Joined December 2016

- Tweets 18,568

- Following 430

- Followers 5,009

- Likes 12,566

1,357 Photos and videos

Pinned Tweet

#geo

Well done to Tom Harris and the team @geoexpltd.

👏 Fantastic 👏

Stay tuned for further updates via RNS.

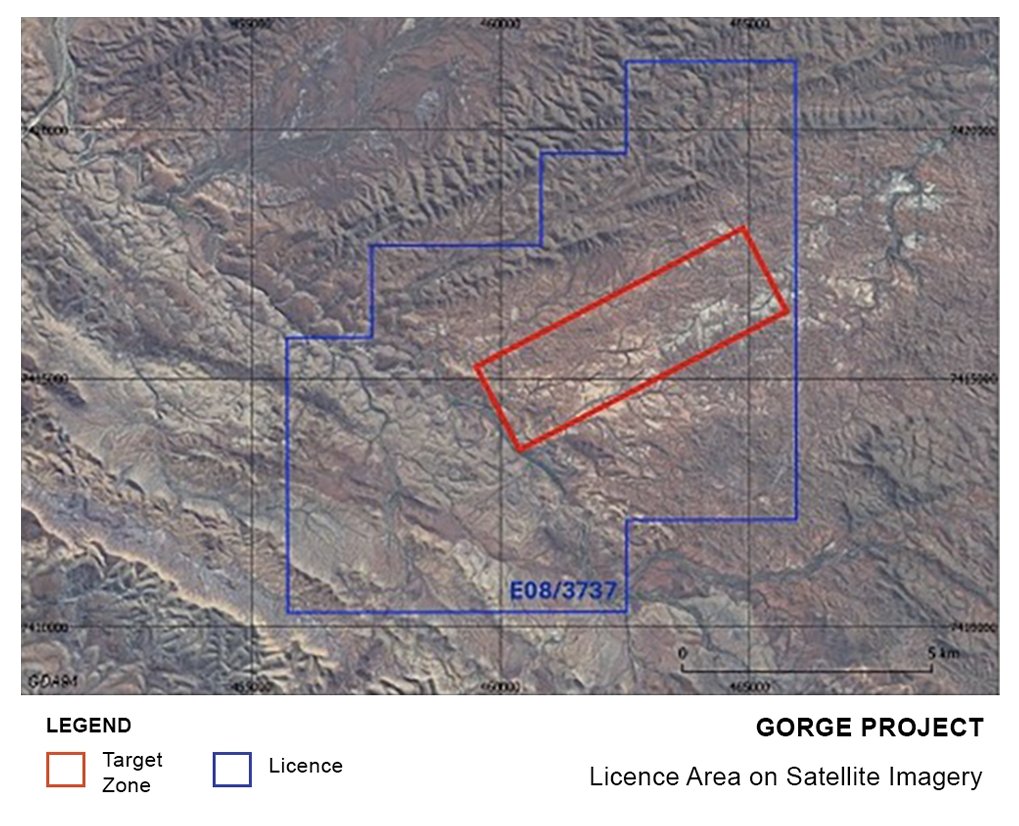

#GEO is pleased to share a final on-site update from our Exploration Manager, Tom Harris, following two weeks of field activities at the Gorge Project in Western Australia.

Recorded shortly before departing the project site, Tom provides an update on the progress made during the recent work programme.

During the programme, the GEO team successfully completed geological reconnaissance and mapping across the project area, advancing our understanding of the geological setting and prospectivity of the Gorge Project.

This phase of fieldwork marks an important step in progressing the project towards future drill target generation and a maiden drilling campaign.

Watch Tom’s update from the Gorge Project below 👇

#Mining #Exploration #GoldExploration #Australia #Gold #Copper #Silver

1

5

797

#geo

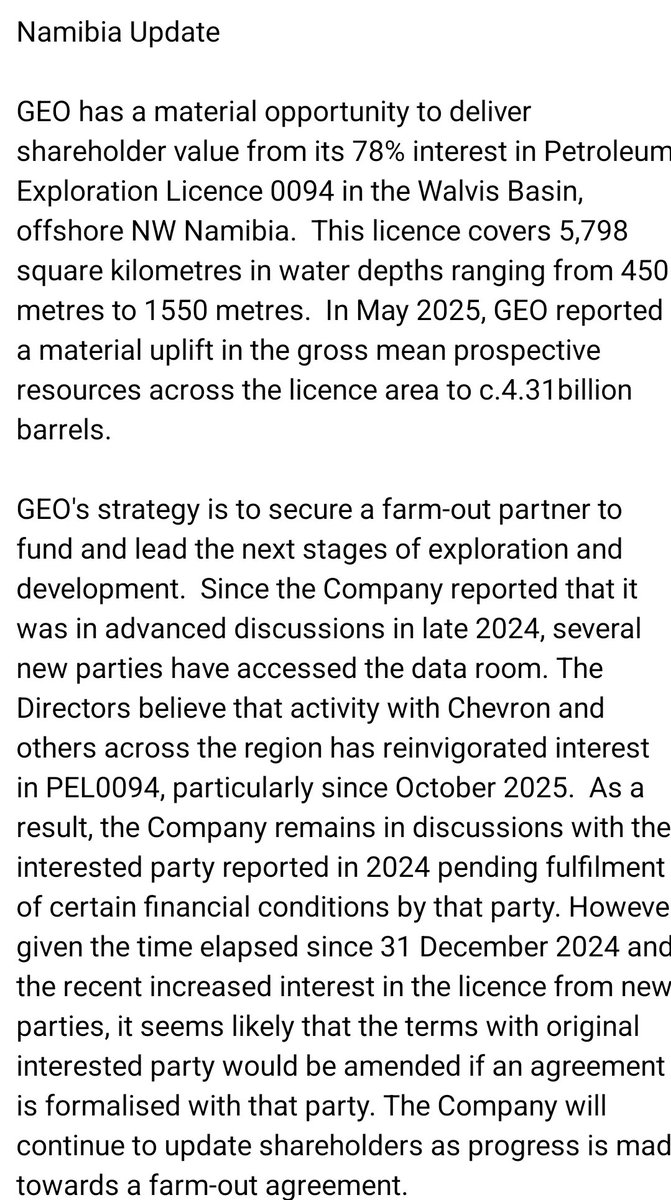

This is a very significant new development for the Walvis bay.

theextractormagazine.com/202…

2

7

503

Omar Ahmad retweeted

Jun 4

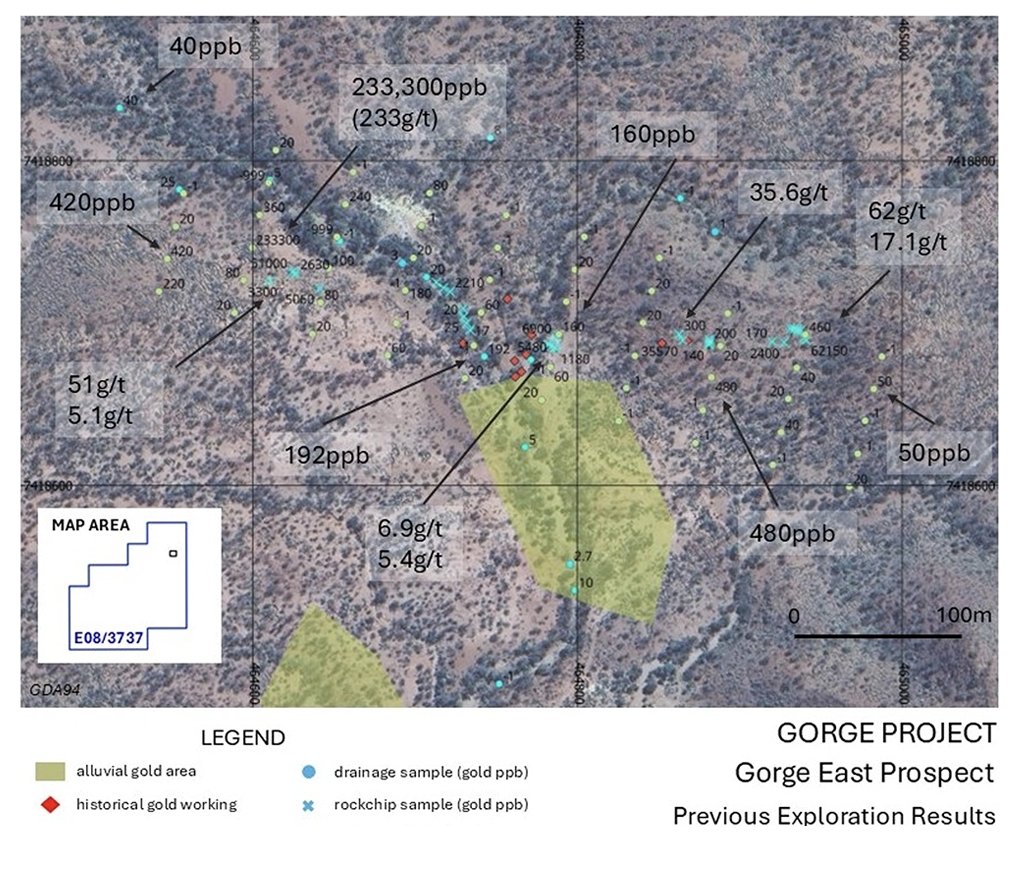

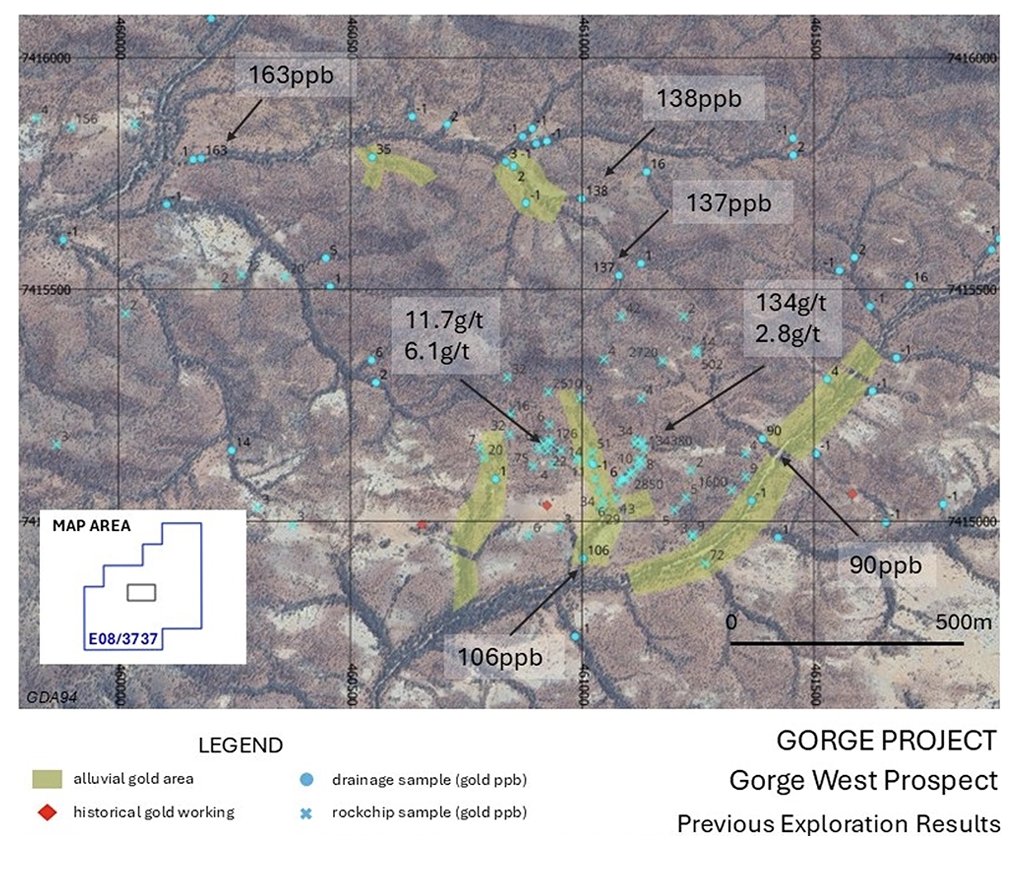

@geoexpltd (AIM #GEO) has completed the initial field reconnaissance programme at its Gorge Project in Western Australia, a key step in its 2026 exploration efforts. This work, following recent airborne surveys, involved validating historical geochemical results, confirming old workings and drill sites, geological mapping, and conducting orientation soil geochemistry over known gold mineralisation areas.

@ValueAimTrader, Chief Executive Officer of GEO Exploration Limited, commented “We are pleased to confirm completion of the initial field reconnaissance at Gorge, marking another key step in advancing our 2026 exploration programme.

The trip was very positive, with the team completing all planned objectives and gathering valuable geological information that strengthens our understanding of the Gorge Project, and the initial signs are exactly what we were expecting to see.

Momentum continues to build as we move through a disciplined, systematic exploration process ahead of our maiden drilling campaign, and shareholders can expect further updates shortly as the reconnaissance findings and technical interpretation are finalised.”

🔗 Read the full update here: share-talk.com/geo-explorati…

Jun 2

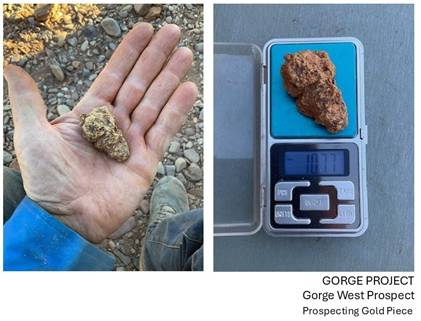

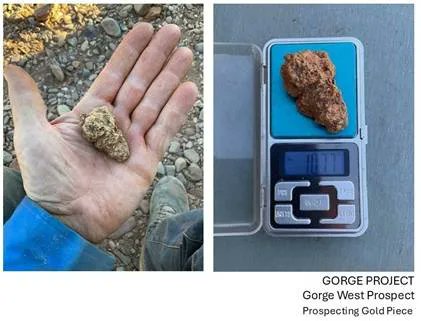

@geoexpltd (AIM #GEO) has successfully completed a fixed-wing magnetic and radiometric survey at its Gorge Project, located in Western Australia, ahead of schedule. Field reconnaissance activities are also underway, including geological mapping and validation of historical workings, which have previously shown significant gold mineralisation with rock chip samples up to 134g/t Au and soil samples up to 233g/t Au, alongside the recovery of gold nuggets.

@ValueAimTrader, Chief Executive Officer of GEO Exploration Limited, commented

"We are pleased with the continued progress being made at Gorge, with the airborne magnetic and radiometric survey now completed ahead of schedule and field reconnaissance activities still underway on site.

Momentum is clearly building across the project. The completion of this survey represents an important step in refining our geological understanding of Gorge and will assist in prioritising targets for follow-up geochemistry and drilling.

With Tom Harris on-site leading field activities, we are moving quickly and methodically through the planned exploration work programme. We look forward to updating shareholders as the results of this work are received and interpreted."

🔗 Read the full update here: share-talk.com/geo-explorati…

10

17

2,968

RT @geoexpltd: #GEO is pleased to confirm that the initial field reconnaissance programme at the Gorge Project in Western Australia has now…

7

RT @geoexpltd: #GEO is pleased to confirm that the fixed-wing magnetic and radiometric survey at the Gorge Project in Western Australia was…

4

Omar Ahmad retweeted

Jun 2

@geoexpltd (AIM #GEO) has successfully completed a fixed-wing magnetic and radiometric survey at its Gorge Project, located in Western Australia, ahead of schedule. Field reconnaissance activities are also underway, including geological mapping and validation of historical workings, which have previously shown significant gold mineralisation with rock chip samples up to 134g/t Au and soil samples up to 233g/t Au, alongside the recovery of gold nuggets.

@ValueAimTrader, Chief Executive Officer of GEO Exploration Limited, commented

"We are pleased with the continued progress being made at Gorge, with the airborne magnetic and radiometric survey now completed ahead of schedule and field reconnaissance activities still underway on site.

Momentum is clearly building across the project. The completion of this survey represents an important step in refining our geological understanding of Gorge and will assist in prioritising targets for follow-up geochemistry and drilling.

With Tom Harris on-site leading field activities, we are moving quickly and methodically through the planned exploration work programme. We look forward to updating shareholders as the results of this work are received and interpreted."

🔗 Read the full update here: share-talk.com/geo-explorati…

May 25

@geoexpltd has moved from a small oil and gas optionality story into a broader exploration vehicle with Western Australian gold projects at the centre of its near term activity. The founding director of Greatland connection, is why Callum Baxter matters

share-talk.com/geo-explorati…

6

10

4,416

May 31

RT @geoexpltd: #GEO confirms that Tom Harris remains on site at the Gorge Project in Western Australia and continues to support ongoing exp…

13

Omar Ahmad retweeted

#GEO is pleased to confirm that airborne geophysical surveying is now being carried out at the Gorge Project in Western Australia as part of the planned exploration programme.

The survey forms a key component of GEO’s wider work programme, which also includes geological reconnaissance and mapping, aimed at refining structural interpretation and defining priority drill targets ahead of future drilling.

Please see the video below featuring our Exploration Manager, Tom Harris, providing an update on the airborne survey currently being undertaken at site👇

#Mining #Exploration #GoldExploration #Australia #Gold #Copper #Silver

8

20

841

May 27

RT @geoexpltd: #GEO confirms that our Exploration Manager, Tom Harris, is currently on site at the Gorge Project in Western Australia, wher…

4

Omar Ahmad retweeted

May 20

@geoexpltd Exploration Manager Tom Harris is currently on site at #GEO’s Gorge Project in Western Australia, bringing direct discovery experience from the world-class Havieron project.

Harris previously worked alongside Callum Baxter at #GGP during the development of the Havieron discovery, one of Australia’s most significant recent gold-copper discoveries. Together they will also explore new opportunities should they arise in the future. @ValueAimTrader

#GEO is pleased to confirm that our Exploration Manager, Tom Harris, is currently on site at the Gorge Project in Western Australia.

Following our 7 May 2026 RNS announcing the planned geological reconnaissance, mapping and airborne geophysical surveys programme for Gorge Project.

Work is now progressing on the ground as GEO advances towards defining priority drill targets and a maiden drilling campaign.

#Mining #Exploration #GoldExploration #Australia #Gold #Copper #Silver

7

12

2,319

May 22

RT @geoexpltd: #GEO is pleased to confirm that our Exploration Manager, Tom Harris, is currently on site at the Gorge Project in Western Au…

8

May 20

RT @geoexpltd: 🎥 Missed last week’s RNS? Here’s a quick recap:

#GEO announced planned exploration activities at the Gorge Project, marking…

3

May 20

RT @geoexpltd: #GEO is pleased to confirm that our leadership team recently attended the Africa Energies Summit 2026 in London.

Our Chief…

8

1

May 20

RT @geoexpltd: Following the Africa Energies Summit 2026 in London, our Chief Executive Officer, Omar Ahmad, highlighted continued industry…

4

1

Omar Ahmad retweeted

May 19

@geoexpltd Africa Energies Summit 2026 #GEO The event supported valuable discussions around exploration, investment, and partnership opportunities, including continued engagement relating to exploration licence PEL0094 in the Walvis Basin, offshore Namibia. @ValueAimTrader

#GEO Exploration Limited's leadership team noted that the Africa Energies Summit 2026 provided an excellent opportunity to engage with industry peers, investors, and technical experts across the global energy sector.

The event supported valuable discussions around exploration, investment, and partnership opportunities, including continued engagement relating to exploration licence PEL0094 in the Walvis Basin, offshore Namibia.

#AfricaEnergiesSummit #Energy #OilAndGas #AfricaEnergy #Exploration #WalvisBasin #Namibia

6

7

1,287

Omar Ahmad retweeted

May 11

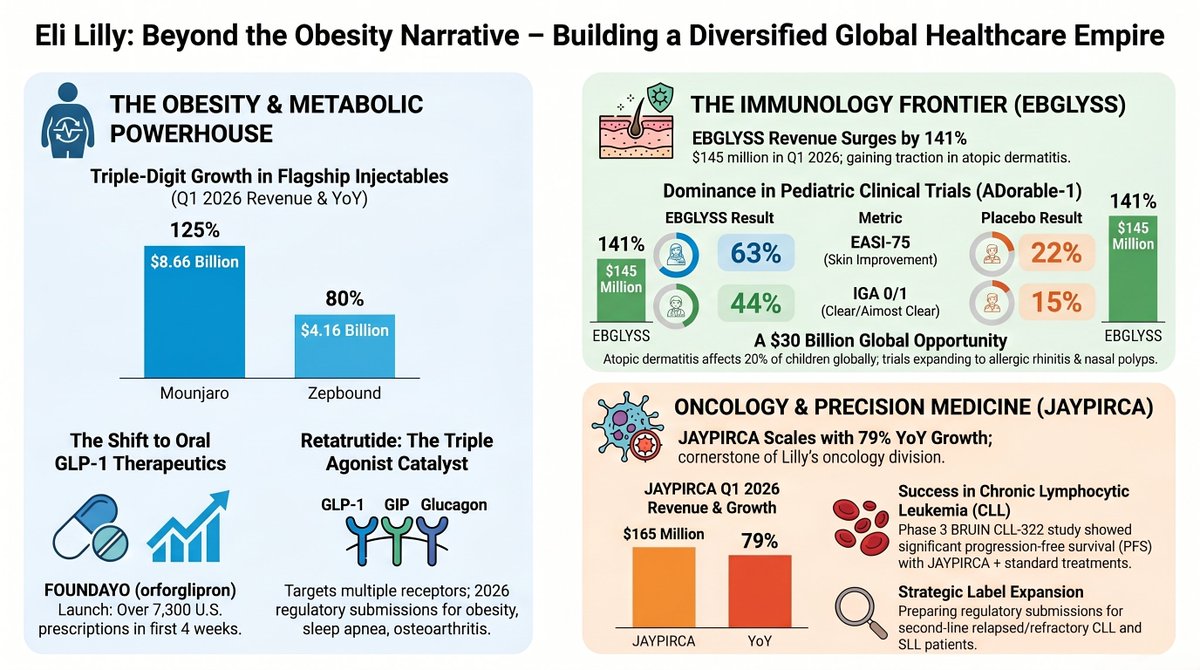

Eli Lilly Is Quietly Building A Healthcare Empire Beyond GLP-1s

When most investors think about Eli Lilly $LLY , they immediately think about one thing: obesity drugs.

And honestly, that makes sense.

Mounjaro and Zepbound have completely changed the trajectory of the company.

These drugs are growing at a pace that very few blockbuster medicines in history have achieved.

But I think the market is still missing the bigger picture here.

This is no longer just an obesity story.

What I believe investors are underestimating is that Eli Lilly is quietly transforming itself into something much larger: a diversified healthcare powerhouse with multiple growth engines operating simultaneously across obesity, diabetes, immunology, oncology, and potentially even oral GLP-1 therapeutics.

The reason this matters is because markets eventually punish single-product dependency.

We’ve seen it happen over and over again in pharma. The moment growth slows in one flagship drug, sentiment collapses.

But Lilly is positioning itself differently.

The company is not sitting still while Mounjaro and Zepbound dominate headlines.

It is aggressively expanding labels, acquiring new assets, developing next-generation obesity treatments, and scaling entirely new therapeutic franchises that could contribute meaningful revenue growth over the next decade.

That’s why despite the massive rally in the stock, I still maintain a “Strong Buy” rating.

And after looking through the Q1 2026 results in detail, I actually think the bull case is becoming stronger, not weaker.

The Market Is Obsessed With Obesity, But Lilly’s Pipeline Is Becoming Much Bigger

The obvious starting point here is still Mounjaro and Zepbound because the numbers are honestly absurd.

Mounjaro generated $8.66 billion in Q1 2026 revenue, up 125% year-over-year.

Zepbound generated another $4.16 billion, growing 80% year-over-year.

Think about how unusual this is.

Most pharmaceutical companies would consider themselves fortunate to have a single multi-billion-dollar blockbuster growing at double digits.

Lilly now has two mega-blockbusters growing at rates that resemble early-stage software companies.

And importantly, this growth is still happening despite increasing competitive pressure from Novo Nordisk.

That matters because the narrative around the obesity market lately has started to shift toward “competition risk.” But when I look at the actual numbers, I simply do not see a company losing momentum.

I see a company that is still gaining scale faster than competitors can fully respond.

What’s even more interesting to me is that Lilly is already preparing for the next phase of the obesity war.

The FDA approval and launch of FOUNDAYO (orforglipron) changes the equation because oral GLP-1 adoption could massively expand the addressable market beyond injectable therapies.

Within just four weeks of launch, FOUNDAYO already generated more than 7,300 U.S. prescriptions.

Now obviously, it is still very early.

I don’t think anyone can confidently declare a winner yet between Lilly’s oral GLP-1 strategy and Novo Nordisk’s $NVO oral semaglutide ambitions.

Investors trying to make definitive conclusions after only a few weeks are probably getting ahead of themselves.

But strategically, Lilly is now attacking the obesity market from multiple angles simultaneously.

That’s the part I think investors need to focus on.

This company isn’t relying on one obesity drug.

It is building an entire obesity ecosystem.

Retatrutide Could Become The Next Major Catalyst

One of the most overlooked parts of the Lilly story right now is Retatrutide.

In my opinion, this could eventually become one of the most important assets in the entire obesity space.

Unlike current GLP-1 drugs, Retatrutide is a triple agonist targeting GLP-1, GIP, and glucagon receptors simultaneously.

And what makes this interesting is that Lilly is not just pursuing obesity alone.

The company is preparing regulatory submissions in 2026 targeting:

🔹Obesity

🔹Sleep apnea

🔹Osteoarthritis knee pain

This is where things start getting very interesting from a long-term revenue perspective.

Because obesity drugs are increasingly becoming platforms for multiple disease categories rather than standalone weight-loss therapies.

That changes the economics dramatically.

We are moving toward a world where these drugs may eventually become foundational metabolic therapies used across cardiovascular disease, sleep disorders, inflammatory conditions, liver disease, and musculoskeletal disorders.

And Lilly appears to understand this shift better than almost anyone.

The company is also advancing Eloralintide, an amylin receptor agonist, into Phase 3 trials for obesity and osteoarthritis.

Again, this reinforces the same theme.

Lilly is building depth behind its obesity franchise instead of depending entirely on one product cycle.

That kind of pipeline layering is exactly what separates temporary biotech winners from companies that can sustain growth for a decade or more.

EBGLYSS Is Becoming A Much Bigger Opportunity Than Investors Realize

While obesity dominates investor attention, I think one of the most underrated parts of Lilly’s business right now is immunology.

Specifically, EBGLYSS.

EBGLYSS (lebrikizumab) generated $145 million in Q1 2026 revenue, growing 141% year-over-year.

For many investors, that number may still seem small compared to obesity revenues.

But that misses the point entirely.

The real story here is not where EBGLYSS is today.

It’s where it could eventually go.

The company recently reported positive Phase 3 results from the ADorable-1 trial evaluating EBGLYSS in pediatric patients between 6 months and 18 years old with moderate-to-severe atopic dermatitis.

And the data was honestly very strong.

63% of patients achieved EASI-75 compared to only 22% on placebo.

Meanwhile, 44% achieved IGA 0/1 scores, representing clear or almost-clear skin, compared to only 15% on placebo.

That’s a clinically meaningful difference.

But what I think matters even more is the size of the pediatric opportunity.

Atopic dermatitis affects roughly 20% of children globally compared to about 10% of adults.

So if Lilly successfully expands the label here, the commercial opportunity becomes substantially larger.

And this is exactly the kind of expansion strategy that can quietly create multi-billion-dollar franchises over time.

The market opportunity itself is enormous.

The global atopic dermatitis market is projected to approach nearly $30 billion by 2030.

But what really caught my attention is that Lilly is already exploring EBGLYSS beyond eczema.

The company is running:

🔹PREPARED-1 in allergic rhinitis

🔹CONTRAST-NP in chronic rhinosinusitis with nasal polyps

This is important because successful immunology drugs rarely stay confined to a single indication.

Once physicians gain comfort with safety profiles and mechanisms, expansion opportunities start compounding rapidly.

We’ve seen this playbook before across multiple blockbuster immunology drugs.

And Lilly appears to be following the same blueprint.

JAYPIRCA Is Quietly Strengthening Lilly’s Oncology Business

Another area that I think the market is underappreciating is oncology.

JAYPIRCA generated $165 million in Q1 revenue, growing 79% year-over-year.

Again, this may look small relative to obesity.

But investors should remember that oncology franchises often scale gradually before inflecting significantly higher following label expansions.

Lilly’s Phase 3 BRUIN CLL-322 study looks particularly important.

The study evaluated:

🔹JAYPIRCA venetoclax rituximab

🔹Versus venetoclax rituximab alone

And the results showed statistically significant progression-free survival improvement.

What makes this especially interesting is the company’s focus on time-limited treatment strategies.

That could become increasingly attractive to physicians and patients because it potentially balances efficacy while limiting long-term treatment burden.

Lilly is now preparing submissions targeting second-line relapsed/refractory CLL/SLL patients.

So again, we’re seeing the same pattern.

The company is not simply launching drugs and moving on.

It is aggressively expanding commercial opportunities through additional indications and treatment settings.

That creates much more durable revenue growth than investors often realize.

I think the biggest mistake investors can make right now is viewing Eli Lilly purely as an obesity company.

Yes, obesity remains the centerpiece.

But underneath the surface, Lilly is quietly assembling one of the deepest and most diversified pipelines in large-cap pharma.

Mounjaro and Zepbound continue growing at astonishing rates.

FOUNDAYO gives Lilly exposure to the potentially massive oral GLP-1 market.

Retatrutide could eventually become one of the most important next-generation obesity therapies in development.

1

1

4

909

May 11

$LLY 2000 level looks like a target here. What a solid business with solid revenues and profits. These pharmas can move v quickly is one thing I realised over the years.

410

May 11

RT @geoexpltd: #GEO is pleased to share that our Chief Financial Officer, Hamza Choudhry, is attending the 121 Mining Investment event.

We…

2