1. Track: Businesses 2. Analyze: Results 3. Listen: Management Commentary 4. Check: Worth Investing? 5. Repeat

Joined August 2024

- Tweets 362

- Following 47

- Followers 154

- Likes 85

273 Photos and videos

May 11

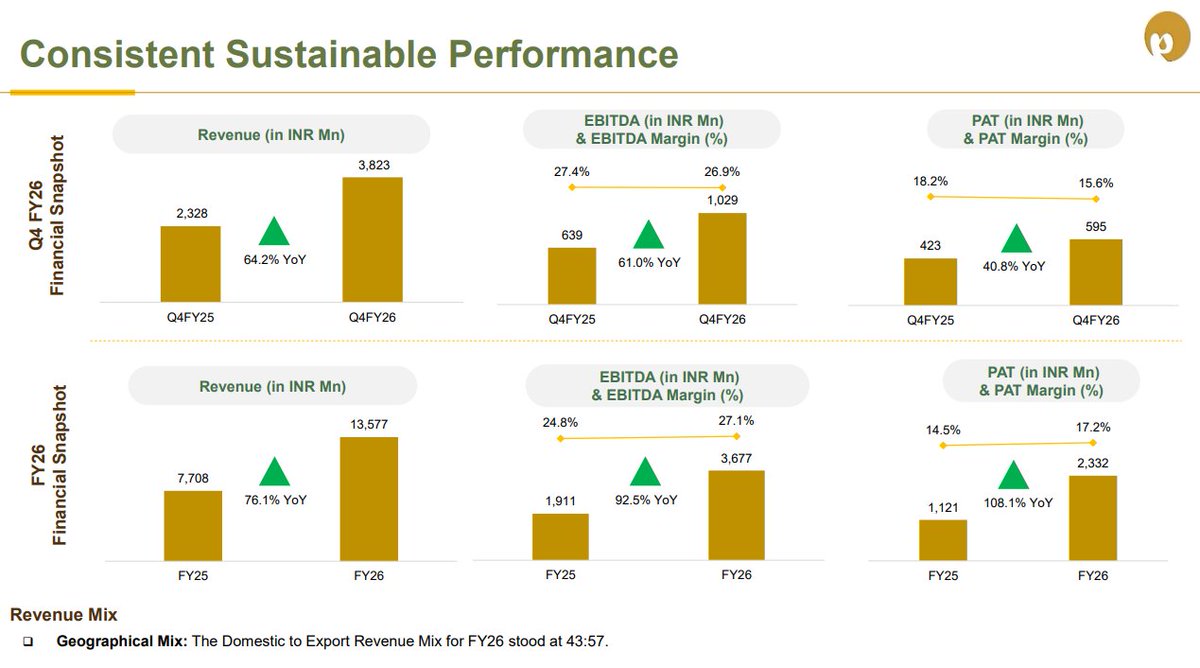

Manorama is no more just a new kid on the block. It continues to maintain legacy of high growth trajectory.

This quarter and FY26 again has delivered robust numbers

Q4FY26:

Rev: 64%, EBITDA: 61%, PAT: 41%, EBITDA%: 26.9% (-54 bps), PAT%: 15.6% (-259 bps)

FY26:

Rev: 76%, EBITDA: 92.5%, PAT: 108%, EBITDA%: 27.1% ( 230 bps), PAT% 17.2% ( 264 bps)

PAT growth is bit slower.. feels bad to call 40% growth bit slower but that's the kind of expectation with go in with Manorama isn't it?

Looking at details - cost of goods has spiked in Q4 impacting gross margins thus effect flowing down to EBITDA % and PAT%

Concall can throw more light on developments. but after raising guidance twice in FY26 they have even surpassed that delivering 76% yoy revenue growth, which is awesome!

More capex is on cards so more room for growth May Manorama keep doing good stuff it does..

#q4fy26 #manoramaindustries #highgrowth #fmcg #confectionary

72

May 11

Slightly longer post, but be patient while reading!

That was the exact message I shared exactly 15 days ago that everyone is talking about today - "Don't get carried away" looking at Q4FY 26 results

Watch this - youtube.com/shorts/VSXnlQnfi…

- War pressure wasn't felt much in Q4, probably only in just last 3 weeks of march, which will obviously be a different situation in Q1

=> Higher energy prices

=> Delayed or less fuel/gas supply

=> Other raw material price inflation

=> Lower demand due to job cuts/ poor job market sentiment

=> Lower price inventory now already over/consumed

=> Pressure on Rupee resulting in expensive imports

=> Softer and delayed Monsoon expectation

This will hit probably all the businesses in some way or other immediately or with delay and directly or indirectly.

So, don't get gung ho looking at Q4 results, that's driving a car looking in the rear view mirror.

Not to forget - businesses closer to vulnerable strata - tier 2/3/4 could be even more impacted with energy crisis - If you listen to news emerging from rural/ semi urban areas - diesel/ petrol availability is a big challenge, LPG situation is neither great.

e.g. farmers who get farm harvested using rented tractor/ machines aren't getting diesel, labor costs have also surged. This is ground reality. Many have moved back to coal, firewood.

So, MFI upturn which we are witnessing currently on back of improving profitability after long period could get hit again and their good times could end abruptly.

Don't be even surprised if companies reduce their guidance, lower down growth/ margin forecast or reduce or delay capex plans - all this will mean slowdown and that's not going to be liked by market.

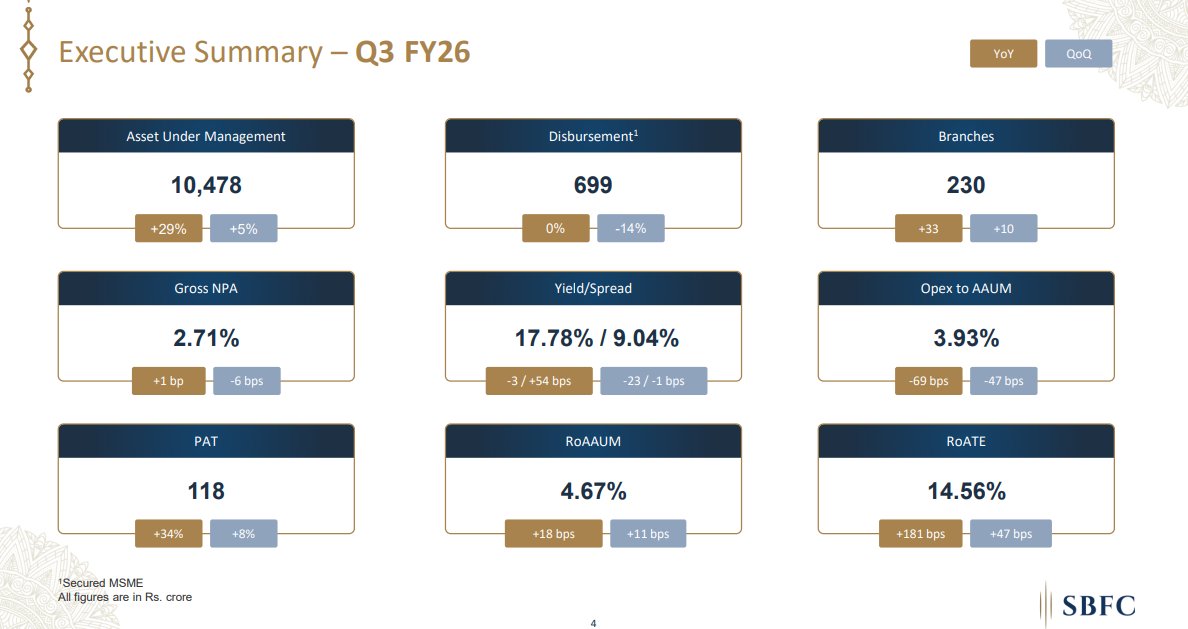

Already DCB, KVB banks, SBFC have toned down investor expectation with cautionary stance - just an example.

Doesn't mean companies wont find ways to navigate around this situation but wont even be able to stay 100% isolated from impact.

So, analyze whatever stocks you have in your portfolio from a above scenario lens and then decide pace of capital deployment.

Go Slow!

#q4fy26 #middleeast #war #crude #highenergyprices #modi #gold

1

112

May 7

Market taking cognizance of RR kabels result and suddenly realizing why the hell were we giving lower valuation to RR kabel ?

RR Kabel's re-rating is result of better performace and it now is standing next to the likes of KEI amd Polycab and not behind them, which was the case in the past.

And that's the beauty of the market.

When company keeps delivering and promises to do so in future, market has to take note of it some day especially when it's products are selling like hot cake.

#rrkabel #polycab #kei #q4fy26 #wireandcable #rerating

1

140

Mar 22

India is that child in a school that is above avg. but situation demands you to be topper in every subject as of now...

India despite advancement seems vulnerable on so many fronts with oil/gas dependence, low manufacturing base, lack of readily available rare earths, chips.

Anything blows and we are caught offguard...

That though is changing but pace is very slow...

#India #War #middleeast #oil #imports

51

Mar 20

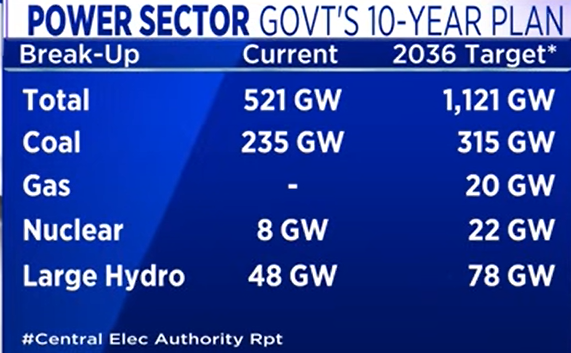

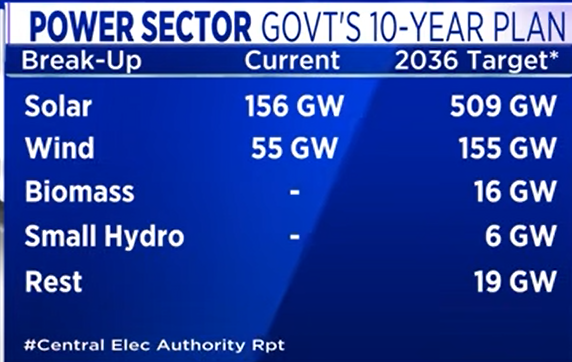

Bharat Electricity Summit 2026 Announcements:

1. Material change in the energy basket with solar, wind & hydro growing meaningfully vs traditional methods such as coal based (PFA).

2. Overall power generation capacity to more than double by 2036 to total 1121 GW out of which Solar will 509 GW (~50%), Coal (~28%, down from 45% contribution as of now), Wind (~14%) will be third largest segment

3. New transmission lines ~1,37,500 km transmission lines to be setup and 8,27600 MVA substation capacity to be installed While, this happens old transmission lines may as well need upgrades

In a Nutshell, any company aiding in this journey benefits with better demand - likes of equipment manufacturers - like transformers, power equipment & power systems, cable & wires also EPC players catering to this space.

There could be near term hiccups due to raw material cost spike, but don't forget this theme will play out over next decade

#power #renewables #transformers #powersystems #kei #polycab #transrail #qualitypower #taril #tdps

69

Feb 12

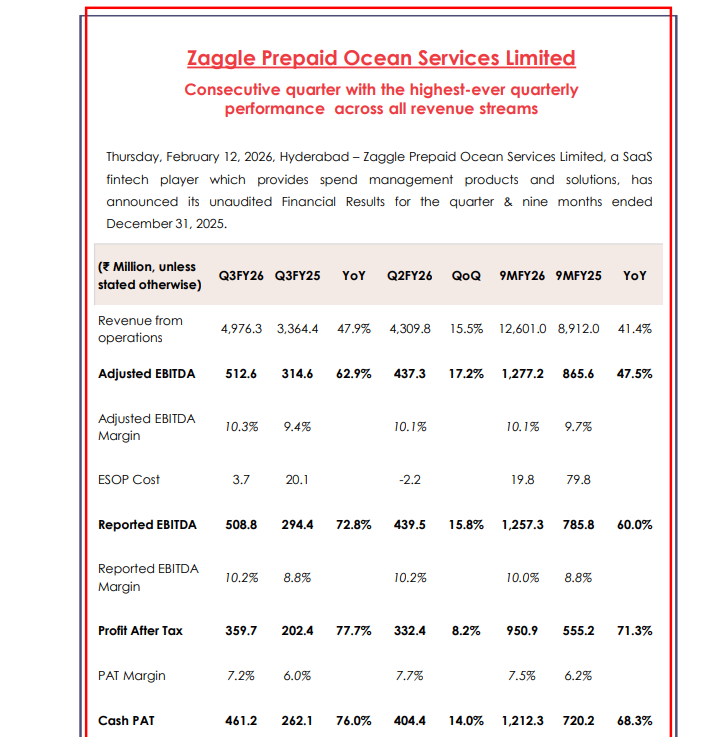

Zaggle Prepaid: All Parameter Bit Performance for Q3FY26

Zaggle delivered highest ever quarterly performance in Q3

Rev: 48%, EBITDA: 73%, PAT: 77%

EBITDA%: 10.2% ( 140 bps YoY), PAT%: 7.2% ( 120 bps YoY)

9MFY26:

Rev: 41.4%, EBITDA: 60%, PAT: 71%

EBITDA% 10% ( 120 bps YoY), PAT%: 7.5% ( 130 bps YoY)

Recall management had revised revenue guidance for FY26 from 35-40% to 40-45% post Q2 results and well on track to achieve that.

More importantly, margin numbers are heartening, because 2nd consecutive quarter when the margins are in the guided range of 10-11%, so finally it is delivering on margin front which was missing piece in zaggle's story for last year.

At 31 PE of FY26 end and growing EPS at >50%, comfortably available at PEG <1

Detailed analysis video post concall tomorrow morning

Stay tuned!

#zaggle #growth #q3fy26 #payment #zaggleprepaid

3

526

Feb 11

Mrs Bectors: Ugly performance

Kaha 20-25% growth karne wale Mrs. Bector ka abhi growth 8% ka aya he.

Margin toh never ever looked going back to 14% mark.

PE abhi bhi 60 ka he. Now it looks more similar to likes of HUL, Dabur jinhone salo se paisa nahi banaya.

Consumption slowdown se bahar nikalte nai dikh raha, or rather forgot its way while it changed it strategy of distribution network expansion.

Whatever could be the reason, result is growth is absolutely invisible.

Inse achha toh fir ye he

1. Manorama

2. Vintage

3. L T Foods

#q3fy26 #mrsbector #fmcg #manorama #vintagecoffee #ltfoods

1

3

305

Feb 9

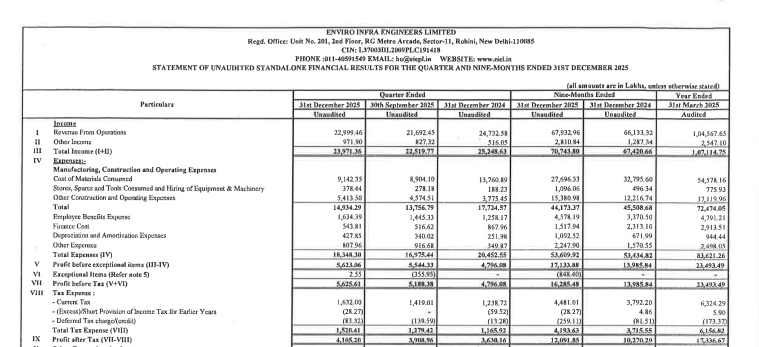

Disappointment: Enviro Infra Q3FY26 Results

Revenues are flat yoy in Q3, on 9M basis revenue growth is in single digit.

The stock went into results with muted expectation, and corrected along with market in last few weeks & months but so far its big underperformance in terms of numbers.

Because, if you recall, management had guided for 35-40% revenue growth at start of FY26 and maintained same guidance post Q2FY26 results, but did mere ~8% growth as of 9MFY26

Now, the revenue recognition can be lumpy given nature of business and order execution but achieving 35-40% revenue growth for FY26 now looks very difficult.

Concall is yet to happen but now if management reduces guidance and if the situation is not alleviated in concall then invites for more trouble

#q3fy26 #enviroinfra #eiel #epc #watertreatment #growth

1

3

2,726

Jan 29

Sky Gold & Diamonds - What does Future Hold?

I am not an expert on Gold & Silver, but I want to talk about a concern that is currently running in my mind that could impact companies in this space - specifically the B2B gold manufacturers

Background – B2B Gold jewellery manufacturer’s growth is primarily driven by volumes and revenue model is cost plus margins.

1. The Current Gold & Silver price rise looks more like a phenomenon that is here to stay, gold may hold onto large part these gains and even can continue to inch up further before it starts to stagnate.

2. Now, people here in India buy gold largely for consumption during festivals or weddings and typically have specific budget in mind to spend for the occasion.

3. With the rise that happened recently, the ability to buy gold quantity has reduced, although value wise it may stay same or slightly increase.

4. Thus, jewellery volume (kgs) consumed by jewellers may decrease resulting in lower demand for manufacturing as inventories would move at slow pace.

5. Now, this situation clouds growth for B2B manufacturers.

6. Smaller jewellers with mediocre design variety may even struggle to survive as customers move to large format stores basically organized jewellers for more options. Unorganized to organized move becomes more prominent.

On the other hand, factors that can work in favour of B2B Jewellery manufacturers are if:

1. Jewellers like Titan, Senco, Kalyan PNG continue to aggressively expand their store network which will drive for gold volume

2. Light weight, inexpensive alternative jewellery demand picks up meaningfully that drive growth for B2B manufacturers

3. Export demand if works out as another growth driver

In all, culmination of all the above points I think still would be negative for B2B manufacturers.

So, commentary of Sky gold post Q3FY26 results will be more important to get cues for the future growth scenario.

I wish and hope I am proved wrong and growth story remains intact but...

What do you think about this space, feel free to comment? #q3fy26 #skygold #b2b #jewellery #b2bmanufacturer #skygolddiamonds

3

1

173

Jan 29

hey @grok can you please validate if sky gold & diamonds charges it clients basis volume of gold or value of gold

1

2

137

Jan 25

Q3FY26 Sterling & Wilson Renewables (SWSolar):

Detailed analysis and concall summary

youtu.be/Mu1cCh9xT2Q

#swsolar #solar #q3fy26 #renewables #sterlingwilson

944

Jan 25

Q3FY26 Cyient DLM

Detailed analysis and concall summary

#cyientdlm #q3fy26 #ems #cyient

youtu.be/M3o_H4bIWFc

527

Jan 25

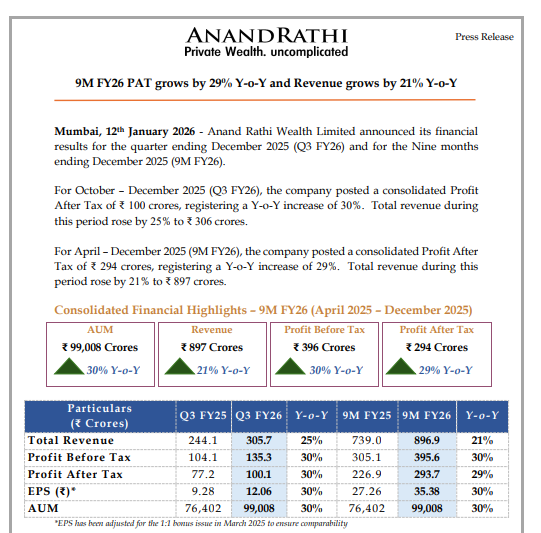

Q3FY26 Anand Rathi Wealth Ltd. (ARWL)

Detailed analysis and concall summary

#anandrathi #wealthmanagement #q3fy26 #growthstocks #arwl

youtu.be/o1buDhYzeyo

268

Jan 25

158