Macro-, geo-, realpolitik independent. Harvesting social media for trades. Putting money where my mouth is. Signal>noise = $. @og_velocirapper is my crypto alt.

Joined August 2023

- Tweets 4,190

- Following 38

- Followers 170

- Likes 6,192

933 Photos and videos

Pinned Tweet

Jun 12

In the beginning, there was gold-backed currency. And the Fed looked at it and it was bad, for Triffin’s Dilemma overwhelmingly incentivized profligate spending and Gresham’s Law drained fast the US’ rapidly-dwindling gold reserves.

But Lo! The Fed was mighty and cunning…

1

1

38

Vibe coding is amazing.

I’m running the next build on my laptop during breaks from swinging the sledgehammer.

7

Of course, the MAG7 and IPO crowd have figured this out and so are unloading a wall of stock issuance into the firehouse of support.

Malinventives rarely produce positive outcomes.

When market doomers scare about 50% mean reversion market crashes, I just remember @Tyler_Neville_‘s “markets are a political utility” and @LynAldenContact’s “nothing stops this train.”

Risks remain skewed right tail until @profplum99’s passive bid volmageddon breaks it.

8

Say whatever you want about @elonmusk, but he’s self-made like 80% of America’s most wealthy. 80% of Europe’s rich were born that way.

Why do you think it’s such a hard job to keep people out?

We complain, but people literally kill to get here.

1

68

When market doomers scare about 50% mean reversion market crashes, I just remember @Tyler_Neville_‘s “markets are a political utility” and @LynAldenContact’s “nothing stops this train.”

Risks remain skewed right tail until @profplum99’s passive bid volmageddon breaks it.

1

38

Jun 13

With Tulsi Gabbard's new revelations about US bio labs in many countries around the world including Ukraine, it's fascinating recall the bizarre series of events that gave rise to this controversy in the first place:

In May of 2022, some of us began asking whether the US had bio labs in Ukraine, what they were for, and why the US had them there. For asking those questions, we were instantly branded as "pro-Russian conspiracy theorists" in official Ukrainian intel reports, on our Wikipedia pages, by countless media outlets, etc. This was and remains one of the most bizarre episodes I've ever seen.

Before May 2022, when we asked those questions, barely anyone had ever thought about let alone asked about "bio weapons in Ukraine"! I certainly hadn't. Like most people, I had never mentioned a word about it because it had never occurred to me we had them there.

But then, Marco Rubio summoned Victoria Nuland to the Senate and asked her in a televised hearing under oath about these "rumors," clearly expecting her to immediately debunk them as obvious Kremlin lies and to proclaim the US had no such bio labs in Ukraine.

Instead, Nuland did the opposite! She *confirmed* key aspects of these "rumors," and she explicitly warned that the US has several "bio research labs" in Ukraine that are so dangerous that they must not be allowed to fall into Russia's hands.

When some of us heard Nuland's rather shocking admission -- the first-ever disclosure about these labs -- we of course asked: wait! what? Why does the US have bio labs in Ukraine, and what are the US and Ukraine doing in those labs that make them (in Nuland's eyes) so dangerous?? (Note: nobody ever suggested that the presence of these bio labs in Ukraine justified the Russian invasion; we just wanted answers about these US bio labs that Nuland had casually divulged).

We never got real answers. We got smear campaigns. To this day, our names are formally attached to claims that we spread "conspiracy theories" for asking about these labs even though it was Victoria Nuland herself who was the one who accidentally revealed them for the first time in a Senate hearing in response to a shocked Marco Rubio. They then quickly tried shutting down any questioning by pretending that Nuland never said this, and it was just a bunch of paid Kremlin mouthpieces who were spreading lies.

You see the same tactics now being against Tulsi for releasing this new intelligence report. Watch the Nuland testimony in question:

1

24

Welcome to our timeline. Ridiculous and extreme, yep, but it’s ours.

Jun 13

What timeline are we on man.

There’s a $60 million UFC cage on the White House lawn for the president’s 80th birthday. 125,000 guests. 494 port-a-potties. He compared it to the Eiffel Tower and said maybe they’ll never take it down.

The world’s first trillionaire was minted yesterday. SpaceX IPO. One person now holds more wealth than the GDP of most countries.

The government is negotiating to own a piece of OpenAI. The CEO walked into the White House and pitched it himself. They’re calling it a Public Wealth Fund.

That same government killed OpenAI’s biggest competitor’s models on a Friday night. The reason? A verbal jailbreak claim from an unnamed company. The same jailbreak works on OpenAI’s models. Nobody touched them.

The competitor got blacklisted by the Pentagon four months ago. Their crime? Refusing to let the military use their AI for mass surveillance of American citizens. A judge called it retaliation. The Pentagon did it anyway.

Both AI companies filed to go public in the same two-week window. Both targeting trillion-dollar valuations. One has a government equity deal in progress. The other can’t keep its products online.

The engineers who built the banned models can’t use them anymore. Because of their passports.

And an AI company that spent thousands of hours cooperating with government safety testing got punished harder than any company that didn’t bother.

UFC on the White House lawn. A trillionaire. Government-owned AI. Export controls based on phone calls. Cage fights and trillion-dollar IPOs in the same news cycle.

Watch the film titled Idiocracy. That’s the timeline we’re on.

43

Jun 13

Envy makes the world go round.

Jun 12

Been brushing up on the discourse and I’ve decided that every single person is richer than me is a greedy bastard and every single person poorer than me is a loser. I and only I have the exact right amount of money.

40

Jun 13

“Our latest model is so good the government made it illegal.”

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

1

42

Jun 12

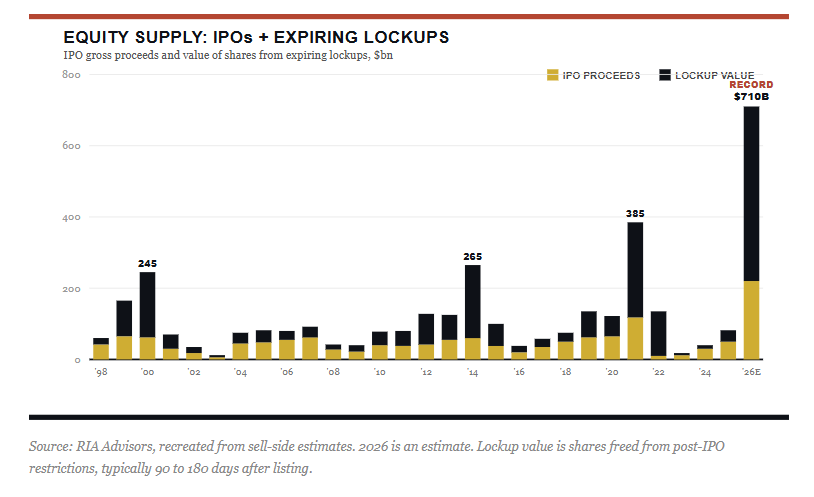

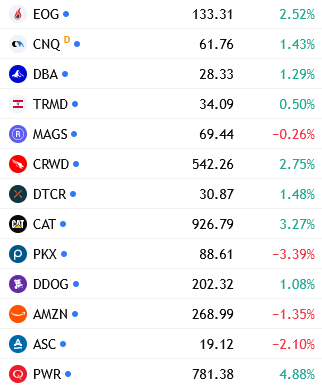

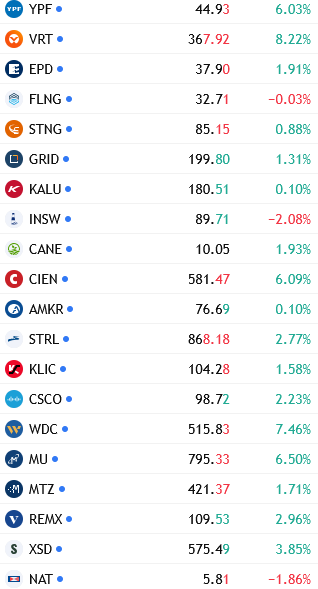

Got in to $SPCX at ~162. Figure it's likely to rally for at least a week before front-running of IPO 15-day lock up sell off.

Tho depends on FOMC next week. They'll hold, but we'll see whether Warsh talks hawkish and tanks markets or talks dovish and bubble rips (I expect dove).

1

103

Jun 12

Fable is notably better than Opus 4.8. Use it as my project manager then it creates prompts for Opus or Sonnet sub-agents depending on how complicated the prompt is.

30

Jun 12

So, roughly how things were before the war? Good thing we did it!

Jun 12

Mehr, an Iranian state media outlet, published what it describes as a 14-point draft memorandum between Iran and the United States. All 14 points as reported:

1. Immediate and permanent ceasefire on all fronts, including Lebanon.

2. U.S. commitment not to interfere in Iran's internal affairs and to respect Iran's sovereignty.

3. Full lifting of the naval blockade within 30 days.

4. U.S. commitment to withdraw its forces from areas surrounding Iran.

5. Reopening of the Strait of Hormuz within 30 days under Iranian arrangements.

6. Suspension of sanctions on Iranian oil, petrochemicals, and related exports, with full access to the resulting revenues.

7. U.S. and its allies to provide reconstruction plans for Iran worth at least $300 billion.

8. A 60-day negotiation period to reach a final agreement on nuclear issues and the complete removal of U.S. primary and secondary sanctions, as well as related UN Security Council and IAEA measures.

9. Iran reaffirms its NPT commitment not to develop nuclear weapons.

10. During negotiations, the U.S. will not deploy additional forces to the region or impose new sanctions.

11. Release of $24 billion in frozen Iranian assets during the 60-day negotiation period, with half made available before talks begin.

12. Establishment of a monitoring mechanism to oversee implementation of the agreement.

13. The final agreement will be endorsed by a UN Security Council resolution

14. Final negotiations will begin only after the release of half of Iran's frozen assets, suspension of oil sanctions, and lifting of the naval blockade.

The final deal would focus solely on uranium enrichment, enriched material, sanctions relief, and Iran's economic reconstruction.

Iran's missile program and support for resistance groups are explicitly excluded from the agenda.

1

46

Jun 12

In the beginning, there was gold-backed currency. And the Fed looked at it and it was bad, for Triffin’s Dilemma overwhelmingly incentivized profligate spending and Gresham’s Law drained fast the US’ rapidly-dwindling gold reserves.

But Lo! The Fed was mighty and cunning…

1

1

38

Jun 12

…and with a word and a promise that could never, ever be kept, the first $100 of true fiat dollars was born, loaned out of pure ether into being in a brilliant burst of transcendent financial alchemy. And for that $100, the only pure-fiat $100 existent, $110 was owed…

1

15

Jun 12

…and many and more of the ills that have transpired since trace back to those fateful moments half-a-century past.

Yet almost no one among our people remembers or understands this root from which our ever-growing Cantillonic slavery is grown.

14

Jun 11

In case you think it’s “serve its citizens’ best interests”, I have some sea-front property in Nebraska to sell you.

Jun 11

The primary goal of every government is to remain in power. All other goals run downstream of that.

2

41

Jun 11

If the US government distributes equity instead of UBI, it would probably increase wealth inequality even faster as the poor would sell it for cash while the government buying added to the passive bidder

Jun 10

The episode is a structured disagreement about whether incoming Fed Chair Kevin Warsh will resist or enable the monetization of US debt. Karsan's central thesis is that the Fed's unspoken mandate is shifting from inflation toward backstopping the Treasury, and that the terminal "elegant solution" to debt, populism, and the equity bubble simultaneously is a sovereign-wealth-fund / Fed mechanism that buys equities outright and hands citizens equity instead of dollars. Booth's counter is that Warsh's documented anti-QE history and the broken transmission mechanism make him the least likely chair to go to the zero bound, and that conventional rate cuts cannot reach the bottom 50% who do not borrow. The unresolved tension is character-and-mandate (Booth) versus incentives-and-structural-pressure (Karsan).

Cross-Cutting Themes

- Monetization is the gravitational endpoint. Every thread -- the debt, the non-bank liquidity bomb, the Paulson balloon, the transmission mechanism, the SWF -- converges on Karsan's claim that direct-to-people money creation (fiscal or Fed) is the only exit, and that it is inflationary by construction.

- Character vs. incentives is the structural axis of the whole debate. Booth repeatedly anchors on Warsh's record and the mandate; Karsan repeatedly reframes to systemic pressure that overrides any individual, including Warsh's potential resignation.

- Distribution, not aggregate policy, drives the inflation. Bifurcation, the bottom-50%-don't-borrow point, the broken transmission mechanism, and the equity-instead-of-UBI proposal all rest on the claim that where money lands determines whether it inflates.

Contrarian or Non-Consensus Views

- Karsan: The Fed will prioritize US debt over inflation as its true (unspoken) mandate, against the consensus dual-mandate framing.

- Karsan: The terminal policy is the state buying equities outright and distributing equity to citizens, against consensus UBI / fiscal-transfer expectations.

- Karsan: Rate cuts and QE operate through effectively the same channel at current rate levels, against Booth and against standard policy distinctions.

- Karsan: The US may prefer the dollar's privilege be used aggressively for printing and buildout, treating reserve status as a license rather than a constraint.

- Booth: Warsh is specifically the chair least likely to reach the zero bound or monetize, against the market's drift and Karsan's inevitability framing.

- Booth: This is not yet the 1970s, against the common stagflation analogy, because aggregate income is falling rather than rising.

84