Cringemaxxing hobbyist intellectual & consigliere to elite startups. Dad to 3 w/ Mrs. of 15 yrs. Unapologetic statue pfp. @UTAustin (Philo/Econ) @Harvard_Law.

Joined November 2010

- Tweets 61,577

- Following 185

- Followers 3,080

- Likes 4,400

1,620 Photos and videos

Pinned Tweet

29 May 2024

Critical commentary about "tech bros" and "mediocre white men" has been circulating the news and mediasphere lately. This inspired me to write another (a third) essay in my years-long rumination on "diversity" in the startup and broader tech world.

siliconhillslawyer.com/2024/…

4

6

54

87,311

José Ancer retweeted

Basically, everyone stopped caring about the Palestine protesters.

WATCH: We asked Google CEO Sundar Pichai for his reaction to 100 Stanford grads walking out of his speech today. @BBCWorld

25

18

772

61,946

56m

A want the ability to have AI summarize chapters in my Kindle books so badly.

18

José Ancer retweeted

Live shot of Elon’s in-house counsel

13

13

607

52,132

Worst: pursue short-term pleasure

Better: pursue long-term pleasure

Best: align your long-term pursuit of pleasure with contribution cross-generationally to a family, community, society, all of which nurtured and sustained you, and will survive you.

57

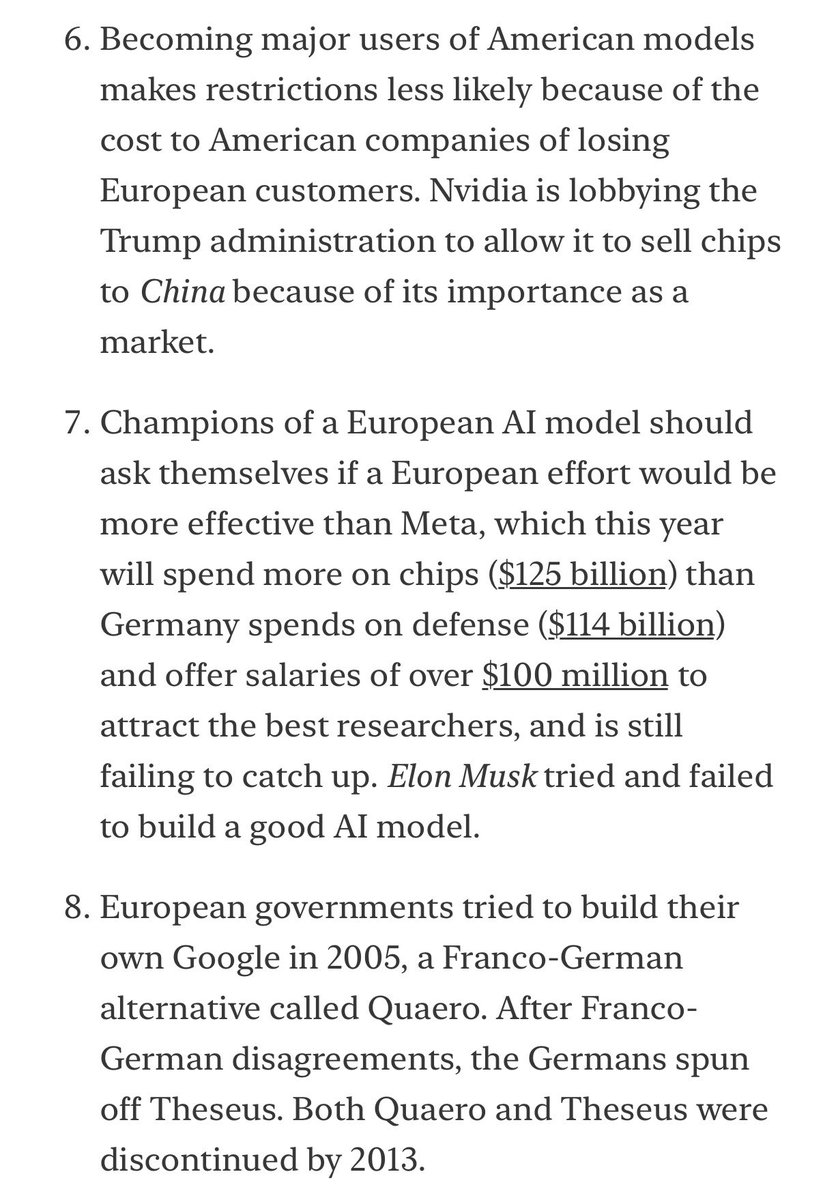

Countries need to be self-aware about their unique strengths/weaknesses, and avoid destructive head-on competition, just like companies.

Competing directly with American AI at its game is a great way to burn 11-12 figure sums.

9h

Good points by @pietergaricano against the idea of a European AI lab national champion. If Elon Musk cannot do it, what chance does the French government have? (I am still open-minded about the question, though I have strong priors against.)

open.substack.com/pub/silico…

1

246

José Ancer retweeted

11h

Totally agree with this great analysis by @michaelxpettis. I would add that the design of China’s post-2008 stimulus plan accelerated and intensified the broader problem of wasteful investment. It added powerful economic incentives to existing political incentives, encouraging local officials to build and invest in projects that often lacked economic sustainability. Visibility projects were one important subset of this broader pattern.

And I completely agree that the advancement of China’s SOEs and the gradual retreat of the private sector should not be understood as an ideological turn, but a structural outcome of China’s political economy model.

Ning Leng makes an important point here: "Over time, state-owned enterprises expand in these spaces because their soft-budget constraints make them better able to absorb the costs of visibility projects."

In a 2012 Carnegie piece I warned that China was finding it increasingly difficult to identify enough productive investment projects (i.e. in which the value of the goods produced exceeded the value of the resources needed to produce them) to achieve the excessively high GDP growth rates Beijing was setting for the economy. If this continued, I argued, we would inevitably see a surge in the country's debt burden and a shift in the share of total Chinese production from private-sector producers to state and quasi-state producers.

The reason was because the private sector mostly operates under hard budget constraints while the state and quasi-state sectors mostly doesn't. This means that private businesses in manufacturing sectors that have growing excess capacity (and over time more and more sectors will suffer from this problem) will find it increasingly difficult to get banks to fund growing losses and rising inventories, and so eventually they would have to cut production.

Because high GDP growth targets required increasing production, rather than cutting it, and because state and quasi-state entities had much softer budget constraints, I argued that this would inevitably shift total production away from hard-budget constrained entities to soft-budget constrained entities, i.e. from the private sector to the state and quasi-state sectors. What many analysts saw as the result of a change in ideological preferences, in other words, is in fact the necessary outcome of the growth model, and this will continue either until Beijing allows GDP growth rates to drop sharply or until the system runs out of debt capacity.

The point is that the regulators can insist all they want that businesses be more disciplined and that manufacturers and local governments behave more rationally, but it is precisely the hard-budget constraint that imposes discipline on investment. By insisting on excessively high GDP growth targets and all but eliminating hard budget constraints, there is simply no way to eliminate involution.

9

11

49

14,502

10h

Creating/elevating new American economic clusters is essential. CA will be at the software frontier for the foreseeable future, but T2 and T3 regions are also rising in their own ways.

The Paradox of California. A cautionary tail.

Fareed Zakaria take nails it 👇

2

2

336

10h

People who spend most of their time in NY, SF, LA are often shocked at how “nice” places like Austin/TX, Miami/FL, Denver/CO, etc can be.

~90% of the bougie amenities of a T1. Great for those not looking to be in the top arena, but still important players in the bigger game.

Jun 12

The elevation of T2 and even T3 American cities is under-discussed. What the Waltons have been doing in Arkansas is part of that.

Spreading dynamism is an antidote to the socio-economic hunger games that generate socialism in dense costal cities.

bloomberg.com/news/features/…

1

151

12h

This is me and my daughter last night.

The one who is nationally ranked in Call of Duty, goes to a gun range regularly, and, should our nation ever devolve into anarchy, will be selected to defend our homestead.

1

4

779

13h

When you hear about X or Y nation being "in decline," that often needs an asterisk in that a ton of its capital is invested in America.

SpaceX is bolstering the fortunes of one of Saudi Arabia’s richest men bloomberg.com/news/articles/…

1

1

147

12h

America was the first culture to apply capitalist economic principles to empire.

You get richer having (meritocratic) rich subjects, not enslaving/exploiting them.

You just need the power gap/hierarchy to remain stable enough to avoid disrupting foundations of the system.

1

36

12h

One caveat is all systems need competition to remain fit.

Thus even nationalists should, counterintuitively, want some strong extra-national competition.

Why I think China's rise, as long as it stays #2, is net positive for Americans.

They help us keep our loonies in check.

25

12h

One obvious point - repeated often about an advantage Indians have as immigrants - is speaking English.

India, UK, Canada = T3 wealthiest immigrant groups to US. All English speakers.

Of course huge other positive selection dynamics as well.

Immigration chart of the day.

Indian immigrants have the highest household income of any country of birth in the United States.

Among the top 20 immigrant groups, Hondurans have the lowest incomes.

2

171

13h

where we're going, anon, we won't need low pay poorly assimilated illegal immigrants

Jun 12

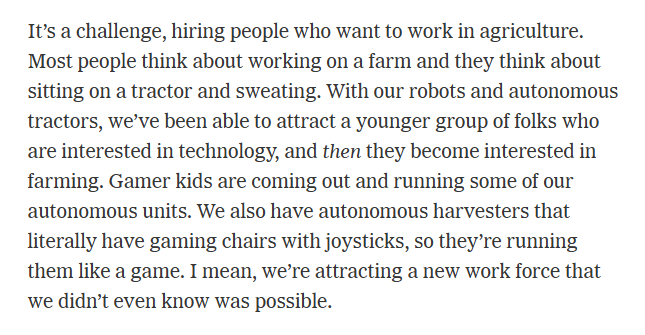

autonomous robot driving through the field at night. no chemicals. no pesticides. just UV light killing pathogens and pests while everyone sleeps. this is @tricrobotics.

this is what chemical-free pest control looks like at scale.

1

99

José Ancer retweeted

It's clear that a lot of people just want to be proud of their country again after a Long Dark Winter when patriotism was basically equated with genocide for a decade-plus

It's not "crass" to lift the national spirit after enduring that, White House should do this all summer

Jun 14

WE HAVE A BALD EAGLE MAKING AN ENTRANCE AT THE UFC FREEDOM 250 WEIGH INS

[ #UFCWhiteHouse | SUNDAY, JUNE 14 | 8PM ET LIVE on @ParamountPlus ]

40

355

4,775

186,281

José Ancer retweeted

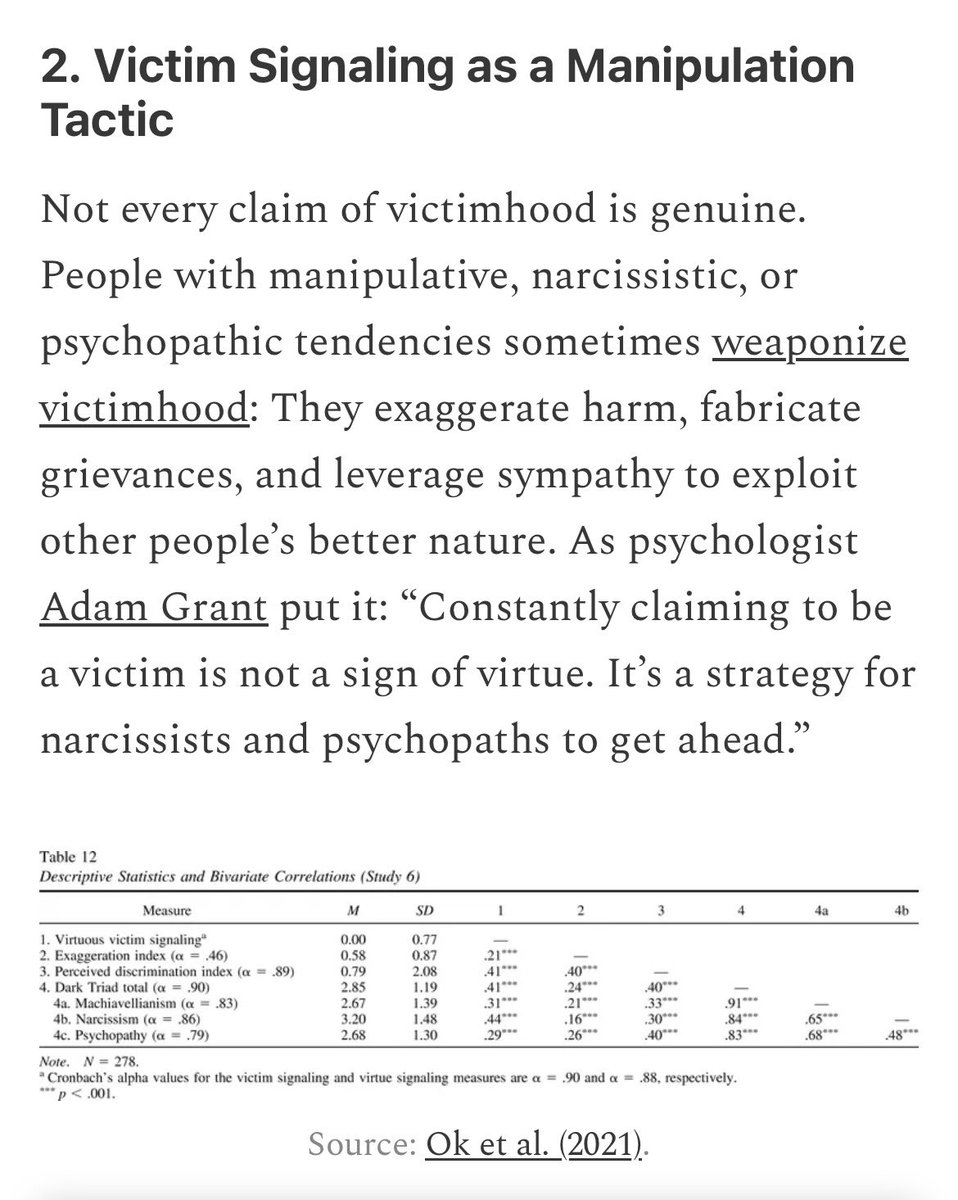

“People with manipulative, narcissistic, or psychopathic tendencies sometimes weaponize victimhood: They exaggerate harm, fabricate grievances, and leverage sympathy to exploit other people’s better nature.”

stevestewartwilliams.com/p/1…

13

100

342

14,189