23 Photos and videos

andany.x (🖤,🤍) ∞ retweeted

Jun 16

Our Mainnet MYT family is expanding.

We’ve integrated @infiniFi's iUSD into our Meta-Yield Tokens, bringing duration-matched, diversified stablecoin yield to the MYT.

Why infiniFi? 🧵

3

15

62

3,287

andany.x (🖤,🤍) ∞ retweeted

Jun 1

After several months of work, I'm proud to announce that EtherFi has made their first deployment to infiniFi - this is strong validation of our neobank distribution thesis!

Thanks to the fantastic folks at EtherFi - this is just the beginning!

8

6

96

8,613

andany.x (🖤,🤍) ∞ retweeted

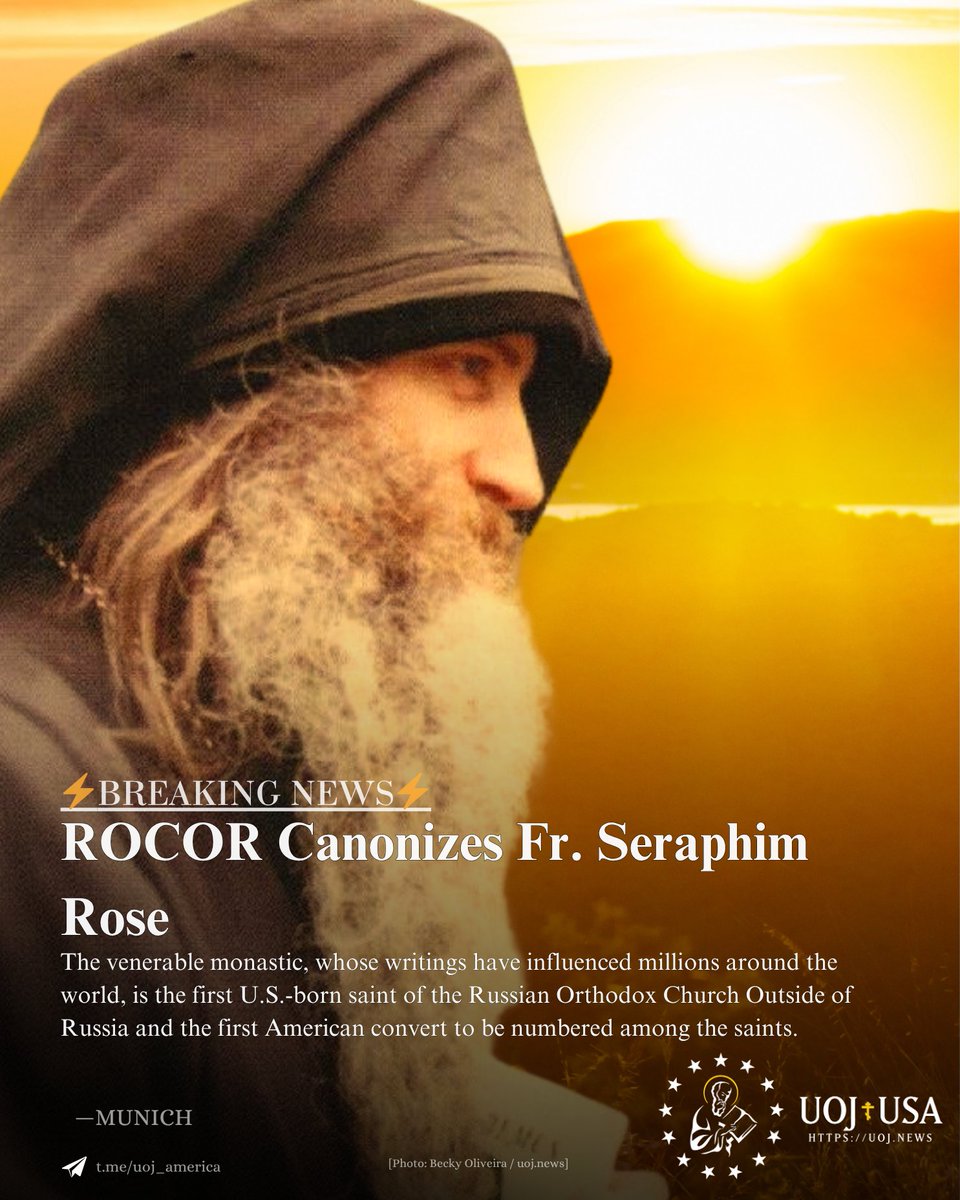

ROCOR canonizes Fr. Seraphim Rose! AXIOS!

32

230

2,237

53,921

andany.x (🖤,🤍) ∞ retweeted

Saint Seraphim Rose

May 4

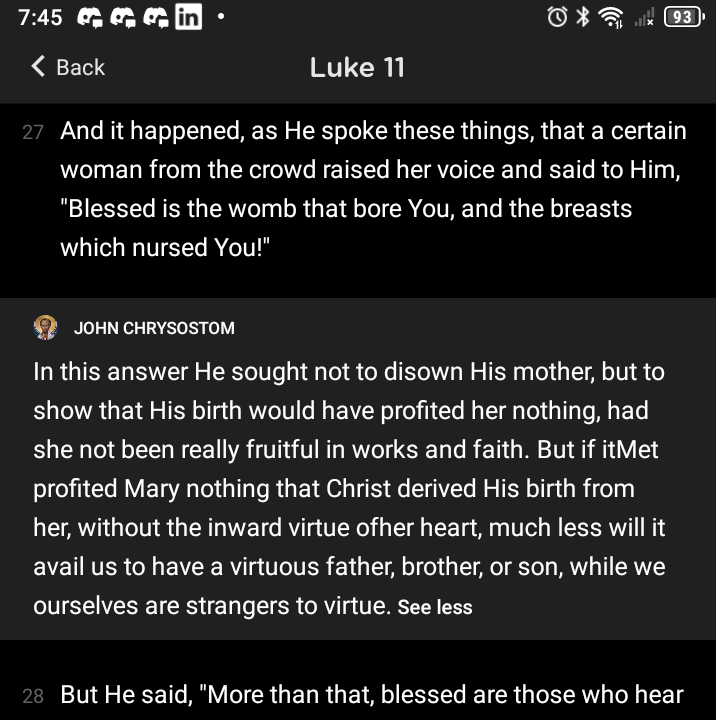

MUNICH — According to UOJ sources, the Council of Bishops of the Russian Orthodox Church Outside of Russia (ROCOR) has canonized Hieromonk Seraphim Rose as a saint. This was first reported by UOJ-Germany.

The decision was reportedly made during Monday's deliberations by the sobor and remains unofficial until a statement is issued by ROCOR. Tentatively, Fr. Seraphim is the first U.S.-born saint of ROCOR and the first American convert to be numbered among the saints.

14

53

521

10,814

Apr 30

This GPT Image 2 prompt is going insanely viral right now.

“Redraw the attached image in the most clumsy, scribbly, and utterly pathetic way possible. Use a white background, and make it look like it was drawn in MS Paint with a mouse. It should be vaguely similar but also not really, kind of matching but also off in a confusing, awkward way, with that low-quality pixel-by-pixel feel that really emphasizes how ridiculously bad it is. Actually, you know what, whatever, just draw it however you want.”

3

5

24

938

andany.x (🖤,🤍) ∞ retweeted

Apr 22

As seen by recent events, the danger of bad debt in defi cannot be overstated. @infiniFi is looking to position itself as the buyer of last resort, a necessary player in any mature market.

Full pod on Thursday.

6

4

26

1,437

1) These hacks in the last few weeks have reminded me why we built infiniFi. Conservative defi has taken a huge hit as a result of the rsETH contagion specifically.

There needs to be optionality in the market for various risk profiles who want to access these yield sources. If you want to take exposure with no insurance (generally most yield opportunities) you might as well get paid a premium to do so via locked iUSD.

Conversely, if you want to truly have a conservative position, you can deposit into siUSD (and earn ~6%) while sitting in an insured environment.

1

3

23

2,115

andany.x (🖤,🤍) ∞ retweeted

Mar 22

One of the things I take for granted with infiniFi is that our system has an embedded proof-of-solvency

If the amount of backing doesn’t match the amount of tokens, infiniFi will not let you do anything until a loss has been realized

What happened with Resolv is something we prevented before even going live - our minter is fully decentralized and has been so since day one.

More people should copy this

7

5

70

5,696

Mar 13

Hello darkness, my old friend.

You asked. We built.

A new dark mode is now live on the infiniFi app 🌑

Let There Be Dark.

1

3

32

infiniFi is evolving - check out the new design👇

Introducing a new look for infiniFi.

We’ve refreshed the branding, launched a new website, & rolled out a new & improved app.

The same infiniFi system, built for what’s coming next.

3

15

19

1,311

andany.x (🖤,🤍) ∞ retweeted

Feb 24

Very proud to share that we're bringing Fasanara's GDADF fund to Mainnet! After an extensive diligence process, we found that this represented an ideal use-case for RWAs on-chain, as the fund has operated for over 8 years without ever experiencing a monthly drawdown

As DeFi takes its first steps into the world of RWAs, infiniFi is proud to be operating near the tip of the spear!

5

18

82

9,072

Tested & Bookmarked.

Go search for infiniFi 👇

Ever had to use a new wallet or defi protocol, googled it, and worried about picking the wrong one from a scam ad?

I built search.defillama.com/ to solve this

It searches over >5k whitelisted domains manually curated by DefiLlama, it's <6kb and loads instantly

Bookmark it

10

23

1,207

Excited for the frxUSD/iUSD PegKeeper pool launch with @fraxfinance on @CurveFinance.

Powering infiniFi's duration engine, keeping iUSD pegged at $1 with deep liquidity & sustainable yields.

Get Started Now: curve.finance/dex/ethereum/p…

Jan 27

1/ @infiniFi is the latest to choose frxUSD as a stablecoin PegKeeper, launching a new frxUSD/iUSD pool on @CurveFinance.

Get started: curve.finance/dex/ethereum/p…

Learn more about infiniFi and the role the PegKeeper pool plays in their protocol👇

2

5

25

1,498

andany.x (🖤,🤍) ∞ retweeted

Jan 26

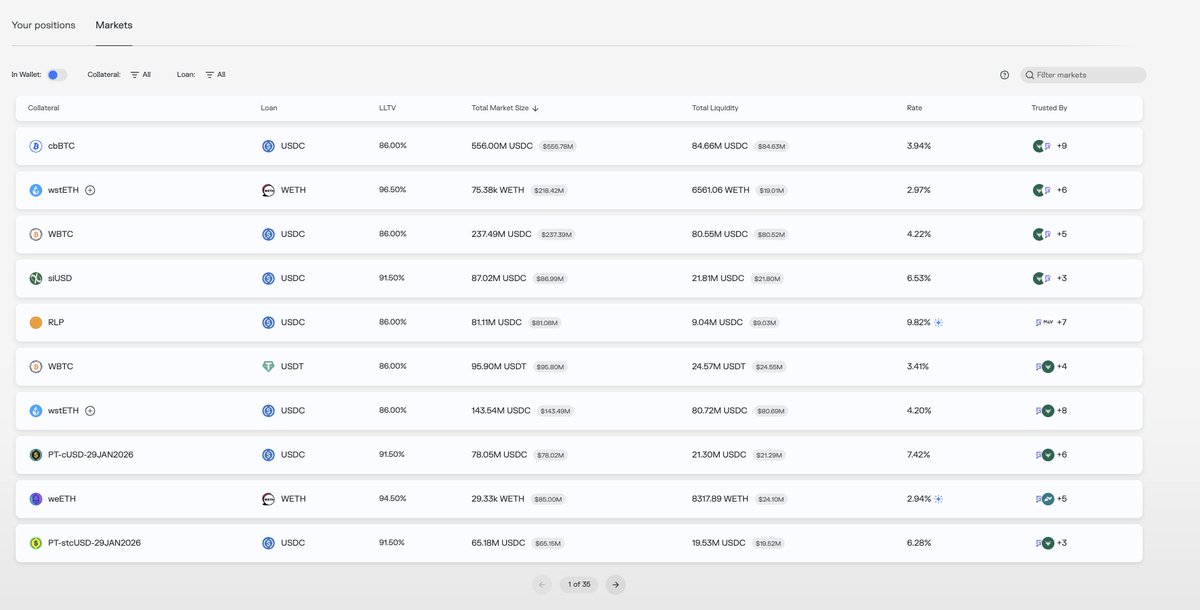

Pretty cool to see infiniFi become the single largest stable-backed market on Morpho 😎

8

6

52

2,771

andany.x (🖤,🤍) ∞ retweeted

Jan 26

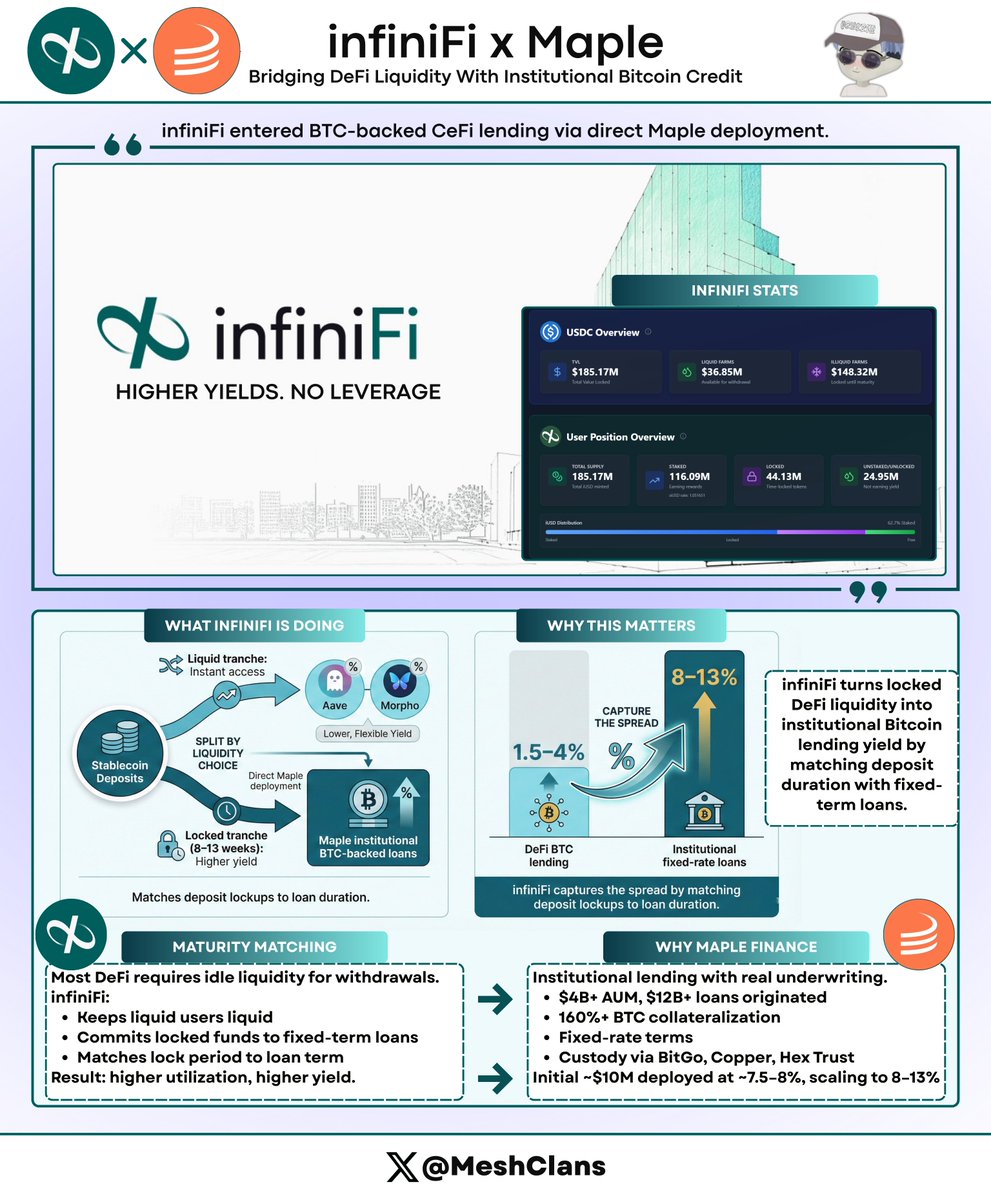

So @infiniFi recently announced they're entering Bitcoin-backed CeFi lending through direct @maplefinance deployment.

Honestly had to dig into what that actually means. Here's what I found:

What are they actually doing?

infiniFi takes your stablecoin deposits and splits them based on how long you're willing to lock them up.

You pick:

> Keep it liquid, get lower rates

> Lock for 1 week to 13 weeks, get higher rates

The locked stuff goes into Maple Finance institutional Bitcoin-backed loans. Market makers and trading firms put up BTC as collateral and pay fixed rates for committed capital.

DeFi rates got crushed in 2025. Bitcoin lending dropped from 6% to 1.5-4%.

But institutional borrowers still pay 8-13% for longer-term capital.

infiniFi is capturing that difference.

What does this maturity-matching thing mean?

Most DeFi lending is instant-access. You can pull your money anytime, which is great, but protocols like Aave have to keep 20-30% sitting around doing nothing just in case people withdraw.

That kills your yield.

infiniFi's approach:

> Want instant access → your funds chill in liquid pools

> Willing to lock → your funds go into institutional loans earning better rates

When you lock for 1-13 weeks, they know that capital isn't going anywhere.

So they can commit it to Maple's institutional loans.

Your lock period covers their loan duration.

How does Maple Finance work?

Maple does institutional lending with proper custody (BitGo, Copper, Hex Trust) and actual credit underwriting.

Their setup:

> $4B assets, $12B loans originated

> 160% overcollateralization (borrowers post $1.60 of BTC per $1 borrowed)

> Fixed-rate terms

> Vetted market makers and trading firms

> Institutions only (regular users can't just sign up)

infiniFi started with $10M at around 7.5-8%, scaling to 8-13% for longer locks.

Here's the thing: you can't access Maple directly as a retail user. It's institutional-only.

infiniFi bridges that gap.

Why are yields higher?

Aave: 3-8% because it's instant-access and needs those liquidity buffers.

infiniFi: Better rates through blended strategies and institutional loan access.

You're getting paid extra for locking.

The longer you commit, the better rates they can get you from institutional markets.

Right now TVL is around $185M with yields around 7-8% on the new Maple deployment.

What do you actually get?

Better yields than Aave without having to:

> Figure out Maple yourself

> Be an institution (because Maple won't let you in otherwise)

> Monitor borrowers

> Rebalance everything manually

You deposit stables, pick your lock period, collect yield.

That's it.

Tradeoff is you're trusting infiniFi's contracts and their allocation decisions. Risks are still there even with onchain transparency.

The capital efficiency thing

Traditional DeFi keeps big liquidity cushions for everyone. Super inefficient.

infiniFi splits it:

> Need liquidity? Funded by liquid reserves

> Willing to lock? Funded by institutional lending

Gets them to 100% utilization within each bucket.

Better yields because they're not keeping 20-30% idle.

Basically traditional banking (borrow short, lend long) but with transparent onchain reserves instead of black box balance sheets.

What this actually means

DeFi is shifting from "farm tokens at 1000% APY" to real yields from actual economic activity.

Institutional lending markets exist. Borrowers pay premiums. But these markets are closed to regular users.

infiniFi solves that.

You get institutional rates without needing institutional status.

That's the regulatory arbitrage play.

The logic is pretty straightforward: capture the gap between crushed DeFi rates (1.5-4%) and institutional rates (8-13%) by matching lock periods to loan durations.

That's what's happening, no fluff.

14

8

55

2,842