Systematic and #Quant Trader. Sharing useful information about 📈📉#QuantitativeTrading #AlgorithmicTrading #AlgoTrading #QuantTrading #Trading #MachineTrading

Joined August 2017

- Tweets 1,322

- Following 829

- Followers 642

- Likes 6,760

6 Photos and videos

Trading Enigma retweeted

3 Sep 2021

I've been writing an article on AMM algorithms, recording what I've learned in the past 2 months. The medium article is kind of long so I made a few key points here. @AnchorDAO @_Dave__White_ @danrobinson @Showen_Peng @dken_w @EtheriaChan @TWAMM_

medium.com/anchordao-lab/aut…

12

31

133

Trading Enigma retweeted

1 Sep 2021

One of my favorite quotes from @chanep ‘s Quantitative Trading books.

31 Aug 2021

1/ A lot of quant traders (including myself at many times) have a knee jerk instinct to believe that if a strategy is technically challenging it must mean there’s more alpha underneath.

5

68

Trading Enigma retweeted

31 Aug 2021

1/ A lot of quant traders (including myself at many times) have a knee jerk instinct to believe that if a strategy is technically challenging it must mean there’s more alpha underneath.

31 Aug 2021

I went to school for math. I got trained in quant trading, and eventually shifted to quant trading in crypto. Over time, I've relied less on math and more on intuition, e.g. for analyzing Elon's tweets.

Yesterday I looked at ... cartoons? for 4 hours.

A thread about adapting.

12

60

352

Trading Enigma retweeted

9 Aug 2021

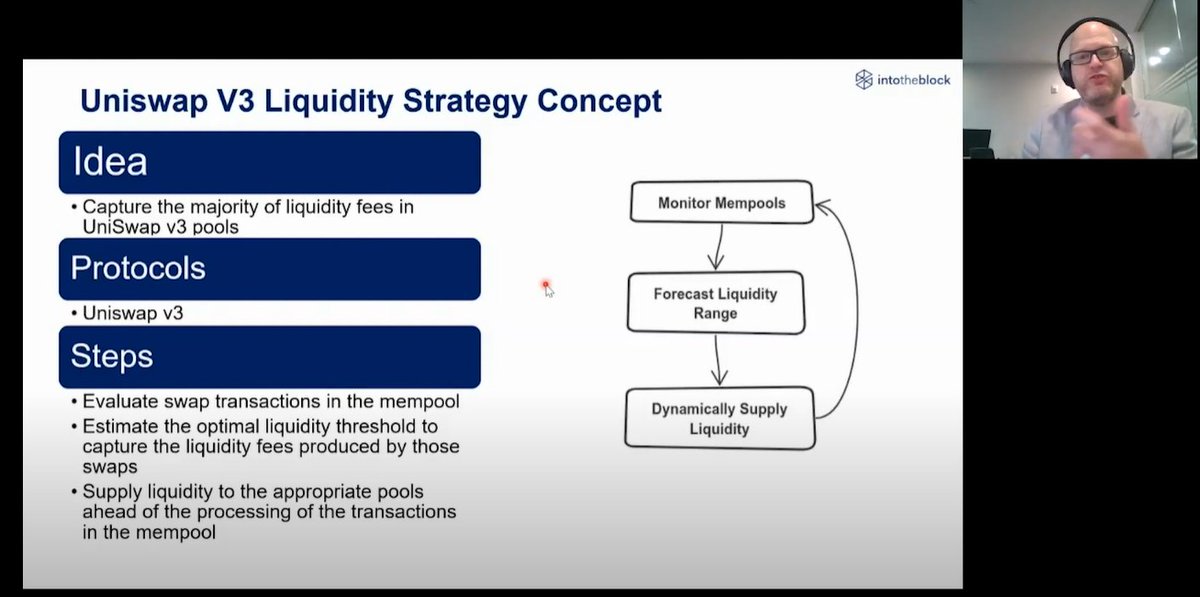

For those interested in developing #HFT strategies in #DeFi, this presentation by @jrdothoughts can give you some approach angles and interesting ideas

9 Aug 2021

Last week, we presented a great session at the @BlockchainZA DeFi Conference 2021.

This session was focused on High-Frequency Trading in DeFi, covering key building blocks of DeFi HFT Strategies as well as some crazy ideas.

Here's the recording👇

youtu.be/MsWIS436do4

2

4

Trading Enigma retweeted

11 Aug 2021

A misconception about DeFi is that HFT doesn't exist, because blocks only occur every few seconds. The truth is that HFT-like price discovery *does* occur. In the mempool (and private networks like Flashbots). If you're only looking on-chain, you're missing a lot of the ecosystem

2

5

23

Trading Enigma retweeted

22 Jul 2021

⚠️ It’s 📰💧 time of the month again 🚨

Don’t want to read 100s of pages of CFMM literature?

You’re in luck! We review the known theory of CFMMs (plus some new goodies!) for an upcoming *textbook* chapter on crypto DeFi w/ two new authors:

(Paper: stanford.edu/~guillean/paper…)

8

43

229

Trading Enigma retweeted

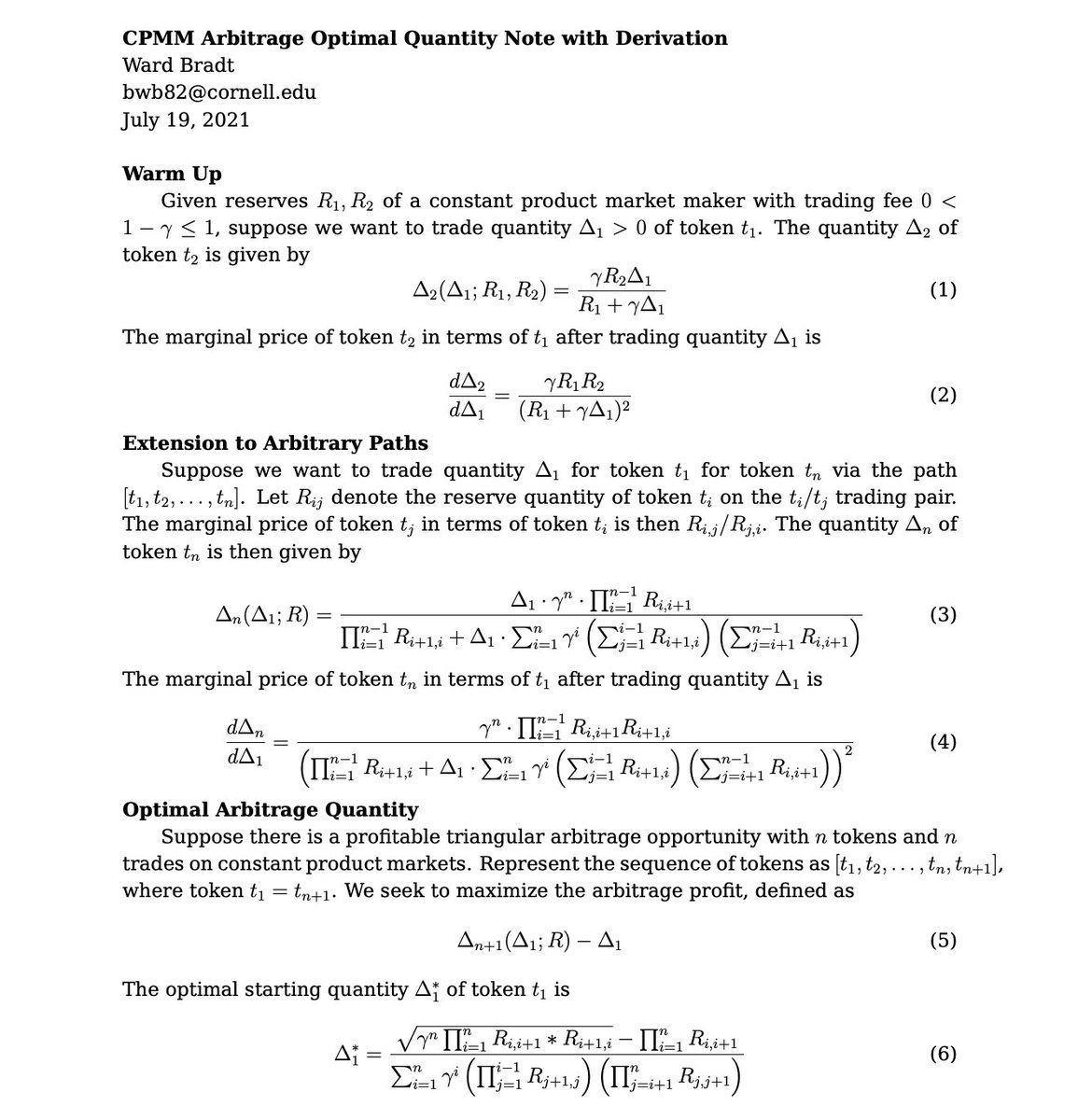

19 Jul 2021

Optimal starting amount for maximizing arbitrage profit on arbitrary-length paths of constant product market makers. (note v3, fixed a typo in numerator of eq 3)

12

14

140

Trading Enigma retweeted

4 Aug 2021

Read my latest article: A Guide for Choosing Optimal @Uniswap V3 LP Positions, Part 1

In this post, I derive a (known) relationship relating the probability that the price of an asset will fall within a predefined range.

medium.com/@lambert-guillaum…

4

11

87

Trading Enigma retweeted

8 Aug 2021

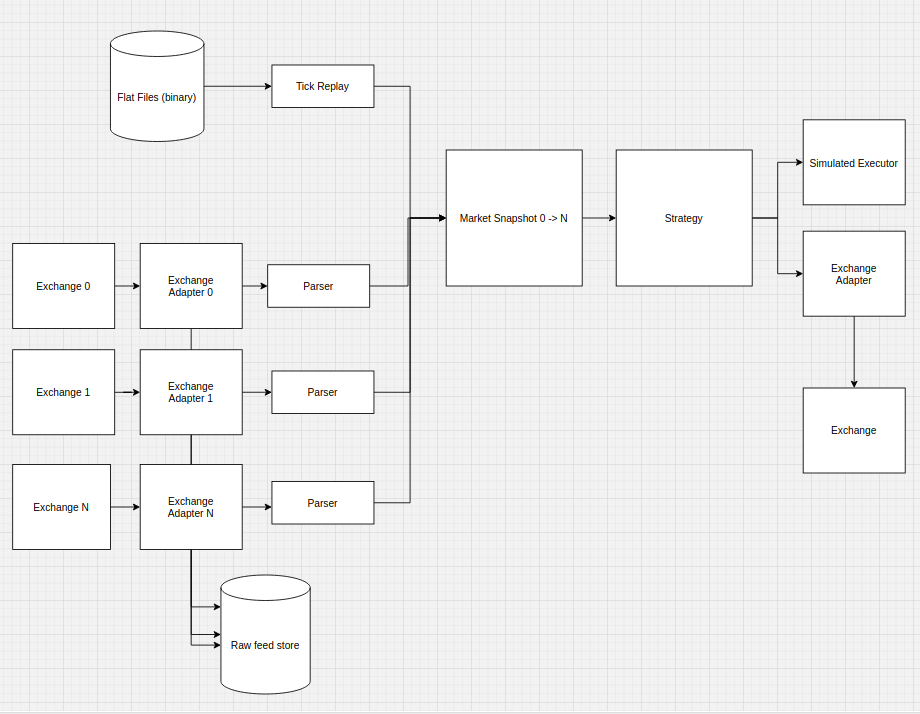

Architecture diagram for HFT crypto trading using exchange adapters and conversion off hot-path for market replay. @Shamitha_R the 👑

8 Aug 2021

Easier to explain with an high level architecture diagram. The raw feeds are stored and there is a scheduled script to convert them to the binary flat files

2

8

Trading Enigma retweeted

24 Jul 2021

The main problem with trading options as retail is the vig you pay on each trade.

You start the game a goal behind.

Can your edge be expressed in a cheaper more liquid instrument?

18

7

134

Trading Enigma retweeted

22 Jul 2021

quick rant about "constructing a neutral exposure" while I wait for something to load. a qualitative description about step by step optimization for us peons who take seconds to calculate (not microseconds on a custom ASIC like some here)

1/ Have a quant strategy. What's that?

7

22

150

Trading Enigma retweeted

16 Jul 2021

"In the 90s and early 2000s, we focused on longer-term price momentum and a relatively slow trading frequency. The current approach is very nimble. The systems are designed to evolve, making fine-tuned adjustments throughout the day, in real-time."

hedgeweek.com/2021/07/16/303…

3

2

26

Trading Enigma retweeted

12 Jul 2021

I wrote about the rise of quants in the credit world. With the jump in electronic trading during the pandemic, quants say their methods are set to sweep the bond world as they did equities decades ago @markets

bloomberg.com/news/articles/…

2

8

38

Trading Enigma retweeted

5 Jul 2021

Trade six types of strategies

If you have momentum trades, add in a system for mean-reversion. If you have trend-following trades, add some carry strategies. 5 from one strategy, could be -4 from the other and it'll auto-reduce scale

h/t discussion w/ @SimpelAlpha

Thread👇

ALT Quant Crypto Trading Strategies

14

99

474

Trading Enigma retweeted

30 Jun 2021

So you like trade tips, eh?

Get some features that are correlated with future returns, combine and stick em in a constrained optimization with a txn cost model and risk model, then trade the delta to your exposures using algorithmic execution to reduce impact.

You're welcome.

8

9

173

Trading Enigma retweeted

27 Jun 2021

How much of trading really just comes down to:

1. Supply liquidity to <forced / price insensitive flow>

2. Don't get run over.

?

9

13

149

Trading Enigma retweeted

22 Jun 2021

"Empyrial is a Python-based open-source quantitative investment library dedicated to portfolio management [combining] risk analysis, quantitative analysis, fundamental analysis, factor analysis, and prediction making." github.com/ssantoshp/Empyria…

43

141

Trading Enigma retweeted

15 Jun 2021

"Statistical arbitrage identifies and exploits temporal price differences between similar assets. We propose a unifying conceptual framework and develop a novel deep learning solution, which finds commonality and time-series patterns from large panels." arxiv.org/pdf/2106.04028.pdf

1

12

49

Trading Enigma retweeted

12 Jun 2021

Blog post on an algorithmic trading platform

medium.com/prooftrading/proo…

4

29

Trading Enigma retweeted

8 Jun 2021

Finally took the plunge and published NSE F&O Bhavcopy summarizer on Github.

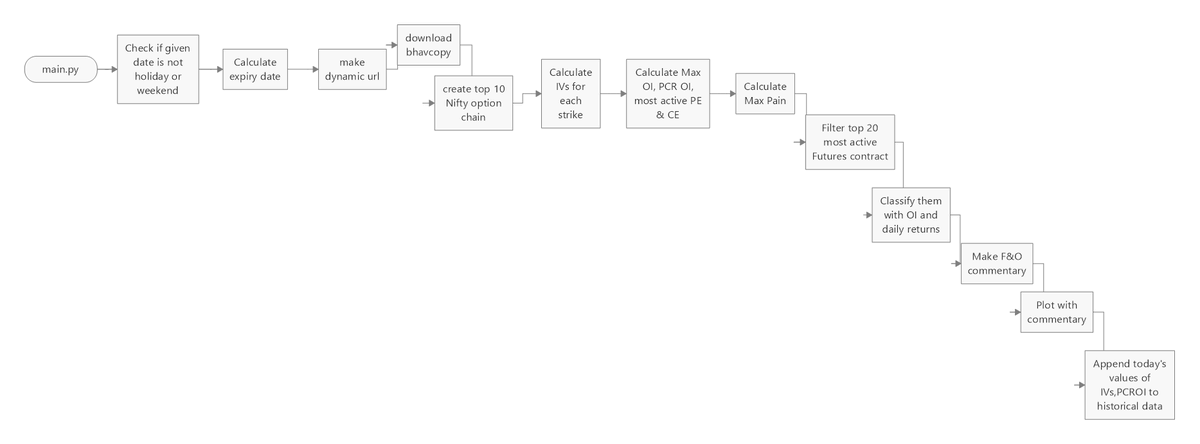

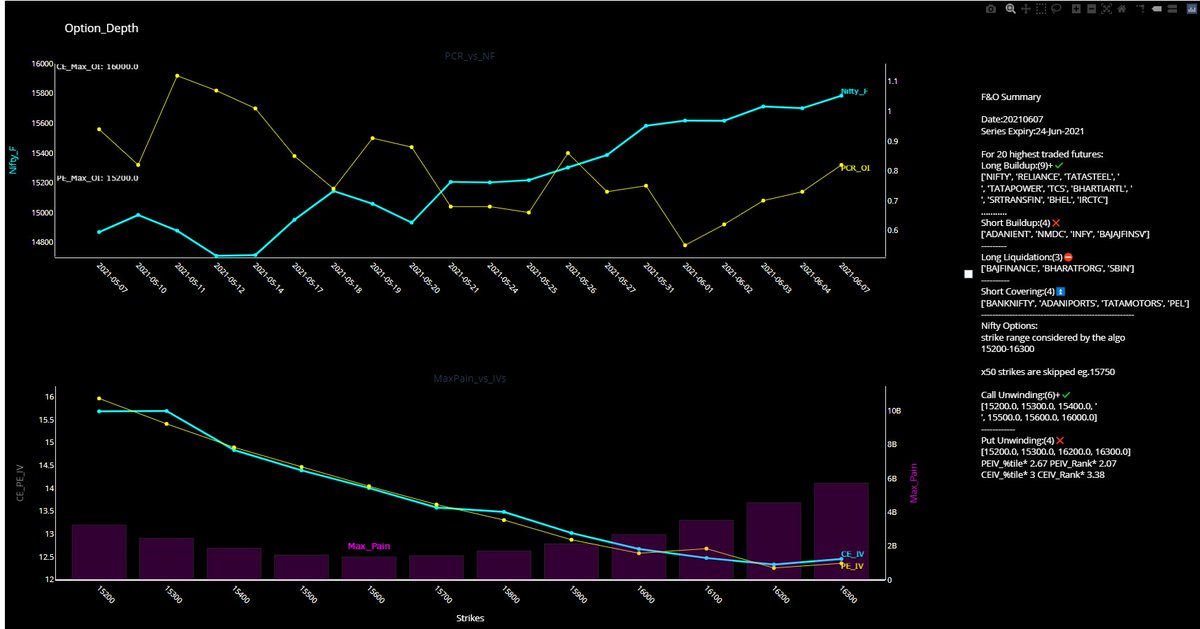

A lot of moving objects there and impossible to explain everything so I just commented the code

github.com/beinghorizontal/B…

This is the code flow and sample diagram it will generate

18

47

207