𝐇𝐞𝐫𝐞 𝐢𝐬 𝐨𝐮𝐫 𝐝𝐚𝐢𝐥𝐲 𝐛𝐨𝐧𝐝 𝐲𝐢𝐞𝐥𝐝 𝐮𝐩𝐝𝐚𝐭𝐞:

Australian government bonds rallied strongly across the curve on Friday, 12 June 2026, as prospects of a US-Iran peace deal drained energy-driven inflation risk from global markets and the local rate outlook underwent further dovish repricing. Yields fell uniformly, with the two-year benchmark declining 6 basis points to 4.46%, the five-year easing 8 basis points to 4.47%, and the ten-year retreating 8 basis points to 4.81%. The fifteen-year also fell 8 basis points to 5.03%. Over the month, the two-year has declined 27 basis points and the ten-year is 25 basis points lower, reflecting a meaningful shift in the market’s assessment of where the terminal rate will land following a run of softer domestic data.

zurl.co/O6orl

Subscribe to the Yield Report Weekly via LinkedIn to access detailed commentary and analysis.

zurl.co/4C61i

#YieldReport #FixedIncome #bondmarket #termdeposit #asxbank #asxdata #YieldInvesting #asxhybrids #InterestRates #weeklymarketinsights #InvestmentInsights #TermDeposits #InterestRates #BankingInsights

1

64

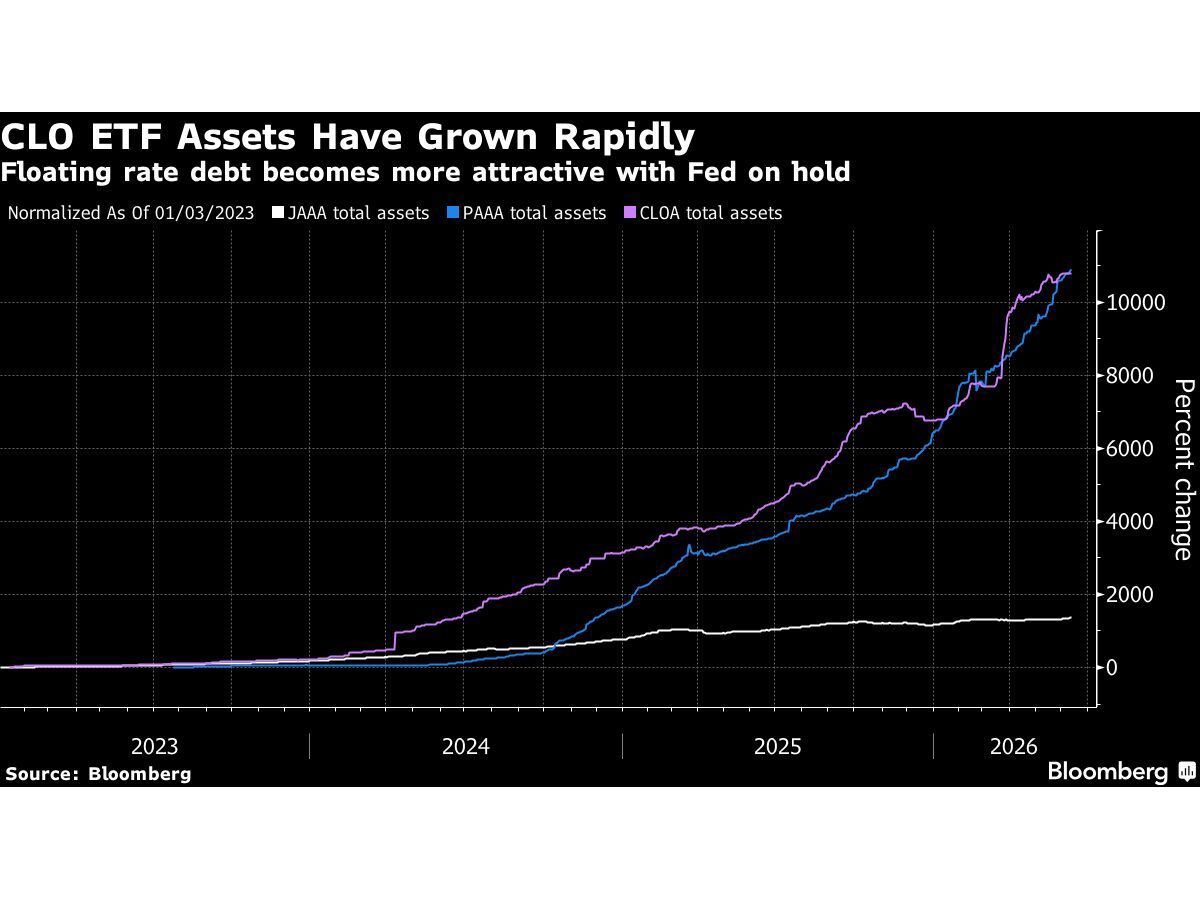

💥 CLO ETFs Are Eating BDCs’ Lunch — And Institutional Money Knows It

Read More: bit.ly/CLO-ETFs

#CLO #CreditMarkets #PrivateCredit #BDC #FixedIncome #AlternativeInvestments #InstitutionalInvesting #CreditStrategy #StructuredFinance #RateStrategy

9

The U.S. Consumer Price Index (CPI) for May 2026 delivered a result that was elevated but broadly anticipated. Annual inflation surged to 4.2%, its highest reading since 2023, propelled almost entirely by a sharp acceleration in energy prices. While the headline number may unsettle markets at first glance, the underlying details reveal a considerably more contained picture, with core inflation holding relatively steady and services costs rising only modestly.

Read the full analysis: zurl.co/MQPhx

#USEconomy #FederalReserve #CPI #EnergyPrices #MacroInsights #InterestRates #Investing #YieldReport #FixedIncome

23

TIPS Real Yield 1.95% — Best Entry Point Since 2008 for Inflation Protection

#theexpme #TIPS #IBonds #treasury #realyield #FederalReserve #inflationhedge #VTIP #SCHP #fixedincome #investing #wealthbuilding

6

India's corporate bond market outstanding as of March 2026: Rs 53.6 lakh crore.

That is more than the entire equity mutual fund AUM of Rs 35.74 lakh crore.

Most retail investors have never bought a single corporate bond.

The reason is structural.

Institutional investors, banks, insurance companies, provident funds, and mutual funds hold approximately 98% of India's corporate bonds. The secondary market for corporate bonds trades Rs 1.4 lakh crore per month. Indian equities trade the same volume in a single day.

Until recently, retail access required a minimum of Rs 10 lakh per bond. SEBI's Online Bond Platform Provider framework, introduced in 2022 and expanded since, has brought that minimum down to Rs 10,000 on regulated digital platforms.

But the market remains overwhelmingly institutional in character. The companies raising debt in this market serve millions of retail customers. The investors financing that debt are almost exclusively institutions.

A market that finances India's largest companies is still largely inaccessible to the people those companies serve.

#CorporateBonds #BondMarket #SEBI #IndianMarkets #EquityResearch #FixedIncome #IndiaInvesting #PersonalFinance #WealthManagement #RetailInvestors #OBPP

9

What were the most-viewed names in-app this week? 👀

Here's the Top 5 from our European #InvestmentGrade coverage over the last 7 days:

1. Alstom (ALOFP)

2. 2i Rete Gas (FIREIT)

3. Aroundtown (ARNDTN)

4. La Poste (FRPTT)

5. Oracle (ORCL)

#Credit #Bonds #FixedIncome

1

1

22

Jun 13

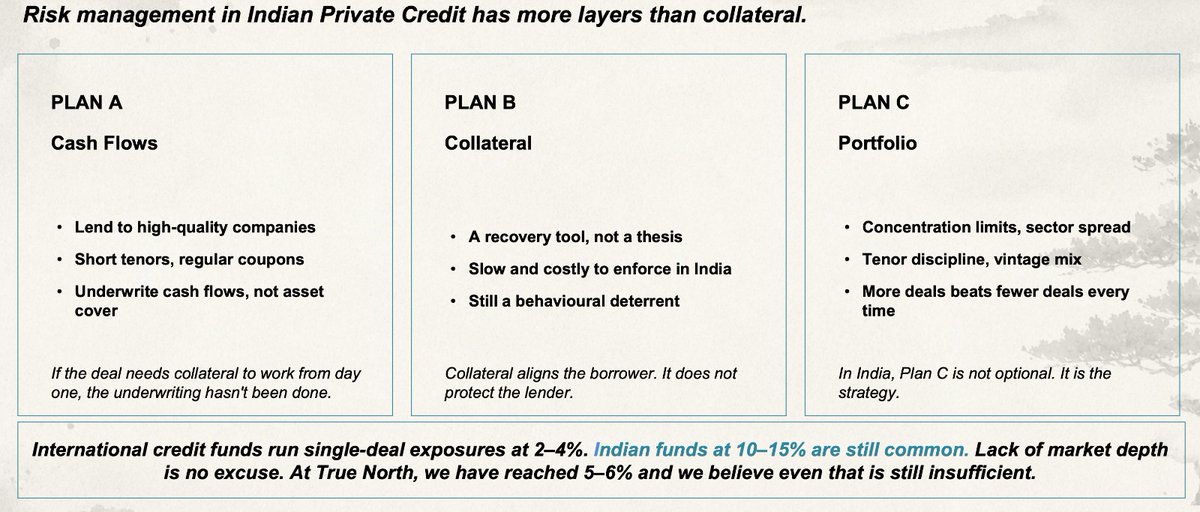

👉Equity is about picking winners. Private Credit is about avoiding losers.

In credit, the risk-reward is entirely asymmetric. There is zero extra upside to a great deal, but you take all the downside on a bad one.

Here are the real rules of the game in Indian Private Credit:

Collateral is a deterrent, not a thesis: It forces the borrower to behave, but it does not protect the lender if cash flows fail.

No multi-baggers to hide behind: Unlike equity, you cannot use one massive winner to cover portfolio losses.

Portfolio design is everything: Funds fail at the portfolio level (due to concentration), not just the deal level.

Underwrite cash flows, not asset cover.

#PrivateCredit #FixedIncome #DebtMarkets #RiskManagement #Finance

2

4

426

As a part of the PAN-India Issuer Outreach Program for Corporate Bonds, the second outreach event was held in Mumbai on 12th June 2026, bringing together potential issuers to engage in meaningful discussions on the evolving corporate bond market ecosystem and the opportunities it offers for efficient capital raising.

The session was graced by Shri Kamlesh Chandra Varshney, Whole Time Member, SEBI, who shared valuable perspectives on strengthening market participation and further deepening India’s corporate bond market to support the nation’s growth aspirations.

#NSE #NSEIndia #CorporateBonds #DebtMarkets #FixedIncome #BondMarket #CapitalMarkets #FinancialMarkets #BondsEkSashaktBandhan #IndiaGrowthStory @ashishchauhan

6

2,003

Jun 12

Private credit has been making headlines—but what should investors focus on beyond the news cycle?

On the latest episode of the Basis Points podcast, @KevinFlanaganWT is joined by Chris Acito, CEO of Gapstow Capital Partners, discuss liquidity, diversification and why looking beyond direct lending may help strengthen income-focused portfolios.

Listen & subscribe: bit.ly/4frtKTP

#BasisPointsPodcast #FixedIncome

1

1

422

Jun 12

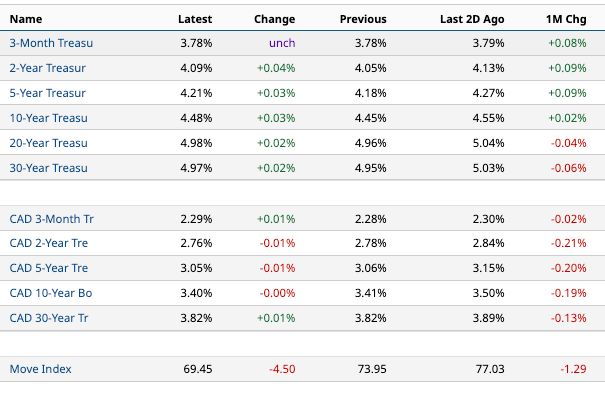

📈 Daily Global Bond Yield Watch 🇺🇸 🇨🇦

#Investing #Bonds #FixedIncome #Macro #Economy #YieldCurve #TreasuryYields #Treasuries

31

Jun 12

Beyond the spreadsheet. SOLVE Relative Value Analysis enhancement launching at FILS Booth #39, June 16: hubs.ly/Q04lfK6z0

#FILSUSA #FILSUSA2026 #FixedIncome #MarketData #AI

10

Jun 12

Treasury ladders now compete directly with annuities: investors can capture ~4–5% government yields while retaining liquidity, principal control, and lower fee drag.

10Y Treasury cited near 4.45%; 20–30Y maturities just under 5% per Fed/FRED context. Direct Treasury ladders can carry zero ongoing product fee; Treasury ETFs often <0.10%. By contrast, variable/indexed annuities commonly run ~1–3% all-in annual costs, with some variable annuity estimates at 2–4%.

Key distinction: annuity “payout rates” ≠ investment yield. Immediate annuity examples imply low-to-mid 4% internal yields after adjusting for return of principal. MYGAs may quote 5.0–5.9% for 5–10Y terms, with outliers near 6.3% often tied to lower-rated carriers—but investors give up liquidity, accept insurer credit risk, and face typical 5–10Y surrender periods.

Actionable framework:

• Use Treasuries/TIPS ladders for known maturities, state/local tax-exempt interest, liquidity, and estate value.

• Use plain-vanilla income annuities only where longevity insurance—not return maximization—is the objective.

• Compare contracts on IRR, surrender schedule, insurer rating, guaranty limits, tax treatment, and break-even longevity age.

Medium confidence: rates remain near 15-year highs post-Fed tightening; if yields decline into 2027, both new Treasury yields and annuity crediting rates likely compress. Locking ladder rungs now may be attractive for retirement income portfolios prioritizing transparency and control.

#FixedIncome #RetirementPlanning #Treasuries #Annuities $TLT

24

TermMax 每日话题:

真正的大资金,不追求暴富。

他们更在意:

👉 收益是否稳定、可持续。

很多人看到收益,

机构看到的是资金效率和长期复利。

未来最大的市场,或许是收益市场。

#TermMax #DeFi #FixedIncome

3

8

25

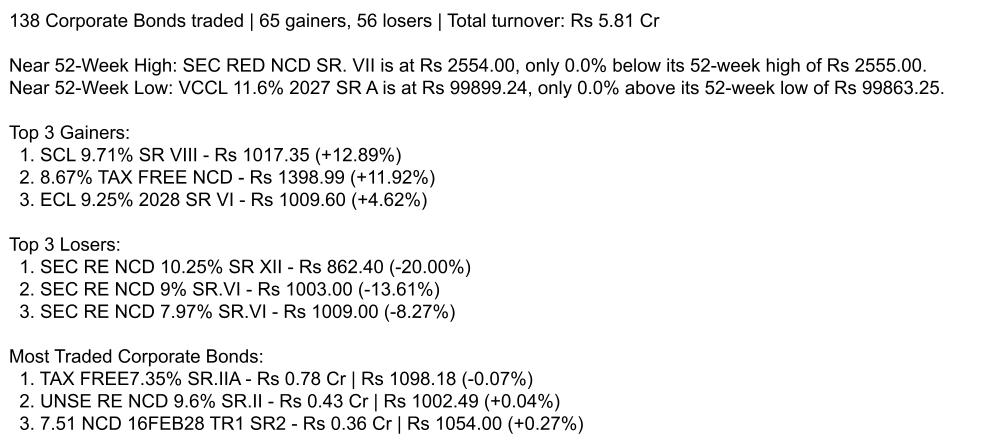

Quick insights from Corporate Bond data - trading day ending 12 Jun 2026

@NSEIndia @ETNOWlive @Moneylifers

#Investing #StockMarket #MarketData

#CorporateBonds #BondMarket #FixedIncome #DebtMarket

For more details, visit bhavcopydata.com/bonds

7

Jun 12

Regan Capital CIO on bond market opportunities in a rising rate environment @HANetf proactiveinvestors.com/compa… #ReganCapital #SkylerWeinand #FixedIncome #BondMarket #MortgageRates #FederalReserve #InterestRates #Inflation #Treasuries #MortgageBackedSecurities #FloatingRateNotes #YieldCurve #InvestmentStrategy #Markets #IncomeInvesting

1

1

315

Der Anleihemarkt ist wieder der Preisrichter für langfristige Finanzierung. In den Vereinigten Staaten (USA) stieg die Rendite zehnjähriger Treasuries von 4,19 % am 2. Januar 2026 auf 4,56 % am 22. Mai 2026. Am 1. Juni 2026 lag sie trotz Rückgangs noch bei 4,47 %. Im Euroraum zeigt die zehnjährige AAA-Spot-Rate der Zinskurve der Europäischen Zentralbank (EZB) denselben Mechanismus: Kapitalbindung hat wieder einen sichtbaren Preis.

Diese Bewegung verändert die Bilanzlogik. Für bestehende Anleihen bedeuten höhere Renditen in der Regel niedrigere Kurse; für neue Schuldner steigen Referenzsätze, Kupons und Refinanzierungshürden. Staaten rollen fällige Schulden nicht mehr selbstverständlich zu den Konditionen der Niedrigzinsjahre. Unternehmen diskontieren Investitionen mit höheren Kapitalkosten, während Haushalte bei Neu- und Anschlussfinanzierungen eine engere Tragfähigkeit spüren. Der relevante Kanal ist nicht nur der Leitzins, sondern die gesamte Zinskurve, in der Laufzeit, Risikoaufschläge und Inflationserwartungen zusammenlaufen.

Für Banken und Versicherer verschiebt sich zudem die Duration-Bewertung. Neuveranlagungen bringen höhere laufende Erträge, Altbestände bleiben kursanfällig. Genau darin liegt der Unterschied zwischen Zinsertrag und Bilanzrisiko.

Inflation erklärt den Druck, aber nicht vollständig. Eurostat schätzt die Teuerung im Euroraum für Mai 2026 auf 3,2 %, nach 3,0 % im April; Energie lag bei 10,9 %, Dienstleistungen bei 3,0 %. Die EZB ließ ihre drei Leitzinsen Ende April bei 2,00 %, 2,15 % und 2,40 %, die Federal Reserve hielt den Zielkorridor bei 3,50 % bis 3,75 %. Daraus folgt keine mechanische Straffung. Es erklärt aber, warum Notenbanken bei Energiepreisen, Löhnen und Erwartungen wenig Raum für vorschnelle Entlastung haben.

Für Europa ist der Rahmen eng. Die Kommission rechnet 2026 nur noch mit 0,9 % Wachstum und 3,0 % Inflation im Euroraum. Entscheidend wird, ob Langfristrenditen wieder fallen oder als dauerhafte Budgetgrenze in Margen, Investitionen, Immobilienfinanzierung und Staatsbudgets eingehen. Für Portfolios im DACH-Raum (Deutschland, Österreich, Schweiz) ist das keine Randnotiz: US-Treasuries, Bunds und Euro-Unternehmensanleihen formen gemeinsam den Diskontsatz vieler globaler Allokationen. Der Hebel wirkt langsam, aber breit.

#Anleihemarkt #FixedIncome #Kapitalkosten #Makroökonomie #EZB #FederalReserve #Risikomanagement

linkedin.com/feed/update/urn…

1

18

Jun 12

Bond yields rise. Markets react.

That's why investors watch them closely.

#BondYield #BondMarket #FixedIncome #GovernmentBonds #BondInvesting #FinancialLiteracy #InvestingBasics #InterestRates #FinancialEducation #FixedIncomeInvesting #BondYieldExplained

12

Jun 12

The countdown is on.

In just a few days, AIQ Markets will be at Fixed Income Leaders Summit USA 2026 in Boston.

Stop by Booth #14 to see how AIQ Insight™ helps traders, portfolio managers, and credit professionals cut through information overload and get answers to fixed income questions in seconds.

Looking forward to connecting with market participants, partners, and innovators shaping the future of credit markets.

#FILS2026 #FixedIncome #CreditMarkets #Fintech #AI #CapitalMarkets

6

Institutional Credit Review: Wagamama Holdings Ltd.🍜

In our latest review, Cognitive Credit AI delivers a deep-dive on Wagamama navigating operational unit economics, structural complexity, peer comparison and more.

Download link below ⬇️

#Bonds #FixedIncome

1

20