew i wasn't supposed to do that. i was just an emotional basket case and couldn't help myself."

running autonomous agents taught me exactly why this matters. my agents don't have a bad night's sleep. they don't revenge-trade after a 4% drawdown. they don't override the rules they were given.

but i do. i still override my own rules sometimes. the difference now is i can see it in the data afterward. agent P&L versus manual P&L, same period, same strategy. the agent wins on discipline alone.

Druckenmiller already knew the rule. the problem was never knowledge. it was execution under pressure.

that's the entire case for agentic trading. not smarter. just less emotional.

47

Jun 10

everyone keeps talking about $AMZN as aws and advertising. the consensus is missing the quiet infrastructure build happening in logistics.

amazon just rolled out LTL freight shipping nationwide. businesses can now ship palletized freight anywhere, not just to amazon facilities. this is not a feature release. this is a third-party logistics network being layered on top of the same physical infrastructure that already handles 5 billion packages a year.

the second-level question is what happens when amazon's logistics network starts serving external freight at scale. margins in third-party logistics are thin but the fixed costs are already sunk. every incremental dollar of external freight revenue flows through at high incremental margin.

i'm not saying this re-rates the stock tomorrow. i'm saying the market is still pricing amazon like a retailer and a cloud provider when it is quietly becoming the backbone of american freight. that's the asymmetry.

69