Senior Equity Analyst at ByteTree | CFA Charterholder | Focused on quality investing | Views my own, not investment advice.

Joined March 2019

- Tweets 3,380

- Following 466

- Followers 555

- Likes 7,455

541 Photos and videos

Pinned Tweet

Jan 30

“A great business at a fair price is superior to a fair business at a great price… The investment game always involves considering both quality and price, and the trick is to get more quality than you pay for in price. It’s just that simple." - Charlie Munger

@ByteTree Quality is an investment research service which does exactly that.

#Quality #Investing

bytetree.com/bytetree-qualit…

1

1

3

695

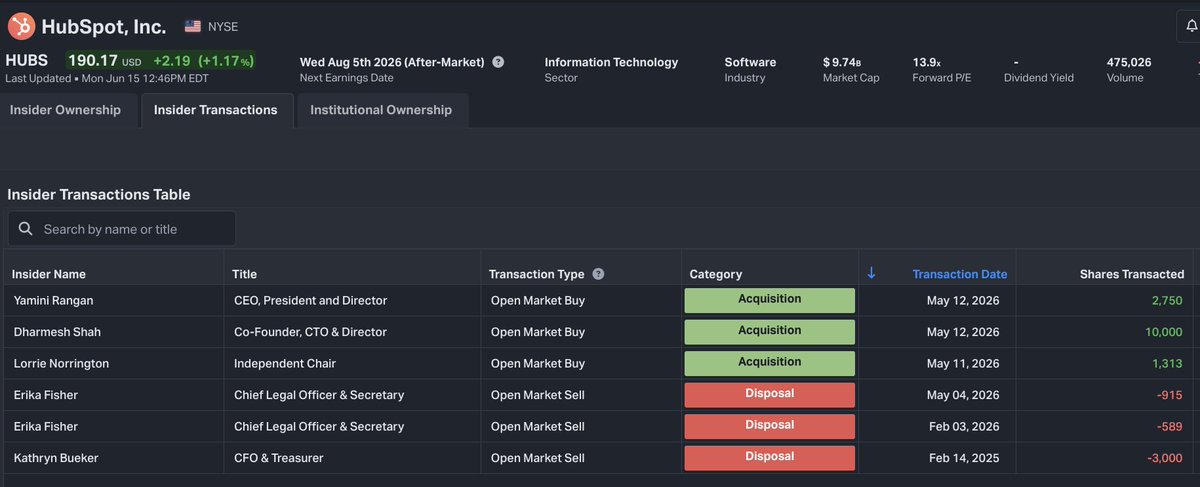

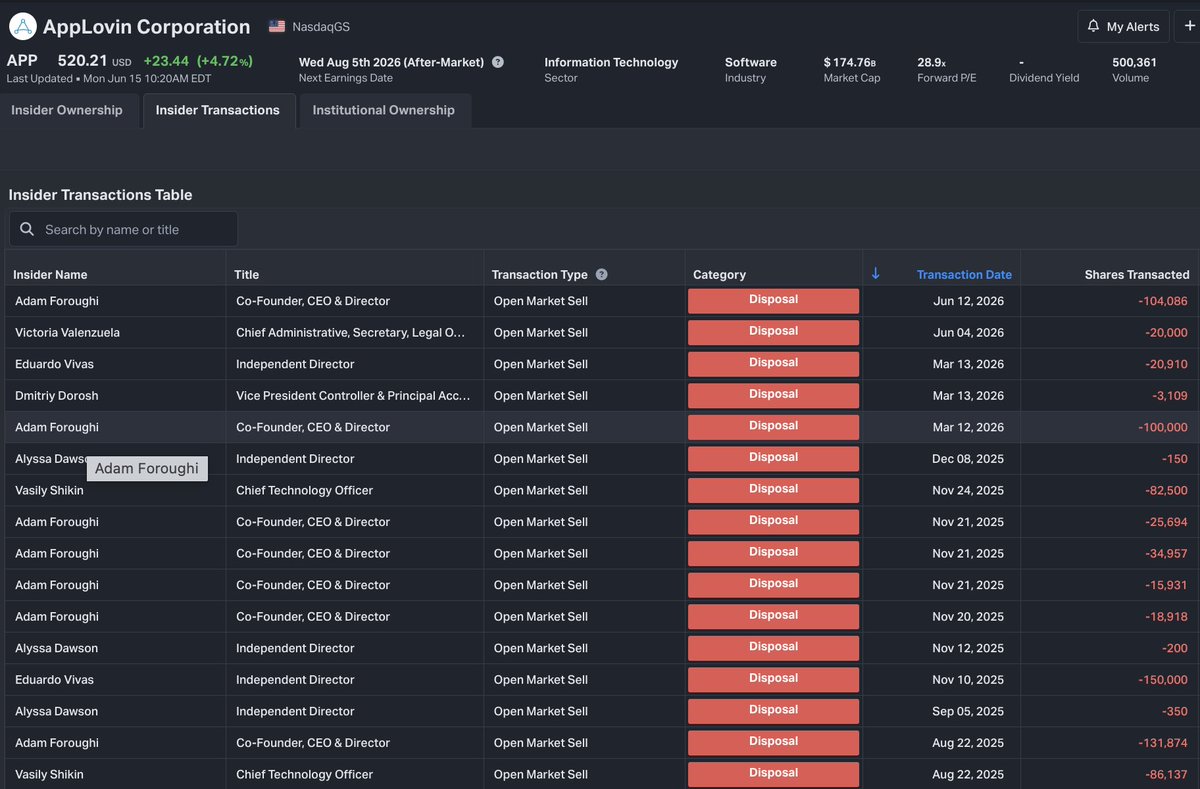

Insider selling can be a sign.

Over the last year, AppLovin $APP CEO Adam Foroughi has sold 425k shares worth c. $200m, and bought none.

Up 36% in the last year, it now trades at 28x sales.

2

3

4

364

A nice analogy for competitive advantage.

If it's that hard to get there, it's that hard for someone to catch up too.

Sometimes, there are no shortcuts

What's nice about calithsenics is that progress is slow. Some movements take months and years to accomplish because tendons, joints and connective tissue adapt much slower than muscle. It takes time to integrate the system.

1

87

KLA Corp $KLAC has reached 25x EV/Sales multiple.

This surpasses its previous record of 16x in 2000.

Meanwhile, revenue growth has actually slowed over the past four quarters, from 30% to 11%.

4

212

Good summary of Iran deal

Until the text of the US-Iran deal is signed and released, there is going to be a lot of spin on both sides. But here is my initial take.

This war was a mistake, and it needs to end. The President thought that the Iranian regime would collapse quickly, but it did not. In fact, it has been strengthened strategically by its survival against a heavy US-Israeli assault and carrying out some effective counterstrikes. Many countries in the region are now courting Iran and looking to deescalate and rebuild ties. A sign of which way the wind is blowing.

Getting the Strait of Hormuz open is the most important outcome of this MOU. Of course, the Strait was open before the war. Now we are paying to reopen it with sanctions relief. Iran has taken a theoretical point of leverage and turned it into a very real and powerful one, imposing costs across the global economy and rattling President Trump.

As for the nuclear issues, there really is no agreement, other than to negotiate over the HEU stockpile and an enrichment moratorium. Iran knows how to drag out those negotiations, and try to pocket concessions along the way. It is possible that no deal will every be reached, and very likely that if one is reached, it will be worse than what we could have achieved through diplomacy before the war.

Iran is not likely to take seriously that the US would return to war, certainly before the US midterms. So that means we will be conducting diplomacy without a credible threat of force.

If any agreement ultimately reached actually safely puts Iran's nuclear ambitions out of reach, I'll acknowledge it. It's just too early to make that judgment.

Trump is mainly focused on comparing his deal favorably to the JCPOA. But we are a long way from being able to make that comparison, and it may end up no better, or weaker than that deal.

But in some ways, Trump's deal and the JCPOA are already similar. Nothing on ballistic missiles, nothing on proxies, nothing on weakening the regime or helping the Iranian people. And plenty of sanctions relief that will strengthen the regime, and be poured into the missile program and proxy network. Honest critics of the JCPOA will not twist themselves into pretzels to defend Trump's approach.

Israelis are deeply disappointed in this outcome, but they should not be surprised. After some initial overlap of Trump's and Netanyahu's interests, there was a strong divergence. The United States needed this war to end. Netanyahu wanted to continue.

Trump's claim to include Lebanon in the ceasefire and his harsh shutting down Israeli attacks on Hezbollah is also a win for Iran. After the JCPOA was signed, Obama and Netanyahu worked together to strengthen Israel's campaign of strikes in Syria to intercept Iranian weapons shipments to Hezbollah in Lebanon.

So let's hope we see the removal of Iran's enriched uranium and a long-term suspension of enrichment, with full verification. But to achieve those goals, Trump's team is going to need to engage in far more sophisticated diplomacy, backed by qualified experts, than they have to date. If it is a phase one splash with no follow-up on implementation of later phases, like in Gaza, we will be much worse off after, and because of, this war.

32

Today is #SpaceX IPO day — and we're selling Seraphim Space (SSIT).

We bought in November 2024 when it traded at a 38% discount to NAV. That discount has since swung to a 22% premium.

"Buy the rumour, sell the news" has rarely felt more apt. 🚀

Read the $SSIT sell note by @AtlasPulse and @WinderKit: bytetree.com/research/2026/0…

1

4

200

Jun 11

This is a common problem for investors.

Accenture $ACN, which may be being disrupted, is down over 50% from its peak.

But it's still at a multiple of sales higher than at its highest level pre-2008?

Anchoring bias is a huge challenge right now.

3

337

Jun 10

Duolingo $DUOL now up 40% from its lows.

EV/Sales below previous record, while FCF keeps marching higher...

4

234

Jun 10

138

Jun 10

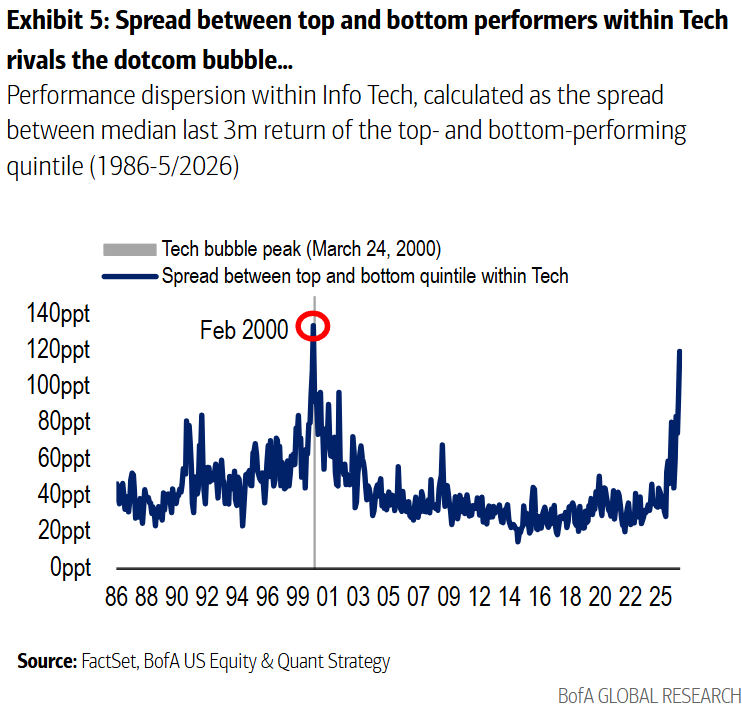

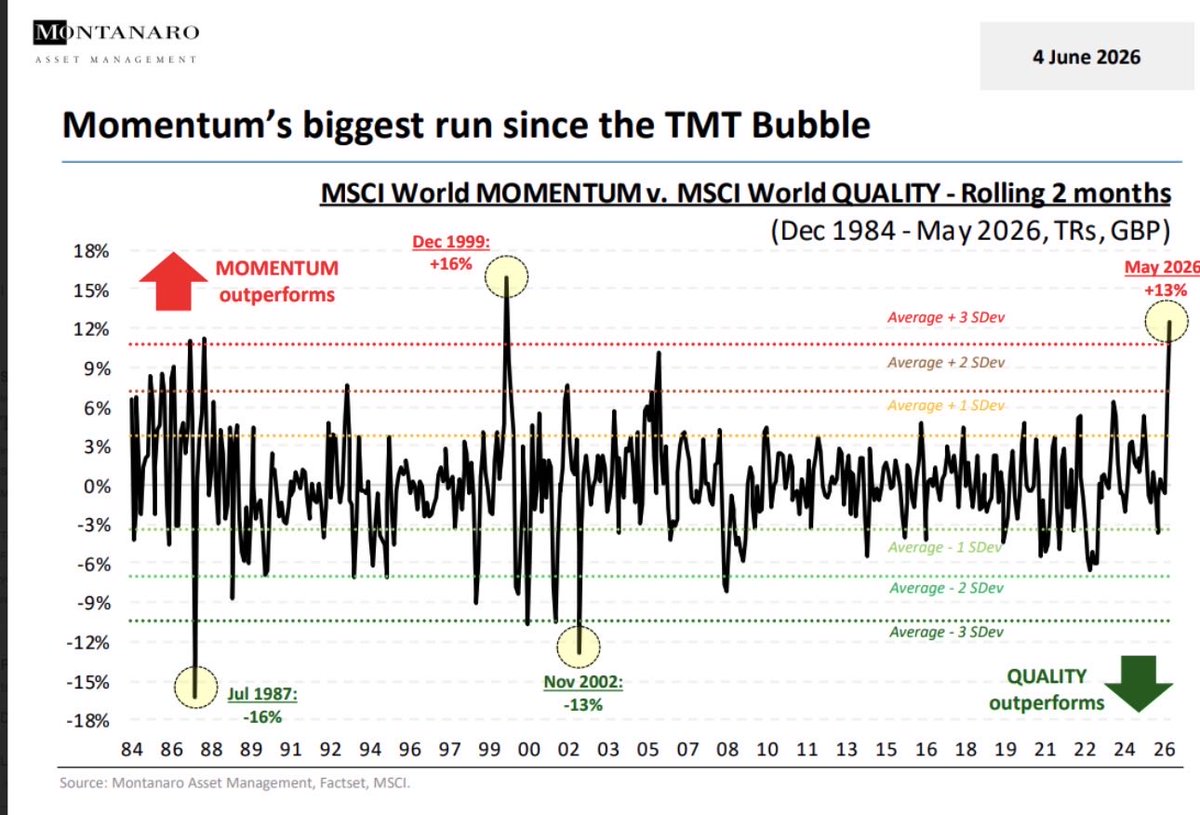

Momo vs quality extreme divergence

🚨 Momentum just beat Quality by the most since the dot-com bubble.

This chart from Montanaro tracks how far Momentum stocks are outrunning Quality stocks, back to 1984.

In May 2026, Momentum beat Quality by 13% in just two months. More than three standard deviations above normal.

In 40 years, this has happened only a handful of times. The single most extreme reading on the entire chart? December 1999. The peak of the dot-com bubble, at 16%.

Let that sink in.

The last time the market chased momentum over quality this aggressively, the Nasdaq was three months from its peak and about to lose 78% of its value, while quality stocks were about to begin one of their greatest runs of outperformance in history.

This is the chart behind everything I've been writing.

Momentum is the AI complex. The vertical movers. The stocks going up because they're going up.

Quality is the boring compounder. Stable margins, pricing power, real cash flow, durable moats. The stuff nobody wants right now.

When the gap stretches three standard deviations, it doesn't stay there. It reverts. Often violently.

The further momentum runs ahead of quality, the more powerful the snap back.

In 2000, that reversal lasted years and made fortunes for the patient.

History doesn't repeat. But it is rhyming loudly.

The most hated trade on Wall Street right now is also the one with the most history behind it.

2

68

Jun 10

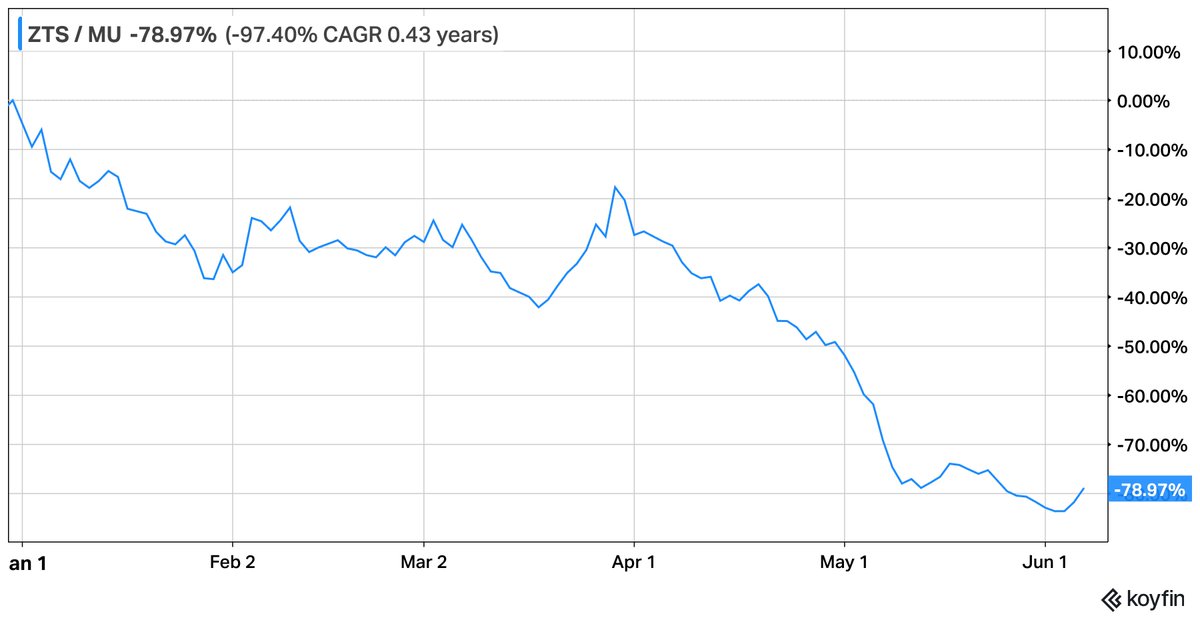

At its worst, $ZTS underperformed $MU by 98.0%, from August 2020 until June 4.

That's a neat -47% CAGR over ~6 years.

Where's your money for the next few years?

#PetsVsChips

Jun 8

1

220

Jun 10

If AI makes employees more valuable, enhancing their speed and capabilities, wouldn't you want more employees, not fewer?

Nice to hear that doomer predictions from last year have turned out to be wrong.

#SaaSpocalypse $NOW

Jun 9

Orlando Bravo: "The SaaSpocalypse is over... AI is an enormous, enormous tailwind for software companies... I was here last year at Super Return, and I think one of the LLM leaders made a comment that by this year, 50% of all white-collar jobs are going to be gone. And somebody in private equity made a comment that 50% of the people in this conference wouldn't have a job by next year. And look at the conference. You even had security outside. There's more people here than ever before... Our companies, 60% of the code that they write is machine-generated. But our number of developers, we have 20,000 of them, they're going up because now they can be a lot more productive."

150

Jun 10

Issuance has turned to buybacks at Tencent, while America turns from buybacks to an IPO frenzy.

Is this the biggest story investors are missing on China?

$TCEHY

2

139

Jun 10

"Investors are ignoring dividend-paying stocks because of their enthusiasm for exciting growth stories.

Despite the huge outperformance of the technology sector over the past several years, the total return of the S&P Dividend Aristocrats index remains substantially higher than Nasdaq’s since the peak of the 1999-2000 technology bubble."

- Richard Bernstein, Head of Macro at Janus Henderson

1

5

386