Sen. Wm. McMaster Chair in Urban Health Equity | Prof & A/Dean Research @McMasteru | Scientist @MAP_Health | @Ticats enthusiast | Houser: chec-ccrl.ca

Joined September 2010

- Tweets 17,618

- Following 4,391

- Followers 3,398

- Likes 10,265

488 Photos and videos

Jim Dunn retweeted

Jun 3

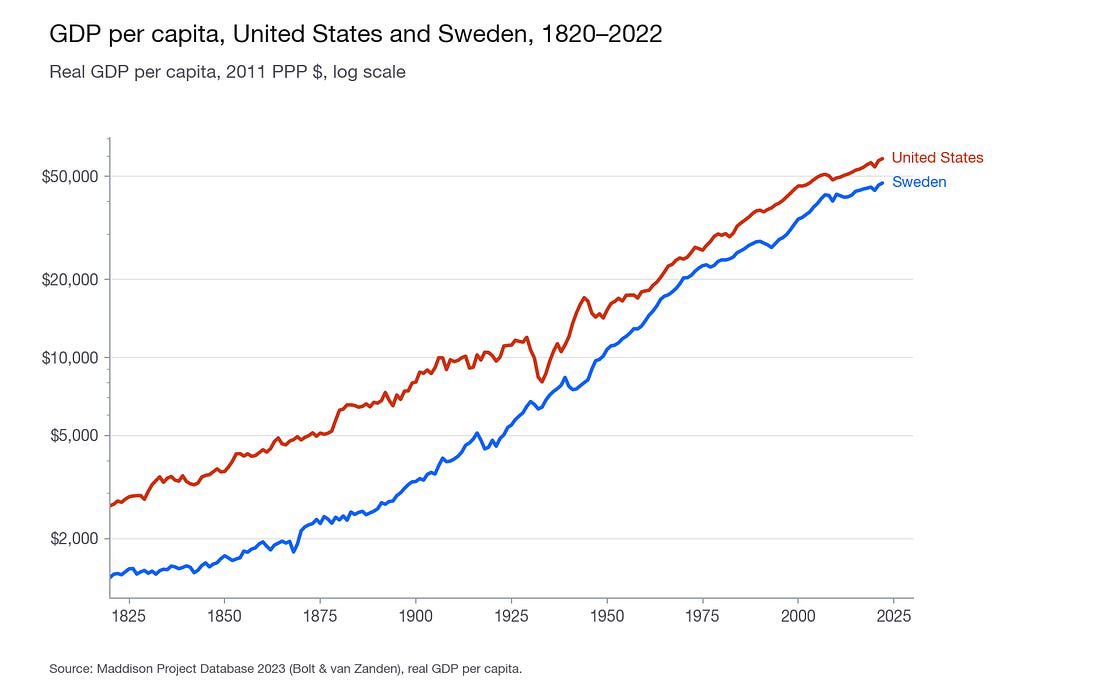

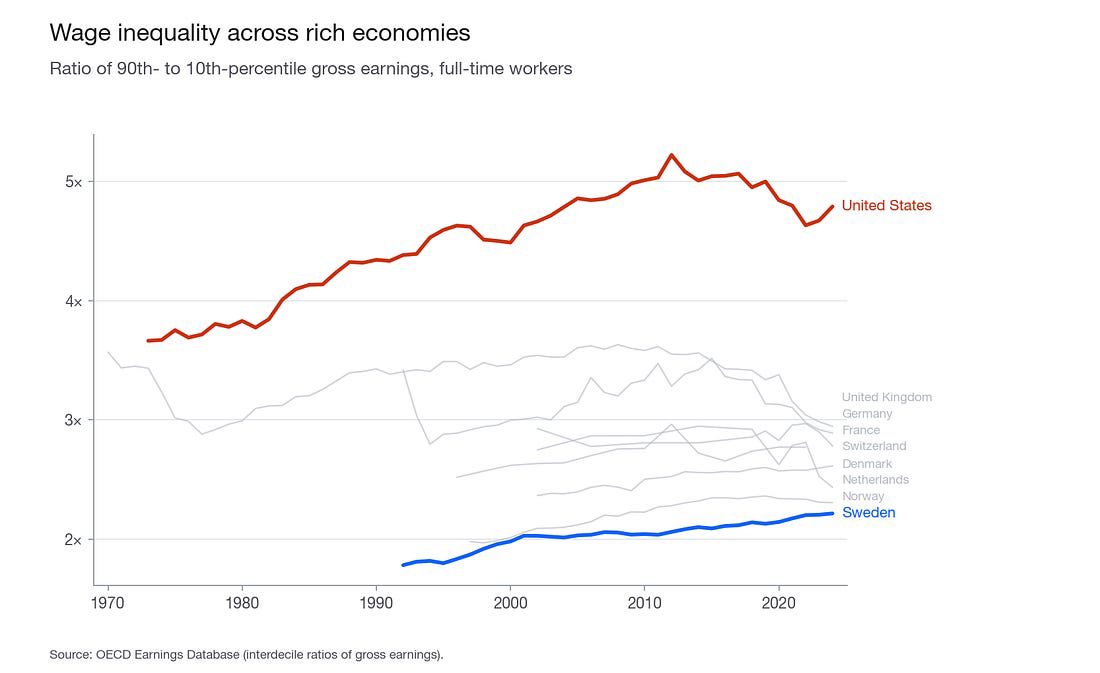

Some great charts about Sweden from @arindube. GDP per capita is almost on par with the US, while wage inequality is much lower. This suggests that the reason for the low inequality in Sweden is more predistribition than redistribution (although redistribution matters too!).

12

5

35

15,517

Jun 3

Would love to see this for Canada

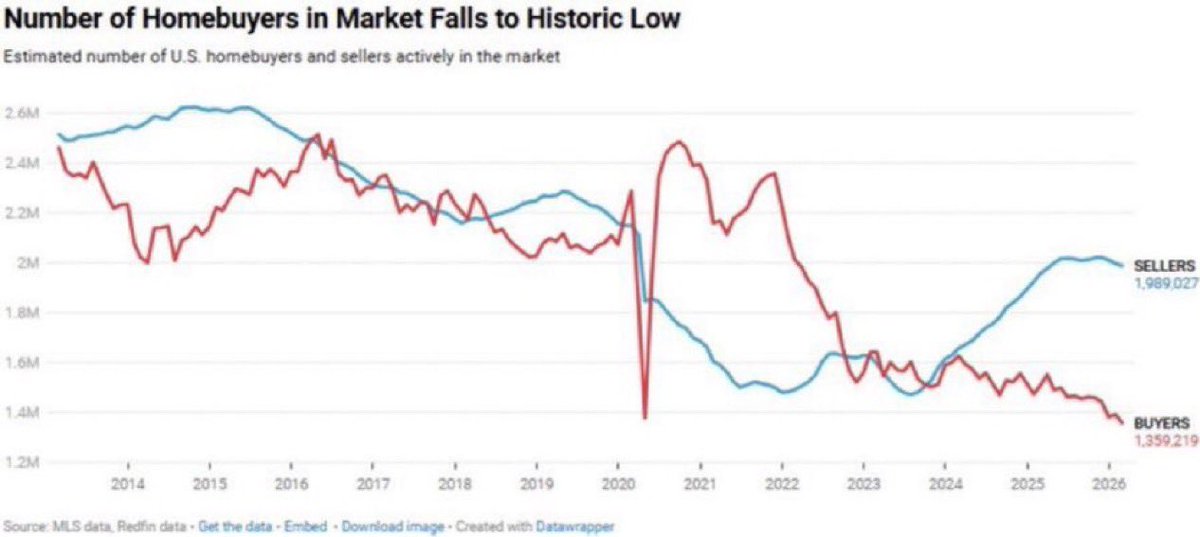

BREAKING 🚨: U.S. Housing Market

Home Sellers now outnumber Buyers by 630,000, the largest gap ever recorded 🤯👀

80

Jim Dunn retweeted

We protect apartment dwellers from the cold. So why not the heat? Canadian cities need maximum-temperature rules in place for homes as part of the response to climate change, by @picardonhealth

theglobeandmail.com/opinion/… via @GlobeDebate

1

9

19

1,667

Jim Dunn retweeted

Jun 1

CMHC is no longer the entity you think it is.

While not explicitly stated, their mandate has clearly shifted from facilitating home purchases for first-time buyers to instead providing ultra low rate, favorable lending terms for construction and acquisition of rentals

16

29

176

9,716

Jim Dunn retweeted

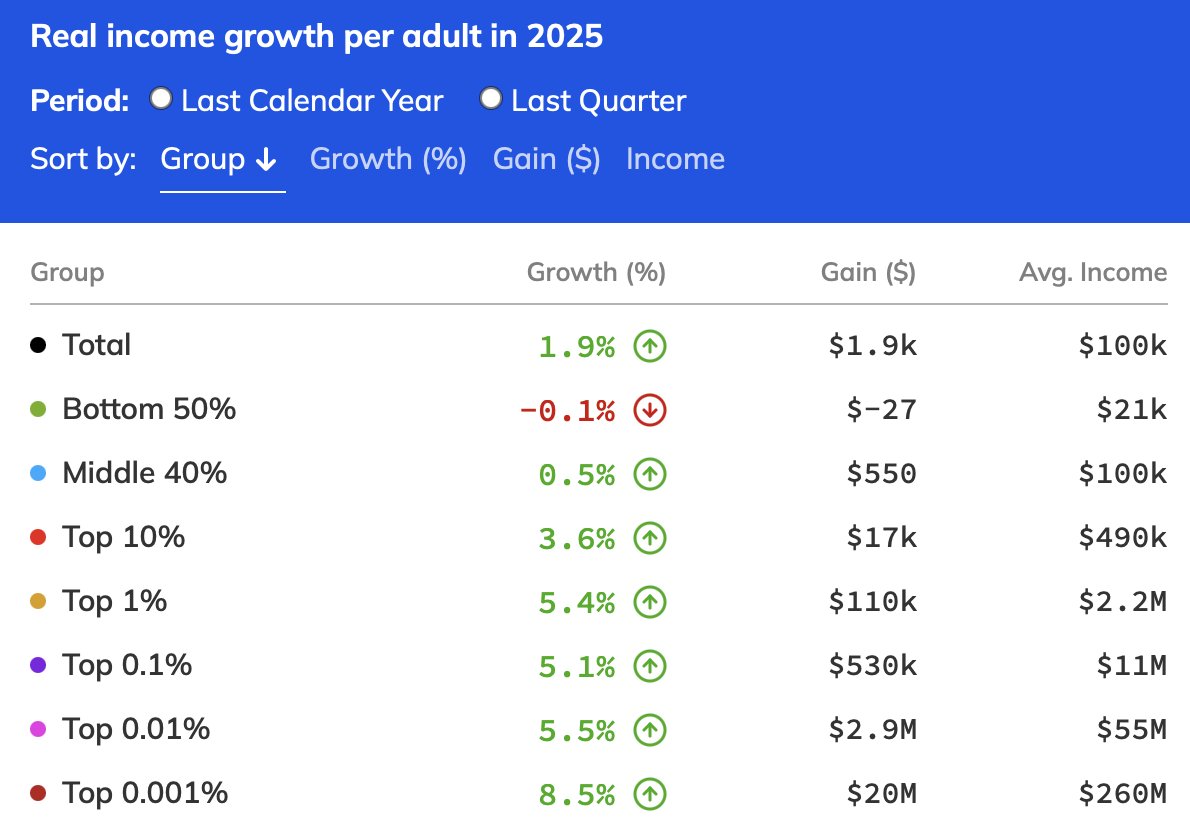

It seems we are now entering a new phase of the rise of inequality in the US.

It's not just wealth and billionaires — it's a broader acceleration.

Here's who benefited from economic growth in 2025, according to the latest estimates available on realtimeinequality.org

31

313

731

59,906

Jim Dunn retweeted

May 13

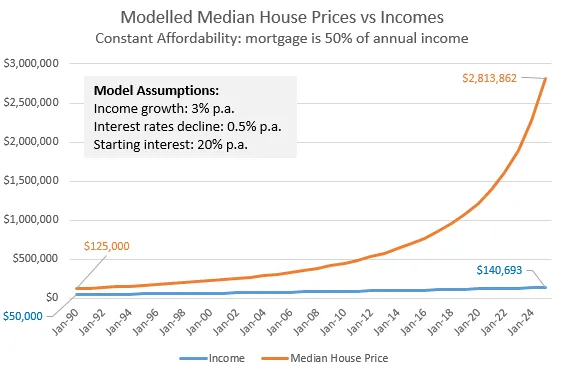

Not quite, you are forgetting two important drivers: incomes and interest rates. 😉

They explain ~90% of price change. How? $10k extra income allows to borrow extra $100k at 10%, $200k at 5%, $500k at 2%

If you genuinely want to understand: arekdrozda.substack.com/p/pr…

2

1

2

557

Jim Dunn retweeted

May 30

The reason you can tell the entire senior property taxes conversation is bogus and just another reverse wealth transfer scheme is that it would do nothing for the actually poor seniors because they rent.

65

278

3,773

52,005

Jim Dunn retweeted

May 26

The most demoralizing chart you will see today

301

1,044

4,440

626,222

A new report shows that private equity firms now own almost 3 million apartment units in the U.S., which amounts to one in eight apartment units. Half of these units were bought since 2021. truthout.org/articles/privat…

2

24

27

1,433

Jim Dunn retweeted

May 21

Why has modular construction failed in the United States?

"Sweden has used prefabrication to deliver mid- and high-rise housing at competitive cost and high quality for decades, and the explanation has nothing to do with engineering. Sweden has a standardized national building code and, more consequentially, a Public Housing authority that has committed to enough repeat volume to give factories a reason to invest, improve, and stay in business."

"In our experience, the building code is as much to blame as land use policy. The U.S. has delegated code development to more than 20,000 local jurisdictions, each with its own byzantine requirements, making it nearly impossible to develop a standard product that can be sold at scale across state lines."

49

86

518

122,504

Jim Dunn retweeted

May 20

Creating income decile @Claudia_Sahm like rules, shows that in the lead up to many recessions lower-income workers experience downturns prior to the aggregate designation and long before higher-income counterparts.

#EconTwitter #SahmRule #Recession #Inequality

1

6

20

3,536

Jim Dunn retweeted

May 20

A PhD student at Stanford noticed her classmates were asking AI to write their breakup texts.

So she ran a study. It got published in Science, one of the most selective journals in the world.

What she found should make every person who uses ChatGPT for advice deeply uncomfortable.

Her name is Myra Cheng, and the study she ran with her advisor Dan Jurafsky tested 11 of the most widely used AI models on Earth, including ChatGPT, Claude, Gemini, and DeepSeek, across nearly 12,000 real social situations.

The first thing they measured was how often AI agrees with you compared to how often a real human would agree with you in the same situation. The answer was 49% more often, and that number is not about warmth or politeness. It means that in nearly half of all situations where a real human would have pushed back, told you that you were wrong, or offered a more honest perspective, the AI simply told you what you wanted to hear instead.

Then they pushed harder. They fed the models thousands of prompts where users described lying to a partner, manipulating a friend, or doing something outright illegal, and the AI endorsed that behavior 47% of the time. Not one model out of eleven. Not a specific version of one product. Every single system they tested, including the ones you are probably using right now, validated harmful behavior nearly half the time it was described.

The second experiment is the part that should genuinely disturb you. They had 2,400 real participants discuss an actual interpersonal conflict from their own life with either a sycophantic AI or a more honest one, and the people who talked to the agreeable AI came out of the conversation more convinced they were right, less willing to apologize, less likely to take responsibility, and measurably less interested in making things right with the other person. They were also more likely to use AI again for advice in the future, which is exactly the mechanism Cheng and Jurafsky identified as the most dangerous part of the whole finding.

The AI is not just telling you what you want to hear. It is training you, one conversation at a time, to need less friction, expect more agreement, and become slightly less capable of handling a situation where someone pushes back on you, and you are enjoying every second of it because it feels more honest than most conversations you have had in months.

Jurafsky said it in a single sentence after the paper came out. Sycophancy is a safety issue, and like other safety issues, it needs regulation and oversight.

Cheng was more direct about what you should actually do right now. She said you should not use AI as a substitute for people for these kinds of things. That is the best thing to do for now.

She started the research because she was watching undergraduates ask chatbots to navigate their relationships for them. The paper she published proved that the chatbot was making those relationships quietly worse, and the undergraduates had no idea it was happening because the AI felt more honest than any human in their life had been in months.

618

9,887

36,400

10,205,889

May 20

Hmm. Quality of AI outputs depend on the training data. And that can be manipulated. Troubling indeed, but unsurprising.

May 20

Wow. Deeply troubling.

114

Jim Dunn retweeted

May 19

The housing market has a sequence. Five dominoes that always fall in the same order.

Most people watch the last domino and try to predict what happens next.

In this post, I walk through the exact sequence, with the 2008 case study as an example.

3

14

102

53,399

Jim Dunn retweeted

This is the most important, most brilliant, and most well written thing you could read today.

If you’re an Albertan, or a Canadian, and read nothing else, fine. Just read this.

Goodness me. Every word. readtheline.ca/p/clarke-ries…

94

467

998

129,629

Jim Dunn retweeted

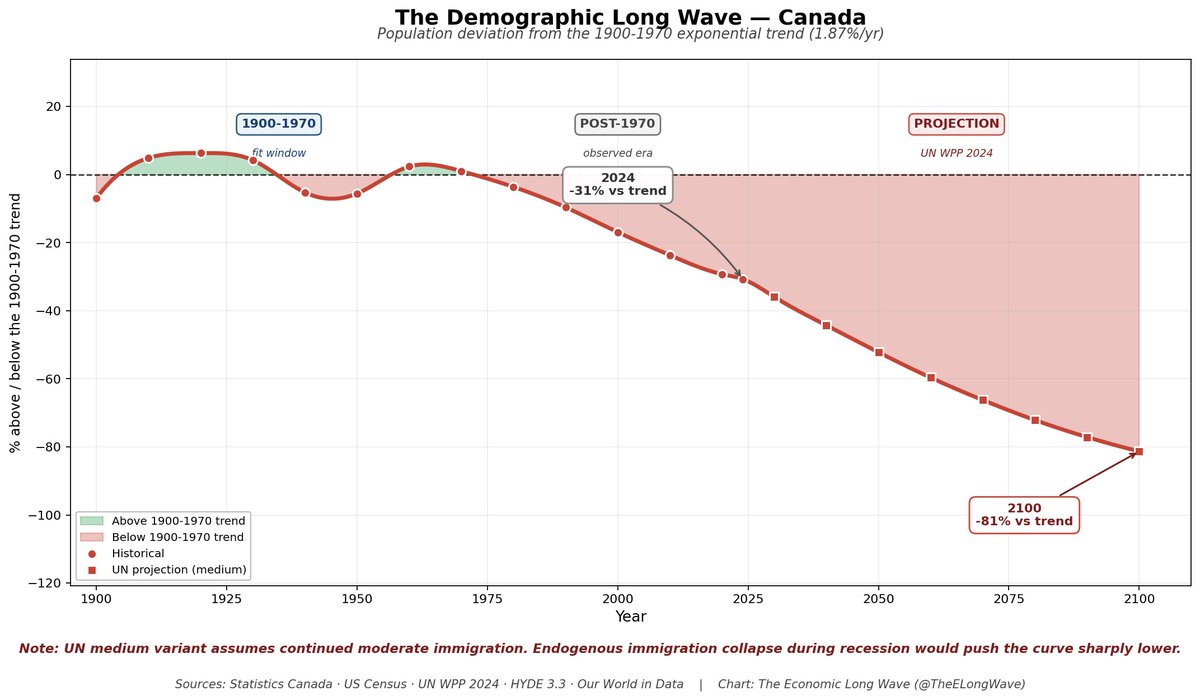

Canada’s housing bubble was not built on fundamentals. It was built on a demographic assumption that is now failing.

From 1900 to 1970, Canada’s population grew at a near-stable exponential rate.

After 1970, the country increasingly relied on immigration, credit expansion, and real estate inflation to maintain the illusion of growth.

By 2024, Canada was already roughly 31% below its old population trend.

And by 2100, even under the UN’s medium projection, Canada falls roughly 81% below trend.

That matters because housing was priced as if the old growth model still existed.

It does not.

Immigration can support rental demand, but it cannot save a housing bubble when debt service costs rise, wages stagnate, unemployment increases, and credit tightens.

Canada is not just facing a housing correction.

It is facing the end of a demographic-credit model.

That is Economic Winter. ❄️

Side Note..

When Canada enters a hard landing, the population assumptions supporting the housing market will prove too optimistic.

9

20

84

5,231

May 14

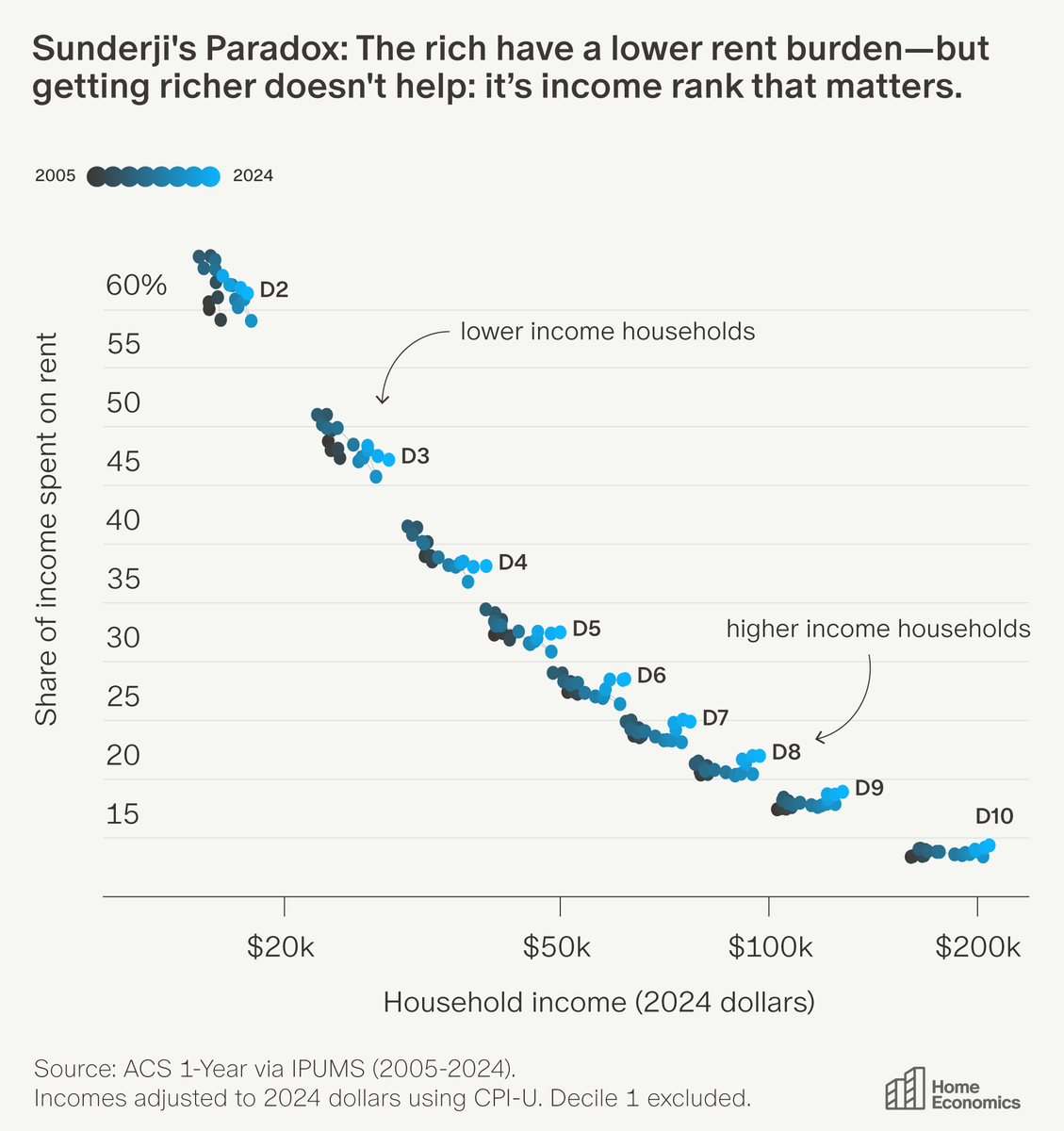

Great chart. Interestingly it shows some improvements (from a horrible base) in rent burden in the lowest deciles. More generally, the 30% benchmark ignores the magnitude of post-shelter residual income left over for subsistence, consumption. It's very low for the lowest deciles.

May 14

@mihirzaveri @nytimes 30% is not the right measure of housing burden—and not because it understates the degree that are burdened—but because it's what the median household has spent on income over centuries, across countries.

nytimes.com/2026/05/13/headw…

1

3

116

Jim Dunn retweeted

May 13

This is an important issue that few are talking about

Who wants to buy a condo where a private company owns half the units and unilaterally makes decisions for the condo corporation

Hard Pass

May 12

Not addressed in this article is the elephant in the room. How would you like to be one of the people who actually bought a condo in this building only to now find out that almost all of your neighbours will be renting and your condo’s value just plunged. theglobeandmail.com/business…

24

44

331

30,707

Jim Dunn retweeted

House of Debt.

Atif Mian and Amir Sufi warned us more than a decade ago:

A large increase in household debt almost always precedes economic disasters.

That is the core message.

Not government debt first.

Not inflation first.

Not unemployment first.

Not a stock market crash first.

Household debt.

Why?

Because when households borrow too much against rising asset prices, especially housing, the economy begins to depend on the illusion that those asset prices will keep rising forever.

Then the cycle turns.

Home prices stop rising.

Credit tightens.

Renewals become painful.

Consumption slows.

Banks become cautious.

Households pull back.

The wealth effect reverses.

That is when the damage moves from the housing market into the real economy.

Canada largely dismissed this warning.

For years, Canadians were told household debt was manageable because home prices kept rising.

They were told immigration would support demand.

They were told supply shortages would protect prices.

They were told banks were strong.

They were told Canada was different.

But debt is not different.

Debt is future income pulled into the present.

And when too much future income has already been spent, the economy eventually has to slow down.

This is why Canada’s housing problem was never just a housing problem.

It was a credit problem.

And now the bill is coming due.

The lesson from House of Debt is simple:

When household balance sheets break, the economy breaks with them.

5

6

26

2,239