Joined November 2019

- Tweets 1,605

- Following 84

- Followers 472

- Likes 882

340 Photos and videos

Pinned Tweet

Apr 12

Everyone's buying the F&G dip blindly while ignoring which tokens actually deserve capital at these levels.

I scored 25 tokens across 7 categories. Some consensus darlings scored poorly. Some "boring" picks came out on top.

Results 🧵

2

1

73

Apr 12

Everyone's buying the F&G dip blindly while ignoring which tokens actually deserve capital at these levels.

I scored 25 tokens across 7 categories. Some consensus darlings scored poorly. Some "boring" picks came out on top.

Results 🧵

2

1

73

Apr 12

One name I'd look at twice: NEAR at 72.5.

Co-founder literally co-authored the Transformer paper (yes, that one). Chain abstraction AI narrative at $2.5B MCap. FDV/MCap = 1.0.

Not calling it undervalued. But the team credential alone warrants attention.

1

1

32

Apr 12

Which token should I deep-dive next? Drop suggestions 👇

Follow @TraderWorst for data-backed analysis.

19

Mar 20

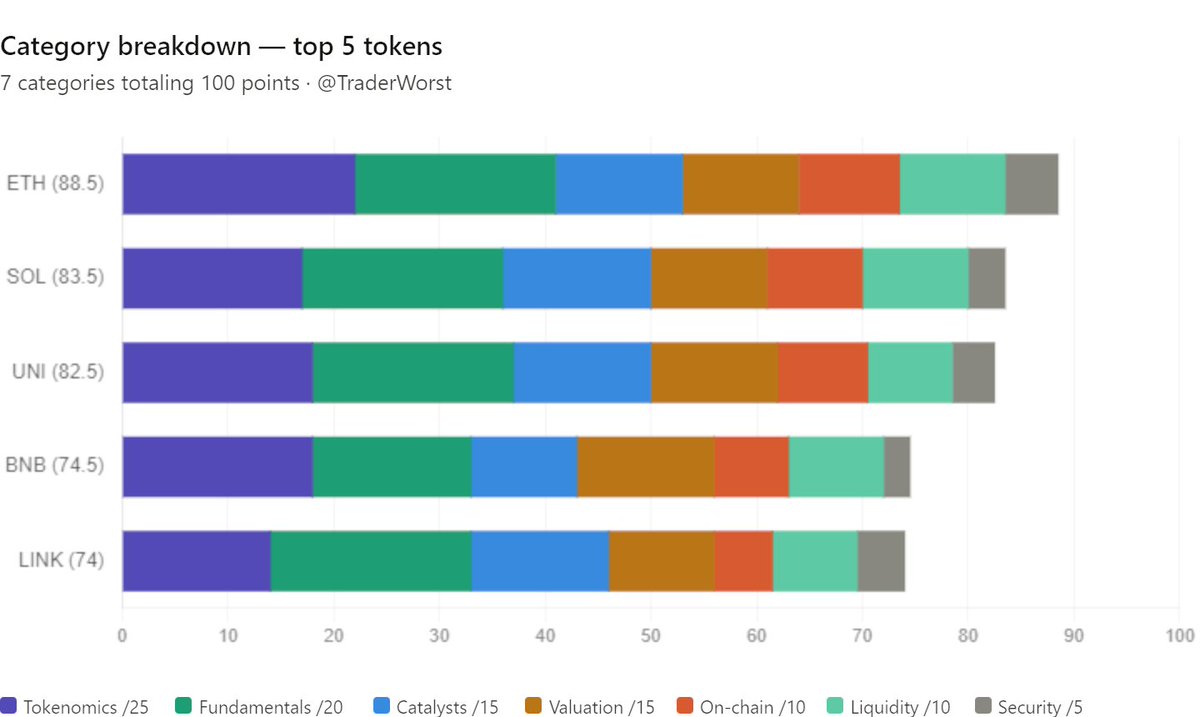

SCORE REVEAL: UNI | 92/100 | Excellent

Highest-rated token in our 28-asset framework.

UNIfication passed with 99.9% governance support:

- 100M UNI burned

- Fee switch live — trading fees now drive token burns

- Annualized protocol revenue: $34M

Next catalyst: L2 fee switch expansion to Arbitrum, Base, Optimism 5 more chains. Revenue target: ~$61M annualized.

UNI went from pure governance token to revenue-generating, deflationary asset. That's a structural repricing event.

Key risks: execution on L2 expansion, macro headwinds (oil at $113, no rate cuts), DeFi regulatory uncertainty.

Tokenomics: 23/25

Fundamentals: 19/20

Catalysts: 14/15

Valuation: 13/15

On-Chain: 9/10

Liquidity: 9/10

Security: 5/5

1

3

111

Mar 19

HEAD-TO-HEAD: ARB vs OP

Both Ethereum L2s. Both down ~96% from ATH. Which scores higher in our framework?

ARB: 67.5/100

#1 L2 by TVL (~$3B)

Deepest DeFi ecosystem (GMX, Pendle, Camelot)

Stylus WASM expansion

- 92.65M ARB monthly unlock until March 2027

- No burn mechanism

OP: 63.5/100

Superchain powers 34 networks

Buyback program launched Feb 2026

- Base leaving OP Stack for own tech (OP fell 20%)

- 51% tokens still locked

- Token captures limited Superchain value

Verdict: ARB edges it on DeFi depth and TVL leadership. But the elephant in the room for OP is Base's departure — removing its highest-revenue chain from the ecosystem.

Neither scores above 70. Both have tokenomics problems. At these valuations, ARB offers marginally better risk/reward.

2

80

Mar 16

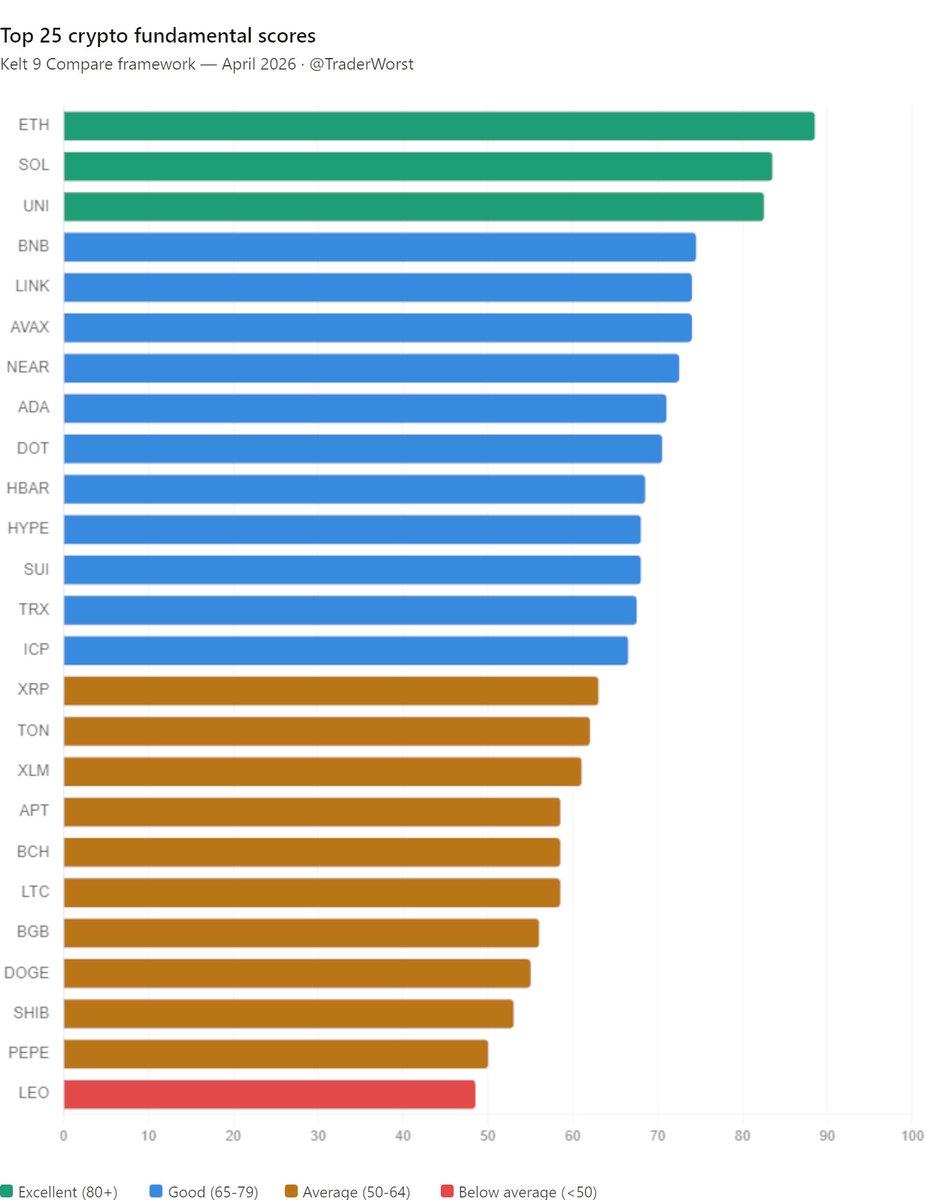

DeFi Protocol Rankings — March 2026

Scored 25 tokens across 7 categories. Here's how the DeFi layer stacks up:

1. $UNI — 92/100 (Excellent)

Fee switch 100M burn deflationary. Protocol revenue across 8 chains. The UNIfication proposal transforms a governance token into a revenue-generating asset. At ~$4 and -91% from ATH, this is the most mispriced DeFi blue chip.

2. $LINK — 79/100 (Good)

De facto oracle standard. CCIP cross-chain expansion driving real fee revenue. The infrastructure backbone DeFi can't function without.

3. $AAVE — 78/100 (Good)

Lending leader with real protocol revenue. GHO stablecoin adds value capture. Fee switch activation underway.

The gap: 13 points between #1 and the field.

UNI's fee switch is the single biggest tokenomics upgrade in DeFi right now. Most are sleeping on it because the price action has been brutal.

When the market reprices revenue-generating protocols, this ranking gap will compress — but probably not because UNI drops.

Full 7-category framework: Tokenomics (25%), Fundamentals (20%), Catalysts (15%), Valuation (15%), On-Chain (10%), Liquidity (10%), Security (5%).

2

179

Mar 16

Sunday market check — the catalysts we flagged are firing.

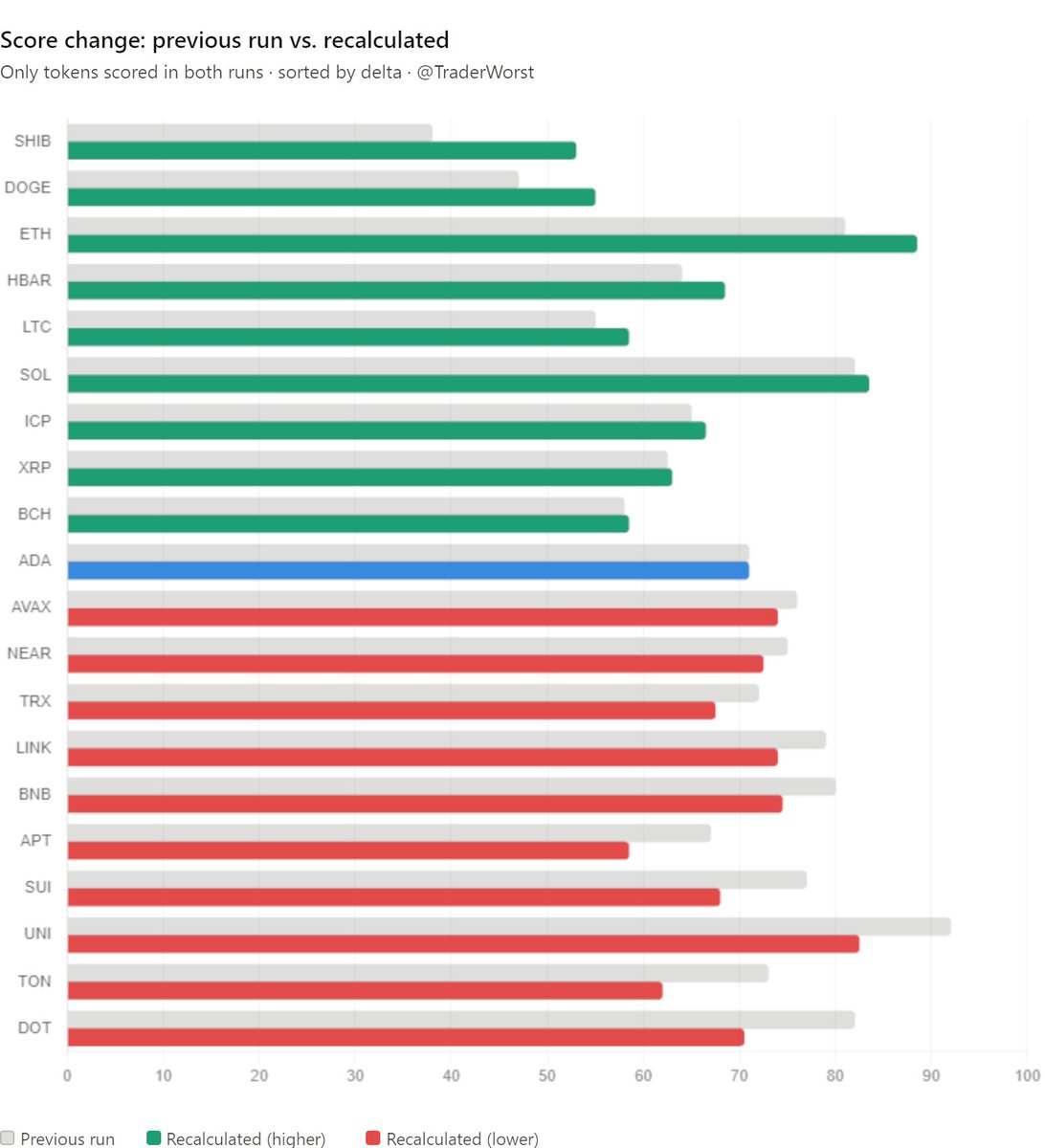

$DOT 12% today. We scored it 82/100 two weeks ago and called the Pi Day halving (March 14) as a structural catalyst. Inflation cut from ~120M to ~55M DOT/year. The market is finally pricing it in.

$ETH 10%. BTC above $74K. Broad altcoin recovery.

What's driving it:

- BTC ETF inflows: $1.34B this month

- DOT supply shock post-halving

- Fed decision Wednesday — markets front-running a dovish hold

Our top-scoring tokens (80 /100) leading the move: UNI, SOL, DOT, ETH, BNB.

This is what a fundamentals-driven rally looks like. Not everything pumps — the tokens with real catalysts move first.

Watch Wednesday closely.

1

85

Mar 16

New Entry: $ONDO — 70/100 (Good)

The RWA tokenization leader just entered our scoring framework. Here's the breakdown:

What it does right:

- $2.5B TVL at all-time highs

- USDY stablecoin crossed $1B TVL

- Real institutional revenue from tokenized US Treasuries

- BlackRock connection

- Ondo Global Markets expanding to European brokers

What keeps the score at 70, not higher:

- Only 48.6% of tokens circulating — significant dilution ahead

- Centralized team control

- Revenue depends on US Treasury yields — rate cuts compress margins

- FDV/TVL less attractive than pure DeFi plays

Current price: ~$0.28 (-87% from $2.14 ATH)

The RWA market is real — $15B in tokenized government securities and growing. But the token dilution is the elephant in the room.

Strong narrative. Real revenue. Dilution risk. Watch the vesting schedule before sizing up.

2

99

Mar 16

Head-to-Head: $ARB vs $OP — The L2 Battle

Our framework scores:

ARB: 67.5/100

OP: 63.5/100

Where ARB wins:

- #1 L2 by TVL, deepest DeFi ecosystem (GMX, Pendle, Camelot)

- Stylus WASM expansion adds non-EVM dev flexibility

Where OP wins:

- OP Stack powers 34 Superchain networks

- Handles 36.4% of all L2 transactions

- Base (Coinbase), Zora, Worldcoin all built on it

Shared risks: centralized sequencer, no burn mechanism, heavy unlock schedules.

The unlock pressure tells the real story:

ARB: ~92.65M tokens/month until March 2027

OP: 51% of total supply still locked

Both down 95% from ATH at ~$0.11 and ~$0.13.

Verdict: ARB edges OP on DeFi depth. OP has the infrastructure moat. Neither is high conviction until unlock pressure eases.

44

Mar 15

SCORE REVEAL: $DOT (Polkadot) — 82/100 | Post-Halving Update

Yesterday was Pi Day. It was also the day DOT's inflation rate was cut in half.

This isn't a narrative play. It's structural supply reduction.

Tokenomics (22/25): Halving cuts new supply from ~120M to ~55M DOT/year. Inflation drops from 6.8% to 3.11%. A hard cap of 2.1B DOT has been established. No more uncapped issuance — this is a fundamental shift in DOT's monetary policy.

Fundamentals (16/20): Substrate framework remains one of the best dev toolkits in crypto. 450-500 monthly active developers. JAM upgrade in development. But ecosystem adoption still lags Ethereum and Solana.

Catalysts (13/15): Pi Day halving is the strongest near-term catalyst in alt-L1s right now. 21Shares launched TDOT ETF on Nasdaq on March 6 — the first US exchange-traded Polkadot fund. Institutional access is now real.

Valuation (10/15): Depressed valuation at -90% from ATH. If the halving narrative gains traction, current levels represent asymmetric upside. But the market needs proof of ecosystem growth.

On-Chain (8/10): 65 active parachains processing transactions. Asset Hub migration consolidates DeFi activity. Cross-chain messaging via XCM is functional.

Liquidity (8/10): Listed on all major exchanges with decent volume. Institutional infrastructure improving with ETF launch.

Security (5/5): Shared security model — every parachain inherits relay chain security. Battle-tested consensus. Validator set is well-distributed.

Key risk: Ecosystem adoption significantly behind competitors. Complex governance. The tech is solid but needs more users.

Our thesis: Best risk/reward setup in alt-L1s at current levels. The halving ETF combination creates a structural floor.

1

6

59

2,745

Mar 15

SCORE REVEAL: $ETH (Ethereum) — 81/100

Everyone has an opinion on ETH. Here's what the data says.

Tokenomics (19/25): Post-merge deflationary via EIP-1559 burn. No VC unlocks. Fully distributed since 2015. Supply decreases in high-activity periods.

Fundamentals (17/20): The dominant smart contract platform. Strongest dev ecosystem in crypto. Institutional adoption via spot ETFs. More developers build on ETH than all alt-L1s combined.

Catalysts (10/15): Pectra upgrade shipped May 2025. Staked ETH ETFs add a new demand vector. But near-term narrative momentum favors competitors — creating a contrarian setup.

Valuation (11/15): Trading at a significant discount to prior highs relative to network fundamentals. L2 revenue cannibalization is the legitimate concern — Base alone generates more fees than ETH L1 on some days.

On-Chain (9/10): $50B DeFi TVL across the ecosystem. Most diverse dApp landscape. 1M validators securing the network post-Pectra consolidation.

Liquidity (10/10): Deepest orderbooks across every major exchange. Most trading pairs. Unmatched institutional infrastructure.

Security (5/5): Battle-tested since 2015. Multiple independent client implementations. No successful consensus attacks in a decade.

Key risk: If value accrues to L2s rather than L1, ETH's monetary premium faces structural headwinds.

Our thesis: ETH remains the foundational layer of crypto. The market is mispricing its network effects at current levels.

154

Mar 15

HEAD-TO-HEAD: $LINK vs $AAVE — DeFi infrastructure, different bets.

Both are blue-chip DeFi. Both have real revenue. But they solve very different problems.

Chainlink (79/100):

- Fundamentals (17/20): De facto oracle standard. If smart contracts need external data, they use Chainlink.

- Catalysts (13/15): CCIP cross-chain expansion is the real play. Every new chain needs oracles.

- Tokenomics (17/25): Token emission schedule is the weakness. Limited on-chain value accrual to date.

Aave (78/100):

- Fundamentals (16/20): DeFi lending leader with real, growing revenue.

- Catalysts (12/15): Fee switch activation GHO stablecoin add direct value accrual to token holders.

- Tokenomics (18/25): Better token structure, but smart contract risk is always present.

The difference: LINK is a picks-and-shovels play on DeFi growth. AAVE is a direct bet on lending demand.

LINK edges it on irreplaceability — there's no real Chainlink alternative. AAVE faces Compound, Morpho, and others.

Both solid. LINK slightly better positioning.

51

Mar 15

HEAD-TO-HEAD: $ARB vs $OP — Which L2 deserves your capital?

Both are down 95% from ATH. Both have token unlock problems. But the data tells different stories.

Arbitrum (67.5/100):

- Tokenomics (15/25): 92.65M ARB unlocking monthly until March 2027

- Fundamentals (16/20): Largest L2 by TVL, Nitro Stylus tech stack

- On-Chain (8/10): Deep DeFi ecosystem — GMX, Pendle, Camelot

- Catalysts (11/15): Stylus WASM expansion, institutional DeFi growth

Optimism (63.5/100):

- Tokenomics (13/25): 51% still locked, ongoing vesting pressure

- Fundamentals (15/20): OP Stack powers Base, Zora, Worldcoin (34 chains)

- On-Chain (6/10): 36.4% of L2 transactions but DeFi depth trails ARB

- Catalysts (10/15): Superchain network effects, but OP token captures limited value

The gap: ARB wins on DeFi depth and current usage. OP wins on infrastructure adoption.

But neither token has a burn mechanism, and both run centralized sequencers.

Verdict: ARB edges it at 67.5 vs 63.5. Better value accrual from actual DeFi activity vs OP's infrastructure play where value leaks to chains built on top.

Neither is a strong conviction play until unlock schedules normalize.

119