John 14:27. Husband, dada, founder @PopPayMoney

Joined October 2012

- Tweets 136,755

- Following 6,564

- Followers 8,252

- Likes 274,505

6,842 Photos and videos

Pinned Tweet

New blog post:

Like an alien technology from the future, Zero-point software has arrived

open.substack.com/pub/basche…

31

2

65

7,354

President Donald J Trump retweeted

Jun 13

TRUMP SAYS 'WE LOOK FORWARD TO WORKING WITH IRAN'

5

4

31

6,435

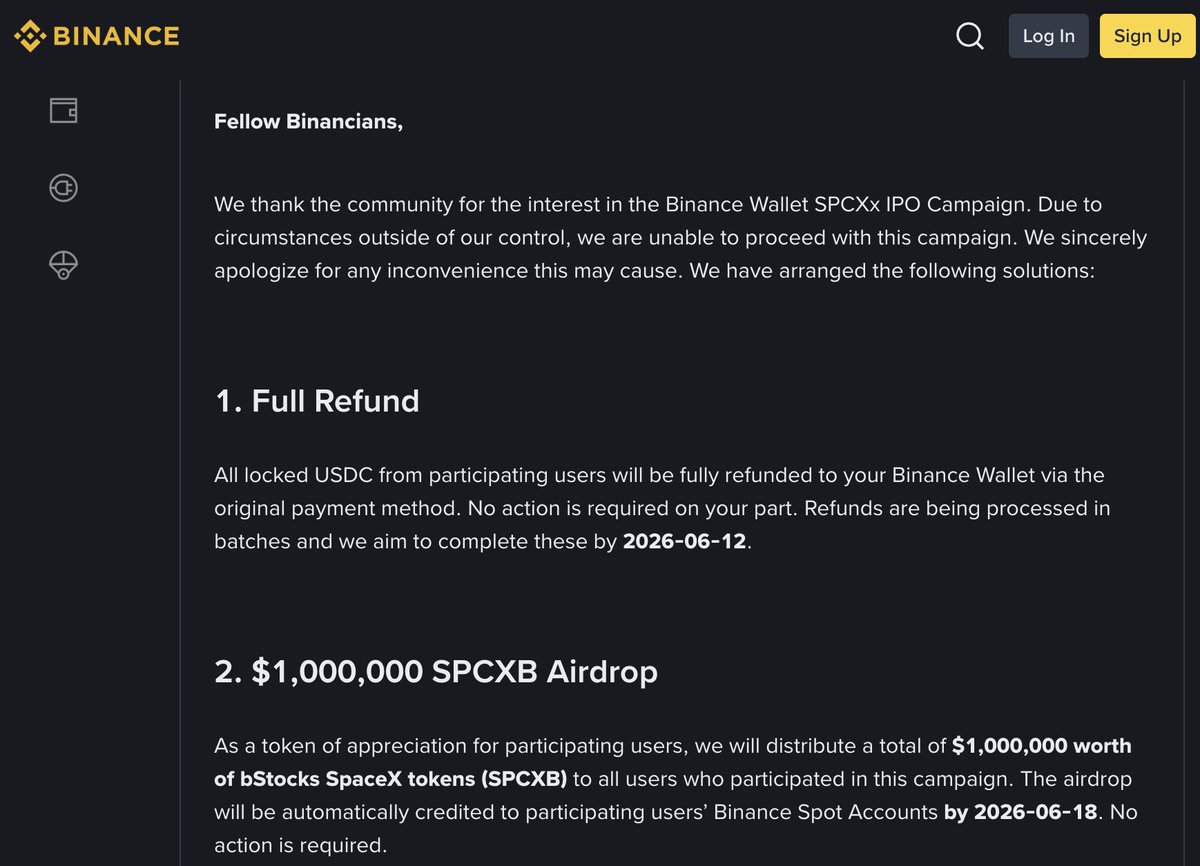

Crypto on its big day to to shine (spacex ipo)

Jun 12

NEW: @binance ANNOUNCES CANCELLATION OF "BINANCE WALLET SPCXX IPO CAMPAIGN"

"DUE TO CIRCUMSTANCES OUTSIDE OF OUR CONTROL, WE ARE UNABLE TO PROCEED WITH THIS CAMPAIGN"

SOURCE: binance.com/en/support/annou…

4

6

615

President Donald J Trump retweeted

*NOTHING EVER HAPPENS - RTRS

1

4

167

President Donald J Trump retweeted

Jun 8

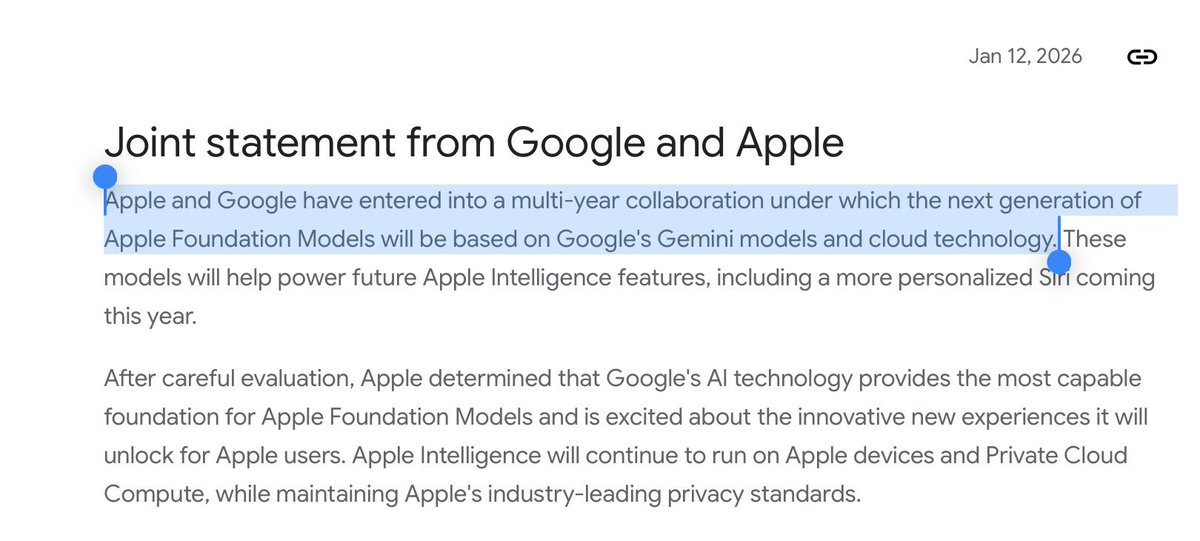

Gemini DOES NOT power Siri

Apple foundational models power Siri

Those models are based on Gemini technology.

It is not Gemini.

Apple and Google have been clear about this since January.

236

308

4,543

354,755

President Donald J Trump retweeted

Jun 8

Getting dangerously close to Trump posting this clip on Truth Social without any caption

Jun 8

Trump scolds Netanyahu in testy phone call: 'You could be left alone against Iran very soon' trib.al/ceoITDL

50

536

8,242

1,052,963

President Donald J Trump retweeted

Jun 8

looks like the hl nodes are moving to a self updating ota system instead of using hl visor

6

2

28

2,934

They’re slowly taking away the second amendment see

388

9,588

142,742

4,460,233

President Donald J Trump retweeted

Jun 6

We give Israel unprecedented access to facets of our government and electoral systems, enabling their overt influence over our foreign policy. Like any competent intel service, they take advantage of that access to further Israel’s agenda, at the expense of Americans.

Our entire relationship with Israel must be redefined—immediately. We need to be clear-eyed going forward and should treat them like a foreign country with different objectives than ours, because they are.

884

5,468

19,673

808,304

President Donald J Trump retweeted

Jun 5

Clavicular in 10 years:

30

220

11,507

160,744

President Donald J Trump retweeted

why does he look like a weeping virgin mary

Clavicular is going to get addicted to plastic surgery and become a grotesque Michael Jacksonesque type

161

817

21,238

1,886,155

President Donald J Trump retweeted

Jun 6

🚨🇮🇱🇺🇸 BOMBSHELL: The Pentagon raised Israel's counterintelligence threat level to "critical," the highest possible designation, over concerns Israel is aggressively spying on top U.S. officials.

According to U.S. officials, the Defense Intelligence Agency issued the assessment in recent weeks because Israel is making "a particular effort to surveil top U.S. officials to get information on the Trump administration's internal deliberations and decision-making" on Iran and Lebanon.

Yep, read that again.

America's "closest ally" is now rated a critical counterintelligence threat, the same tier as hostile foreign powers, because it's spying on the President's inner circle to find out whether he'll resume bombing Iran or sign the deal.

The details are stunning.

U.S. officials already use burner phones and avoid speaking in hotel rooms when visiting Israel.

A CSIS expert calls Israeli intelligence "hyper-aggressive" and "exceedingly interested in what we are up to."

Now stack the timeline.

Trump screams at Netanyahu, "you're f***ing crazy."

The Axios leak that enraged Levin.

Netanyahu's letter designing permanent military integration.

Section 224 linking the two countries' military systems and data.

And now the Pentagon formally designating Israel a critical espionage threat, in the same weeks Congress moves to wire Israel directly into America's defense industrial base.

The two stories are happening simultaneously and almost nobody has connected them.

The Pentagon says Israel is spying on America at a critical level.

Congress is responding by giving Israel deeper access to American military systems than ever before.

At what point does Washington admit this relationship is not what Americans were told it is?

Source: NBC

1,195

6,994

17,807

2,077,948

President Donald J Trump retweeted

Jun 5

i have different interpretation that fits the data in the article. the authors found it takes 2 blocks before hyperliquid fills have price information (~700ms) but hyperliquid provides other price information: the orderbook/best-bid/offer and gossip

if best bid/offer rather than fills is the metric for discovering prices, hyperliquid discovers prices every block

we can fill into (1) arbitragers who are trying to pick off stale quotes and (2) non-arbitragers who are willing to execute against the latest quote

hyperliquid batches transaction into blocks, prioritizes cancels/ALO then emits execution results (fills). whereas lighter adds 300ms to all taker orders and executes trades continuously

on hyperliquid, the arbitrage fill signal would be strongest at the first block, and fall off in later blocks

vs lighter, where any signal from arbitragers picking off stale quotes would be at least 300ms after binance and fills from 0-300ms would be dominated by non-arbitrage (2)

if we filtered out arbitrage transactions, i think we would find hyperliquid non-arbitrage fills do discover prices

and hyperliquid gossip should allow latency sensitive users to discover new prices even before transactions are committed

we could view the arrakis article as a measurement of stale quote arbitrage on hyperliquid

the natural followup question would be, does lighter have less stale quote arbitrage?

it wouldn't surprise me if lighter has less arbitrage because they continuously execute trades which minimizes jitter

the reason for this could be that hyperliquid executes and prioritizes cancels in blocks: even with cancel priority, if the price moves close to block a boundary an arbitrager can still land first, especially with write priority

the counter-factual would be we see a spike of lighter correlation to binance at 300ms which i dont see in the article

5

4

83

13,972

President Donald J Trump retweeted

don't worry, your data is protected by laws

4

10

110

3,504

President Donald J Trump retweeted

Jun 3

77

1,467

13,127

1,637,423

President Donald J Trump retweeted

the fact he may carve out time to attend two basketball games merely weeks after saying he didn’t have time to attend his own son’s wedding is objectively hilarious 😂

Jun 4

Trump says he's going to an NBA Finals game at MSG next Monday, and he might be there for Game 4 too

297

7,117

91,061

2,275,628

President Donald J Trump retweeted

Jun 5

Fiat is a sham, the banking class is corrupt, decentralized digital currency and the blockchain are the inevitable future, and the incumbents will fight it to the death.

291

276

2,841

702,187

Lmao at all of the conservative hacks on here losing their shit when Bernie suggested this last week and obviously Sama is gonna try to get a federal backstop in this way

Welcome to maga communism

Jun 5

🚨🚨🚨Trump has now confirmed the story I broke yesterday, says he wants “pieces” of AI companies given to US government — “we are looking into that”

4

2

345