Associate Professor of Finance at @IESEG School of Management. Quant finance, empirical asset pricing, ML, portfolio management. All views are my own.

Joined August 2008

- Tweets 2,014

- Following 929

- Followers 3,059

- Likes 2,200

467 Photos and videos

Pinned Tweet

Feb 26

If you enjoy my threads, I now write longer, structured pieces on empirical asset pricing, systematic trading, and the role of #machinelearning and #AI in finance here → substack.com/@systematically…

1

1

9

1,592

Some adults in the room at last.

Jun 4

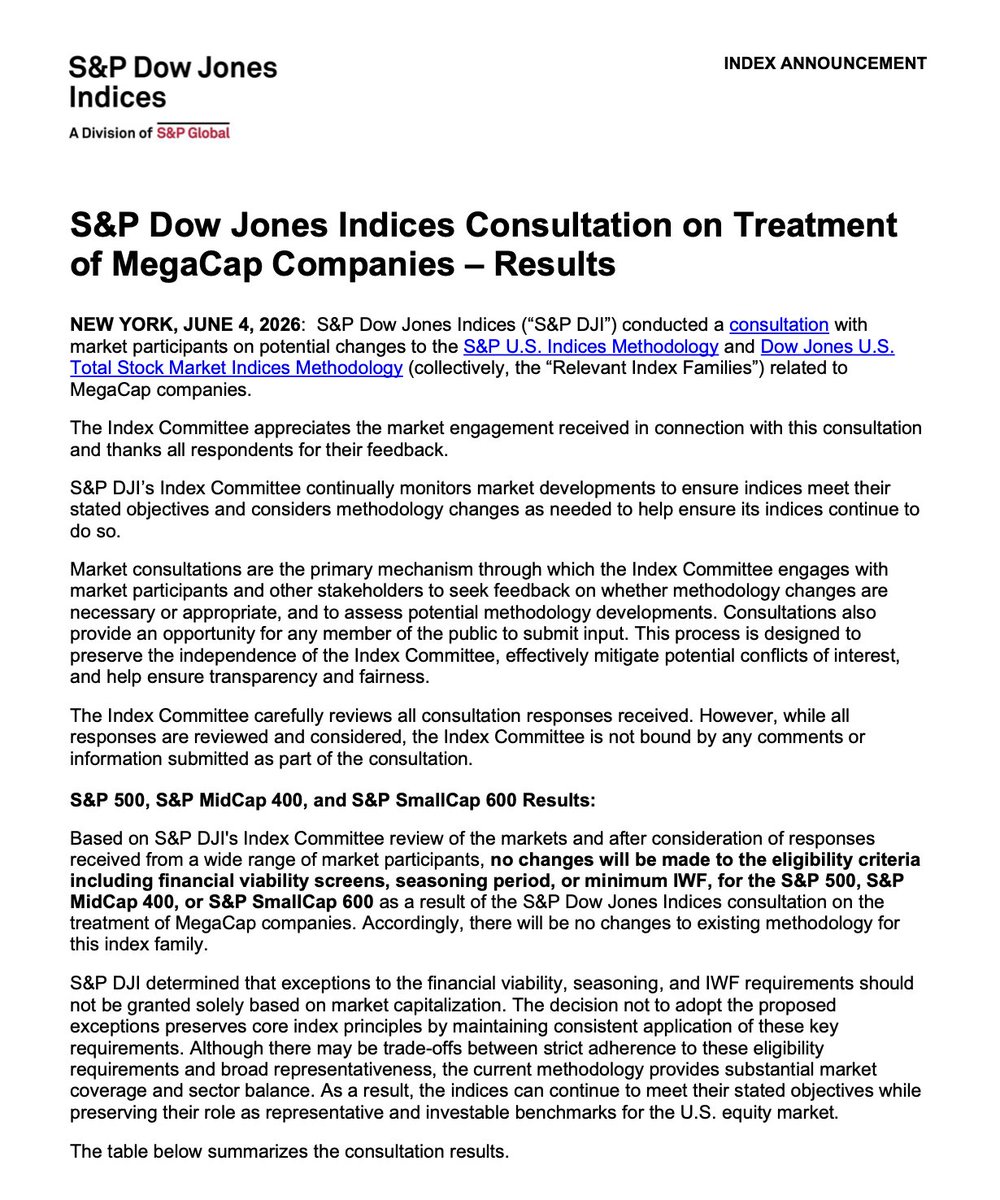

Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

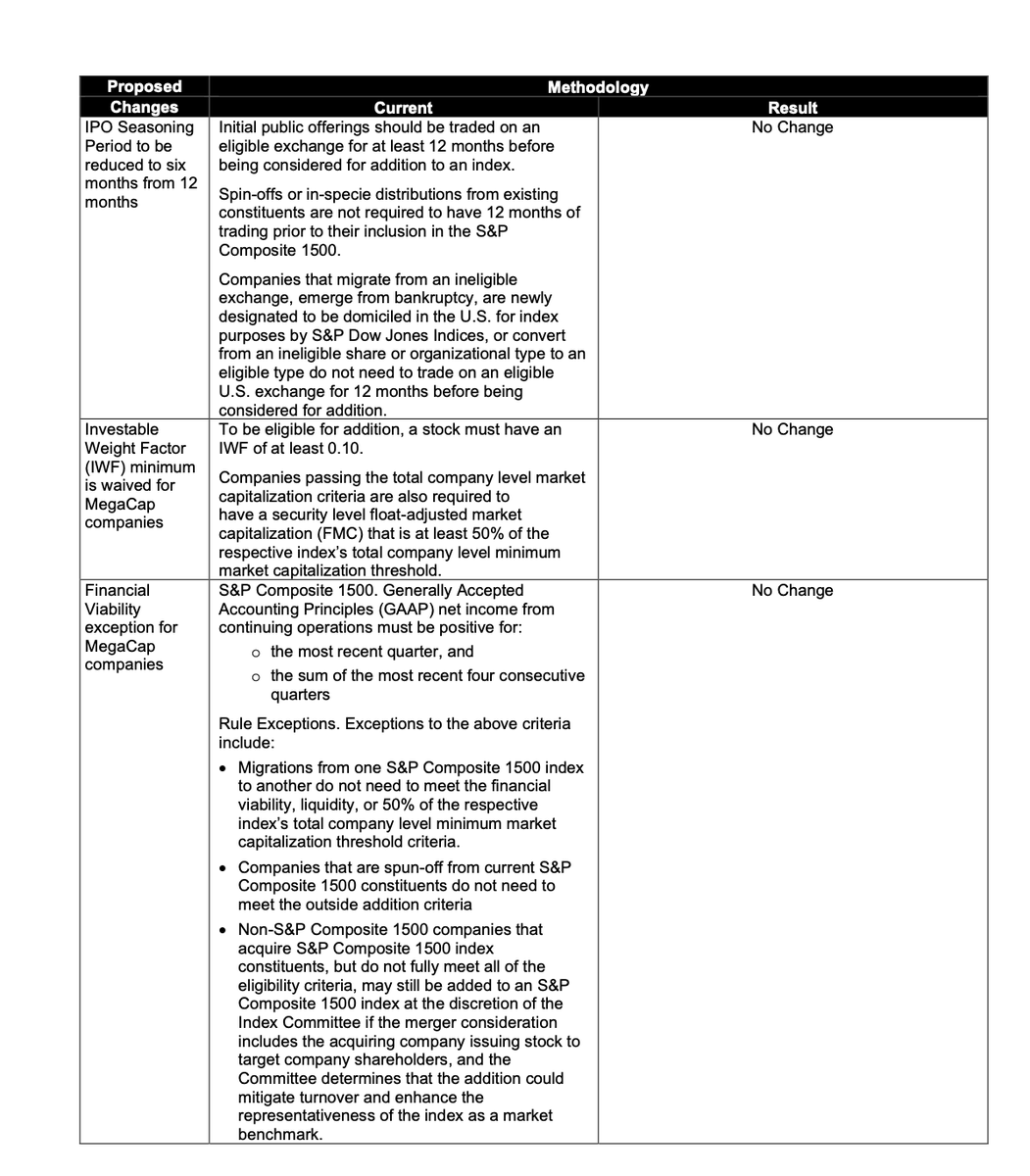

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

1

4

700

Alexandre Rubesam retweeted

Here's my promised explainer. Doing my best to synthesize a lot of info here so check all my info; don't rely on it

So - the SpaceX IPO (SPCX:NASDAQ)

1/ Normally, a company with a massive valuation has to wait months to a year after its IPO before index funds are allowed to buy

Kiss your pensions goodbye, folks

May 20 - SpaceX's (SPCX) S-1 filing

Ludicrous targeted valuation: $1.8T despite $4.28B loss over last year

June 11 - offering price set

June 12 - first day of trading / IPO

July 6 - index funds add the stock

Absolutely unheard-of fast-tracking

39

446

2,394

478,766

May 29

Mean-variance portfolio optimization is taught in Finance courses in every business school. However, it is often criticized - and dismissed - due to it's sensitivity to the inputs, poor out-of-sample performance, and for producing overly concentrated/unstable portfolios.

2

1

14

1,302

May 28

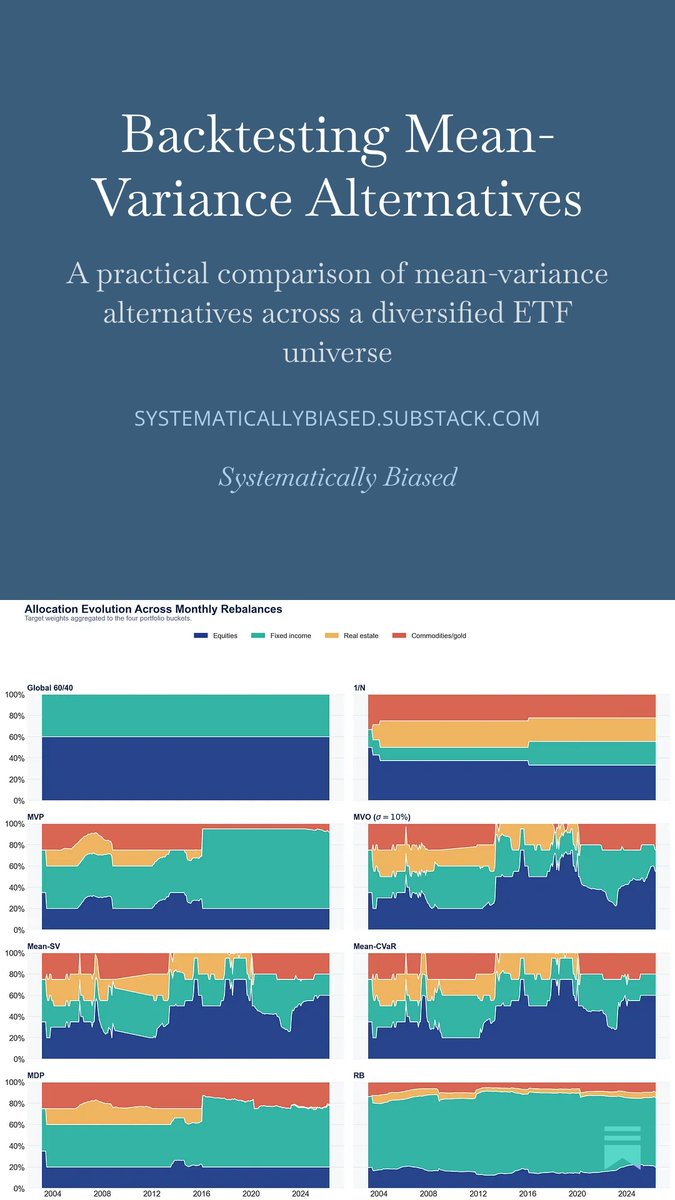

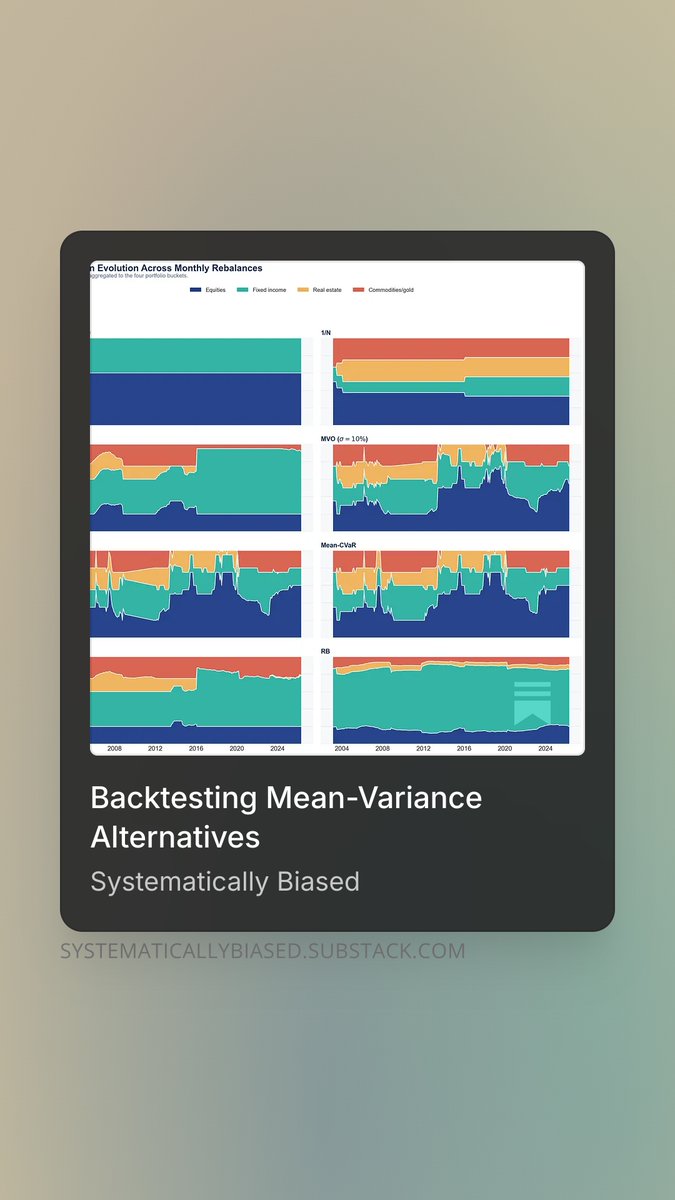

New post: Backtesting alternatives to mean-variance optimization.

1

12

545

May 25

I recently discussed how mean-variance optimization (MVO) can go wrong. In the most recent post, I discuss some alternatives to MVO.

Post here 👇

open.substack.com/pub/system…

#QuantFinance #PortfolioOptimization #AssetAllocation #SystematicInvesting #Investing

2

2

15

797

May 25

12/ The broader lesson:

Alternatives to MVO do not eliminate judgment.

They relocate it.

To the asset universe.

To the risk model.

To the benchmark.

To the tail scenarios.

To the constraints.

To the risk budgets.

1

138

May 25

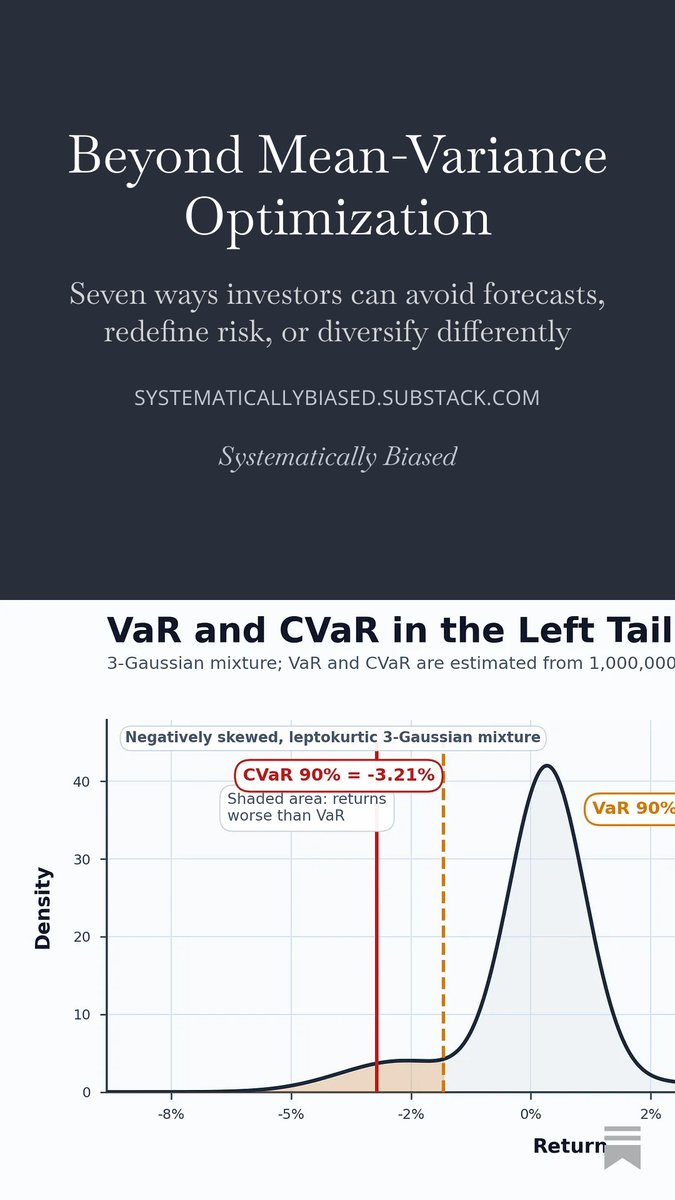

13/ That is the focus of the new post:

Beyond Mean-Variance Optimization

Seven ways investors can avoid forecasts, redefine risk, or diversify differently.

open.substack.com/pub/system…

1

135