90 Photos and videos

Traits retweeted

11h

BRUH

🤣🤣🤣🤣🤣

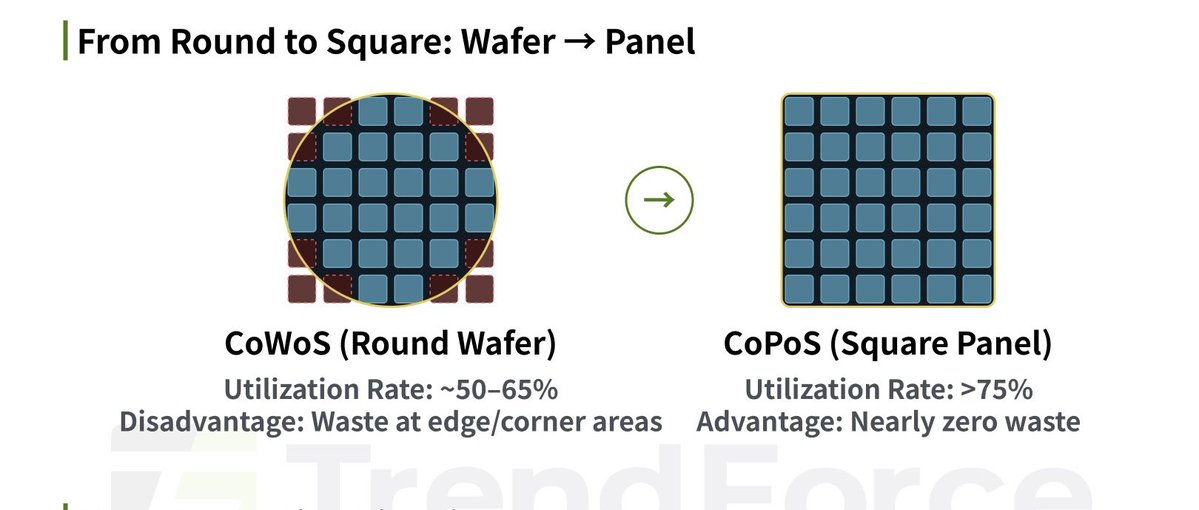

Why the fuck do people think that these are silicon panels??

Go read about panel-level packaging before writing shit like this

The big square panel is glass

I once saw a video of how those crystals are grown. Unless you know a way to grow square crystals or reduce the chance of creating fractures while cutting the cylinder crystal, it might not be worth it.

8

6

161

57,260

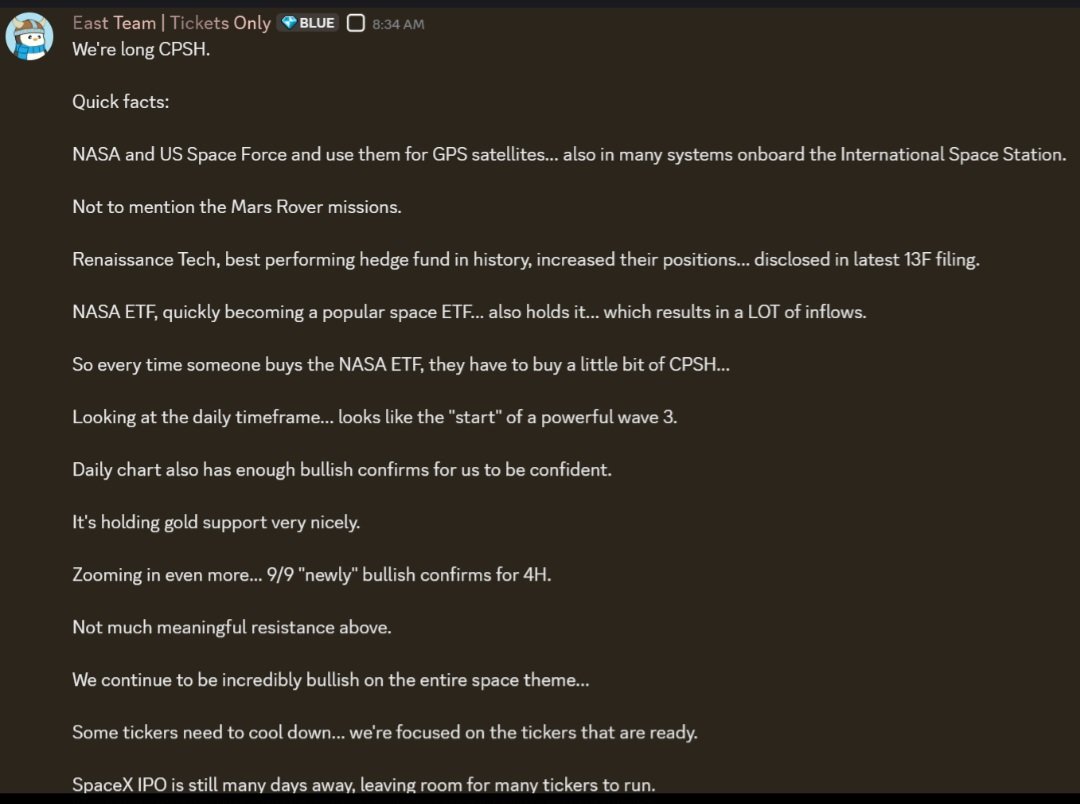

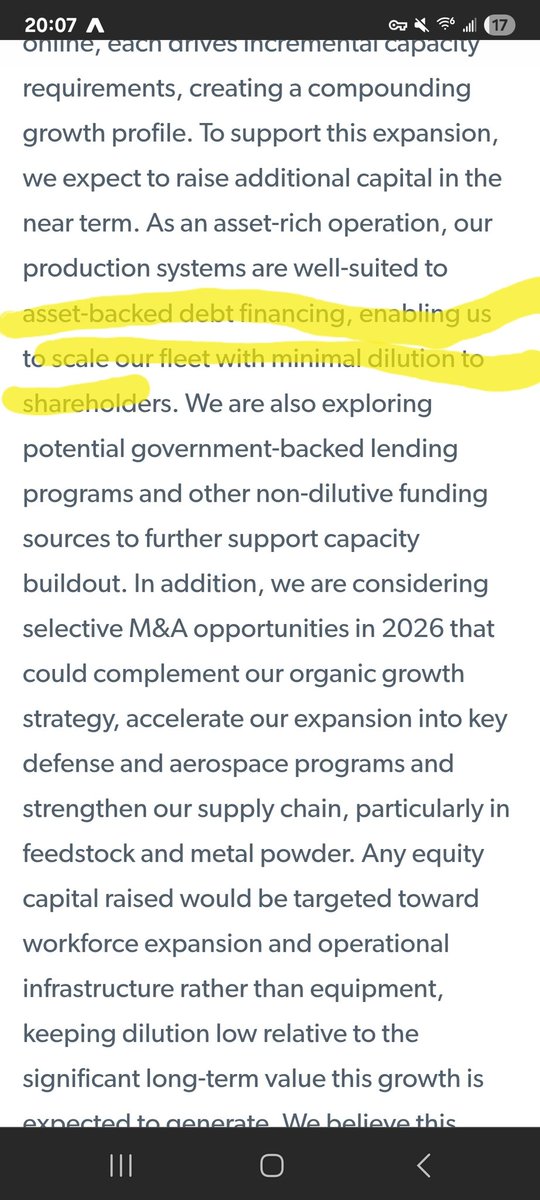

For example in crispy's spaces arun said there were ~22 machines on their floor now only 15?? Obv they could have sold them on. But lost of gaps like that all over. From avoiding CA in the future, to now 100 machines planned there? Or 400 machines in 5 years to 7 now 10? Etc.

1

632

Traits retweeted

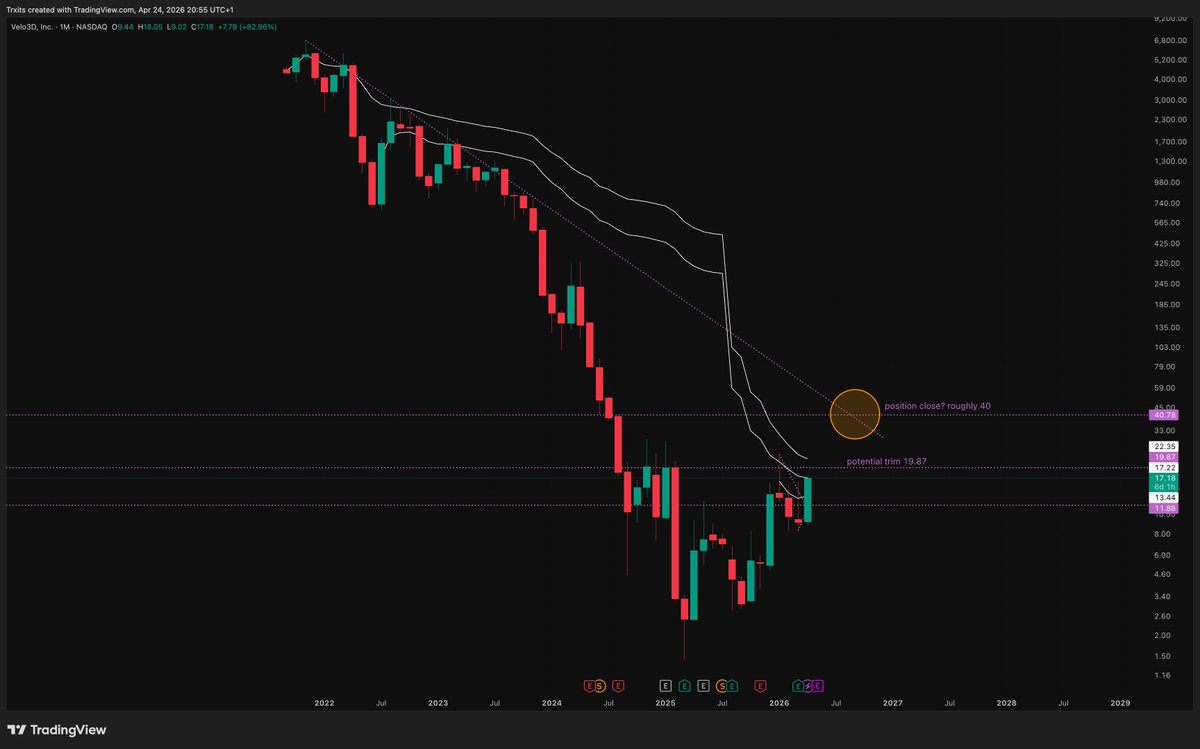

It's no wonder that $VELO is down 10% AH. Matter of fact, I'm surprised its not down more:

Positive EBITDA projections got postponed by half a year.

Velo reported $46M for 2025 with expectations for $60-70M in 2026. They’ll have to hit the upper end of that range in order for their prior 50% annual growth projections to hold true. Implicit in such guidance is a tacit admission in the form of them invalidating their prior 50% growth target due to the vast majority of that range not being sufficient in attaining 50% growth.

In prior public engagements he said 400 hosted printers in 5 years, now he’s saying a decade.

He noted that RPS gross margins are 40-60% versus prior statements of 50-60%, which is relevant due to making RPS look more profitable by juxtaposing it to 35%-40% for the machines. Now the delta doesn’t look to be so much.

He threw in somewhat of a curve ball regarding M&A which sounds like Jeldi intends to leverage $VELO's public status and capital-raising ability to bring in one of his private magnesium companies (most logically Crown for feedstock control) (i.e., public buyout of a privately owned entity via an insider transaction).

They called for “Gross margin: >30% exiting 2025”. Instead they delivered a gross margin of negative 73%. Even if you adjust for the $7M obsolete inventory write-down it was still only 0.3%.

Etc.

5

4

32

3,999

$VELO correct good sir!

Mar 6

$VELO: New post on Linkedin. This seems to be in partnership with $LMT and $GE.

defensescoop.com/2026/01/16/…

A brand new Fridays with Fern is here! See how we printed a hypersonic ramjet capable of Mach 5.

The engineering inside is impressive and worth a watch to see what's possible with additive.

Fernando breaks it down for us. A brand new Fridays with Fern is here! See how we printed a hypersonic ramjet capable of Mach 5.

The engineering inside is impressive and worth a watch to see what's possible with additive.

1

639

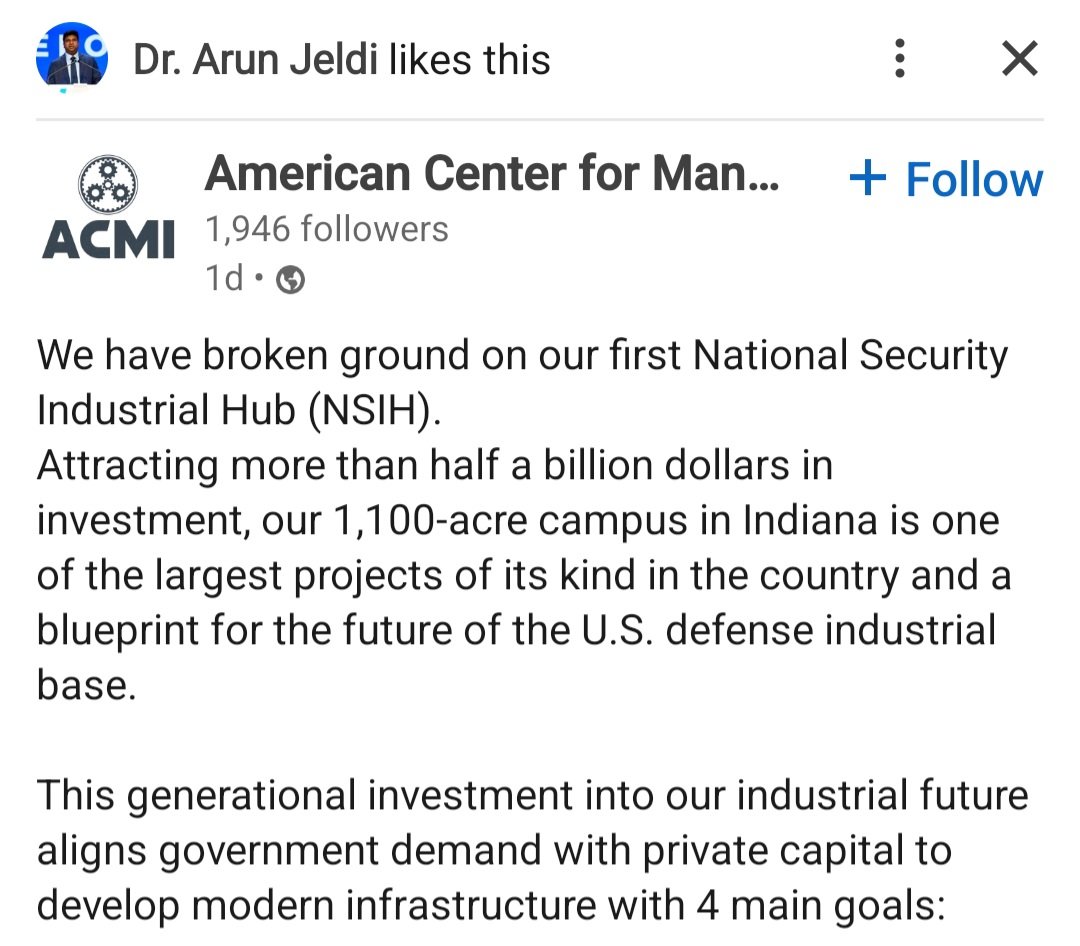

$VELO Indiana = Midwest ✅️

acmigroup.com/2026/02/20/acm…

@kingtutcap @GrumpierBTDay @pennycheck @fundmyfund

4

2

30

4,139