Joined June 2009

- Tweets 2,398

- Following 292

- Followers 3,226

- Likes 428

Photos and videos

anil hansjee retweeted

Apr 29

Yesterday we unveiled the latest cohort from R[3]sidency backed by @coinbase, @base, @animocabrands & @foundersfactory.

8 teams building across the Machine Economy.

Meet Cohort R[3]04 ↓

@autodotfun_ @kash_bot @polldotfun @robinmarketsxyz @rosetta_hl @unifiedmargin @betterasaweb

8

16

93

16,603

anil hansjee retweeted

Apr 1

What an evening 🌅

Thank you to everyone who joined our private golden hour soirée. Founders, investors & friends of the ecosystem all in one place.

Special thanks to our co-host @NextBlockvc for making this one happen with us.

Snaps below & video coming soon! See you around @EthCC for the rest of the week.

9

4

29

2,378

anil hansjee retweeted

Feb 25

The IDOS CCA Sale is Live!

- Phase 1 has started and will run for 2 days.

- Phase 2 starts on Friday, Feb 27, and will run until March 5.

- IDOS Token launch on March 5.

Only participate through the @tallyxyz app 👇

292

187

852

205,471

anil hansjee retweeted

Feb 24

Why did idOS choose to use @Uniswap CCA for our token distribution?

Because how tokens launch matters as much as what they power.

If we’re building open identity infrastructure, distribution must follow the same principles.

🧵

198

132

656

62,320

anil hansjee retweeted

Feb 19

One month into R[3]sidency and it’s Base day.

R[3]sidency lead @LataPersson checked in with the cohort on how it’s going so far, while @clemens_ led the first in our @base & @coinbase masterclass series and spent the afternoon in 1:1s with founders.

Watch below ↓

4

5

17

3,822

We are pleased to announce that we have partnered with @Visa to become a direct Visa principal member.

Through this partnership we will:

✅ Facilitate the issuance of virtual Visa debit cards

✅ Act as a BIN sponsor for fintechs and platforms

✅ Enable customers to spend regulated e-money and stablecoins wherever Visa is accepted

This is a major step in making regulated digital money truly usable in everyday payments across Europe.

Read the full announcement here: quantoz.com/blog/quantoz-par…

17

62

244

34,606

anil hansjee retweeted

Feb 11

.@ErikVoorhees asked how x402 could handle pay-as-you-go for LLMs when costs aren't known upfront

So we created a demo for an extension that solves this

See it in action 🌊

6

6

26

4,339

anil hansjee retweeted

Feb 12

The internet for money is at a crossroads.

We let web2 take our data and centralize the social graph.

Stablecoins can either stay open - or get captured.

This time it's in our hands.

🎥 A 22 min documentary on what’s broken, what’s at stake, and how we fix it.

218

148

651

184,069

anil hansjee retweeted

With respect to Haseeb, I think he’s misreading Chris’s argument a bit - and in doing so, actually proving Chris’s point.

Chris is not saying “better regulation will unlock web3 gaming.” He’s saying that finance comes first because it builds the infrastructure - wallets, identity, liquidity, trust - that everything else depends on. Regulation isn’t the missing piece for consumer web3. It’s the missing piece for financial crypto to reach hundreds of millions of people, which then creates the substrate for the next layer of applications. The order of operations matters. You don’t get HTTP before TCP/IP.

Haseeb’s timeline is instructive, but it’s incomplete:

2008: Bitcoin : non-sovereign store of value

2014: Tether : stablecoins

2015: Ethereum : programmable money

2017: ICOs : capital formation

2018: Prediction markets (Augur, later Polymarket)

2020: DeFi : lend, borrow, yield vaults

2021: NFTs : non-fungible financial(ised) assets

2022: DeSci : decentralised science funding and coordination (VitaDAO, Molecule)

2023: DePIN : decentralised physical infrastructure (Helium, Hivemapper, GEODNET)

2024: RWAs : tokenised real-world (existing financial) assets

2024: DeAI : decentralised AI compute and inference (Bittensor, Ritual, Gensyn)

2025: Agentic economies : AI agents transacting, staking, coordinating on-chain

Notice something? The trajectory isn’t narrowing toward finance. It’s expanding outward from it. DeSci, DePIN, and DeAI are not “consumer web3” in the sense Haseeb is dismissing - they’re not decentralised Spotify (yet). They are new coordination architectures that happen to use financial primitives as a foundation. Which is exactly Chris’s thesis.

Definitions matter here. Web3 was never just “consumer apps but on-chain.” Go back to Gavin Wood’s original framing in 2014: web3 is an internet where individuals and their aggregations own their identity, their value, and their data. That’s not a consumer play. That’s a structural transformation of how institutions, markets, and networks operate.

And this is the key insight Haseeb’s framing misses: the defining characteristic of a web3 architecture is that it’s the first time software can make and keep financial promises. That’s not a be all end all - it’s a superpower. It means every application built on this stack can natively coordinate people and capital without intermediaries. DeFi isn’t the ceiling. It’s the floor.

Consider what a DAO actually is: a new form of organisation with a programmable treasury and governance embedded in code. That’s not “finance” - it’s the transformation of the firm itself. Coase told us firms exist because coordination costs are high. Blockchains compress those costs radically. And now, with agentic AI systems that need to transact, own resources, and make commitments autonomously, the case for on-chain coordination becomes not just compelling but *necessary*. AI agents can’t open bank accounts. They can hold wallets. THe emergent properties of web3 are the only way we will continuously organise the world’s data for AI.

On social: web3 social networks are almost tautological. Every web3 wallet is inherently social - it’s built around a self-sovereign identity with a public history of interactions, credentials, and affiliations. The question was never “can we build decentralised Twitter?” The point is to invert the architecture, to make people the platform, not the product. That won’t look like displacing incumbents head-on. It will look like fluid, adaptive networks where the economics don’t depend on lock-in and attention extraction. Here Lens, Farcaster, and others are early experiments, not failed endpoints.

Haseeb says “every single use case in crypto that has worked at scale has been financial in nature.” I’d reframe: every use case that has worked at scale has used financial primitives as its coordination layer. That’s a feature, not a constraint.

Feb 8

With all due respect to Chris, I completely disagree with this take.

Chris argues that "web3," particularly crypto-powered gaming and media, failed due to scams and regulation, and that better regulation will unlock these non-financial cases.

OK, think about this for a second.

Does this pass the smell test?

Do you think web3 gaming failed because of Gary Gensler? Do you think web3 media plays failed because the scammers crowded out the honest media innovators? Really?

If this is true, why didn't they kill financial crypto, which had WAY more of both? Financial use cases were right in the crosshairs of the regulatory harassment, and they also attracted way more scams.

Why shouldn't we instead accept the more obvious answer: non-financial use cases for crypto have failed because no one wants them.

Let's just admit it. They were bad products. They failed the market test. It was not Gensler or SBF or Terra that caused these things to fail, it was that no one wanted any of it. Pretending otherwise is cope.

Enormous sums of capital and talent explored these ideas, and we should acknowledge what we learned. That lesson is not "if we just had better laws, then finally people would finally be using decentralized Spotify" or whatever.

Call a spade a spade. Every single use case in crypto that has worked at scale has been financial in nature.

2008: Bitcoin - non-sovereign store of value

2014: Tether - stablecoins

2015: Ethereum - programmable money

2017: ICOs - capital formation

2018: Prediction markets (Augur, later Polymarket)

2020: DeFi - literally finance is in the name

2021: NFTs - non-fungible financial assets (to the extent they worked)

2024: RWAs (the year BUIDL took off)

All this stuff was adopted bottoms-up. We as investors discovered that people wanted to do these things with crypto. The web3 consumer stuff, on the other hand, was primarily conjured up by investors and pitch decks, ZIRP accelerationism, and "wouldn't it be crazy if" blog posts. This was the opposite of the "what smart people are doing on their weekends" thesis.

In fact, if you go back to the Ethereum white paper from 2014, almost every single Ethereum use case Vitalik describes is financial in nature: token issuance, stablecoins, derivatives, on-chain treasuries/DAOs, on-chain savings, insurance, price feeds, escrow, gambling, prediction markets. It's all in there.

This is nothing to be ashamed of. Finance is almost 10% of GDP. It's an enormous part of the world economy, and banks are some of the lowest NPS score companies in the world. People hate their banks and the outdated financial architectures their money runs on. It's literally why Bitcoin was created. There is so much to innovate in the realm of finance, and I truly believe we are only at the beginning of that displacement. You don't need to assume anything more to project the next 10x in crypto.

The old saying goes "crypto will do to finance what the Internet did to every other industry."

I respect Chris's optimism. But 18 years in, we should not be propagating this meme about consumer web3 use cases as though they're inevitable. If you are hanging around the rim hoping that crypto is going to disrupt media and gaming, you should know the history and look at it with clear eyes.

Now if you as a founder believe that despite that, you know the secret to cracking this market--I respect that, and I certainly don't begrudge anyone to follow their convictions.

But I think it's important that investors be honest that all the evidence points the other way.

2

3

15

1,682

anil hansjee retweeted

Feb 4

It looks like the @billions_ntwk app is leveling up with each update 😌

You may not realize this yet, but you are experiencing decentralized identity in production for the first time.

190

95

637

41,678

anil hansjee retweeted

The transition to an on-chain economy is accelerating, but our identity stack is stuck in the past.

🔹 Stablecoins processed $40T in 2025 (~48% of on-chain volume).

🔹 @idOS_network is launching reusable, privacy-first KYC.

🧵 on why @idOS_network is the missing piece.

53

18

103

119,809

anil hansjee retweeted

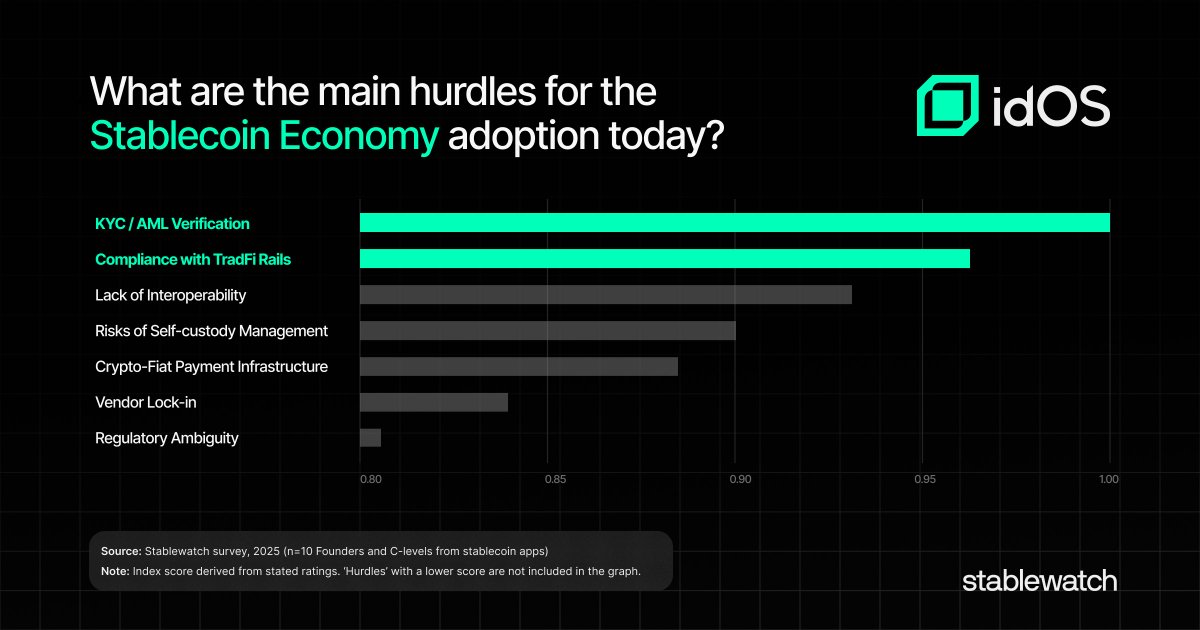

Jan 29

The Stablecoin Economy's Identity Crisis

Our friends at @stablewatchHQ did some research on the hurdles for stablecoin adoption and interviewed 10 founders & c-level executives from leading apps like @aave, @ready_co, & @MidasRWA.

Check the full report in the article below 👇

163

65

482

41,592

anil hansjee retweeted

Jan 22

Today, we're visiting the office of @wintermute_t to sit down with founder and CEO Evgeny Gaevoy, one of our Fireside Faculty. He'll share lessons from over 8 years of building in crypto with our R[3]sidency founders.

Here's what he has to say 👇

3

36

32

6,113

anil hansjee retweeted

Jan 19

We painted the town orange with the launch of R[3]sidency 🟧

Cohort in. Partners locked. Ecosystem government in the room.

Backed by @coinbase, @base, @animocabrands & @foundersfactory, we kicked off 16 weeks of building, shipping, and pressure-testing venture-scale ideas in the UK.

See day zero 👇📽️

21

136

136

20,231

anil hansjee retweeted

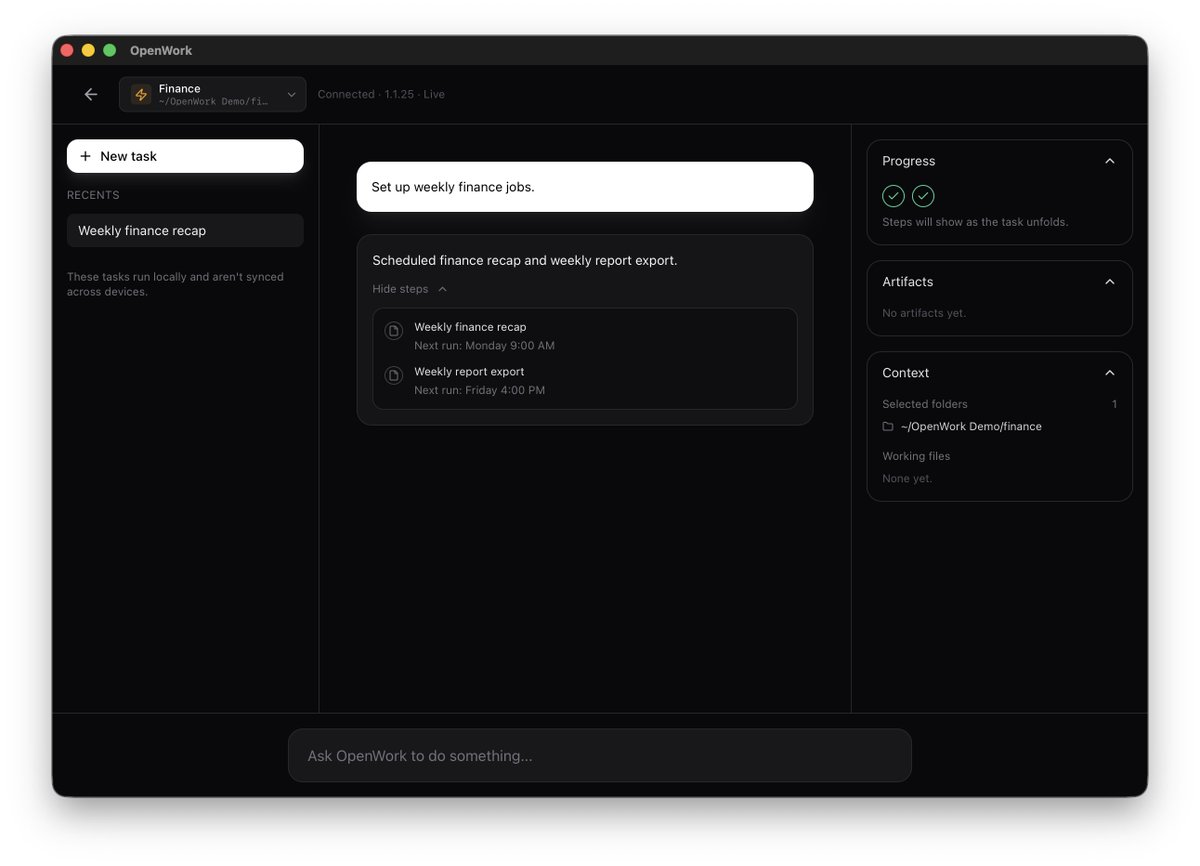

openwork is live. been a wild few days:

- 0-> 1.3k stars on gh

- no product -> live app you can download

- reached front page of hackernews

oh and we're on product hunt today ! if you have some feedback check it out (and if you like upvote!)

producthunt.com/products/ope…

23

9

50

7,792