jack of all trades, master of none

Joined June 2021

- Tweets 1,822

- Following 2,697

- Followers 1,039

- Likes 6,929

58 Photos and videos

Alan Bialo retweeted

20

20

165

19,932

Jun 15

“The Industrial Revolution devalued muscle; the AI revolution is devaluing "pure-compute brains." The winners of tomorrow will be the social system operators who can steer algorithms with language and anchor value with storytelling.”

Jun 14

硅谷PayPal帮主彼得·蒂尔认为,AI正终结过去200年,以数学能力为核心的精英体系。工程、量化等“数学型人才”的逻辑优势,正在被AI迅速替代,其职业护城河也正在消失。未来真正的竞争力,在于叙事、社交语境理解,以及把AI嵌入社会系统的语言型人才,这才是人类独特优势。

工业革命让肌肉贬值,AI革命正在让“纯计算的大脑”贬值。未来的胜出者,是那些能用语言驾驭算法、用叙事锚定价值的社会系统操盘手。

作为程序员: 别只埋头代码,而是要多练自然语言描述问题;学产品思维和用户研究,理解非技术需求;开发时优先考虑伦理、社会影响;选领域深耕;把代码变成“能讲故事”的系统。未来你的优势是“代码 叙事”。所以,年轻人别慌着放弃STEM,也别觉得学文科就躺赢了。真正该练的,是用AI思考更深的问、讲出更动人的故事、构建更复杂的社会系统。蒂尔指出了方向,但真正的游戏,才刚刚开始。

说白了,需要文理兼修,才能走得更远。

3

215

Alan Bialo retweeted

Jun 14

2,791

7,864

39,932

64,310,096

Alan Bialo retweeted

Jun 13

I’ve had a number of conversations with folks inside and outside government about the current situation with Anthropic, and here is what I believe to be true:

— As we know, Anthropic publicly released its Mythos class models earlier this week under the commercial name Fable.

— Fable is Mythos with guardrails. But if those guardrails fail, then you’ve exposed Mythos and its advanced cyber capabilities to people who shouldn’t have them. (Keep in mind that Anthropic itself widely promoted the idea that Mythos was a cyberweapon and needed to be regulated as such. They asked for government regulation of Mythos and championed the guardrails on Fable. If there is a vulnerability — big or small — it is Anthropic’s responsibility to patch.)

— A highly credible trusted partner of both Anthropic and the USG who was testing Fable came forward with a jailbreak of those guardrails. The Admin asked Dario to fix the jailbreak or de-deploy the model. Dario refused.

— In their blog post, Anthropic defended its decision by saying the jailbreak isn’t serious. That is not what the trusted partner and the USG believe; nor is that kind of minimizing language consistent with Anthropic’s brand as the AI safety company. It’s difficult to fathom how they could claim a jailbreak allowing operability of a cyber weapon could be defined as not “serious.”

— In the past, Anthropic has always said that safety must be top priority and taken super seriously. In this case, Anthropic prioritized the continued offering of the consumer model over safety.

— In reaction, the Admin issued the export control. The Admin did this reluctantly. It’s been very surprised that Anthropic hasn’t wanted to cooperate with a reasonable safety request (ie fixing the jailbreak issue). Anthropic’s reaction is very much at odds with their branding and ethos as a safe AI research community.

— The Admin’s hope now is that Anthropic remediates the safety issue, the export control is lifted, and Fable goes back into general release. The Admin wants all of this to happen as soon as possible. It is frankly bewildered that Anthropic hasn’t wanted to comply with safety requests that it previously said were its highest priority.

— Those trying to misdirect and tie this action to the prior DoW/Anthropic issues are wrong. The Admin values Anthropic’s technical capabilities and feels that this issue, while serious, should be easily resolved. The ball is in Anthropic’s court.

2,202

3,240

25,438

7,768,228

Alan Bialo retweeted

Jun 12

When I give my savings to @elonmusk they multiply. When I give them to you and all of the US government, they disappear.

Jun 12

Elon Musk just became the world's first trillionaire.

The typical American household would have to work more than 11 MILLION years to make Elon Musk's level of wealth.

We need a wealth tax.

679

5,769

44,042

791,427

Alan Bialo retweeted

Jun 12

The most important SpaceX detail nobody is talking about: the lockup is staggered.

There is no single 180-day cliff. Insiders get to sell in tiers, starting MUCH earlier than a standard IPO.

Here’s exactly when insiders can start selling:

After Q2 2026 earnings (around August 11): Up to 20% unlocks. Another 10% on top if SPCX trades 30% above the $135 IPO price (so $175.50 ) for 5 of the prior 10 sessions.

Five time-based tranches at 70, 90, 105, 120, and 135 days post-IPO. Each releases 7% of eligible shares.

After Q3 2026 earnings (late October to early November): Another 28% unlocks.

180 days post-IPO (around December 9): Everything else unlocks.

Elon and certain major investors get a longer 366-day lockup. They stay locked until around June 2027.

Some context on the size:

The IPO sold around 555.6M shares, representing roughly 4.2% of total shares outstanding. The other 95.8% was locked pre-IPO. The staggered pool (employees and early backers) is where the early releases happen.

The structure is smart. It spreads selling pressure instead of concentrating it on one day.

Still, watch August earnings closely. That is the first real wave of potential selling, up to 30% of eligible shares. After that it drips steadily through fall.

Float is tiny right now, so volatility cuts both ways.

Not financial advice. This is the lockup mechanics from the S-1 and reporting.

115

209

2,180

412,591

Alan Bialo retweeted

Jun 12

BREAKING: Elon Musk's full speech ahead of SpaceX IPO

631

1,716

13,008

654,530

Alan Bialo retweeted

Jun 11

“People who love all fields of knowledge are the ones who can best spot the patterns that exist across nature.”

― Jeff Bezos

73

644

5,216

243,871

Alan Bialo retweeted

Jun 11

NEW: Argentina inflation slows to an 8-month low.

41

90

1,345

71,067

Alan Bialo retweeted

Jun 10

Business Insider reported yesterday that Citrini Research thinks the AI trade is moving from free AI to tokenomics. Good word. Every founder using agents feels it already. A chatbot answer is cheap. An agent that reads files, calls tools, tries again, tests code, writes reports and runs all day is a small factory consuming tokens, memory, GPUs and electricity. The demo looks like software. The bill looks like operations. Winners will measure cost per useful task: one bug fixed, one insurance claim processed, one radiology worklist triaged, one contract reviewed. Tokens will become like cloud spend after 2010. First nobody cared. Then AWS bills became a board topic. Local inference and edge AI matter for exactly this reason. If every useful workflow crosses a hyperscaler toll road every second, margins flow to the infrastructure owners. If more inference runs on PCs, phones, hospital servers, cars and factory machines, AI becomes an operating advantage instead of a subscription tax. The AI bubble debate is too abstract. The founder question is simple: can this intelligence lower unit cost? If yes, it compounds. If no, it is a very expensive toy.

10

4

52

6,499

Alan Bialo retweeted

Jun 10

NUEVO UPGRADE 🇦🇷🇦🇷🇦🇷

ARGENTINA LONG-TERM RATINGS RAISED TO 'B-' BY S&P

367

1,737

13,835

701,780

Alan Bialo retweeted

Jun 8

13

62

360

241,942

Alan Bialo retweeted

Argentina is the first country in the world to develop a legal framework for AI personhood. President Milei is positioning the entire country as a special economic zone for the singularity. Just that same week, Anthropic called for a global pause on frontier AI.

-- 80% of Anthropic's code is written by Claude. Engineers shipping 8x more per quarter.

-- US added 172,000 jobs in May vs 85,000 expected. Unemployment: 4.3%.

-- Autonomy time horizons are doubling every four months. 100x algorithmic improvement is already baked into existing architectures.

-- The three countries with the highest robotics penetration: Sweden, South Korea, Germany have the lowest unemployment on Earth.

107

374

1,903

231,817

Alan Bialo retweeted

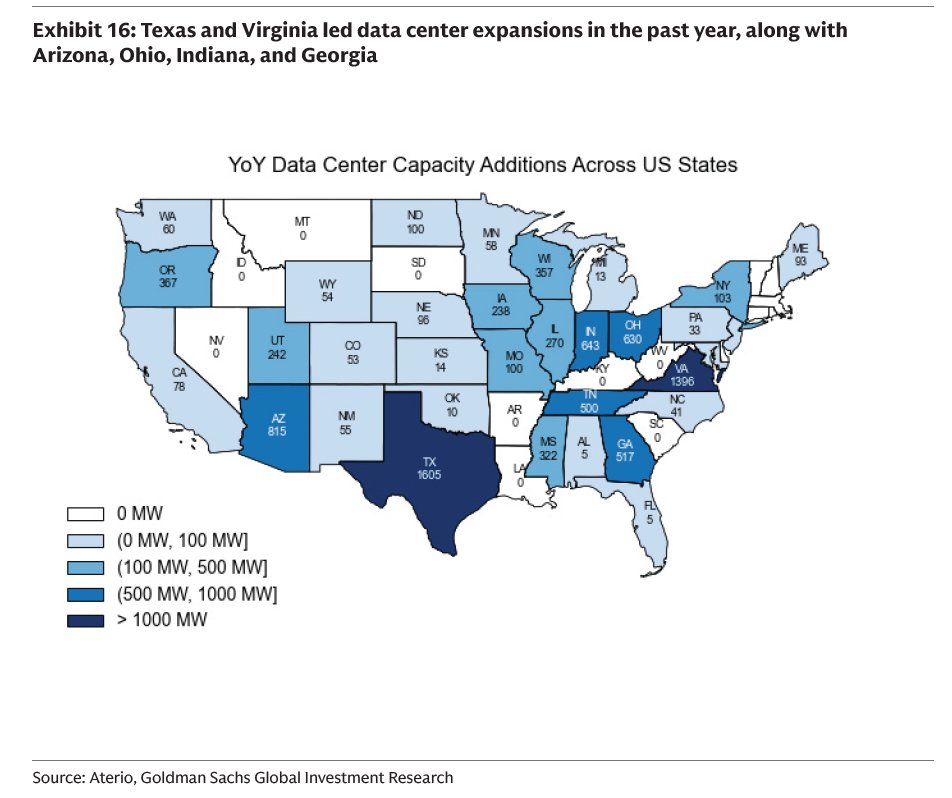

Jun 8

Which states added the most data center capacity in the past year

43

117

585

89,632

Alan Bialo retweeted

Jun 8

Behind-the-meter (BTM) solutions - Geothermal (One to Watch)

As most of you know, powering data centers is a hot topic. Power is a real constraint. Grid connection queues in the US have long lead times right now. And that's why hyperscalers and other companies are increasingly looking for BTM (behind-the-meter) solutions. So you build the power right on-site. Time to compute is still the leading factor here.

You see Bloom Energy $BE making deals for example, 328 megawatts with Nebius $NBIS to deploy fast.

When you look further into the trend, you've got different options. And together with nuclear, geothermal is a very durable one and one that's very overlooked by the market. Google signed a 115-megawatt deal with Fervo. Meta signed for 300 megawatts across Sage and XGS. Further the leading company in it, Fervo, IPO'd at around ten billion, and is currently trading at eleven billion. (See video by @fervoenergy below)

Michael Terrell, Global Head of Advanced Energy at Google, stated that getting to 24/7 carbon-free will take "more than just wind, solar and storage."

And the technology has seen some incredible leaps these past years. Next-gen enhanced geothermal, or EGS, uses the horizontal-drilling and fracking playbook that the shale industry spent two decades perfecting (See AAIG cost curve image below) It used to only work in certain places on Earth, but now, in theory, it works almost anywhere.

So why is it overlooked? Because the share of US electricity generation it makes up today is negligible. Part of the market still sees it as a science project while real projects, with real results, are already being built.

And when you dive deeper into the total addressable market, the IEA sees cumulative investment somewhere near one trillion by 2035, climbing toward 2.8 trillion by 2050.

The bandwidth of estimates how many gigawatts of geothermal can actually come online varies a lot. And that's exactly what makes this a potentially very interesting opportunity, because the sector also has a bunch of inflection points. If they can reach them - which will bring more market adoption- it gives you access to a long-term, durable market with enormous potential to deliver a lot of gigawatts.

We researched a part of this market, and the opportunity, and added a company to our Ones to Watch playbook. The base of this business is very solid and it has geothermal adoption on top that the market hasn't priced in. Very interesting market.

Through our Substack, you can get access to the platform where we wrote it out in full a PDF on the opportunity, on what we see in it, and why it's interesting.

3

3

22

8,878

Alan Bialo retweeted

Jun 3

Welp, that happened faster than I predicted. Thought it would be end of 2027, then early 2027, but agentic traffic growing so fast that bots have now passed human traffic online for the first time in the Internet's history. radar.cloudflare.com/traffic…

388

2,154

8,318

2,247,392

Alan Bialo retweeted

Good take

My guess is

- demand for intelligence is near infinite

- but 80% of workloads will be running on 99% cheaper models within 12-18 months

- 20% of workloads will still run on latest gen models where IQ maxing is important (scientific breakthroughs, higher level ochestrator agents?)

- rough analogy might be what % of macbooks or gaming PCs sold have the maxed out specs for CPU/GPU, prices are falling much faster than Moore's law here though

- this leads me to think the limiting factor will be energy and compute, not better models

At Coinbase we're working hard on routing prompts to cheaper models where appropriate, and in some cases have been able to keep costs roughly flat, while token usage continues to grow exponentially.

Jun 2

The most basic way AI could blow up imo. I'm not saying it does but this is the most obvious way I can see it happening

- Per seat subscriptions are massively subsidized. The flat fee was priced way below what heavy usage actually costs

- For real business use you have to move to the API anyway. Data protections, work integrations and compliance officer approval

- On the API you pay metered rates, and businesses are burning credits way faster than the per seat pricing ever led them to expect

- This is everywhere right now. Internally for us, Codex users, Uber torching its entire 2026 AI budget in 4 months, the Microsoft comments. Just go try an API

I shared more on this here: x.com/Shaughnessy119/status/…

- And I don't think most businesses have the money to keep paying increasing API rates without a real change to how they operate (caps needed)

- Because they have a cheap alternative. They can reach open source models through any aggregator (OpenRouter, Venice, Baseten, Together) and still get strong privacy. Venice private data centers, or E2EE/TEE serving GLM 5.1.

More on open source inference provider raises here: x.com/Shaughnessy119/status/…

- And the discount is enormous. DeepSeek V4 codes within a hair of Opus on SWE bench at roughly 1/30th the price, and the cheapest open models run closer to 1/100th

- Chinese labs open source frontier grade models. The model is the single biggest cost an inference provider has, and they get it for free

- This idea dies if China goes closed source. That is actually bullish web2 AI labs, because if everyone is closed you pay up for the best intelligence. China goes closed source if they are tired of giving away an asset and they want the revenue and data flow to train new models

- Is this showing up in web2 AI lab revenue yet? No. Revenue is off the charts. Anthropic went from 9B to 47B run rate in five months

- So go forward, what happens?

- I think revenue slowly starts leaking to the open source inference providers (see Venice usage, OpenRouter's $113M raise, Baseten is raising at $11B or triple its valuation in three months, on revenue that went from $200M to $600M annualized in a single quarter)

- It doesnt move overnight, but it caps the labs ability to raise prices, and margins are already deeply negative. OpenAI is reportedly running near negative 122%

- With margins that bad there is no cash flow, so the labs are fully dependent on outside capital to buy GPUs, train models, and keep subsidizing usage (I.e. see Google tapping $80b equity sale, granted 30b for employee RSU taxes. Clearly they think Equity is overvalued or you wouldn't sell it)

- The break comes when that capital stops. Pricing is capped so margins cant improve, and the moment investors lose conviction on payback, the whole flow reverses

- Why would they lose conviction on payback? Back to the start - the inability to improve margins or get businesses to pay more

- This is also limiting, if we start making new drugs with AI or create entirely new businesses, you better believe people will pay up to the max for AI usage

475

619

6,651

2,820,525

Alan Bialo retweeted

$IREN: The cloud market's dark horse

I bet most $IREN bulls are starting to get increasingly exhausted by the price action. I certainly am.

However, as long-term investors, we should see day-to-day price action as nothing more than noise.

$IREN is particularly "noisy," which makes it an especially difficult hold. Yet in times like these, it's important to step back and refocus on the company's fundamentals rather than let price action sway one's emotions.

And the way I see it, $IREN's competitive standing is rapidly improving.

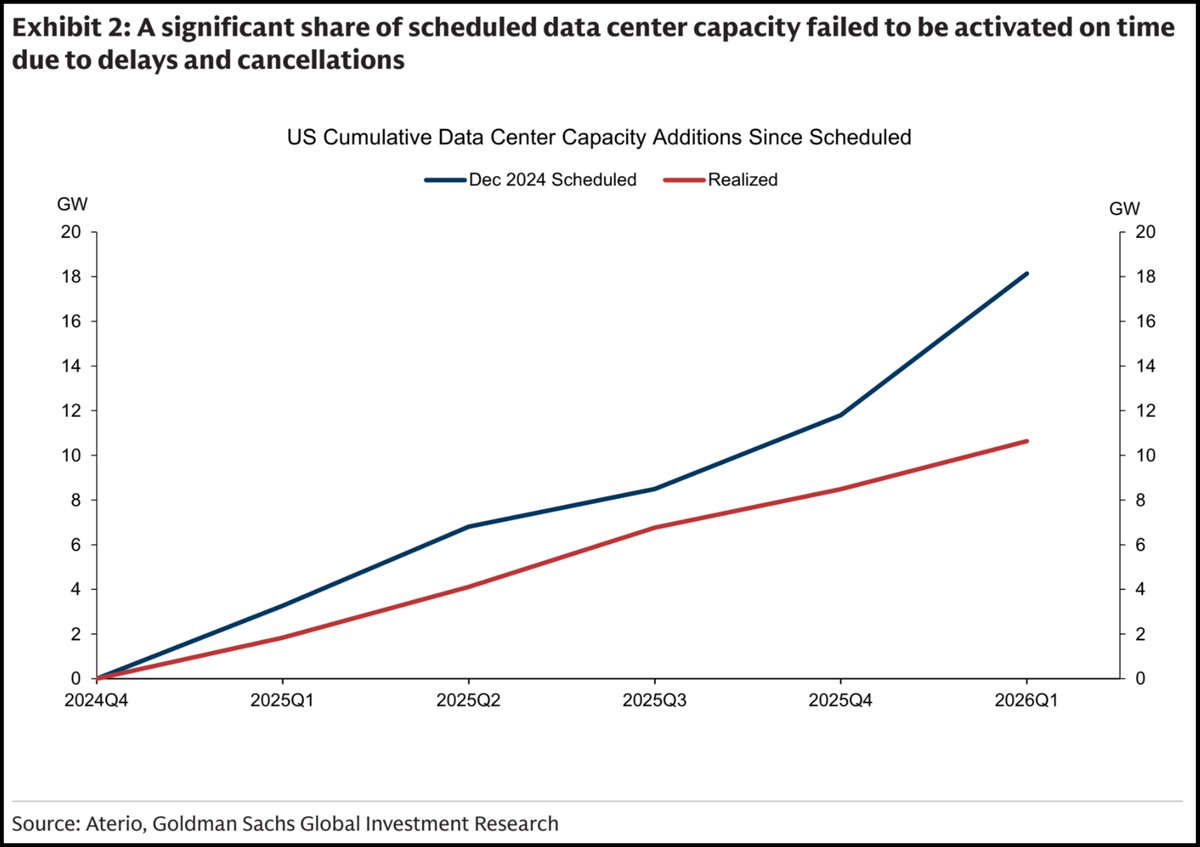

I recently came across an interesting research report by Goldman Sachs that highlighted the discrepancy between planned data center capacity and realized capacity.

Out of the ~18 GW planned to be commissioned over the past 6 quarters, only about ~11 GW actually got built.

Not only is the gap between planned and realized capacity rapidly widening, but the rate at which new capacity is coming online has actually declined over the past couple of quarters.

Much of this discrepancy comes down to power continuing to be a major bottleneck.

As grids get more and more constrained with lead times reaching 5 years, many developers are moving toward behind-the-meter (BTM) generation (on site power generation), circumventing the need for grid connectivity.

Yet that comes with its own set of problems and bottlenecks. The end result is an increasing amount of delays and outright project cancellations.

This industry backdrop plays directly into the hands of $IREN, which now has 5.8 GW of secured grid-connected power across global jurisdictions.

The only reason the industry is switching toward BTM is that it's the only option if you don't want to wait in multi-year queues to secure grid connections. But don't get it twisted, grid-connected power remains the preferred option.

$IREN is in a unique position to capitalize on this structural bottleneck and become one of the few cloud providers that can actually bring on 5 GW of compute capacity over the coming years.

I'd even go as far as saying that this structural advantage is the primary reason the $NVDA partnership came to be.

While $NVDA undoubtedly remains king of the hill, even they face a real dilemma that could cause cracks in their growth trajectory.

On the supply side, they have to come to terms with the fact that the gap between planned and realized data center capacity is widening, while the trend of new capacity coming online is actually decelerating.

This is the issue I just flagged, and it could act as a potential growth bottleneck for $NVDA, since fewer builds means fewer GPU sales.

Layered on top of this is the demand side. It's perfectly clear that demand for $NVDA's AI hardware remains insatiable. However, when looking closer, it's also apparent that competition is increasing.

Pretty much every hyperscaler is working on their custom chips (TPU, Trainium, Maia, MTIA), and not exclusively for internal use cases anymore, but increasingly to service the compute needs of large AI labs. Anthropic alone has signed deals worth billions for Google TPU and AWS Trainium capacity.

Then you obviously have the likes of AMD and Cerebras directly competing against the AI giant, trying to claim market share.

Taken in aggregate, these two issues could gradually lead to a growth problem for $NVDA if not addressed.

This is exactly where $IREN comes in.

They've got the largest secured power portfolio of any neo-cloud at 5.8 GW and growing fast, they develop 100% of their data centers themselves, and they're not building competing silicon.

That makes them the most reliable demand outlet $NVDA can partner with at scale.

The Sweetwater partnership, positioning the 2 GW campus as a "flagship DSX deployment," isn't $NVDA doing $IREN a favor. It's $NVDA solving its two biggest problems at once.

I'm sure you know the popular saying that "history never repeats, but often rhymes." I think today's neo-cloud market is somewhat similar to the dot com era search engine war.

Back then, the front-runners leading the race were AltaVista, Excite, and Yahoo, while Google was a latecomer that ultimately came out on top.

Today, the vast majority of investors in this space are declaring either $CRWV or $NBIS the obvious winners in the race to become the next hyperscaler.

However, I believe the real dark horse that the mainstream doesn't give much credit to is $IREN.

I believe they have all the ingredients to leapfrog every competitor in a short amount of time, in large part due to their structural advantages and pursuing the right long-term strategy from the get go.

The asset-light model, which both $CRWV and $NBIS have been leaning into, doesn't work well in capital-intensive industries, at least not over the long run.

It's somewhat of an oxymoron, since it seems intuitive that one way to circumvent some of the CapEx burden is to outsource from colocation providers.

Yet that approach leaves you with less control, less flexibility, and ultimately higher costs in aggregate in the form of operating expenses (the landlord also has to earn $).

I studied the Bitcoin mining industry for years, and the asset-light model was once a popular strategy around the 2021 bull market. While it proved to be a strong growth lever, it ultimately ended up being a disaster for anyone who adopted it.

Companies like $MARA are the perfect example.

$MARA heavily adopted the asset-light model and grew to become the largest $BTC miner, yet ended up as one of the most unprofitable public miners of all, leading to significant value destruction for shareholders over time.

Once it became obvious that asset-light wasn't a sustainable strategy, $MARA tried to pivot away from it by increasing self-deployments. But developing infrastructure in-house is a much harder discipline to master, and you don't simply switch into it overnight.

$IREN ultimately won the mining race last cycle by doing the exact opposite of $MARA from the start.

They developed all of their data center infrastructure in-house, backed by a seemingly unlimited pipeline of secured power, which ended up making them the fastest growing and most profitable miner of all time.

While the cloud sector has significant differences from the mining industry, the primary drawbacks of the asset-light model carry over.

Over time, it will become obvious to Wall Street and the broader market that this strategy sounds great in theory, but in practice leads to a stack of operational issues and severe margin compression.

Out of the two current front-runners, $CRWV and $NBIS, I think Nebius will do better. They've at least started moving toward a more diversified mix of self-owned capacity rather than purely relying on hosted colocation, which is the right direction even if they're still early in that pivot.

That said, as the $MARA example showed, developing in-house gigawatt projects at scale is not something you learn overnight.

It's clear to me that a player like $IREN, which has been building this discipline from day one, has the most realistic pathway toward sustained, profitable growth in this space.

In my view, $IREN is the dark horse that will end up winning the race. Thus overthinking today’s price action wouldn't do me any favors.

Cheers guys, have a great weekend! ✌️

91

125

1,103

151,756