explaining market structure for people who were never handed the insider seat. earnings, flows, positioning without the jargon wall

Joined September 2025

- Tweets 709

- Following 114

- Followers 201

- Likes 1,016

19 Photos and videos

Pinned Tweet

Apr 27

Crypto moves fast and explains itself badly. This account slows it down.

Here you'll find:

💹 on-chain data breakdowns

💹 protocol news with context

💹 what the price move actually reflects

💹 no trade setups, no "this is the bottom" calls

If you care about understanding crypto without needing to already be inside it, this is the lane.

16

685

Jun 11

The headline is real. The timeline needs context before you trade on it.

Japan advancing the 20% crypto tax bill is the third piece of a regulatory framework that has been quietly assembling all year:

June 1: Japan legalized foreign stablecoins including USDC under the Payment Services Act

Last week: Japan began reviewing MiCA to align with U.S. CLARITY Act framework

Today: Bill advancing to reclassify crypto as a financial product and cut taxes from 55% to 20%

The numbers that matter: Japanese asset managers are already planning ¥5 trillion in crypto ETFs - that capital has been waiting on exactly this regulatory clarity. The reform also introduces three-year loss carryovers - a structural change that makes Japan competitive with Singapore and Hong Kong for the first time.

The caveat worth knowing: the 20% flat rate for individual traders isn't projected to be fully enforceable until January 1, 2028. Staking rewards, lending yields and NFTs also remain taxed as miscellaneous income at rates up to 55% - the reform is meaningful but not complete.

The macro picture: Japan, the EU, and the U.S. are converging on compatible crypto regulatory frameworks simultaneously. That coordination is what institutional capital has been waiting for.

Let's see whether the ¥5 trillion ETF pipeline starts moving on this news.

Jun 11

JUST IN: 🇯🇵 Japan advances bill to reclassify cryptocurrencies as financial products and cut taxes from 55% to 20%.

2

2

25

Jun 10

4.2% headline. Met estimates. The market is breathing a sigh of relief it probably shouldn't.

The number that actually matters: energy prices accounted for over 60% of the monthly CPI gain. Gasoline up 40.5%. Fuel oil up 58.9%. This is an Iran war inflation print dressed up as a broad inflation report.

Core CPI rose just 0.2% month-over-month - below the 0.3% estimate and well below April's 0.4%. That's the number the Fed actually cares about. And it came in soft.

So here's the real read:

Headline inflation is being driven by a single geopolitical event. If a US-Iran deal closes - oil is already below $90 on deal hints - the energy component reverses fast and headline CPI drops hard. The Fed knows this. They won't hike on oil war inflation.

Core inflation at 2.9% is elevated but decelerating on a monthly basis. That's not a hiking environment.

Markets largely expect the FOMC to hold on June 17. The more interesting question is Warsh's press conference language - does he signal the bar for a hike is rising or falling?

The Iran situation is doing more work in this report than monetary policy can fix.

Let's see the June 17 press conference's tone. Oil price direction. Those two things determine whether 4.2% is the peak or just a waypoint.

BREAKING: May CPI inflation rises to 4.2%, the highest level since April 2023.

Core CPI inflation also rises to 2.9%, the highest since September 2025.

Inflation in the US is officially back above 4% and more than double the Fed's target.

Odds of Fed rate hikes are rising.

145

Taiwan isn't just aligning with U.S. policy. It's trying to stay in Tier 1.

The context most posts will miss: the U.S. already split the world into two tiers for AI chip access. Tier 1 - closest allies including Taiwan - gets unlimited access to U.S. AI technology. Everyone else gets capped. Taiwan's "consideration" of China export restrictions isn't altruistic policy alignment. It's the price of keeping that Tier 1 status.

The smuggling problem is what's forcing the issue. Since November 2025 the DOJ has uncovered multiple hardware smuggling rings routing Nvidia chips through Taiwan and Southeast Asian intermediaries into China. Supermicro's co-founder was arrested in March. The paper trail runs through Taiwan.

The stock read-through is direct:

$NVDA - China revenue already at zero in guidance. Taiwan alignment closes the smuggling loophole that was partially backfilling that number

$TSM - TSMC is already enforcing U.S. restrictions after the Sophgo incident. Formal government policy just catches up to what TSMC is already doing

$ASML - Netherlands is the next domino. Every Tier 1 country that formalizes controls increases pressure on holdouts

The global AI chip control regime is becoming real infrastructure. Taiwan just became its eastern anchor.

Jun 9

TAIWAN IS CONSIDERING RESTRICTIONS ON AI CHIP EXPORTS TO CHINA TO BE IN LINE WITH US POLICIES.

51

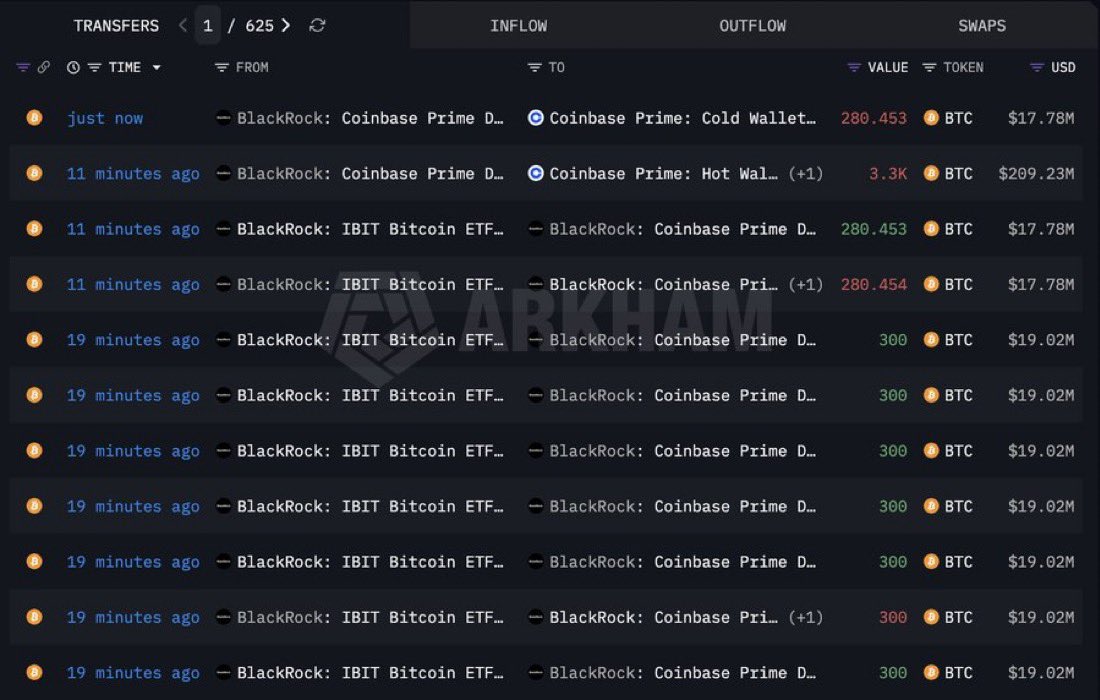

Everyone calling this "selling" has it backwards.

BlackRock depositing $226M in Bitcoin to Coinbase Prime is an inflow signal. Coinbase Prime is IBIT's custodian - BTC gets deposited there when new ETF subscriptions come in and BlackRock converts fresh institutional cash into custody.

This is how you know $54B in IBIT assets actually exists. The Bitcoin physically moves to Prime every time a large institution buys in.

The flow that matters: cash comes in from an institution, BlackRock buys BTC on the open market, BTC moves to Coinbase Prime custody. That's what a $226M deposit looks like on-chain. Someone seeing it and posting "more selling" is reading the transaction backwards.

Eight years in finance. Custody flows get misread like this constantly - usually by people who've never seen how institutional settlement actually works.

Jun 8

🇺🇸 BlackRock deposits $226M worth of Bitcoin to Coinbase Prime.

More selling...

38

The headline is brutal. The context matters.

Bitmine raised $400M to build an ETH treasury in March - when ETH was trading above $2,600. It's now below $1,800.

The $10B unrealized loss figure includes the full equity market cap drawdown, not just the ETH position. Classic conflation that makes the number sound worse than it already is.

The real question: Tom Lee ran the same playbook as Saylor with Bitcoin. Saylor survived multiple 80% drawdowns because BTC eventually recovered and the thesis held. ETH bulls are making the same bet.

The difference: ETH has underperformed BTC by 35% this year. The recovery thesis requires ETH to stop bleeding relative to BTC first.

Jun 5

JUST IN: Tom Lee's 'Bitmine' $ETH investment is currently at a $10,000,000,000 unrealized loss.

1

1

68

$AMZN just committed €10B to automate European fulfillment. Everyone's talking about the 25,000 jobs. The margin story is what actually moves the stock.

Amazon's North America retail operating margin hit 6.9% last quarter. Two years ago it was 3.5%. Robotics is the primary driver - Proteus, STARK, Deepfleet AI coordinating over 1 million robots across fulfillment centers.

European retail margins still lag North America by ~400bps. This investment is the catch-up play. Same playbook, different geography.

The robots deploying across European sites:

• Proteus - free navigation alongside humans, no safety cages

• Vulcan - touch sensitivity for handling fragile items, coming 2027

• STARK - tote and trailer unloading, historically the most labor-intensive step

• 50,000 electric vans globally on top of all of this

The $1B worker retraining commitment by 2030 is the political cover that comes with deploying robots at scale across five countries. Worth noting - not worth overstating.

Look out for the European segment operating margin in Q3 and Q4. That's where this investment starts showing up in the numbers.

5

9

114

Perpetual futures are the most traded crypto derivative on the planet. Until May 29 every single one was offshore.

Hyperliquid, Binance, Bybit - U.S. traders were accessing them anyway, just through unregulated venues with no CFTC oversight, no margin protection, no clearing standards. The regulator looked the other way for years.

That just changed.

Kalshi's BTCPERP is the first true Bitcoin perpetual approved by a CFTC-registered exchange. Same day, Coinbase got a no-action letter to route customers into global perps through its Bermuda subsidiary - with BTC, ETH and stablecoins accepted as margin collateral.

What this actually unlocks:

• Institutional players that couldn't touch offshore perps for compliance reasons now have an onshore venue

• Hyperliquid's U.S. market share is now directly threatened - regulated competition just arrived

• Polymarket already announced it wants to offer perps on NVDA, $COIN, silver and gold with 10x leverage

The regulatory dam broke in one afternoon. Japan legalized foreign stablecoins June 1. The CLARITY Act is moving through Senate. Now the CFTC brings perps onshore.

The global regulatory coordination that was theoretical six months ago is starting to look structural.

Watch: whether Hyperliquid volume migrates onshore and how fast Polymarket gets its own approval.

Bitcoin Perpetuals are now live for trading.

The First American Perpetual Future.

Only on Kalshi.

1

4

184

Google spent 11 years and $250B telling shareholders they were the priority.

then AI showed up and shareholders became the funding mechanism.

the arms race doesn't care about your buyback program.

Jun 2

🚨 GOOGLE ENDS AN 11-YEAR BUYBACK RUN TO GO ALL-IN ON AI

Google has bought back its stock every year for the last 11 years in a cumulative $250 billion repurchase. Now, Alphabet is pivoting to an all-out AI spending spree.

The company plans to raise $80 billion to build AI infrastructure and data centers. It has already committed $10 billion to Anthropic, with up to $30 billion more tied to performance targets.

Alphabet now expects to spend as much as $190 BILLION on capital expenditures in 2026 alone.

The AI arms race is replacing shareholder returns.

1

51

May 29

Susquehanna just raised their $MU target from $600 to $1,750. That is not a typo.

The channel checks behind it are the more useful part:

Q2 DRAM ASPs trending up 50-60% QoQ - ahead of the 50% consensus estimate

NAND ASPs up 75-100% QoQ - unchanged from prior checks, meaning the pricing holds

Margin sustainability is the new debate - Hosseini is saying the high-margin regime is not a one-quarter event

The structural reason this is happening: every HBM wafer requires 3x the fab capacity of standard DRAM. Micron, SK Hynix and Samsung are all choosing HBM over commodity memory. Supply stays tight by design, pricing stays elevated, margins expand.

The risk worth flagging: a $1,750 target implies Micron crosses $2 trillion in market cap. That prices in the margin expansion holding through 2027 with no meaningful competitive response from CXMT or new fab capacity coming online.

Samsung's yield issues gave Micron share it was not supposed to have. Samsung is fixing those yields.

The pricing strength is real. The question is duration.

⚡️Micron $MU price target raised to $1,750 from $600 at Susquehanna

Susquehanna analyst Mehdi Hosseini raised the firm's price target on Micron to $1,750 from $600 and keeps a Positive rating on the shares.

The firm's checks suggest Q2 DRAM average selling prices are trending to be up 50%-60% quarter-over-quarter, ahead of expectations of up 50%, while NAND ASPs are trending unchanged at up 75-100% quarter-over-quarter, reports the analyst, who is increasing estimates for memory manufacturers under coverage, driven by continued strength in blended ASPs and growing confidence in the sustainability of the margin profile.

1

3

306

May 28

The original post covers what's happening. Here's what it means for how you actually trade these names.

Pre-market options: 7:30am ET to 9:25am ET Post-market options: 4:00pm ET to 4:15pm ET Live date: July 13, 2026

Why this changes things structurally:

• Earnings are almost always released pre-market or after close. Right now you can't hedge or position in options during those exact windows. July 13 changes that

• Asian and European investors get their first real-time access to single-stock options on U.S. names during their trading hours - GTH volume already up 32% YoY on index products

•The 15-minute post-market window is surgical - designed specifically for companies that report right at 4pm close

The part nobody's discussing: liquidity. Extended hours equity options are going to have wide spreads early. Market makers price uncertainty into every session. Pre-market $NVDA options the morning of an earnings print will be expensive - the implied volatility premium will reflect that thin book.

December brings 23x5 equities trading on CBOE EDGX. Two launches. One direction.

$CBOE at a 52-week high today. The infrastructure play here writes itself.

May 28

THE OPTIONS MARKET IS ABOUT TO GO EXTENDED HOURS: THE MAG 7 ARE FIRST IN LINE

CBOE just received SEC approval to launch extended trading hours for options. Launch date: July 13, 2026.

Here's who makes the cut at launch:

About 20 stocks, including all Magnificent 7 names:

• Apple $AAPL

• Microsoft $MSFT

• NVIDIA $NVDA

• Google $GOOGL

• Amazon $AMZN

• Meta $META

• Tesla $TSLA

To qualify for extended hours options trading:

- $50B market cap

- 150,000 contracts minimum

- 10M shares in daily average trading volume

CBOE Global Markets $CBOE also plans to launch 23x5 equities trading on its CBOE EDGX Exchange in December. Nearly around-the-clock trading, 5 days a week.

Two separate launches. One direction: the market is open longer than ever.

58

May 27

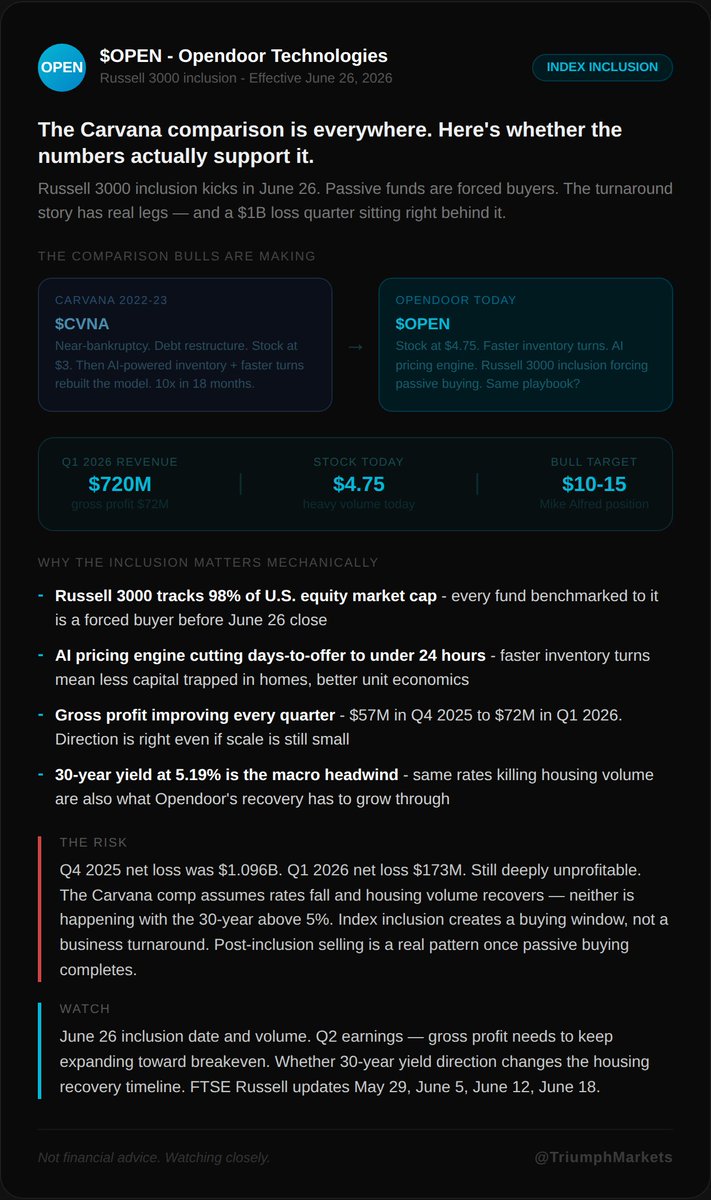

$OPEN Everyone's making the Carvana comparison. Here's whether the numbers actually support it.

Russell 3000 inclusion kicks in June 26. Passive funds are forced buyers between now and then.

The Carvana comp in plain terms: $CVNA was near-bankrupt in 2022, rebuilt on faster inventory turns and AI pricing, then 10x'd in 18 months. Bulls think $OPEN is running the same playbook at $4.75 with a $10-15 target.

The data that supports it:

Gross profit growing every quarter - $57M in Q4 2025 to $72M in Q1 2026

AI pricing engine cutting days-to-offer to under 24 hours

Faster inventory turns mean less capital trapped in homes

The data that complicates it:

Q4 2025 net loss was $1.096B - one quarter

Q1 2026 net loss still $173M

30-year yield at 5.19% - the housing recovery this thesis needs isn't happening at these rates

Index inclusion creates a buying window. It doesn't create a business turnaround.

June 26 forced buying window. FTSE Russell updates May 29, June 5, June 12, June 18. Q2 gross profit direction is the actual signal.

5

1

13

639

May 26

$MU just hit $1 trillion. Twelve months ago it was worth $70 billion.

That is a 14x in one year. For context, it took Apple 42 years to reach $1 trillion.

Here's what actually drove it - and it was not the memory cycle people have been trading for 20 years.

The AI datacenter buildout changed the demand structure for memory permanently. HBM3E - the high-bandwidth memory stacked directly onto NVIDIA's Blackwell GPUs - has margins three times higher than standard DRAM. Micron spent years being a commodity. It is now a critical path supplier to the most important infrastructure buildout of the decade.

The numbers that explain the move:

HBM revenue tripled YoY last quarter

Gross margins expanded from 22% to 38% in 12 months

Every Blackwell GPU requires Micron, Samsung, or SK Hynix HBM - and Samsung's yield issues gave Micron share it was not supposed to have

The risk worth knowing: Samsung is fixing those yield problems. SK Hynix is adding capacity. The supply advantage Micron has right now has a shelf life.

$1 trillion is the market pricing in the new margin structure holding. The next two earnings prints will tell you whether it does.

BREAKING: Micron stock, $MU, officially hits $1 trillion in market cap for the first time in history.

12 months ago, this stock was worth just $70 billion.

2

1

131

May 25

Microsoft invited a rival tool into its own engineering teams. Engineers picked it over Microsoft's own product. Microsoft cancelled it.

That is a Copilot problem.

The detail that matters: Claude models are not banned. They still run inside Copilot and Azure Foundry. Only the interface is going away - because the interface was winning.

June 30 cutoff. End of Microsoft's fiscal year. The timing does not need explanation.

What this actually signals for the market: the 2024 "try everything" phase of enterprise AI tooling is over. Finance teams are now making the calls that engineering teams used to make. Productivity has to justify the line item.

That shift hits every third-party AI tool vendor. Not just Anthropic.

May 25

Microsoft, $MSFT, has started canceling Claude Code licenses, per the Verge

2

2

212

May 22

Nobody's talking about how $SATA and $ASST actually work. Here's the mechanic in plain English.

Strive issues SATA preferred stock at $100 paying 13% annually - starting June 16, that dividend hits every single business day. They take the proceeds and buy Bitcoin. 15,009 BTC on the balance sheet. Cash reserves cover 19 years of interest regardless of where BTC trades.

The flywheel:

SATA issuance → more BTC bought → NAV premium expands → $ASST stock rises

$ASST at a premium → easier to issue more SATA → repeat

It's not a bond. It's a capital markets confidence instrument that runs on BTC momentum.

The catch: this runs in reverse just as fast. BTC drops hard, SATA trades below par, issuance stops, accumulation stops, premium collapses.

Tuttle Capital just filed an ETF to wrap both $SATA and Strategy's $STRC into one product. When that gets approved, this structure gets its first real institutional on-ramp.

Worth understanding before it gets crowded.

May 22

2

182

May 21

This post has the right instinct. Here's the full picture before you trade on it.

RAMageddon is real - and deliberately engineered:

• DDR5 went from $6.84 in Sept 2025 to $27.20 in Dec 2025 - 297% in 3 months

• Goldman forecasts 4.9% DRAM undersupply in 2026 - worst in 15 years

• Every HBM wafer requires 3x the capacity of a DDR5 wafer - $MU, $HXCO and $SSNLF are choosing margins over volume on purpose

• OpenAI's Stargate alone locked up ~40% of global DRAM output

The China disruption thesis is real but has a timeline problem:

• Chinese DRAM fabs (CXMT) are 2-3 generations behind on process nodes

• New fab capacity - including Micron's Idaho facility - doesn't hit meaningful volume until 2027 at earliest

• Samsung and SK Hynix have explicitly told investors they are NOT pursuing aggressive capacity expansion

The stock read-through:

• $MU most exposed to a price reversal - pure commodity DRAM play

• $NVDA and the hyperscalers actually want prices lower - cheaper memory = cheaper AI compute

If China floods the market, $MU gets hurt first and hardest

The cartel cracks eventually. Just probably not within a year.

Pay attention to CXMT yield rates and process node progress. That's the real timeline indicator.

May 21

🚨 THE MEMORY CARTEL IS ABOUT TO FALL.

Ex-Samsung chip boss says heavy Chinese investment in the memory market could crush the 414% DDR5 price spike within a year.

Goldman calls it RAMageddon.

Samsung, SK Hynix, and Micron control 70% of global DRAM and pushed prices from $6.84 to $27.20 in 3 months.

Now China is gearing up to flood the market.

Cheap memory = cheap AI compute = the cartel cracks.

10

11

680

May 20

The EU reviewing MiCA 6 weeks before its own deadline is the proof of concept.

MiCA full enforcement: July 1, 2026. 18% of European crypto platforms have already shut down rather than comply. €540M in fines issued since enforcement began. And now the European Commission is reviewing the framework before the ink is dry.

That's what U.S. policy leadership looks like in practice:

CLARITY Act advancing through Senate - SEC and CFTC signed an MoU on March 11 ending years of jurisdictional turf wars

Japan reviewing MiCA to align with U.S. framework - cutting crypto capital gains tax from 55% to flat 20%

EU scrambling to review stablecoin rules - French Finance Minister already called the current euro stablecoin landscape "not satisfactory"

South Korea, UK, Singapore all moving toward U.S.-compatible frameworks simultaneously

MiCA took years to build and is already being reconsidered. The CLARITY Act hasn't even passed yet and it's already setting the global standard.

The countries that move fast get the capital. The ones that don't get regulatory arbitrage - firms simply incorporate elsewhere.

Waiting for: CLARITY Act Senate vote June-July. Every jurisdiction that aligns with it gets institutional crypto flows. Every one that doesn't loses them.

May 20

🚨 That’s what I said: The rest of the world will follow the United States on crypto policy. They can’t afford not to.

3

4

116

May 19

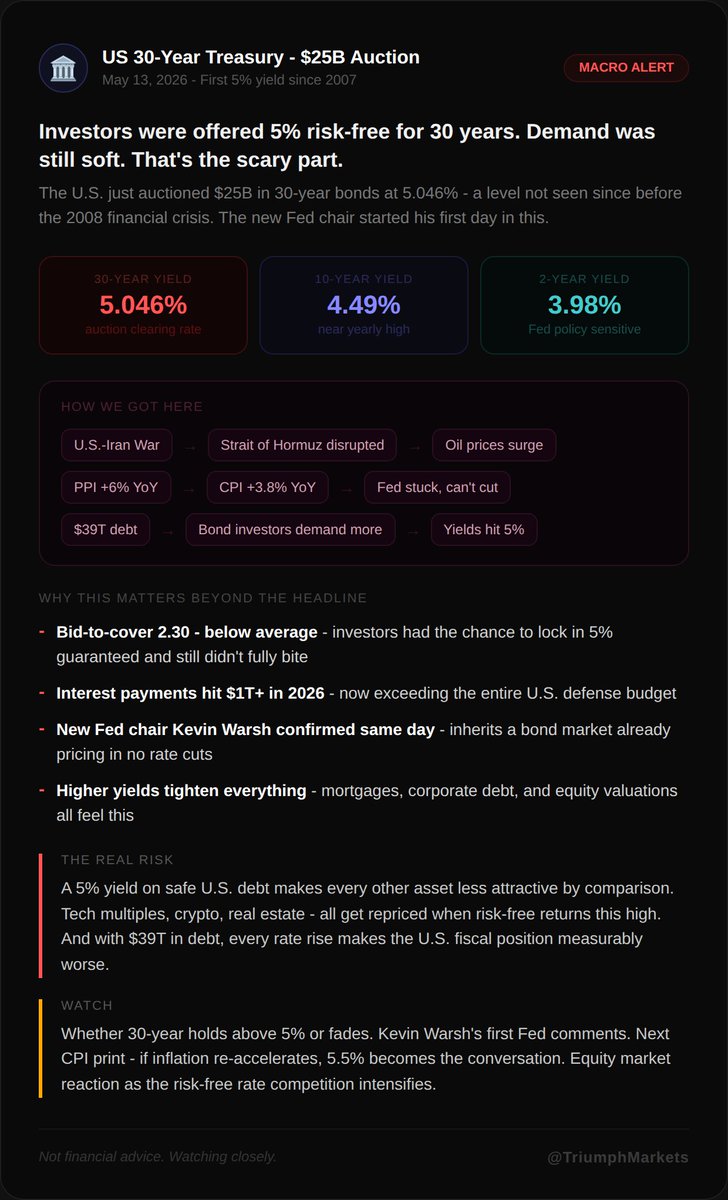

The thread explains what's happening. Here's what it means for what you actually own.

30Y at 5.19%. 10Y at 4.687%. Mortgage rate today: 6.41%. S&P down 0.8%. Nasdaq down 1.2%. Third red session in a row.

What this reprices right now:

Every growth stock with earnings weighted 5-10 years out gets hit hardest - higher discount rate, lower present value. That's most of tech

Mortgage rates heading toward 6.5% - the housing recovery just got colder

$39T in U.S. debt compounds faster at every uptick - interest payments already exceed defense spending

The number that changes everything: 62% of global fund managers in the BofA survey expect the 30Y to hit 6%. BMO's rates chief says 5.25% triggers a "more durable pullback" in equity valuations. We're 6bps away.

The Fed is paralyzed. Traders are now pricing in a hike, not a cut.

Just observe: 5.25% on the 30Y. That's the line BMO flagged. If it breaks, the equity repricing this thread is warning about becomes structural, not just noise.

Bond markets are flashing red.

Today, the US 30Y Note Yield officially hit its highest level since July 2007, at 5.19%.

This will soon become Americans’ biggest problem, yet the vast majority do not even know it is happening.

What is happening? Let us explain.

(a thread)

97

May 18

the chart says it all. here's why it's happening.

ETH/ETH/ ETH/BTC ratio sitting near 0.028 - down 35% from its August peak. well below the 200-week moving average of 0.048.

this isn't random. three structural reasons:

BTC ETF inflows dwarf ETH. Bitcoin ETFs pulling $16B vs ETH a fraction of that - institutions chose simplicity

ETH ETFs still seeing outflows. The institutional demand floor that supported ETH in 2025 has cracked

L2 networks are cannibalizing ETH fees - more transactions, less economic weight on mainnet

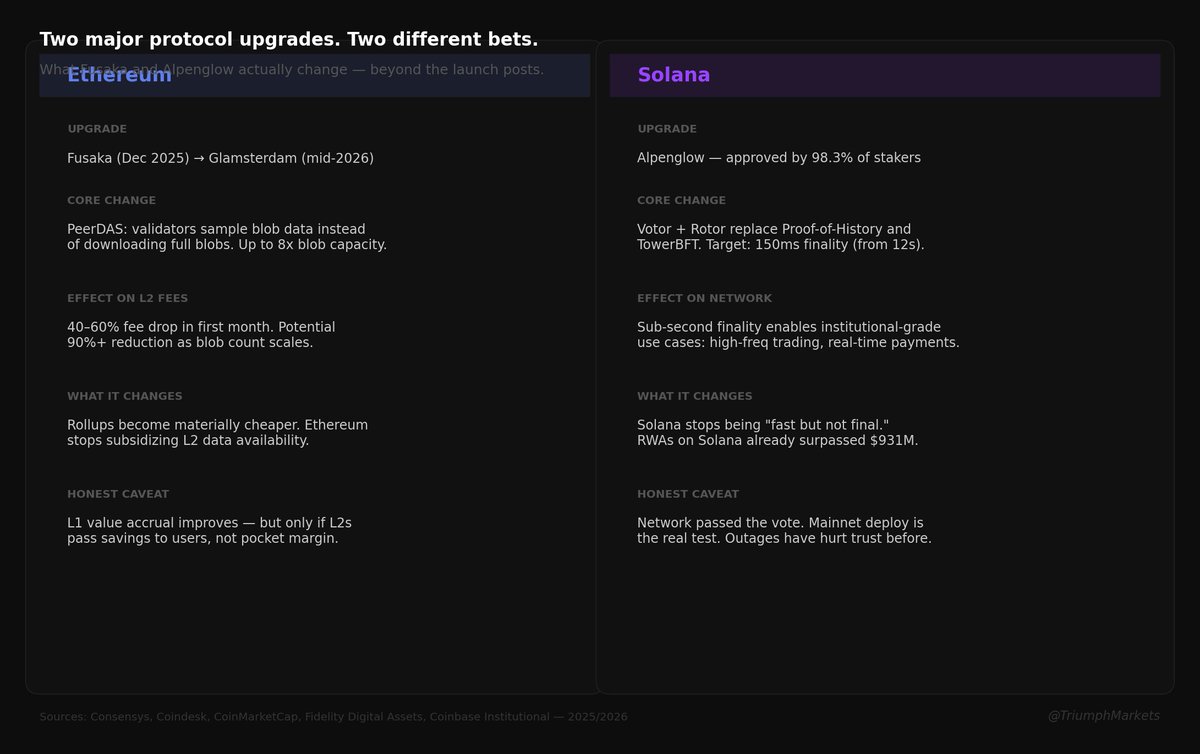

The bull case for a reversal: Glamsterdam upgrade due H1 2026. Staking ETFs in the pipeline. ETH/BTC ratio this stretched has historically snapped back hard.

watch: ETH ETF weekly flows flipping positive is the institutional signal that matters. until then the ratio has no floor.

6

154

May 18

$ZETA calls itself the "OS for marketing." the numbers make that less crazy than it sounds.

Q1 2026:

Revenue $396M - up 50% YoY

19 straight quarters of beating and raising guidance

Full year guide raised to $1.755B

the OpenAI partnership isn't a press release - it's embedded directly into Athena, their enterprise agent. 7x more agent interactions last quarter.

the real moat: 245M US adults in a proprietary identity graph. that's what the $1T TAM actually rests on.

risk: still GAAP negative. fighting Salesforce and Adobe in every deal.

watch: whether Athena shows up as a revenue line in Q2 - not just a product feature.

May 18

$ZETA CEO David Steinberg said the company’s vision is to become “the operating system” for clients entire marketing ecosystem.

Zeta also announced an OpenAI advertising partnership as it positions itself as an AI business intelligence platform targeting a $1T TAM.

8

268

May 18

before you buy that dip, here's what the tweet didn't tell you.

$IREN bull case is real. $9.7B Microsoft deal, NVIDIA partnership, 5GW owned power, $70 consensus price target.

but right now:

Q3 revenue missed by 34% - $144.8M vs $219.9M expected

Notes offering upsized to $3B - shares outstanding already up 53% in one year

JPMorgan Underweight. Flagged complex structure and GPU access uncertainty

the story isn't broken, but the dilution is just real.

know what you're buying. not financial advice.

7

2,121