Joined February 2011

- Tweets 32,835

- Following 4,112

- Followers 49,134

- Likes 43,214

2,247 Photos and videos

Pinned Tweet

Jun 11

Alpha Architect, alongside our affiliated ETF Architect, has overseen 35 351 exchange launches, and every step of the way, we’ve continued improving systems and passing cost savings back to investors.

And today, we’re proud to announce the next step.

4

4

50

9,267

Jun 12

New Post: The Factor Zoo Has Hundreds of Animals — But Only a Handful of Species alphaarchitect.com/factor-in…

1

2

19

2,998

Wes Gray 🇺🇸 retweeted

Jun 11

We invited @SamHartzmark on our channel to put to rest the dividend debate once and for all.

Okay, that's maybe a huge ask... But at least watch the episode and see for yourself!

1

1

2

1,263

Wes Gray 🇺🇸 retweeted

Jun 11

This is literally insane.

His PR was 13.01. He dropped 0.26 seconds in a sprint race to break the long standing world record by 0.05 seconds...in a prelim.

JA'KOBE THARP ARE YOU KIDDING ME 🤯 12.75

✅ NCAA RECORD

✅ WORLD RECORD

#NCAATF x 🎥 ESPN / @AuburnTFXC

44

203

4,133

314,235

Wes Gray 🇺🇸 retweeted

Jun 10

alley oop: etf.com/sections/etf-basics/…

Fair warning: This is the most fascinatingly nerdy niche of the ETF market I've stumbled upon in years. It's gonna get CRUNCHY. 🤓

2

2

16

30,402

Wes Gray 🇺🇸 retweeted

Jun 10

new primer just dropped

the SOFR-FF basis

conks.plumbing/p/the-sofr-ff…

8

14

97

12,500

Jun 4

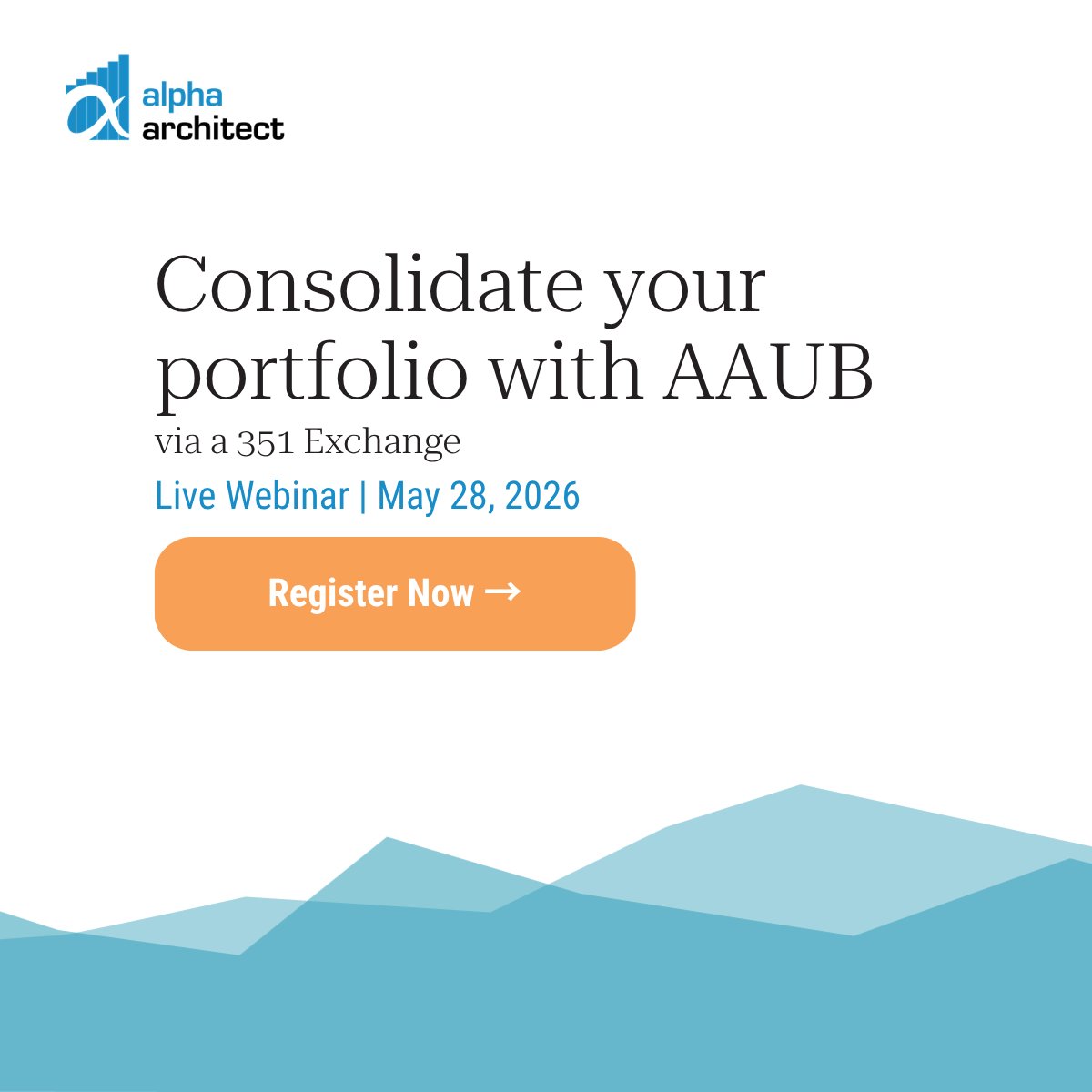

Want to swap an old portfolio for shares of core U.S. equity without triggering a tax bill?

Join me and @UseCache on 6/11 for a LIVE session on how investors may exchange legacy assets for shares in our latest ETF, the Alpha Architect U.S. Equity 4 ETF ( $AAUB ).

Don’t miss it!

Register: us06web.zoom.us/webinar/regi…

Learn more: funds.alphaarchitect.com/aau…

1

1

7

1,448

BUBBLES AND DIVERSIFYING ASSETS

As a large bubble inflates and creates the unbearable FOMO vacuum that sucks almost everyone in, the bubble causes people to sour on otherwise sensible, reasonably high expected-return diversifying investments. One of the signs of the bubble is the expected long-term real returns actually increasing on assets that aren't participating in the bubble.

For example, during the 1999 TMT bubble, U.S. REITs, EM equities, EM debt, U.S. TIPS, Barclays developed gov't debt, and international small-cap equities were all shunned and had their expected returns grow to reasonable levels. You could lend money to Bill and George W. at 4% real because the market loved equities and there was no love left over for anything else! The price of these diversifying investments didn't go up or down much during the 1999 TMT bubble, even though fundamental values did steadily grow, which over time increased the long-term expected returns on these diversifying investments.

Investing in those kinds of bubble non-participants doesn't really protect your mark-to-market relative P’n’L during the bubble. Only being long the bubble can protect your relative P’n’L from the bubble!

However, investing in those diversifying investments does position you well for the bubble burst and deflation, as those investments work well during the deflation stage. Such diversifying investments during the bubble may make sense if you aren't confident about being better at timing the bubble than the next guy.

Of course, those who believe they have the divine touch of market timing will plan to be long the bubble until they can see the eyeballs of the enemy and then rotate to these diversifying investments at the last moment. Godspeed to those of you, whom I know are numerous!

Relating this to my framework about the stages of bubbles:

Steps 5-8:

- Diversifying investments become less correlated with the bubble.

- Diversifying investments start producing disappointing returns.

- Diversifying investments begin to have muted price reactions to legitimately good fundamental news.

Step 9 and after:

- Diversifying investments continue to produce acceptable absolute returns and start producing very good alpha.

- Diversifying investments’ past fundamental news will be reinterpreted more positively as new fundamental news arrives.

THE LIFE CYCLE OF A BUBBLE

1. A genuine advancement creates real productivity gains. A real technological or economic improvement increases productivity and leads to genuine revenue and earnings growth.

2. Stock prices leak into reported profitability. Rising stock prices improve reported earnings, financing conditions, collateral values, and perceived business performance.

3. Reported profitability drives real investment. Companies increase hiring, capital spending, construction, expansion, and speculative investment because of their own or their customers’ reported profitability.

4. Bubble beliefs and abandonment of present-value discipline. Investors stop focusing on discounted cash flows and begin relying on continuing gains from the greater fool theory, believing they can sell later at a higher price.

5. Inflows from sideline investors. Previously cautious investors enter the market in large numbers. New money from existing and new investors participation drive prices higher.

6. Extreme overvaluation. Prices rise far above historical normal multiples of reported fundamentals, even ignoring the fact that reported fundamentals have been driven by rising stock prices.

7. Issuance. Companies take advantage of high valuations through IPOs, secondary offerings, stock-based acquisitions, SPACs, and insider selling.

8. Exhaustion of inflows. The flow of new investors starts shrinking while existing investors approach their risk and leverage limits. Volatility and dispersion grow and gains become less uniform across stocks.

9. Earnings disappointments from slowing price appreciation. As stock prices stop rising rapidly, the earlier boost from higher valuations into earnings weakens or reverses. Companies begin missing expectations.

10. Stock-price collapse with high volatility. Confidence in both the fundamental growth and in the greater fool theory break down and prices fall sharply. Volatility rises further as leverage unwinds.

11. Bear-market rallies and progressively greater exhaustion. Bargain hunters and frustrated latecomers repeatedly buy the dips, creating violent temporary rallies that fail. Markets make lower highs and lower lows.

12. Capitulation, abandonment, and normalization. Bubble participants eventually give up in disgust or exhaustion. Volatility falls, valuations normalize, and the market returns to more ordinary behavior.

10

13

156

59,843

I wrote a new book...

𝗜𝗻𝘃𝗲𝘀𝘁𝗶𝗻𝗴 𝗶𝗻 𝗔𝗺𝗲𝗿𝗶𝗰𝗮: 𝗧𝗵𝗲 𝗥𝗶𝘀𝗲 𝗼𝗳 𝗮 𝟮𝟱𝟬-𝗬𝗲𝗮𝗿 𝗕𝘂𝗹𝗹 𝗠𝗮𝗿𝗸𝗲𝘁

Coming July 4, 2026 🇺🇸

Pre-order: amzn.to/4dOo2sB

9

9

90

14,378

May 31

Stocks are an inflation hedge? Are you sure?

Seems like it all boils down to if the company can boost ROIC.

ksestocks.com/blog/wp-conten…

ht @JohnHuber72

1

2

15

2,565

Wes Gray 🇺🇸 retweeted

May 28

We are at Basis Northwest with @TaxAlphaInsider. Come say hi!

@RyanPKirlin

1

7

1,562

Wes Gray 🇺🇸 retweeted

Dimensional Fund Advisors exploring sale

@dimensional

This will be atypical in the market

Whoever the buyer is, will significantly impact the "story" of DFA going forward

More to watch here...

10

11

126

37,499

May 26

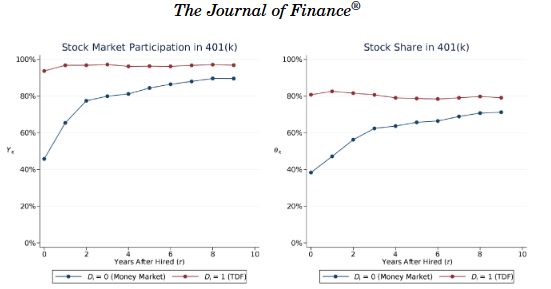

New Post: What Drives Investors’ Portfolio Choices? It’s Not What You May Think buff.ly/X4iVBvE

2

4

23

4,232

May 24

New Post: When Everyone Trades the Same Factor Playbook alphaarchitect.com/factor-st…

1

7

35

4,272

May 24

Updated Post: Long-Only Value Investing: Size Doesn’t Matter! alphaarchitect.com/attention…

1

4

13

2,494

May 24

Updated Post: Why you should trust the investment process (even though it’s hard) alphaarchitect.com/trust-the…

1

1

21

3,538