Everything passes

Joined August 2019

- Tweets 4,537

- Following 49

- Followers 335

- Likes 44,766

763 Photos and videos

While $META, $AMZN, $GOOG & $MSFT spent the week getting grilled in Columbus over grids and water, $MARA walked in with a different message:

“We own the power”

A 505MW plant at Long Ridge.

Flexible load that strengthens grid reliability instead of straining it. Industrial site redevelopment, not farmland.

Minimal water use.

This is the vertically integrated energy story the market still hasn’t priced.

Excited to share that @MARA testified this week before the Ohio Joint Data Center Committee. We appreciated the opportunity to participate in a thoughtful, fact-based discussion on how data centers impact Ohio’s economy, energy grid, and communities. Our message was clear: MARA is committed to responsible development - using advanced cooling technologies that minimize water use, redeveloping existing industrial sites, delivering flexible load that strengthens grid reliability, and creating local jobs and tax revenue. We’re in Ohio for the long term and focused on being a transparent partner to the state. Grateful to the Committee for their time and leadership. #TeamMara #Ohio #DataCenters

2

4

31

3,151

$MARA

In 2025: the CEO drew a $978.5K salary a $2.2M cash bonus at 100% of target. The trigger? "Hashrate Hours." The equity (67% PSUs) vests on the same family of operational metrics Hashrate Hours, Total Exahash, Megawatts plus relative TSR against a basket of other miners.

Read that again.

Not one of those is profitability. Not one is absolute shareholder value. You get paid for getting bigger, and for being less-bad than peers never for making money.

The scorecard those metrics actually produced: a $1.7B net loss in Q4, then $1.3B more in Q1.

The ask on June 18? 18M more shares.

Two votes are on the ballot:

→ Prop 3 (say-on-pay) is advisory. It binds no one but a NO is the loudest signal holders have.

→ Prop 4 (the 18M-share dilution) is binding. That's the one with teeth. Vote NO.

The lease is still the only thing that re-rates.

4

2

17

2,313

$MARA is trading at a $4.8B market cap.

Here is the math the market refuses to do:

→ 35,303 BTC in treasury = ~$2.2B (even with Bitcoin down 50% from ATH).

→ That leaves ~$2.6B for the ENTIRE operating company.

→ 72.2 EH/s of hash rate 1.3 GW of energized power infrastructure roughly covers that on its own.

Which means the market is pricing at **ZERO**:

⚡ Long Ridge - 505 MW vertically integrated power campus, ~$144M annualized EBITDA, 76% contracted, ~$15/MWh operating cost, path to 1 GW. Closing hurdle cleared 48 hours ago.

🇫🇷 Exaion - 64% of EDF's nuclear-powered AI compute arm. Sovereign French energy access. Unreplicable at any price.

🏗️ Starwood JV - hyperscale campus development where Starwood carries the capex, not MARA's balance sheet.

🤝 And management, on the record: "advanced conversations with multiple prospective tenants across multiple sites." Inbound interest from investment-grade hyperscalers. ~90% of owned capacity in active tenant discussions.

2.2 GW at closing. In PJM. In 2026. While hyperscalers fight over electrons.

Before the bears scream "debt", converts were cut 30% in ONE quarter. $1B retired at 91 cents on the dollar.

One signed lease changes the entire equation.

IREN traded like this once. Ask the shorts how that ended.

13

20

94

6,317

Xanny retweeted

Jun 9

Most investors still see $MARA Marathon as a Bitcoin miner

The company now has a 2.2 GW power pipeline and exposure to the sovereign AI infrastructure market via Exaion

Power and AI sovereignty are becoming 2 of the most valuable assets in the world

Must watch for investors:

8

16

40

7,377

$MARA Exaion on French national TV at Macron’s Choose France summit. Anthropic filing for French entry in the ticker crawl right above.

Coincidences?

In this market? 👀

At Choose France, President Macron's annual investment summit at Versailles, French national media turned to MARA and Exaion.

Hear from MARA CEO Fred Thiel (@fgthiel) and Exaion CEO Fatih Balyeli (@balyeli_fatih):

7

22

1,976

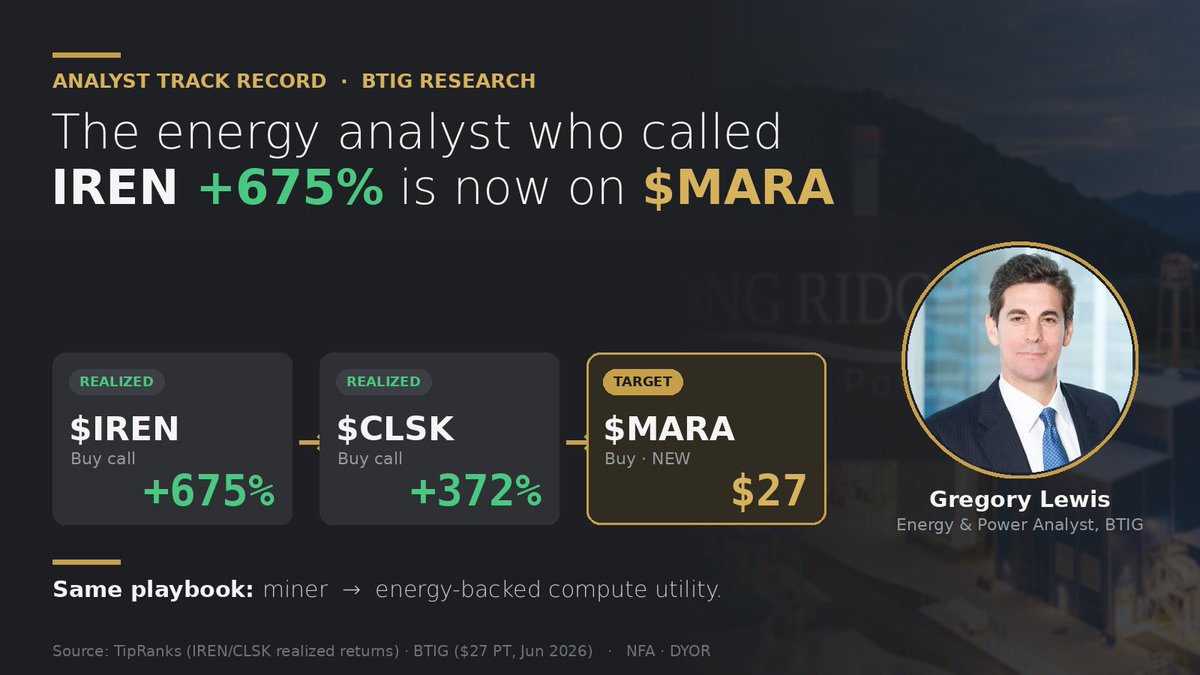

BTIG’s Gregory Lewis who covers oil tankers and power plants just put a $27 target on $MARA.

Lewis doesn’t price Bitcoin miners. He prices power assets.

Last time he made this call on a miner pivoting to compute:

$IREN — Buy → 675%

$CLSK — Buy → 372%

Same playbook. Same analyst. Same setup.

Now he’s looking at $MARA.

He sees Long Ridge a 505MW gas plant, $140M EBITDA and prices it for what it is:

not a miner, an energy-backed compute utility.

When the energy guy who called IREN at 675% lands on $MARA at $27…

the market’s still reading the old story.

3

22

77

4,249

Free optionality on every single AI deal.

Market handed this one out for free.

We must thank @MorganStanley analyst for pointing out the forgotten truth which is - $MARA bears need exactly one thing to be right:

Zero deals. Forever. Not one.

Good luck.

May 20

I was getting concerned that the AI deals for $MARA were getting priced in, but thankfully the Morgan Stanley analyst yesterday clarified that the market has completely discounted the possibility of any deals ever being signed

Rare to find a stock where big news is NOT priced in

3

11

1,441

Hi @grok I want hard predictions on $MARA. No hedging, no “it depends”.

Setup (May 2026):

(1) 1,900 MW operating, 19 data centers, 4 continents

(2) Long Ridge acquisition: 505 MW $144M annualized EBITDA, closing H2 2026 (PJM grid, 1,600 acres in Ohio)

(3) Starwood JV: multi-GW AI infrastructure pipeline

(4) Exaion (64% of EDF subsidiary): French nuclear-powered HPC

(5) Q1 2026 earnings call: 90% of MARA’s owned sites in active tenant discussions

(5) Zero hyperscaler leases signed to date

(6) Morgan Stanley just cut PT to $7 (Underweight), valuing pipeline MWs at 10% probability of electrification

Three predictions. Commit to numbers:

1) Predict MARA’s next 3 concrete strategic moves over the next 12 months. Specific deals not “they’ll pursue diversification.” Name names. Give timelines.

2) For MARA’s first signed hyperscaler/AI lease, allocate probability across these tenants. Must total 100%:

•Microsoft / Azure ____%

•Google / Alphabet ____%

•AWS / Amazon ____%

•Meta ____%

•Oracle ____%

•xAI / Colossus ____%

•CoreWeave ____%

•Apple ____%

•Other (specify) ____%

3) Same allocation exercise, but specifically for the Long Ridge Ohio campus (505 MW, PJM, near hyperscaler-dense corridor).

Who gets those electrons?

Show your reasoning chain. Commit to the percentages. Don’t hide behind probability ranges.

2

2

28

5,570

Let's do the math the @MorganStanley analyst couldn't:

According to his own calculation:

$7 PT × 381.27M shares = $2.67B implied market cap.

What $MARA actually holds (per Q1 2026 SEC filing):

35,303 BTC ≈ $2.82B

Cash ≈ $80M

**Total liquid: $2.9B

Even gross of debt, Morgan Stanley's entire valuation is less than MARA's BTC stack alone.

After netting $2.3B in convertible debt (already reduced 30% via March buyback), MS still has to justify giving ZERO credit to:

*1,900 MW of operating power capacity

*19 data centers across 4 continents

*Exaion (64% of EDF subsidiary — French nuclear-powered HPC)

*Long Ridge ($1.5B acquisition adding 505 MW $144M annualized EBITDA, closing H2 2026)

*Starwood JV (90% of MARA's owned sites in active tenant discussions per Q1 call)

Same Morgan Stanley values $CIFR operating contracted MWs at ~$19M each.

$MARA's MWs at the $7 PT? ~$1.4M each.

~13x discount for the same physical electrons.

Different rationale: CIFR has signed hyperscaler leases. MARA hasn't yet.

Which brings us to MS's own admission.

Per MARA IR @RobSamuelsIR, quoting directly from the MS analyst's note today:

"We value pipeline MWs at a 10% chance of electrification until the partnership results in a deal."

90% written off. Before a single signature.

This is the same Morgan Stanley that told clients Bitcoin's intrinsic value could be $0 in 2017.

Today they run $MSBT the cheapest spot BTC ETF on the market at 0.14% and bought 430 BTC on launch day.

The bank long Bitcoin is underweight the equity holding 35,303 of them.

3

7

36

4,292

8/ Most analysts model $MARA as a Bitcoin miner pivoting to AI.

The real model: MARA is becoming what EDF is to French electricity, a global utility selling the same electron into the highest-bid compute use case at any moment.

The valuation framework for this doesn't exist yet.

12

885

Xanny retweeted

May 16

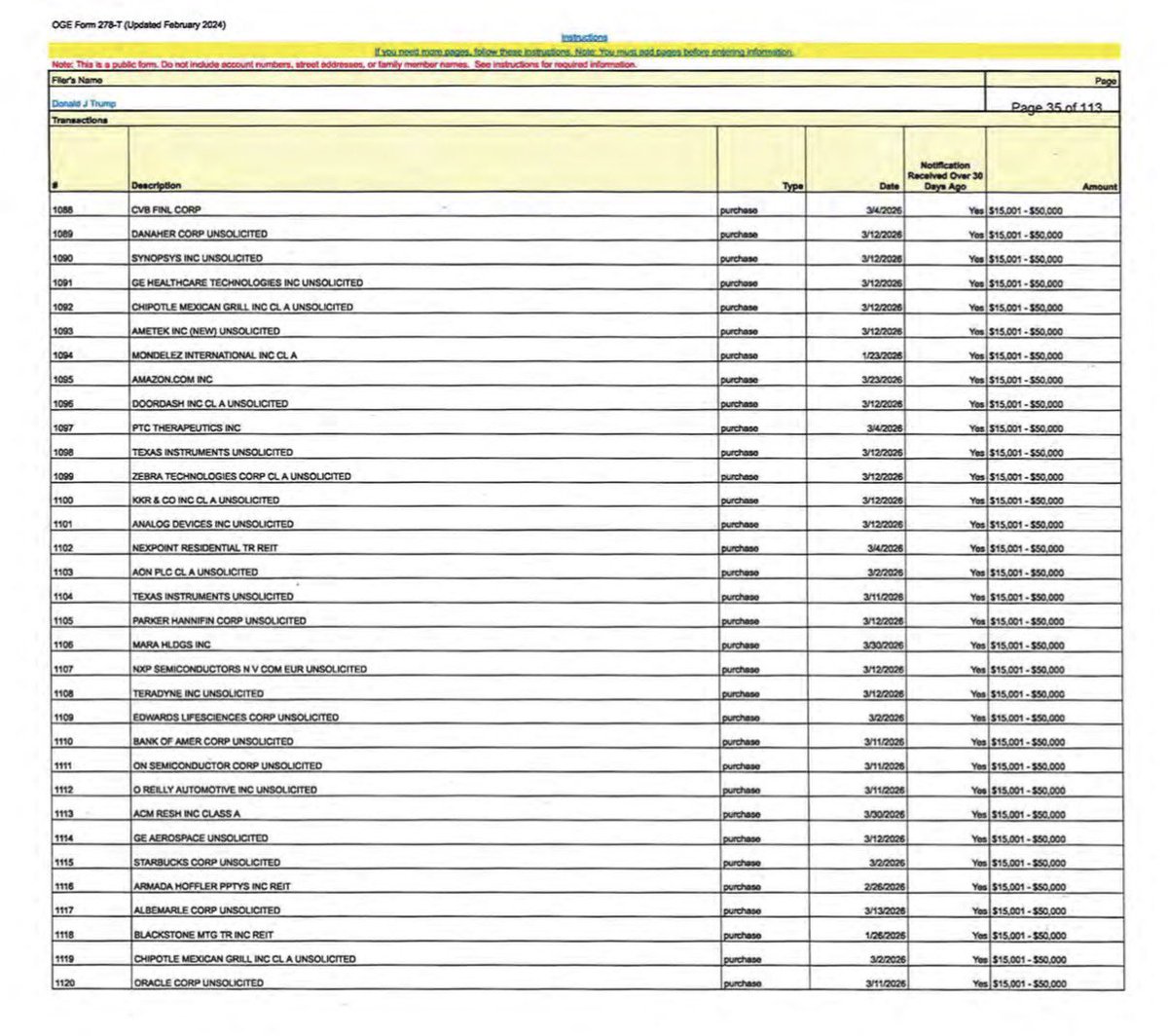

LATEST: 🇺🇸 President Trump and his family bought shares of Coinbase, Strategy, and MARA Holdings during Q1, per a new financial disclosure.

116

155

790

52,110