Senior Product Director @zama. Co-founder @cheqd_io. Co-chair of Technical SteerCo @DecentralizedID. Ex @FinTechLabLDN, @inside_r3, @Accenture

Joined October 2008

- Tweets 11,478

- Following 1,370

- Followers 4,583

- Likes 39,192

722 Photos and videos

Pinned Tweet

Mar 4

Things I wish I could do with AI (that is still surprisingly hard) 🧵

10

32

1,356

Jun 12

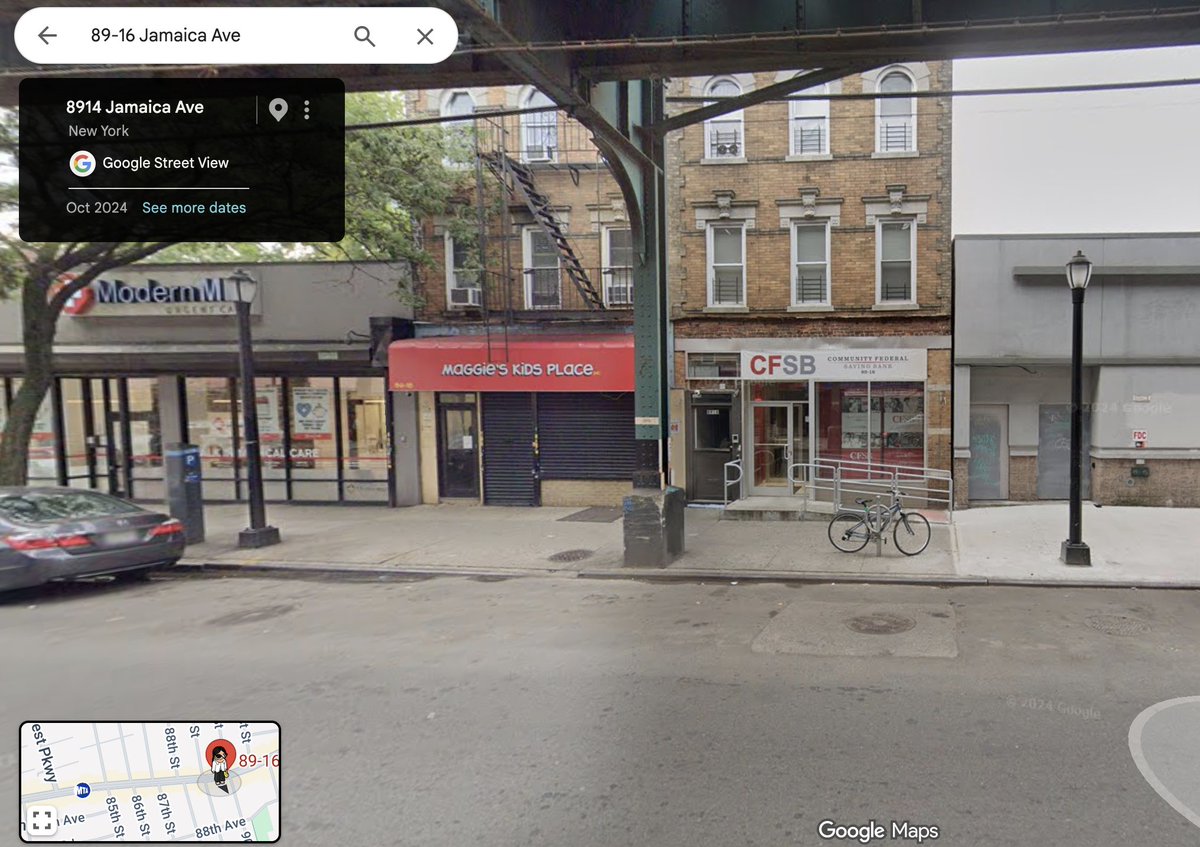

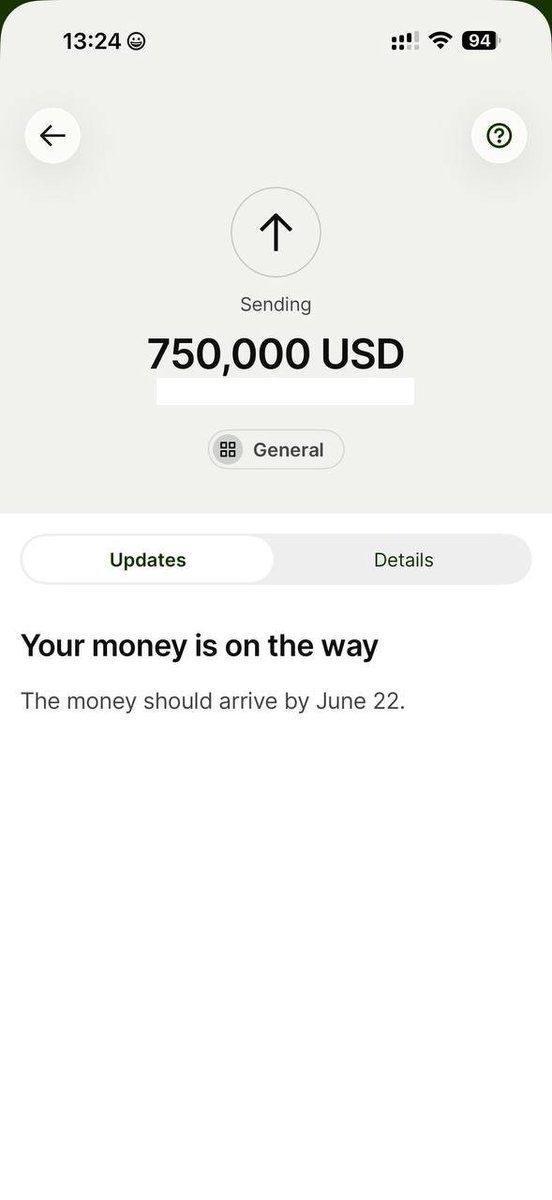

The issue with Wise, especially when dealing with USD, is that they are not the actual bank handling the inbound/outbound funds: the real bank behind the scenes is Community Federal Savings Bank (CFSB).

This is what "CFSB" looks like on Street View. You think you're interacting with Wise, but you're not - the full compliance and payment rails is running through this mom-and-pop bank. There is a huge mismatch in the size of this bank and their capability to deal with it and what a client like Wise puts through their system. More often that not, any significant transfer will likely get flagged for manual processing.

Wise is slightly better when dealing with GBP or EUR as they do have in-house entities with relevant licenses, so they can have better automated processes.

The dirty secret of a lot of fintech is so much of it is a shiny API/UI wrappers around very, very legacy infrastructure.

I'm pretty excited to move off of Wise Business permanently after realizing I can't just transfer my money out when I need to

They keep my money hostage for 10-14 days at least for a big transfer, like they literally won't transfer my money

I remember when dinosaur banks did this? Like they'd purposely delay transfers or not transfer at all in the weekend to then make money on the interest of it

But now fintechs like Wise have started doing it too?

Obviously you don't want to use fintechs to store lots of money, but sometimes you receive money and you wanna transfer it elsewhere (like your broker) but Wise just delays that entire process by 2 weeks, which is quite mad!

Excited to move to @Stripe Business banking ASAP!

1

1

321

Jun 11

Q. What do you ask when your team is missing one legendary researcher to build foundational LLMs?

A. Il y a Sutskever ?

(needs knowledge of French and English)

74

Jun 8

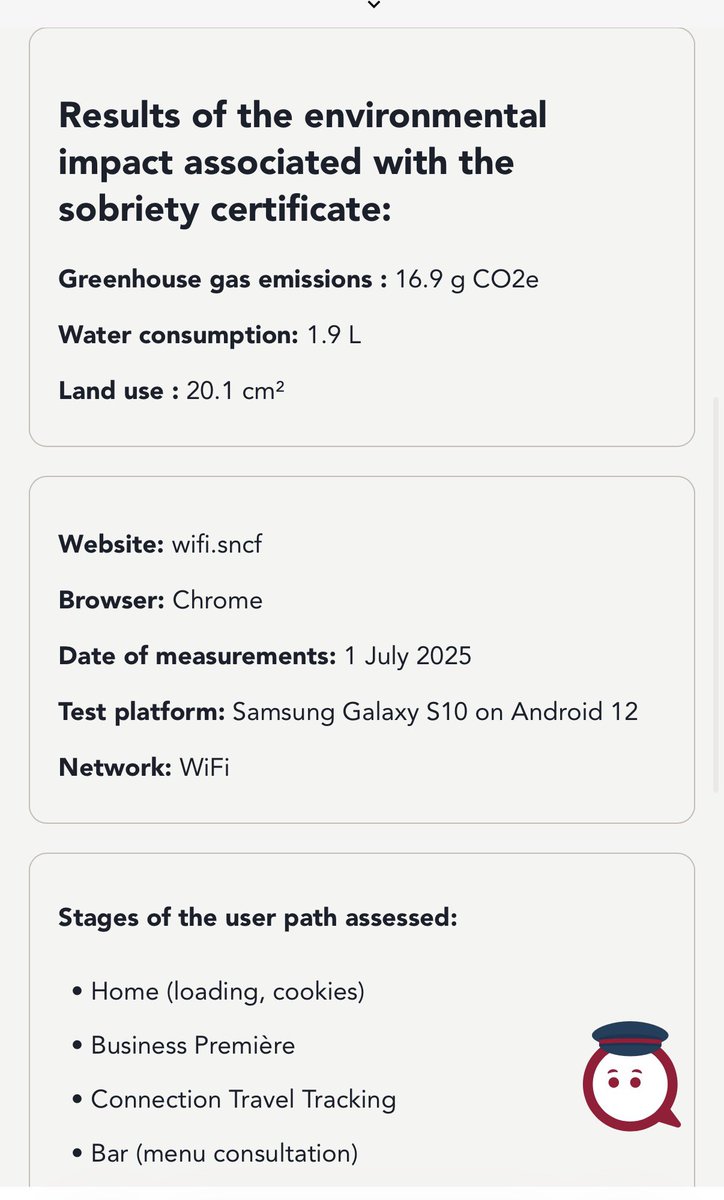

What in the fresh pseudoscience is a “greenspector” certificate?

Basically seems like run Playwright journeys and then apply some magic multiplier based on how long tests run. greenspector.com/en/home/

1

84

Ankur Banerjee retweeted

Jun 3

Welp, that happened faster than I predicted. Thought it would be end of 2027, then early 2027, but agentic traffic growing so fast that bots have now passed human traffic online for the first time in the Internet's history. radar.cloudflare.com/traffic…

386

2,173

8,315

2,240,245

Jun 3

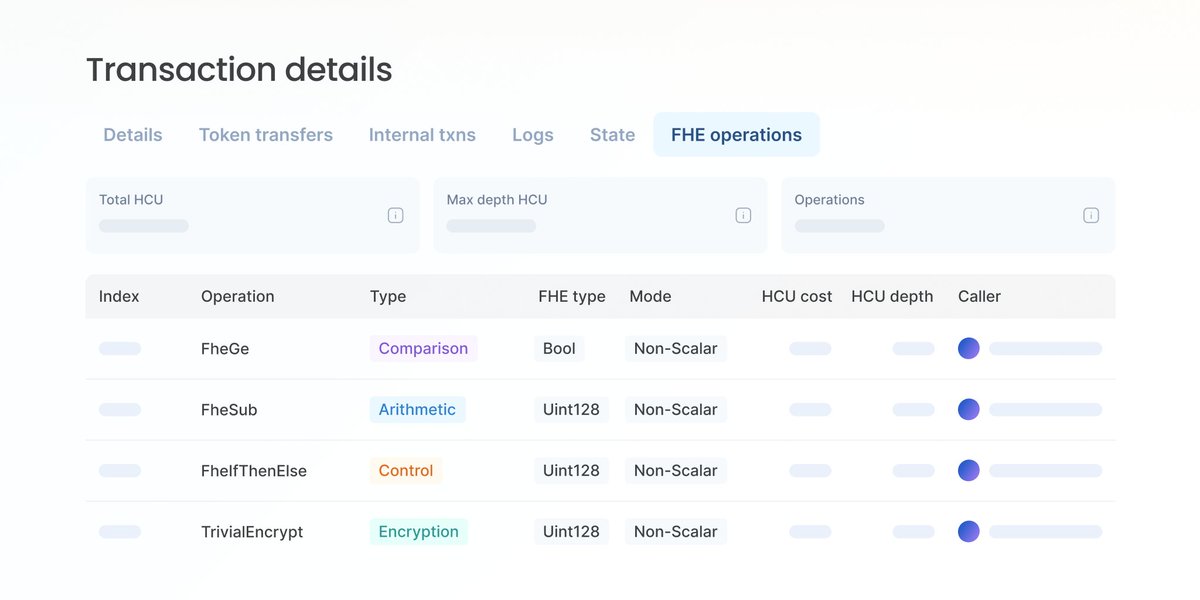

Love this collab with Blockscout to demystify how FHE-powered transactions work on Ethereum - a great tool for anyone building privacy applications on @zama!

Jun 3

Have you explored the "FHE operations" tab on Blockscout yet? 🛡️

Let’s break down a live transaction to see how we maintain total on-chain transparency while keeping your sensitive data completely private. 👇

eth.blockscout.com/tx/0xd2d5…

8

171

Jun 1

The EU used to be a leader in privacy-preserving digital ID for a very long time (2017 to 2024 or so), but has unfortunately since ceded ground to groups that want zk/decentralised only “in theory”.

They’ve got a maximum of 2-3 year more years they can keep coasting on their previous reputation as a supporter of such privacy tech.

But with the way things are heading, they are simply not serious about any of their zk/decentralised work, and the factions wanting to push through centralised, state-controlled tech are growing stronger.

Jun 1

The EU age verification app is presented as “completely anonymous”. But the risk is that member states (the countries are supposed to create their own versions of the open-source EU app) use it to introduce identity verification that makes it impossible to post anonymously on social media.

The idea behind “completely anonymous” is to use Zero-Knowledge Proof (ZKP) cryptography to break the link between the age credential issuer (EU governments) and the regulated services/sites. Currently, the EU app does not have ZKP functionality, contrasting Ursula von der Leyen’s claim that the app ”is technically ready to be used”. But more importantly, the app is designed to always function without ZKP technology; if ZKP is unavailable, the app falls back to a non-ZKP model. Even if fully developed ZKP technology could be implemented in the future, it would remain an optional extra feature that countries may choose to disable and that the EU could remove at any time.

This means that the EU could decide at any time that ZKP may no longer be used, and in one stroke the app would fall back to its default mode, meaning that every post on social media carries an ID tag. By that point, an infrastructure will already have been rolled out; people will have gotten used to it, and it will be harder to roll it back.

More details on mullvad.net/blog/age-verific…

5

422

Jun 1

Many such instances where confidentiality is important 🤭

Jun 1

Anthropic has confidentially submitted a draft S-1 registration statement to the Securities and Exchange Commission.

Pending completion of SEC review, this gives us the option to pursue an initial public offering.

Read more: anthropic.com/news/confident…

3

289

May 22

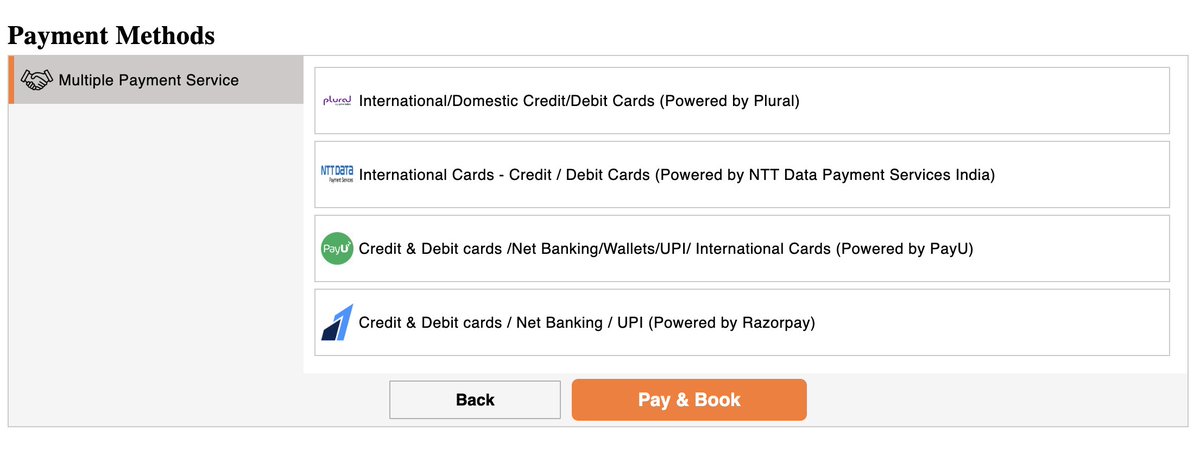

One of the wildest design quirks you’ll find in Indian e-commerce (especially on the Indian Railways booking site) is that the UI forces the user to choose the payment processor.

At a glance, it looks like bad UX. Why make the user choose between PayU, Razorpay, or NTT Data? If the goal is resiliency, shouldn't automated "smart routing" just dynamically handle failovers behind the scenes?

But if you scratch beneath the surface, it’s actually a masterclass in market-specific engineering. It's actually quite clever:

1. Mind-boggling scale: About 50% of ALL online payments globally happen in India. By comparison, US's share of online payments is ~1-2%, Europe is about ~3-5%.

India's real-time transaction volume is huge: 100 billion transactions yearly! That number is greater than the transaction volumes in the US, UK, Canada, France, and Germany combined...and then multiplied by eleven.

(Where India's share is smaller is transaction value. If you want an insight into the future of micropayments, look here. Because the sheer infrastructure strain is immense, no single traditional payment processor can guarantee 100% uptime.)

2. Power-user overrides: If a Stripe payment fails on a regular e-commerce site, waiting 10-15 minutes while the system figures out what happened is annoying but fine.

But on Indian Railways, high-demand tickets sell out in seconds. You're competing with thousands of people for a fixed number of seats releasing at a specific moment. Those 10-15 minutes could be the difference between getting the ticket or not.

So, counter-intuitively, users want to be power users. They'd rather immediately retry with a different processor, than wait for automated fallback logic to catch up.

3. Anti-monopoly by design: On publicly-funded services such as this, locking into a single payment processor would hand one company a dominant position over an enormous share of transaction volume...and the processing fees that come with it.

The multi-processor setup avoids creating that winner-takes-all dynamic. In fact, the order in which these payment processors are shown is also randomised on every page load, so that the order on the screen itself doesn't disproportionately drive volume to a single processor.

4. Transaction costs aren't always absorbed by the merchant: Unlike the West, where merchants quietly absorb a 2-3% card processing fee, in India the processing fees are often directly passed to the user as a "convenience fee."

Different processors negotiate different rates with specific banks, and some pass on the savings to the users, which creates a live competitive market.

Users actively pick the processor with the lowest fee for their transaction based, or cashback provided based on special promotions. It's a local version of pointsmaxxing.

There's enormous richness and complexity in India's payments ecosystem, and more broadly across the global south. It is a fascinating look at high-velocity financial infrastructure built under real constraints: scale, competition, scarcity, that Western fintechs largely never had to contend with.

But that same ecosystem is also ripe for disruption. Moving payments and finance onchain will be a generational shift in speed and cost, but only if the privacy problem gets solved. No national or local payments infrastructure can run without that, as financial data is some of the most sensitive data there is.

138

Mar 4

Things I wish I could do with AI (that is still surprisingly hard) 🧵

10

32

1,356

May 18

Best feature ever, and I wonder why other LLMs do not implement this besides Claude.

1

1

78

Ankur Banerjee retweeted

May 17

The THORchain $10.8M is gone - let's protect the next protocol or wallet.

Here is a short list of ECDSA TSS protocols and libraries that should not be in production right now. The list exists. The deprecations are documented publicly, please follow them:

13

44

261

51,947

May 16

Hard to believe my first song ever on Spotify was Shania Twain 😂

2

1

4

605

May 14

Me too, Golshifteh. The new story I *really* want to read is about how she fared with French bureaucracy like CPAM (the health insurance system). 12 months and waiting to have things finalised by them. 🫠

“She had previously indicated her intent to leave France, explaining that she was severely impacted by the bureaucracy and banking system.”

And on top of that, I do think it’ll be extremely tough for an Iranian person with all the sanctions to deal with French bureaucracy.

2

2

320

May 14

Due to the extremely archaic ways sanctions screening works, any names common in certain communities e.g., from the Middle East get entirely debarked because of partial/fuzzy hits against sanctions lists.

2

65

Ankur Banerjee retweeted

May 14

As crypto matures into financial infrastructure, moats will be defined by security posture, compliance enablement and confidentiality.

We keep treating privacy as a silo - a category or a chain you go to.

Security stopped being a product the moment it became table stakes. Privacy will have the same arc, and those that embrace this sooner than later will own the rails everyone else ends up renting.

1

2

16

313

Ankur Banerjee retweeted

May 7

The team has been working hard on this one.

It's not a refactor or a rewrite, it is a totally new product that is helping multiple teams deliver @zama protocol integrations in record times.

For developers: building confidential dApps just got easier. Introducing the new Zama SDK: a TypeScript SDK that abstracts FHE complexity behind familiar ERC-20-style interfaces.

Build from 0 to a working confidential transfer in < 5mins. Quick start: docs.zama.org/protocol/sdk/g…

1

9

50

9,938

May 7

It’s 2026, and it’s still not possible to provide Gemini with custom instructions/customisation.

In the long line evidence of “Google does not understand how to build consumer apps” 🫠

47

May 7

This has been an exciting project to work on in the past few months, to reimagine what building on Zama Protocol looks like.

The core design principle our team had in mind: how close can we get the developer experience to, say, something like ERC-20? Not “how do we expose FHE to developers” but “how do we make FHE invisible to them.”

Confidentiality on blockchains shouldn’t require a developer to understand the internals of advanced cryptography and mathematics – the same way they don’t need to understand the full HTTPS stack and its library of associated specs to ship a secure web app. That complexity exists; it just shouldn’t be your problem.

One north star metric I’ve always used when building products: can someone build a *meaningful* app in under 30 minutes, starting from scratch with no prior background?

That benchmark is getting even more interesting with widespread access to AI coding tools. We’ll be releasing official Zama skills for the SDK shortly, enabling anyone to build meaningful, secure, production-ready apps with confidentiality baked in. Faster than 30 minutes. A lot faster.

Clear-text in, clear-text out. That’s the principle. Everything else is our problem @zama to solve, not yours.

For developers: building confidential dApps just got easier. Introducing the new Zama SDK: a TypeScript SDK that abstracts FHE complexity behind familiar ERC-20-style interfaces.

Build from 0 to a working confidential transfer in < 5mins. Quick start: docs.zama.org/protocol/sdk/g…

2

148

SHIELDED PREVIEW

→ Fastest privacy protocol to reach $100M TVS

→ 45% of circulating $ZAMA staked

→ #1 app on Ethereum during the Auction

Public release tomorrow. Stand by!

zama.org/shielded

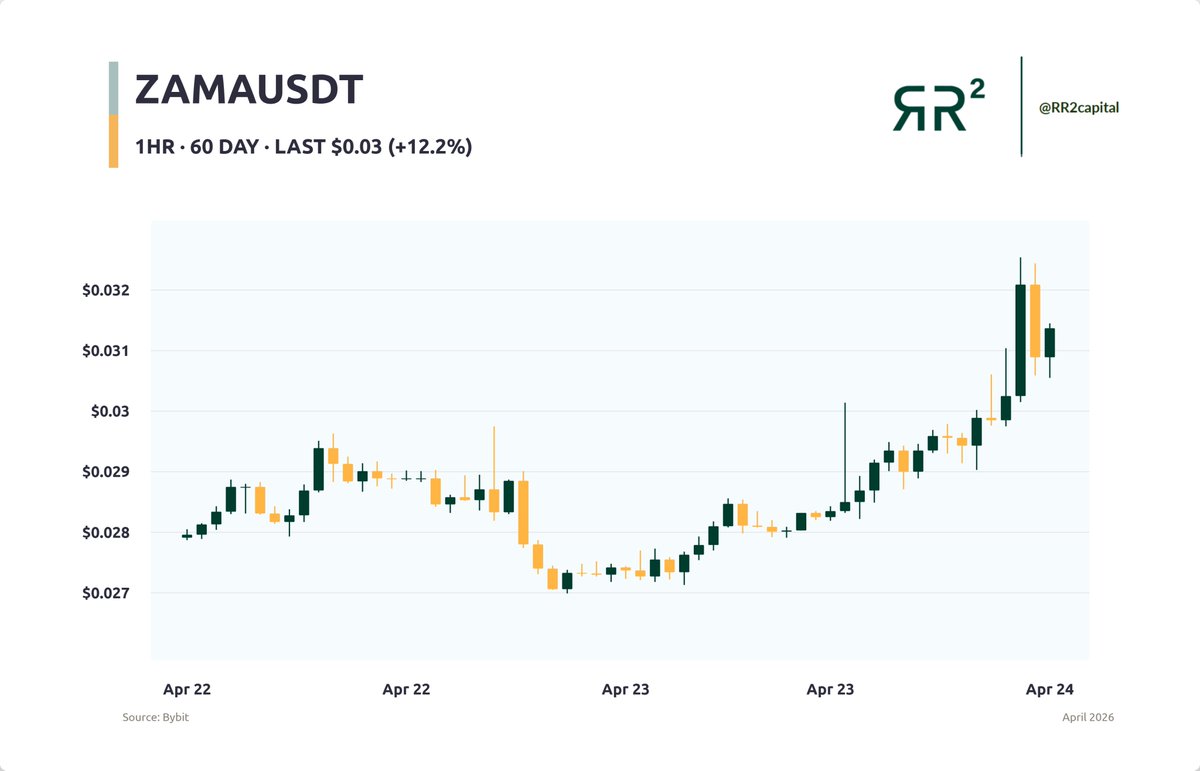

Apr 24

We tracking almost all privacy sector projects

Listened to the Shielded quarterly report yesterday from the ZAMA team

Really pro and a lot of alpha on that call

Price following fundamentals it seems ⚡️

10

22

135

11,138