Joined May 2020

- Tweets 4,922

- Following 2,046

- Followers 3,993

- Likes 3,490

236 Photos and videos

SirVol retweeted

23 Oct 2025

Long idea pitch time: $DCTH

$DCTH an FDA commercially approved treatment for liver cancer with peak sales estimates around $350M, just saw positive ph2 results in their additional trials which would expand peak sales to ~$500M if approved

Currently trading sub $300M EV ($90M cash, profitable, ramping sales)

Conservative fair value for bios should be around 2X peak sales. Would put fair value around $1B or a 3X from here.

Trading at range lows of 10-11 range. I have traded this twice 9 to 16, then 11 to 16. Now back down to range lows while business outlook just improved so I think next time we test that range high, we break out.

Seeing 20 seems very realistic. 30 (fair value) isn't far-fetched. And in a bio bull, could see much higher as multiples expand beyond fair value.

Even if peak sales are $400M. Still trades sub 1X EV/S (big margin of safety)

The stock was $15 after recent ph2 results, but completely gave back all gains as company pre announced an expectedly weak Q3 and guided down more than analysts expected. For me? Not a concern. This is a treatment that requires many medical professionals. After investing in med tech for a while, it's common for doctors to take summer off for vacation, so it becomes difficult to schedule treatments. Miss was expected and mgmt is early in their launch and learning.

Now we have good and bad news priced in and the price is too low. Expected expanded peak sales from positive data. Lowered 2025 rev guide now we know the extent of pricing discounts for their treatment (~12%) under rule 340B. So it's all baked in / known info.

I wasn't expecting much from their pipeline but this CHOPIN trial data changed my mind. They also have ongoing earlier trials for colorectal and breast cancer. Big positive: they can self-fund trials with cash on hand earnings.

If those succeed, could boost peak sales to $1B , giving reason for this to be a promising long term hold. In that scenario, this could be >7X from here just for fair value.

13

10

152

29,561

SirVol retweeted

26 Jul 2022

From an operations’ standpoint, this makes a lot of sense for $TRMR. Amobees automated platform is proven to optimize results by understanding consumer action across channels. This is huge in a digital world with endless offerings, most of which are all based on story, not data.

26 Jul 2022

$TRMR to acquire Amobee for $239M to expand global market share bit.ly/3Bi4ADg

1

1

11

SirVol retweeted

21 Jun 2022

#TRMR investing $25 million in VIDAA, a smart operating system installed in tv’s etc

They already have a strategic relationship with them

After last nights rumours Tremor are certainly having a busy week

Now if the share £ could just reflect this🤞🏼

I hold voxmarkets.co.uk/rns/announc…

1

1

12

SirVol retweeted

20 Jun 2022

Tremor set for a very compelling acquisition. Sky News have been right with every historic transaction so expect this to happen. news.sky.com/story/london-li… $trmr #trmr @PsychoStock @Yield_Fanatic

1

2

19

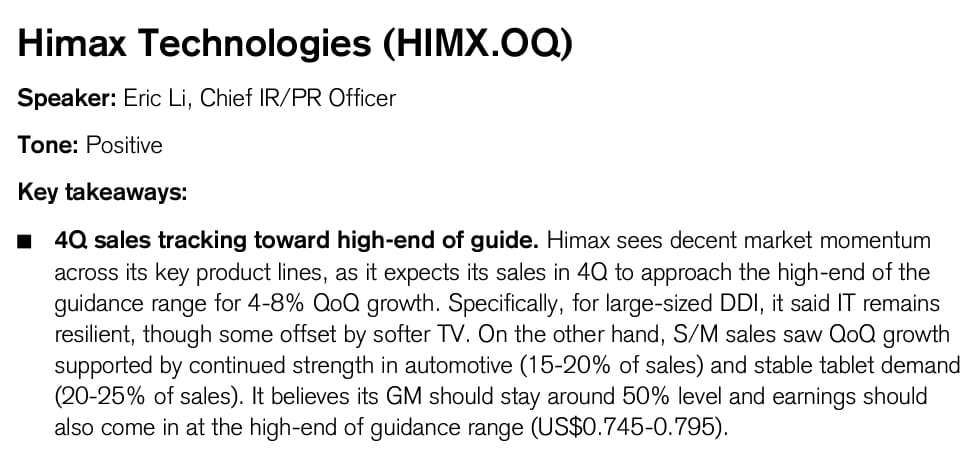

20 Jun 2022

1/

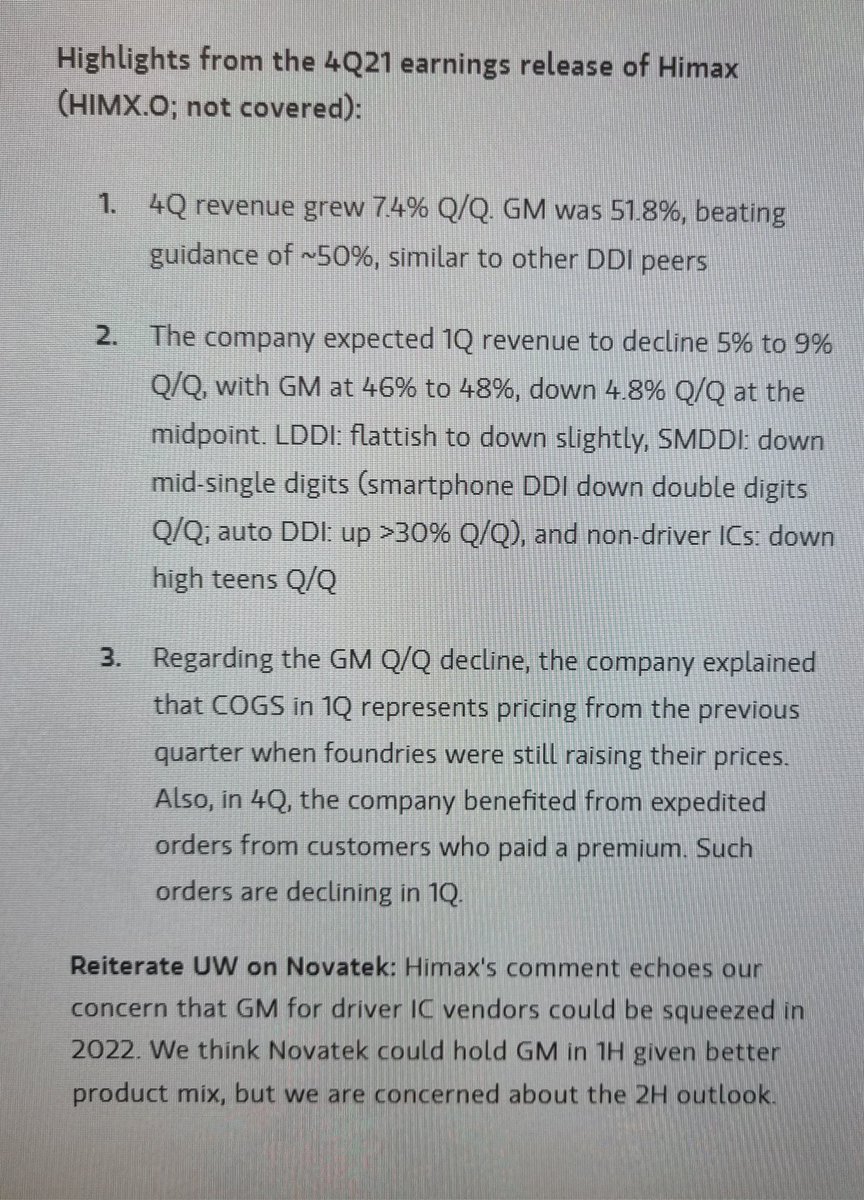

$HIMX updates Q2 guidance:

- Q2 rev now expected to down -22% to -27% qoq (previous: -16% to -20% qoq)

- Gross margin guide unch at 43-45%

- Non IFRS diluted EPS now $0.4-$0.45 (vs $0.45-$0.5 previously)

- IFRS diluted EPS of $0.365-$0.415 (vs $0.415 to $0.465 previously)

2

6

20 Jun 2022

2/

"The revised Q2 guidance reflects weaker macro environment and slowing end market demands, resulting from recent interest rate hikes and inflationary pressure. In response, panel customers are cutting back production and further tightening inventory levels."

$HIMX

3

4

SirVol retweeted

A thing of beauty

68

114

831

SirVol retweeted

17 May 2022

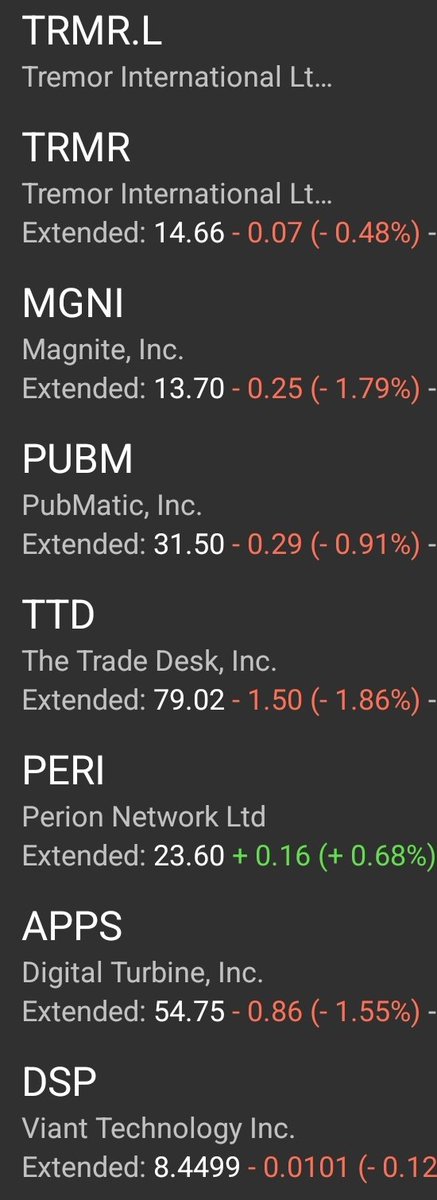

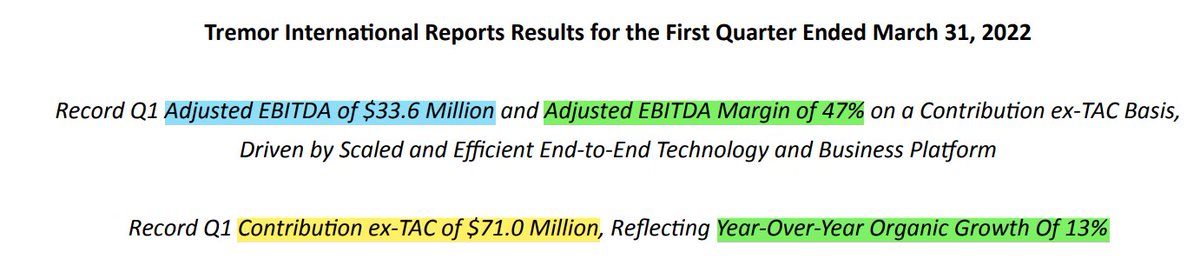

$TRMR's 1Q2022 Results:

- Contribution Ex-TAC: $71m (vs. guidance $73m)

- Adjusted EBITDA: $33.6m (vs. guidance $33m)

- Adjusted EBITDA Margin: 47.3% (vs. guidance 45.2%)

13% YoY Organic growth. Beaten the EBITDA $$ and % guidance .

6

1

20

12 May 2022

Well, I got that wrong on $HIMX. Q2 outlook looks terrible although a lot of the impact is down to Chinese lockdowns. Mngmt noting it will be a trough quarter but even so, despite a 16-20% seq decline in revenue, they are still projecting for a $0.45-$0.50 EPS. Interesting.

2

4

12 May 2022

$HIMX declares $1.25 div. Record date of 30th June, payable 12th July.

Payout ratio of 50% is lower than historical average. "Reflects our decision to reserve sufficient WC in light of macro uncertainty and to facilitate our anticipated growth for the next few years".

3

1

10

12 May 2022

At yesterday's close of $7.97, the 1.25 div represents a yield of 15.6%.

1

5

10 May 2022

1/

$HIMX has been super weak - a lot of this is undoubtedly related to market weakness but this is now a business trading at 2.3x LTM EBITDA and 3.3x P/E.

Of course this is a diff year. Smartphone demand is weak by double digits qoq (further weakened by Chinese lockdowns) ...

1

13

10 May 2022

12/

3. Strong $HIMX EPS even in FY22 means total divi for FY21 FY22 together will be around $3.3 - $3.7.. representing, together, 40-45% of current outlay today!

1

2