Australia’s leading online research and data platform on Interest rates, Income focused Managed Funds, ETF, LIC and the factors that move them.

Joined September 2013

- Tweets 6,529

- Following 273

- Followers 544

- Likes 393

5,461 Photos and videos

𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

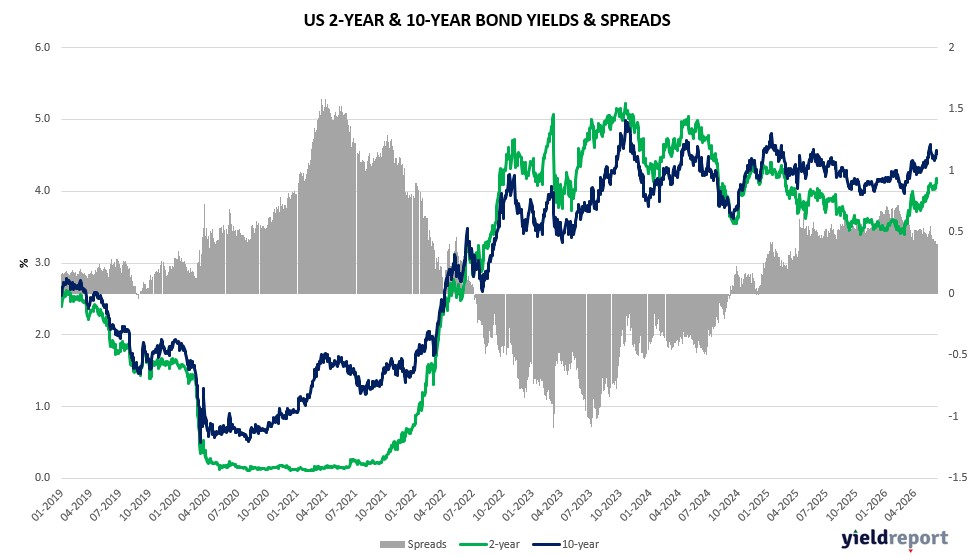

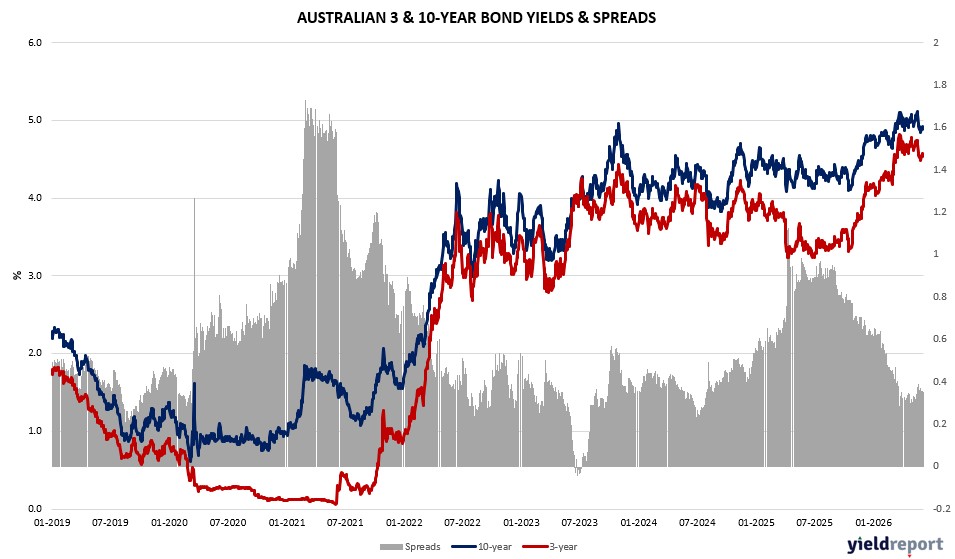

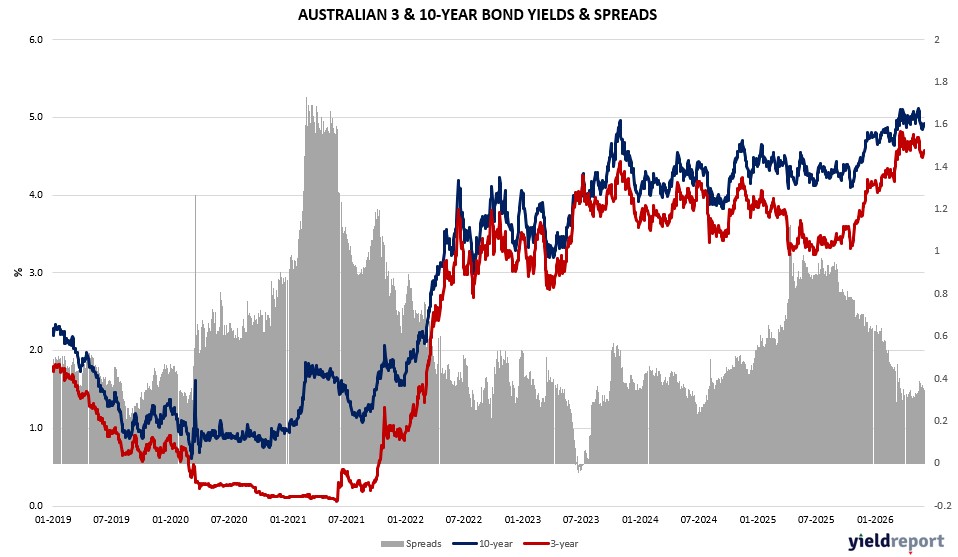

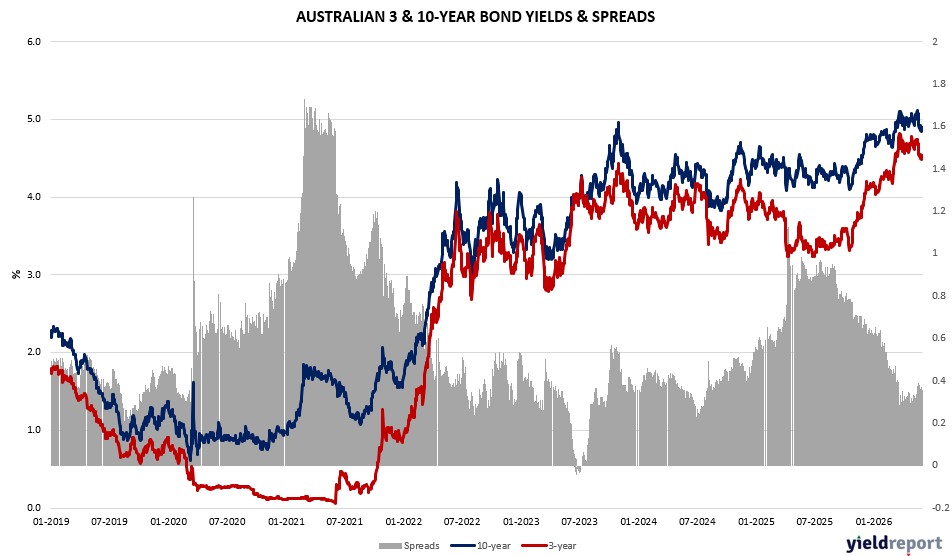

Australian government bonds rallied strongly across the curve on Friday, 12 June 2026, as prospects of a US-Iran peace deal drained energy-driven inflation risk from global markets and the local rate outlook underwent further dovish repricing. Yields fell uniformly, with the two-year benchmark declining 6 basis points to 4.46%, the five-year easing 8 basis points to 4.47%, and the ten-year retreating 8 basis points to 4.81%. The fifteen-year also fell 8 basis points to 5.03%. Over the month, the two-year has declined 27 basis points and the ten-year is 25 basis points lower, reflecting a meaningful shift in the market’s assessment of where the terminal rate will land following a run of softer domestic data.

zurl.co/O6orl

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

zurl.co/4C61i

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank #asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights #TermDeposits #InterestRates #BankingInsights

1

66

The U.S. Consumer Price Index (CPI) for May 2026 delivered a result that was elevated but broadly anticipated. Annual inflation surged to 4.2%, its highest reading since 2023, propelled almost entirely by a sharp acceleration in energy prices. While the headline number may unsettle markets at first glance, the underlying details reveal a considerably more contained picture, with core inflation holding relatively steady and services costs rising only modestly.

Read the full analysis: zurl.co/MQPhx

#USEconomy #FederalReserve #CPI #EnergyPrices #MacroInsights #InterestRates #Investing #YieldReport #FixedIncome

23

Weekly Overview of the ETF Markets.

The week ending 29 May 2026 was characterised by a continuation of the technology and Asia-focused rally, with South Korean and semiconductor exposures dominating the leaderboard. The iShares MSCI South Korea Capped ETF (IKO) was the standout performer with a 9.2% weekly return, extending its remarkable 12-month gain to 204.5% — the best across the entire Australian ETF landscape. The Betashares Asia Technology Tigers ETF (ASIA) followed at 7.7%, with the Betashares Space Industry ETF (RCKT) close behind at 6.8%. Global X’s suite performed well, with the FANG Currency Hedged ETF (FHNG) and Ultra Long Nasdaq 100 ETF (LNAS) each rising 6.7%, and the Semiconductor ETF (SEMI) adding 6.3%. Clean energy and AI also featured among weekly winners, with VanEck Global Clean Energy (CLNE) and Global X Artificial Intelligence (GXAI) each gaining around 6%.

On the downside, digital assets remained firmly out of favour. Ethereum products led the declines, with EETH falling 7.0% and Monochrome Ethereum (IETH) down 5.9%. Bitcoin ETFs shed between 4–6%, with EBTC and BTXX each declining 6.2% and SNAS (the inverse Nasdaq product) dropping 6.3%. Crude oil (OOO) was also a notable laggard, falling 9.5% for the week — the worst performer across the broader market — while Betashares Global Energy (FUEL) slipped 4.9%.

Read more - zurl.co/IkKys

#ETFs #MarketUpdate #InvestorFlows #SectorRotation #GlobalMarkets #YieldReport #EquityOutlook #FixedIncome #Commodities #DigitalAssets

185

𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

zurl.co/39K8e

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

zurl.co/39K8e

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank #asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights #TermDeposits #InterestRates #BankingInsights

18

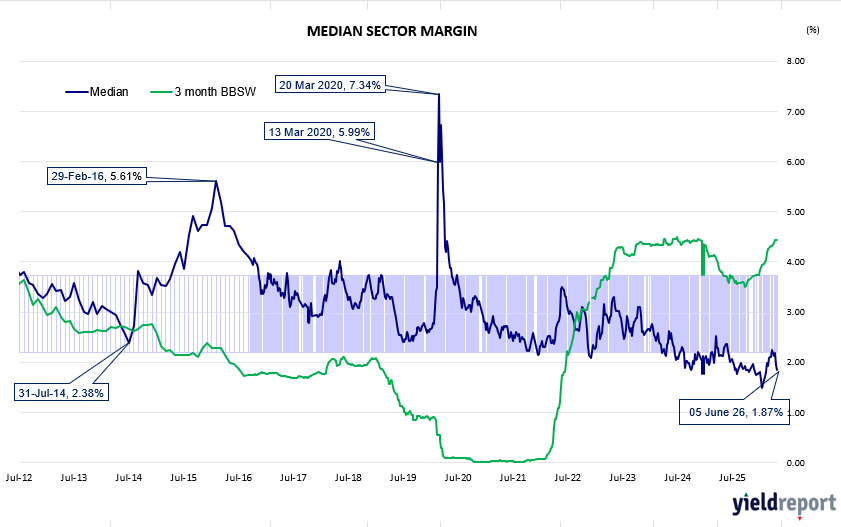

A notable split between near-term funding benchmarks and the interest rate swap curve continued to shape Australian fixed income through the week to 5 June 2026. Unlike the prior week’s divergence — where BBSW held firm while swaps retreated — both market segments registered gains in this period, yet the magnitude and direction of monthly moves remain starkly at odds, reflecting two distinct forces acting on either side of the yield structure.

Front-end BBSW rates extended their upward grind with characteristic tenacity, sustaining the firmness that has taken hold across the short end since late April. The 1-month tenor closed flat on the week at 4.30 per cent, yet its monthly advance of 8 basis points remains among the more pronounced gains across the strip — a consistent signal of tightness at the immediate funding horizon. The 3-month rate gained 3 basis points over the week to settle at 4.47 per cent, with a matching monthly gain of 8 basis points indicating that the pressure has spread further along the front end. The 6-month tenor posted the week’s largest BBSW move, climbing 6 basis points to 4.86 per cent, while its monthly rise of 13 basis points suggests conditions in the medium-term funding window are still tightening, rather than approaching the equilibrium seen at shorter horizons. The trajectory across all three tenors reinforces a picture of a funding market operating under sustained policy constraint.

Read more - zurl.co/AZBgE

#FixedIncome #InterestRates #BBSW #InterestRateSwaps #BondMarket #AustralianMarkets #YieldCurve #MarketUpdate #InvestmentResearch #YieldReport #foresightanalytics

35

𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

zurl.co/0easv

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

zurl.co/0easv

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank #asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights #TermDeposits #InterestRates #BankingInsights

16

The ASX hybrid market concluded the week ending 5 June 2026 on a constructive note, with positive price momentum across much of the standard segment and income dynamics remaining firmly at the centre of investor decision-making in both cohorts.

Yield leadership held its familiar shape. Nufarm (NFNG) continued to head the non-standard space at 10.51%, with Ramsay Health Care (RHCPA) close behind at 9.17%. In the standard universe, Judo Capital (JDOPA) extended its lead to 9.78%, followed by Latitude (LFSPA) at 9.28% and Macquarie Bank Capital Notes 2 (MBLPC) at 9.10% — a trio that persists in offering a compelling yield premium relative to the densely clustered major bank names, sustaining their appeal among higher-income mandates.

Weekly price moves in the standard segment tilted decisively to the positive side. MBLPC was the week’s strongest performer, rebounding 2.22% after recent softness, while CBA PERLS 13 (CBAPJ) gained 1.07% and Latitude (LFSPA) recovered 2.09%. Challenger Capital Notes 4 (CGFPD) added 0.79% and Insurance Australia Capital Notes 2 (IAGPE) rose 0.59%. The principal detractor was Macquarie Group Capital Notes 4 (MQGPD), which gave back –4.67% following its sharp technical bounce the prior week, with Westpac Capital Notes 7 (WBCPJ) also slipping –0.80%. In the non-standard segment, NFNG eased a marginal –0.05% while RHCPA firmed 0.02%.

Trading margins sustained their barbell character. NFNG held at 6.04% and RHCPA at 4.70%, while within the standard cohort, Latitude (LFSPA) widened notably to 6.59% and MQGPD settled back to 3.95%. Core bank hybrids remained tightly ranged — AN3PL at 1.80%, WBCPM at 1.69%, and CBAPM at 1.68%. Closing prices stayed well above par for most names: JDOPA at 113.25, WBCPM at 106.95, AN3PL at 105.41, and CBAPM at 104.65, while NFNG edged higher to 84.50, continuing its gradual recovery.

The hybrid market reaffirmed its standing as a durable income allocation, with higher-beta names again delivering standout yield and core bank hybrids absorbing the week’s volatility with characteristic resilience.

zurl.co/BCV7U

#foresightanalytics #yield #asx #termdesposit #cpi #finance #marketupdate

1

39

𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

zurl.co/x7nhY

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

zurl.co/x7nhY

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank #asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights #TermDeposits #InterestRates #BankingInsights

23

Australia’s central bank is drawing a hard line: inflation first, growth second. RBA leaders stress that price stability is non‑negotiable, even as higher rates weigh on households and businesses. With inflation re‑accelerating since 2025 and energy shocks adding fuel, the Bank expects GDP growth to slow to ~1.3% and unemployment to edge higher.

The message is clear — policy will stay tight until inflation is back under control, even if it takes years.

Read more - yieldreport.com.au/insights/…

#Inflation #AustraliaEconomy #MonetaryPolicy

1

26

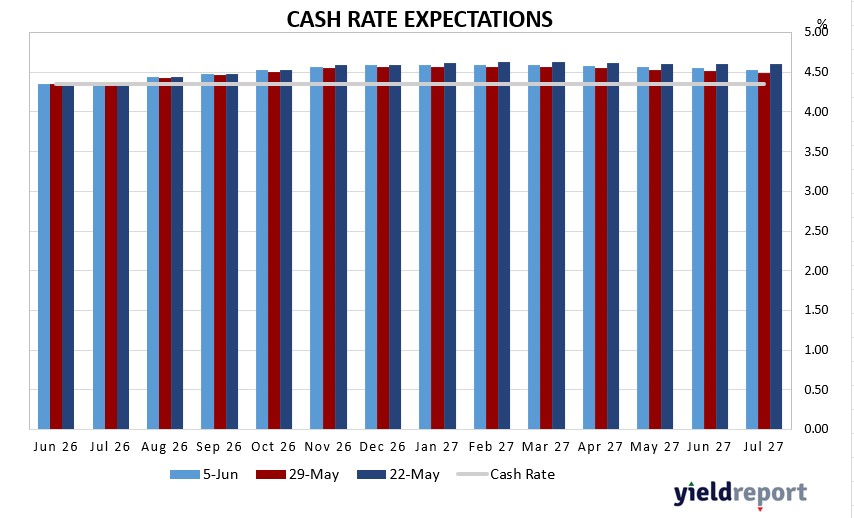

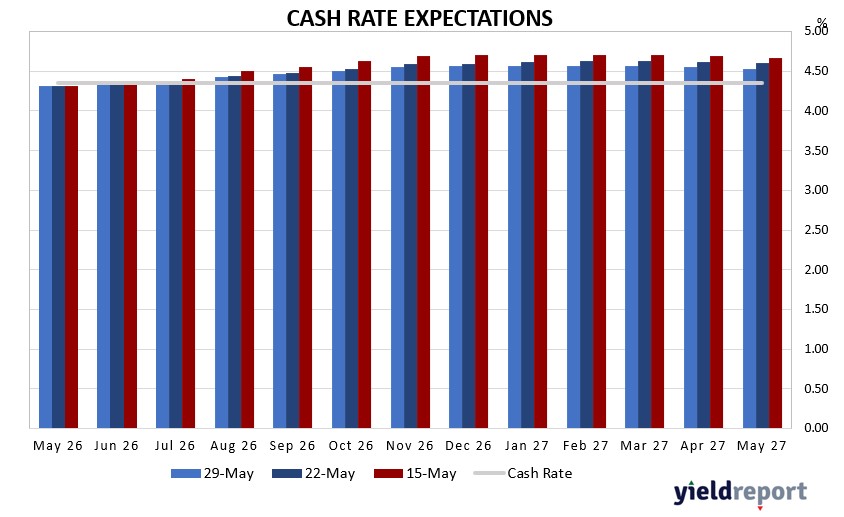

Australian interest rate market pricing has remained broadly stable over the week to 5 June 2026, with the 5-Jun curve sitting largely in line with or marginally below both the 29-May and 22-May profiles across the forward horizon. Rather than a hawkish reversal, the week’s movement reflects a modest dovish drift, with markets showing little appetite to price in additional tightening beyond current settings.

At the front end, implied rates for June 2026 remain firmly anchored near the prevailing cash rate of 4.35%, with near-term move probabilities remaining contained. The 5-Jun curve shows no meaningful divergence from prior weeks at shorter tenors, suggesting markets are comfortable that the RBA is on hold in the immediate term.

read more - zurl.co/M78KN

#WeeklyCashReport #RBACashRate #InterestRateOutlook #AustralianMarkets #SavingsAccounts #FixedIncome #YieldReport

1

2

42

Weekly Overview of the US Equities Market

Strong Jobs Data Ends Wall Street Rally and Revives Rate-Hike Fears

Wall Street’s powerful rally came to an abrupt halt as stronger-than-expected US employment data triggered a sharp reassessment of interest rate expectations, leading to a broad sell-off across equities, bonds and cryptocurrencies. Markets had enjoyed a strong recovery since late March, supported by easing geopolitical tensions and enthusiasm surrounding artificial intelligence, but investors became increasingly concerned that resilient economic growth could keep inflation elevated and delay monetary easing. The technology sector bore the brunt of the sell-off. The Nasdaq 100 fell nearly 5%, its worst daily performance since April 2025, while a major semiconductor index plunged 10%. The S&P 500 dropped 2.6%, ending its attempt to record a tenth consecutive week of gains. The decline reflected growing investor concerns that valuations in AI-related stocks had become stretched after months of exceptional performance and strong earnings results. Some investors are now questioning whether the extraordinary growth rates achieved by AI leaders can be sustained.

Read more - zurl.co/5lK5b

#USEquities #StockMarket #WallStreet #SP500 #Nasdaq #Investing #Markets #Equities #MarketUpdate #FinancialMarkets #yieldreport

38

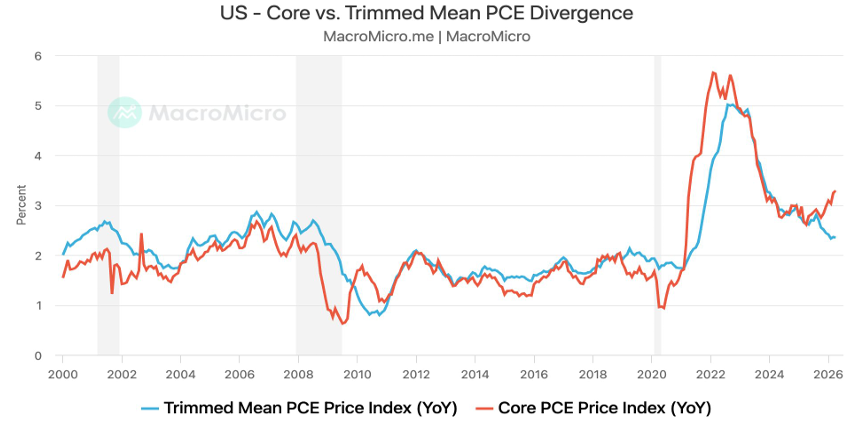

Chart of the Week - Warsh’s Preferred Gauge Points Lower, but Its Reliability Is in Question

Federal Reserve Chair Kevin Warsh has signalled a preference for the Dallas Fed’s trimmed mean inflation measure over traditional core inflation gauges, arguing it better captures broad-based price pressures by excluding extreme price movements. However, a growing divergence has emerged, with core PCE inflation re-accelerating while trimmed mean inflation continues to trend lower. Much of the gap reflects sharp increases in AI-related software prices, which carry a significantly larger weight in PCE than in CPI. Critics argue the trimmed mean measure may be understating inflation because its methodology excludes a disproportionate number of large positive price moves. Similar shortcomings were evident during the 2021 inflation surge, suggesting the current moderation in trimmed mean inflation may reflect limitations of the measure rather than genuine easing in underlying price pressures

Read more weekly update - zurl.co/JhOs8

#TrimmedMeanInflation#CorePCE #AIPricePressures #InflationMetrics #FedPolicy#UnderlyingInflation #MacroTrends #EconomicAnalysi #PriceDynamics #MonetaryPolicy

72

𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

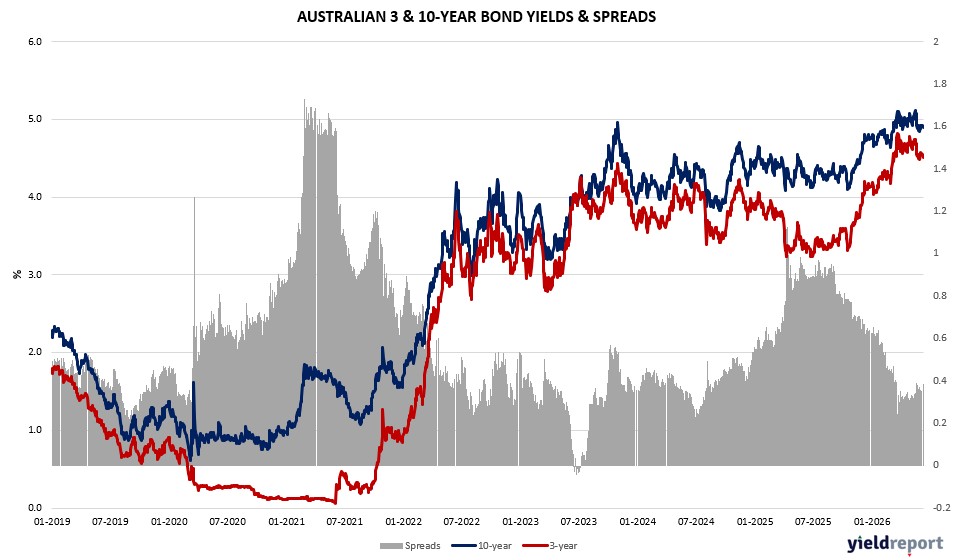

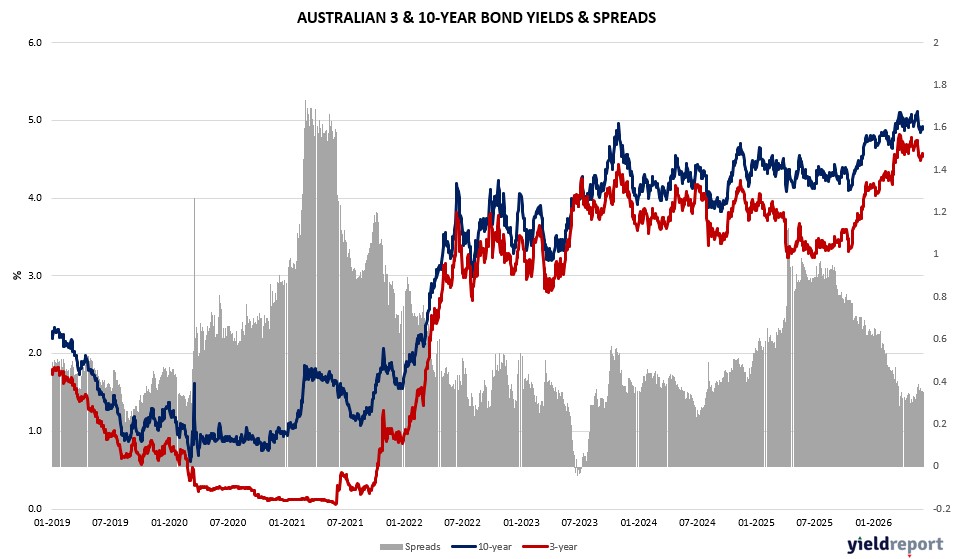

Australian government bond yields were marginally softer on Friday, 5 June, with the 10-year yield easing one basis point to 4.90% and the 2-year yield holding at 4.59%. The modest resilience in Australian bonds stood in contrast to the pronounced selling in US Treasuries following the blowout American payrolls report, reflecting both Australia’s distinct domestic growth picture and the proximity of the RBA’s upcoming June 15-16 policy meeting.

zurl.co/vOLgz

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

Subscribe on LinkedIn - zurl.co/vOLgz

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank #asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights #TermDeposits #InterestRates #BankingInsights

27

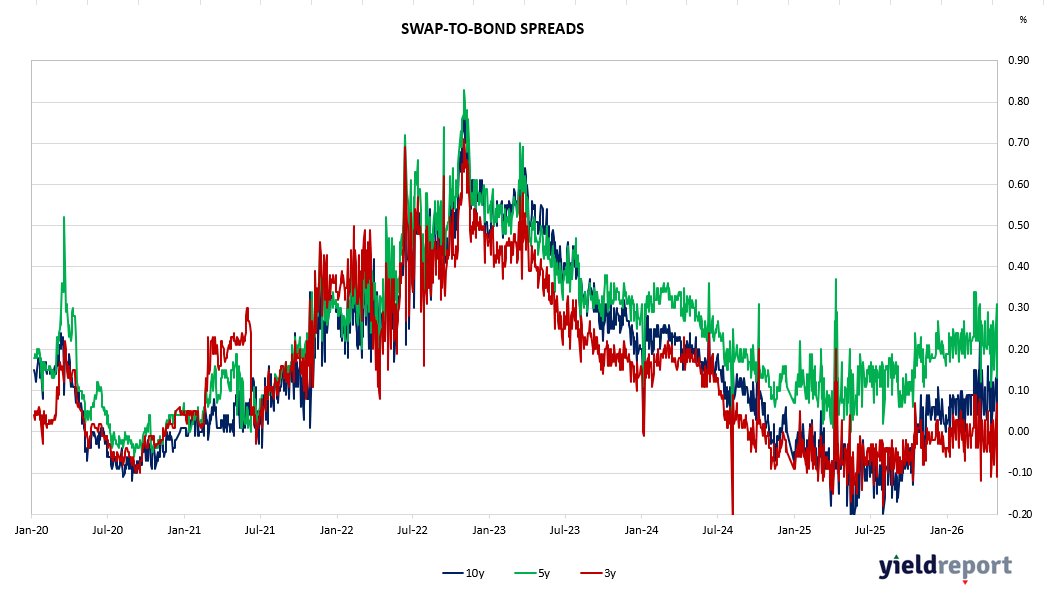

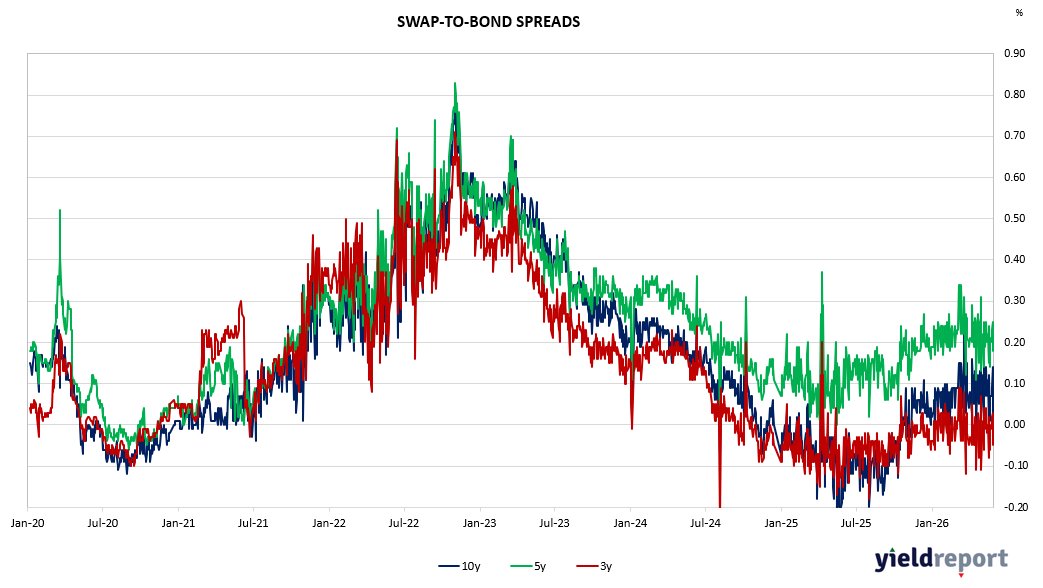

Both bank bill swap and interest rate swap markets maintained an upward bias through the week to 1 May 2026, affirming that the re-pricing cycle which took hold in March, continues to exert influence. Rather than a sharp directional move, the week was characterized by measured but broad-based firming, with rate levels across the curve remaining elevated against a backdrop of constrained liquidity and limited market confidence in an early policy pivot.

At the short end, BBSW rates advanced across tenors, pointing to sustained tightness in near-term funding conditions. The 1-month rate gained 5 basis points over the week to close at 4.20 per cent, extending its monthly rise to 15 basis points the largest monthly move across the BBSW strip. The 3-month tenor added 2 basis points to reach 4.37 per cent, with a more contained monthly increase of 6 basis points reflecting some stabilization at that horizon. The 6-month rate firmed 4 basis points on the week to 4.77 per cent, though it finished the month marginally softer, dipping 1 basis point below its level from four weeks prior. The persistence of front-end pressure is consistent with markets continuing to price policy settings as restrictive for an extended period.

Across the swap curve, upward pressure was distributed more evenly, with weekly gains of 3 to 5 basis points recorded at all tenors. The 1-year swap rate raised 3 basis points to 4.68 per cent, while the 3-year and 5-year rates each added 4 basis points, closing at 4.70 and 4.95 per cent , respectively. The 10-year and 15-year tenors led weekly gains, both climbing 5 basis points to 5.11 and 5.21 per cent. Notably, monthly changes at the long end around 7 to 9 basis points have been more uniform than the pronounced front-end moves seen in prior weeks. Swap-to-bond spreads remain elevated, with hedging demand and ongoing credit risk re-pricing continuing to exert upward pressure, particularly across short-to-mid tenors.

#WeeklyBankBills #BankBills #BillsAndSwaps #BBSW #foresightanalytics

45

𝐎𝐯𝐞𝐫𝐯𝐢𝐞𝐰 𝐨𝐟 𝐭𝐡𝐞 𝐖𝐞𝐞𝐤𝐥𝐲 𝐄𝐓𝐅 𝐌𝐚𝐫𝐤𝐞𝐭𝐬.

Australia – Defence Rises, Crypto Falls

The week ending 22 May 2026 saw a decisive shift in market leadership toward defence, cybersecurity and technology, marking a notable departure from the energy-driven gains of the prior week. The Betashares Space Industry ETF (RCKT) led all comers with an 11.8% weekly return, followed by the Global X Cybersecurity ETF (BUGG) at 8.8% and Betashares Global Cybersecurity ETF (HACK) at 7.1%. Defence-focused products — Betashares Global Defence (ARMR), VanEck Global Defence (DFND) and Global X Defence Tech (DTEC) — each rose around 5%, a rare cluster of defence outperformance that reflects growing investor attention to geopolitical risk. Hydrogen (HGEN, 6.1%) and global technology (TECH, 6.5%) also featured strongly among weekly winners.

On the other side, digital assets bore the brunt of selling pressure. Ethereum ETFs were the worst performers, with QETH falling 6.9% and IETH down 5.6%, while Bitcoin products shed roughly 4%, pushing their YTD losses to around −38–39%. Crude oil (OOO) reversed the prior week’s sharp gains, declining 4.3%, and precious metals softened across the board.

Over twelve months, hydrogen (HGEN, 195.7%), South Korea (IKO, 193.0%) and semiconductors (SEMI, 146.7%) remain the standout performers across the Australian ETF landscape.

On flows, the headline story was an unusually large A$140m inflow into the VanEck FTSE Global Infrastructure ETF (IFRA), suggesting institutional appetite for defensive real assets alongside the risk-on tone. Broad equity ETFs — IVV, BGBL, HGBL — also attracted solid inflows, while gold (GOLD) and semiconductors (SEMI) saw the largest redemptions of the week.

Read more -

#ETFs #MarketRotation #DefenceSector #Cybersecurity #TechnologyThemes #GeopoliticalRisk #HydrogenEnergy #GlobalTech #DigitalAssets #Bitcoin #Ethereum #foresightanalytics.

Jay Kumar Sangeeta Kumar Prashant Kumar George Zhao, Ph.D. Mitra M RAKESH NAYAK Brigi Meeha Forelytics Data Science and Innovation Eswar Sanjeeviraj

1

99

𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

zurl.co/Z3EnQ

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

Subscribe on LinkedIn - zurl.co/I094O

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank #asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights #TermDeposits #InterestRates #BankingInsights

25

A sharp divergence between near-term funding markets and the interest rate swap curve defined Australian fixed income through the week to 29 May 2026. Rather than moving in concert, BBSW rates held their ground or edged marginally higher while swap rates retreated across every tenor — most decisively in the belly of the curve — pointing to a meaningful reassessment of medium-term rate expectations in the wake of sustained upward pressure over recent months.

Read more - zurl.co/rc5yS

#BankBillSwaps #InterestRates #FixedIncome #AustralianMarkets #YieldReport #BBSW #MonetaryPolicy #IncomeInvesting

25