Every day is a bonus

Joined February 2018

- Tweets 24,970

- Following 349

- Followers 275

- Likes 15,808

91 Photos and videos

AH retweeted

Jun 2

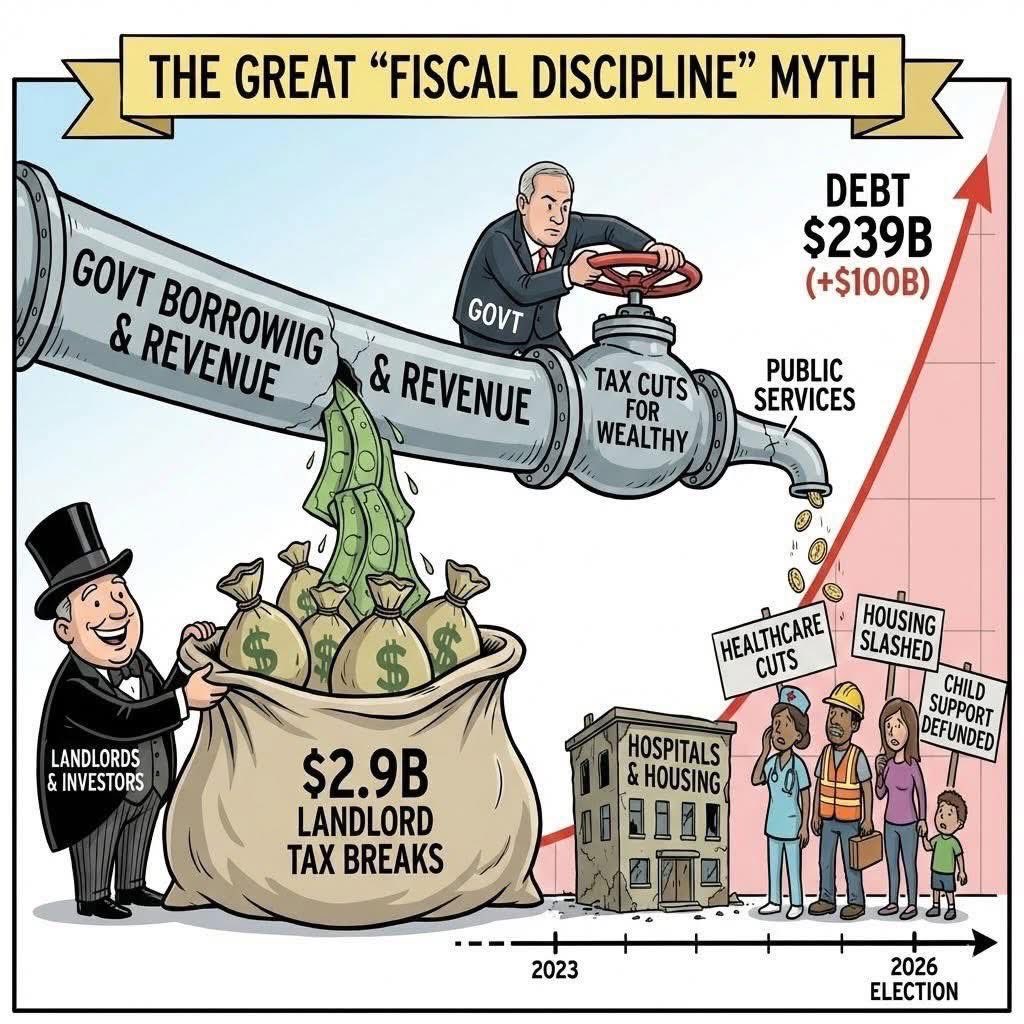

Everything that is wrong about the UK in one image.

Yet deluded unionists seem to revel in the fact they are being had by washed up old grifters, while claiming those on benefits to be the problem.

Talk about The Blind Leading the Blind. 🙄

12

131

134

1,990

AH retweeted

Ireland 🇮🇪

Data centres used 22% of country’s electricity last year (more than all urban homes combined), pushing up household bills. The centres have drained €715m (£620m) from the Irish economy.

86

1,583

2,380

47,372

AH retweeted

in 2000 a FOI act was released from the MOD. The MOD concluded that trident must be based in Scotland. It's reasoning is frightening

In case of an accident it would be more preferable for Scots to die than English people to die.

c dailyrecord.co.uk/news/scott…

18

407

410

7,657

AH retweeted

May 24

Too on point not to share. This is great, but too bad the Orange Felon’s enablers won’t let him see it.

This Australian's reply to #Trump's rant about “NATO not being there for America” is perfect.

"Mate. You run a country with 600,000 homeless people sleeping on the street tonight. A country where 40% of adults can't cover a $400 emergency without borrowing money. A country where insulin costs more than a car payment and people are rationing it to survive. A country where medical debt is the number 1 cause of bankruptcy. A country where women are dying in hospital car parks because doctors are too scared of abortion laws to treat a miscarriage.

You lock up more of your own citizens than any nation on earth. More than China. More than Russia. More than North Korea. The land of the free has 2 million people in cages, and a quarter of them haven't even been convicted of anything. They're just too poor to make bail.

Your life expectancy is going backwards. You're the only developed nation where that's happening. Your infant mortality rate is worse than Cuba's. Your kids do active shooter drills between maths and English while you sell the gunmaker's stock to your mates.

Your minimum wage hasn't moved in 15 years. You've got teachers working 2 jobs and veterans sleeping under bridges and you just spent a trillion dollars flattening a country that didn't attack you.

And you’ve got a convicted felon, adjudicating raping, paedophile protecting, porn star shagging insurrectionist running the biggest dumpster fire war campaign since the Taliban thanked you very much for losing again.

And you're calling Greenland poorly run?

Greenland has universal healthcare. Free education. One of the lowest incarceration rates in the world. Nobody goes bankrupt there because they got sick. Nobody dies in a waiting room because their insurance said no.

'NATO wasn't there when we needed them." When exactly was that, champ? September 11? Because NATO invoked Article 5 for the first and only time in history FOR YOU. Soldiers from dozens of countries deployed, fought, bled, and died in Afghanistan FOR YOU. Australia wasn't even in NATO and we still showed up. For 20 years.

And you pulled out at 2am without telling anyone and left them to deal with the mess.

So maybe before you start calling other countries poorly run, have a look at your own backyard, you spray-tanned aluminium siding salesman. The only thing poorly run in this picture is your f----- mouth."

- Tony Locke

1,110

15,984

34,306

700,915

May 22

Labour now borrowing every month, more than half of what it gives Scotland to run the country for a year

May 22

The UK borrowed another £24.3 billion in April, above the £20.9 billion forecast by the Office for Budget Responsibility.

The ONS said the debt interest bill rose to £10.3 billion last month – the highest on record for April, which marks the start of the new financial year. The government is paying more than £100 billion a year to service its debts. Yet a cacophony of Labour and Green pols think we should borrow even more.

49

AH retweeted

May 16

The team behind Gaza: Doctors Under Attack just won BAFTA… and used the stage to expose what the BBC tried to bury.

“Israel has killed over 47,000 children and women in Gaza. Bombed and targeted every single one of Gaza’s hospitals. Killed over 1,700 Palestinian doctors and healthcare workers. Imprisoned over 400 in what the UN now calls a medicide.”

These are the findings of the investigation the BBC paid for but refused to show.

When they come for the children, then the hospitals, then the doctors who try to save them… it stops being war.

It becomes the erasure of a people’s future.

99

1,984

2,792

26,607

Scotland's free banking era from 1716 to 1844 delivered stable money, financial innovation, and zero bank runs. No government deposit insurance, no lender of last resort, no regulatory capture. Just competition and market discipline doing what they do best.

Three major Scottish banks- the Bank of Scotland, Royal Bank of Scotland, and British Linen Company- competed directly with dozens of smaller institutions. Each bank issued its own notes backed by gold and silver reserves. When you received notes from another bank, you could either accept them at face value (if you trusted that bank) or demand immediate conversion to specie. This created instant accountability. Banks that overissued notes or made bad loans watched their currency get rejected by the public and returned for redemption, draining their reserves fast.

The market developed elegant solutions that would make today's financial engineers weep. Banks formed clearing houses to settle daily note exchanges. They established correspondent relationships across Scotland, creating a payments network more efficient than anything government bureaucrats designed. Interest rates moved freely based on supply and demand for capital, not the whims of committee-driven monetary policy. Scottish banks pioneered overdraft facilities, small-denomination notes, and branch banking while their English counterparts remained trapped by regulations.

The results speak louder than any economic theory. Scotland experienced remarkable economic growth during this period, transforming from one of Europe's poorest regions into an industrial powerhouse. Bank failures were rare and contained; when institutions failed, shareholders lost money, not taxpayers.

Parliament killed this monetary paradise in 1844 with the Bank Charter Act, forcing Scotland into England's central banking straitjacket. The politicians called it "reform" while destroying 128 years of monetary evolution that had actually worked.

61

530

1,506

74,711

May 12

Reform at their finest

May 12

This is what people voted for...fucking hell :D

Bizarre moment Reform Councillor Kieran Lay, Thorne and Moorends Ward, asks Full Council for measures to monitor UFO activity as part of reopening Doncaster Sheffield Airport.

Step 1- Work towards cutting council tax.

Step 2- Set up a panel for UAP sightings.

Couldn't make this up... #doncasterreform #reform

21

AH retweeted

UKGOV, now saying no mandate for indyref. BUT

70

177

310

7,421

AH retweeted

May 11

Bu fotoğraf, 1972 yılında İrlanda’da çekilmiş.

İngiliz ordusuna karşı verilen direnişte, nişanlısı vurulduğunda onun silahını alıp ateş eden genç bir kadını gösteriyor.

Yaralı nişanlısı, bir araba ile

güvenli bir yere götürüldü ve hayatta kaldı.

Ancak bu cesur kadın, sevgilisini koruyup topraklarını savunmak için

İngiliz askerlerine karşı tek başına savaşmaya devam etti

— ta ki öldürülene kadar.

Kadının cansız bedeninin başında duran İngiliz tabur komutanı,

sonunda düşmanlarının bir kadın olduğunu anlayınca askerlerine şu emri verdi:

> “Bedenine dokunmayın.

Bırakın onu İrlanda halkı gömsün.”

Ve ardından,

tarihe geçen şu sözleri söyledi:

> “Biz, sayılarımıza ve silahlarımıza

önem vermeyen bir prensesle savaşıyorduk

O, nişanlısı ve ülkesi için savaştı…

İrlanda için.”

Yıllar sonra, bu fotoğraf Dünya Kadınlar Günü’nün simgelerinden biri haline geldi.

Üzerine,

Che Guevara'nın ölümsüz sözü yazıldı:

> “Güçlü bir kadının yanında olmaktan

asla korkmayın.

Bir gün, o sizin tek ordunuz olabilir.”

Community note

Gönderideki hikâye uydurmadır; nişanlısının vurulması, tek başına savaşması veya İngiliz komutanının sözleri gibi detaylar için hiçbir kanıt yoktur. Fotoğraf 1973'te Colman Doyle tarafından Belfast'ta çekilmiş olup propaganda amacıyla kullanılmıştır. snopes.com/news/2020/04/3… leadstories.com/hoax-alert/202… rte.ie/brainstorm/202…

357

5,095

24,147

1,442,863

AH retweeted

Do you support another referendum on Independence?

please RT for bigger response

86%

Yes

14%

No

511 votes • Final results

63

770

285

13,568

AH retweeted

May 10

ONE WOMAN TRIED TO STOP BRITAIN'S BIGGEST CORPORATE COLLAPSE

Emma Mercer was new to her finance job at Carillion, one of Britain's biggest construction companies. Six weeks in, she found something that should have stopped everything. The numbers in the company accounts were made up. Debts were hidden. Profits were invented. Projects worth hundreds of millions of pounds were lying on paper.

She told her boss. He ignored her. She told the CEO. Same. She went to HR because she had nobody left to tell. A board member later put it in writing. Emma was a whistleblower who did not feel she was listened to.

She was right about every single thing.

So what did the board do? They cancelled the independent investigation and gave the job to KPMG @KPMG instead.

The same company that had been checking Carillion's accounts every year for 19 years and calling them healthy. The same company being paid £29 million by Carillion to do it.

MP Frank Field @frankfieldteam said it out loud in Parliament. KPMG were asked to mark their own homework.

They gave themselves top marks.

Eight months after Emma raised the alarm, Carillion collapsed. January 2018. The biggest company bankruptcy in British history.

Here is what that meant for real people. 3,000 workers lost their jobs overnight. 28,500 people saw their pensions cut. There was a £2.6 billion hole in the pension fund that ordinary workers had paid into for years. Taxpayers spent £150 million just keeping hospitals, schools and prisons running while the mess was cleaned up.

Meanwhile, the former Finance Director Richard Adam sold every share he owned on the exact day the 2016 annual report was published. He walked away with £750,000 in his pocket. The shares were worth nothing a few months later.

The regulator @FRCnews took five years to do anything. When it finally did, KPMG was fined £21 million, the biggest fine ever handed to an auditor in Britain. It also came out that KPMG staff had faked meeting notes and changed spreadsheets to fool the regulator when it came to inspect.

The lead auditor was banned from the profession for 10 years.

The fine was still less than what KPMG was paid by Carillion.

One woman walked into a new job and told the truth in her first six weeks. She was ignored and pushed aside. The executives who ignored her kept their bonuses. The auditors who backed them up kept their fees. The workers who had nothing to do with any of it lost their jobs and their pensions.

Rachel Reeves @RachelReevesMP said it at the time. The board claimed they never saw it coming. Emma Mercer saw it in a month and a half.

This is how British corporate accountability works.

Sources:

BBC News @BBCNews

The Guardian @guardian

Financial Times @FT

Private Eye @PrivateEyeNews

Accountancy Age @AccountancyAge

38

742

1,265

30,501

AH retweeted

🚨 NEW: Panorama investigated Christopher Harborne’s £10m donation to the Brexit Party back in 2020 - now, years later, fresh questions are being raised under strikingly similar circumstances.

The old clip of Nigel Farage hanging up on a BBC interviewer when pressed about Harborne is resurfacing again.

86

2,721

5,351

398,199