India News / Industry Updates / Sector Insights || Not an Investment Advice

Joined May 2024

- Tweets 4,470

- Following 0

- Followers 199

- Likes 47

1,581 Photos and videos

Pinned Tweet

Sharda Motors - Deep Dive Analysis

Meet Sharda Motor Industries Ltd - a hidden auto-tech leader commanding a massive 30% value market share in India's passenger vehicle exhaust systems.

Sharda Motor Industries Ltd is a primary manufacturer of automotive components in India, specializing in the design, development, and production of emission control systems and suspension components. Headquartered in New Delhi, the company was incorporated on January 29, 1986.

Yet, it flies completely under the radar. Let's break down why this is an asymmetric investing goldmine.

(1/12)

#ShardaMotor #LetsDoGreatThingsTogether #SafetyFirst #AIForSafety #DigitalWorkplace #HealthAndSafety

1

19

Sharda Motors - Deep Dive Analysis

Meet Sharda Motor Industries Ltd - a hidden auto-tech leader commanding a massive 30% value market share in India's passenger vehicle exhaust systems.

Sharda Motor Industries Ltd is a primary manufacturer of automotive components in India, specializing in the design, development, and production of emission control systems and suspension components. Headquartered in New Delhi, the company was incorporated on January 29, 1986.

Yet, it flies completely under the radar. Let's break down why this is an asymmetric investing goldmine.

(1/12)

#ShardaMotor #LetsDoGreatThingsTogether #SafetyFirst #AIForSafety #DigitalWorkplace #HealthAndSafety

1

19

THE PEER VALUATION GAP

- Sharda Motor P/E: 12.99x

- Auto Component Sector Average: 50.89x

The market prices Sharda like a sunset ICE supplier, ignoring its negative cash conversion cycle (-31.40 days), massive cash pile, and premium structural pivot.

(11/12)

1

7

THE ASYMMETRIC BET

At ₹782.40, Sharda Motor is a prime compounding candidate. You acquire a dominant supplier for almost free when stripping out the ₹980 Cr liquid treasury.

(12/12)

#ShardaMotor #LetsDoGreatThingsTogether #SafetyFirst #AIForSafety #DigitalWorkplace #HealthAndSafety

5

Centrum || Economy Research

CPI Firms to 3.93% on Fuel Pass Through and Food Rebound

India’s headline CPI inflation under the new Base 2024 series rose to 3.93% YoY in May 2026, up 45bps from 3.48% in April and the highest reading of the new series. The print came in largely in line with our estimate of 3.96% and sits just under the RBI’s 4% medium term target.

The increase was driven by a sharp acceleration in food inflation, which rose to 4.78% from 4.20%, and the first order pass through of retail fuel hikes, with transport turning positive at 1.75% from near zero.

Restaurants and accommodation services accelerated sharply to 5.75% from 4.2% as lower commercial LPG supply lifted input costs, while the personal care and miscellaneous goods division stayed elevated at 18.46%, continuing to reflect surging precious metal prices.

The supply side, however, offers near term comfort as reservoir storage in early June stood above normal level for the period, TOP (tomato, onion, potato) arrivals improved around 5-6% MoM, and the IMD’s two week outlook flagged a less intense heat phase. The risk picture has nonetheless shifted.

The IMD’s second stage forecast places the 2026 southwest monsoon at 90% of LPA (below normal), with a 60% probability of deficient rainfall and El Nino conditions developing through the season.

With Brent in the $90s through the West Asia conflict, the balance of risks to the inflation trajectory is firmly tilted to the upside as we expect CPI to average at 5.1% for FY27.

#EconomyResearch #Indiastocks #Investment #StocksAnalysis #StocksUpdates

33

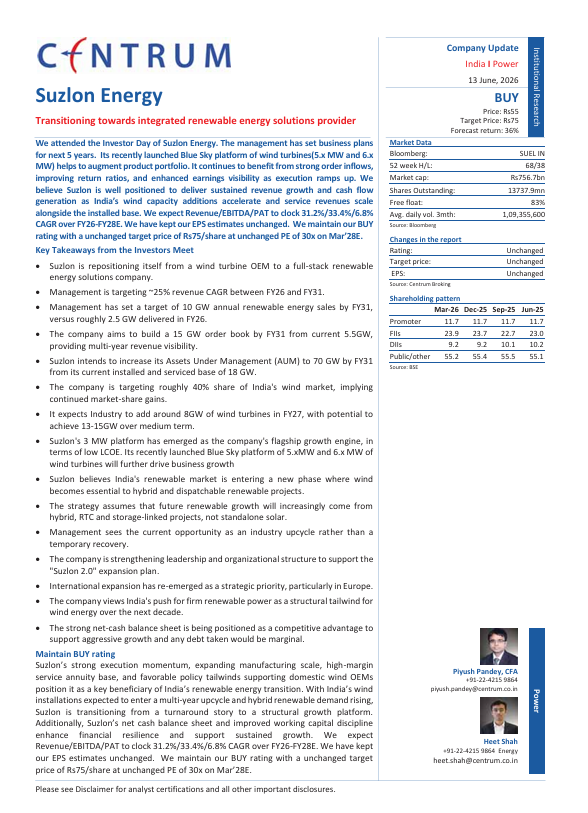

Centrum || Suzlon Energy

Transitioning towards integrated renewable energy solutions provider

We attended the Investor Day of Suzlon Energy. The management has set business plans for next 5 years. Its recently launched Blue Sky platform of wind turbines(5.x MW and 6.x MW) helps to augment product portfolio.

It continues to benefit from strong order inflows, improving return ratios, and enhanced earnings visibility as execution ramps up.

We believe Suzlon is well positioned to deliver sustained revenue growth and cash flow generation as India’s wind capacity additions accelerate and service revenues scale alongside the installed base. We expect Revenue/EBITDA/PAT to clock 31.2%/33.4%/6.8% CAGR over FY26-FY28E. We have kept our EPS estimates unchanged.

We maintain our BUY rating with a unchanged target price of Rs75/share at unchanged PE of 30x on Mar’28E.

#SuzlonEnergy #Indiastocks #Investment #StocksAnalysis #StocksUpdates

1

1

64

Centrum || Cement

Near-term pain, improving risk-reward

We believe recent weakness in cement stocks reflects concerns around Q2FY27 profitability stemming from elevated costs, lower-than-expected price hikes, lokely softness in demand and pricing due to monsoon, maintenance shutdowns and negative operating leverage.

While Q2FY27 is likely to be challenging, our analysis suggests margin pressure in Q1FY27 should be relatively moderate, supported by price upticks and full impact of higher fuel costs likely to be more pronounced in Q2FY27.

We also believe a significant portion of the near-term risk is already reflected in expectations, with Consensus FY27 and FY28 EBITDA estimates across our coverage universe revised down by ~11% and ~7%, respectively, versus pre-war levels.

The Russia-Ukraine fuel shock offers a useful case study, highlighting that cement sector valuations can begin stabilizing well before profitability recovers.

With cement stocks under pressure and sector sentiment remaining cautious, we believe much of the near-term uncertainty is already reflected in stock prices, improving the risk-reward for select names.

At current levels, we see attractive entry opportunities, with UltraTech Cement (UTCEM IN, BUY, TP Rs 13,691) and JK Cement (JKCE IN, BUY, TP Rs 5,990) as our top picks.

#Cement #Indiastocks #Investment #StocksAnalysis #StocksUpdates

26

Jun 12

Antique || Pharmaceuticals

Robust chronic therapy performance continues to drive IPM

The Indian Pharma Market (IPM) grew 12% YoY in May’26 compared to 7% YoY in May’25, while declining 4% MoM.

On a MAT basis (May’26), the IPM registered 11% YoY growth, led by price/volume/new products growth of 5%/3%/3% respectively.

Chronic therapies remained the key growth driver, expanding 15% YoY, while Acute therapies grew 10% YoY. Among large therapies, Cardiac outperformed the market with 15%YoY growth.

The anti diabetic therapy remained a key contributor, registering 15% YoY growth, supported by strong uptake of Semaglutide branded Gx. However, Anti infective/Gastro/ Derma underperformed overall IPM, growing 8%/ 11%/ 11% YoY, respectively.

Company-wise, seven of the top 10 companies reported growth higher than that of IPM for May’26. LPC/INTAS/TRP/CIPLA were the fastest-growing players (posting growth of ~17%/17%/15%/14% YoY), followed by SUN/ALKEM/DRRD. Overall, Indian companies and MNCs reported 12% YoY and 13% YoY growth.

#Pharmaceuticals #Indiastocks #Investment #StocksAnalysis #StocksUpdates

82

Jun 12

Corporate Governance & Promoter Commentary

Corporate governance has remained stable, with a strong focus on capital discipline and transparency.

Zero Pledged Shares: The entire promoter stake of 72.62% is unpledged.

Promoter Commitment: Executive Chairman Nikunjkumar Patel has repeatedly emphasized a focus on organic growth and preserving the balance sheet. During the FY26 earnings call, he stated that while the company will briefly take on debt to fund the massive capex cycle through FY27, their primary corporate goal is to return the company to an entirely debt-free status by FY27-28.

(20/25)

1

28

Jun 12

Key Takeaways

Stellar Growth Profile: A 3-Year CAGR of over 93.6% in revenue and a 99.2% 5-Year CAGR in net profits.

Unmatched Financial Efficiency: Outstanding return metrics outclassing major competitors.

Clean Balance Sheet: Low leverage, virtually debt-free, and an unpledged promoter holding of 72.62%.

Significant Valuation Discount: Trading at just $10.8x P/E and $6.55x EV/EBITDA, representing a compelling entry point.

(24/25)

1

22

Jun 12

Future Outlook & Management Guidance

For FY27, management has guided for a 30% to 35% growth rate in top-line revenues, with expectation of improved operating margins.

This conservative guidance (adjusted down from initial targets of 60%) reflects a strategic pivot towards high-margin projects and cautious working capital management over pure volume scaling.

The company's long-term roadmap focuses on entering the Battery Energy Storage Systems (BESS) market and the utility-scale ground-mount supply segment, positioning APSIL as a highly efficient, multi-vertical green energy champion.

(25/25)

#AustralianPremiumSolar #APSIndia #SolarEnergy #RenewableEnergy #CleanEnergy #SolarPower #SolarPanels #MadeInIndia

33