building @damper_vc | prev: Cliza

Joined April 2010

- Tweets 15,369

- Following 2,925

- Followers 12,353

- Likes 37,114

1,461 Photos and videos

Some thoughts on crypto market-structure and where we go from here.

1. Crypto produces six times more in terms of revenue, for each venture dollar deployed this year, compared to '22. The problem is, that revenue is concentrated in a handful of players. Which is why venture in crypto has struggled.

It used to be a consensus, early stage market. Now the players making money are the ones deploying into power law players in the late stage.

2. If you remove stablecoin issuance (can't back it now), hyperliquid (doesnt need VC), polymarket (gambling??) - the investible opportunity subset are quite few.

If you take L2s , you have a situation where transaction throughput and valuation have no correlation. There are protocols with 10k tps, trading at sub 100mil mcap, because nobody uses them.

3. The market - at this point, splits into networks, protocols and platforms. I see Privy (yes the wallet guys) as a network. I see Tradexyz as a platform. And I see solana/ethereum as a protocol.

Semantics aside, here's what I mean. Privy wins with each marginal application that embeds it. They are network agnostic. They actually own the user with more stickiness than any protocol. At some point, Privy became the standard - like Google single sign on pages did.

Tradexyz is a platform, because it is the default layer built atop Hyperliquid for trading interface. They can upsell other products there. They can integrate other markets if they choose to. Currently that can look like RFQs/ block-trades and enabling cross-market arbitrage with tradfi avenues. It is a platform, because it has the optionality to do it and therefore has the highest LTV per user.

Solana and Ethereum are in this situation where they are likely to scale TPS, but the case for network fee rising is not strong. The next marginal user in the web, cares about fee going from $1 to $5 and no they are not coming for meme coins. For networks to have value, the applications built atop it need to be sticky. Right now the only place a developer rushes to is Hyperliquid given liquidity moats. It may change, but Solana was there 18-24 months back.

Protocols in crypto have a single product and that is liquidity. All else, is hogwash. You can't simultaneously hold the truth that crypto is about capital markets and not acknowledge that liquidity is the product.

4. There are new money networks that are valuable. Chainlink, LayerZero, Ondo - come to mind. These interact with traditional layers and are protocol independent. These businesses grow regardless of which protocol is evolving.

The mental model I've been using is that of Visa/Swift. Neither of those networks are token governed. Neither of them are open or customisable to the needs of a developer.

Yes, all these products are vulnerable to hacks, but I think as we see a new class of tokenised assets moving hands more often, mostly owing to agents - these networks will be crucial infrastructure. They grow more powerful with each protocol they embed into so you may see a world where a developer is no longer thinking of deploying on Solana or Base, but simply using these money networks. That is interesting.

5. I think, when an ecosystem trends to concentrating in late stage players there are two things that happen. One is the cost of media goes exponentially higher because anyone surviving has incentives to go where the money is. That makes it harder for smaller players to reach end-users. I see this on the daily now.

The second, is the capital that used to go from VC -> startup -> employee , often used to be the first entrant to new capital primitives. If there is employment displacement (which has happened) in crypto, we will see newer capital primitives struggling to find users.

So you have this situation where culture is defined by late-stage corpo-bros, and startups struggle to find early users. Which is equal parts an opportunity and crisis.

6. I say opportunity, because this is where I expect the bulk of future VC returns and wealth generation to happen. Crypto has reached a point of maturity where talking about the underlying protocol, extent of decentralisation, wallet security and all that nonsense is actually going to make you look stupid. The end user doesnt care. They care about what the product does.

The users within crypto don't care either. Which means, founders are incentivised to expand TAM and position products without the techno jargon and look at what makes money harder. Earlier you could be ethereum or solana or hyperliquid aligned and have a shot at survival. The market has wisened up and nobody cares. That is equal parts scary and an opportunity.

This is also where founders that have zero experience in crypto or the ability to forget all they studied the past few years will win. Fwiw - go study lightspark or altitudes' comms. They do this quite well.

7. In the past three months, we've seen clear dispersion of a few players from Bitcoin. Hyperliquid. Near. VVV. I will also go ahead and presume Virtuals may see a similar fit in the next few months.

My understanding is that crypto money rails are valuable, but to build it is not a function of issuing tokens, faking community with bots and talking techno jargon. You need these thigns to work. You need them to be useful. Most founders get lost in the first half and forget the end user. Tokens will continue to be valuable, so long as founders can communicate what it does, back it with action and commit to it explicitly.

8. I remain long crypto. I am also long crypto venture. The idea that tokens are down does not discount the opportunity subsets that exist in the long-tail of financial applications that are yet to be built. I think being bearish is an extension of a lack of imagination. And while you can run an incredible hedge fund book running things by the facts, venture has always been a dreamer's playground. Maybe i choose to dream. maybe that's stupid - or maybe its just gut instincts from seeing this story play out a few times in past cycle.

14

10

126

8,501

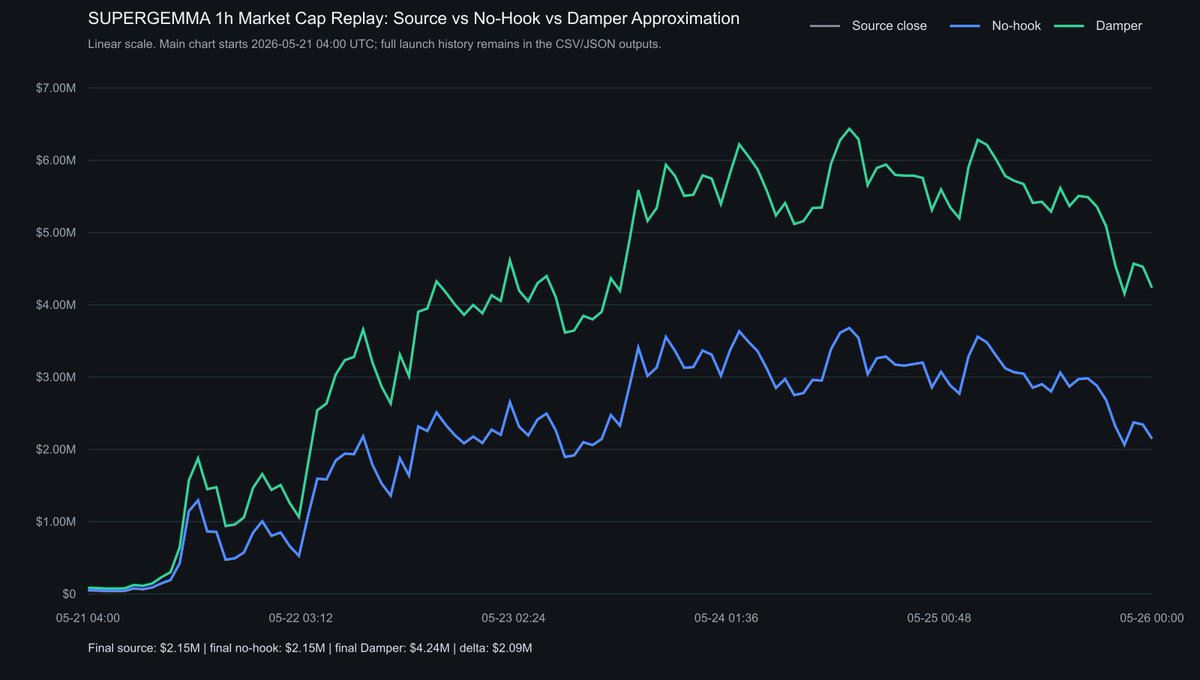

Damper will change this

How? Will start to reveal this week

$SURPLUS is a case study in how founder ambiguity can turn a “community token” into startup runway.

the setup was simple: $SURPLUS launched on bankr, and @mac_eth was the fee receiver from day one.

every trade created volume, every trade paid fees, and those fees accrued to a wallet connected to the founder side of the story.

that matters because the entire market was trading one question: will mac accept this token or not?

early on, the answer looked like no.

he publicly distanced himself from existing community tokens, saying he was “not really planning to endorse one of those” and wanted different mechanics, including a DIEM pair.

then the answer started to move.

as the token ran, the framing changed from “not planning to endorse” to “i’ll acknowledge the token in a bit.” later, the community had “coalesced around the existing token.” then fee revenue was being discussed as something that could potentially pay for community/token management.

then the framing softened again.

SURPLUS became “just a community launched bankr token.” there was opportunity to build on top of it, but “nothing exists right now.” later, the line was: no allocations, just a bankr community token.

read that sequence carefully:

• not planning to endorse

• will acknowledge

• community coalesced around it

• maybe use fee revenue

• just a community token

• nothing exists right now

• no allocations

that is not clear founder communication. that is a moving target.

and every time the target moved, the chart repriced.

SURPLUS went from around ~$65k mcap near the early “not endorsing” stage to roughly ~$10m near the highs.

that move was not driven by clean token utility or product revenue. it was driven by founder proximity, market speculation and the question of whether this would become the accepted Surplus token.

that is where the incentive conflict starts.

the same person whose words moved the market was also the fee receiver on the volume created by those words. whether intentional or not, that is a dirty setup.

there was another thing that felt strange early on. before mac had fully acknowledged the token, i noticed he followed me even though we had never interacted before.

maybe that means nothing. but when you look at his account, he follows 3,000 people, including a lot of base influencers, trenchers and attention nodes.

why does that matter?

because if your token narrative depends on mindshare, then surrounding yourself with the exact people who can move that mindshare is not random.

it looks like pre-positioning: build visibility, get closer to the base attention graph, keep the token unofficial enough for deniability, but visible enough for speculation.

maybe it was just networking. maybe it was not. but in the context of everything that followed, it fits the same pattern: move attention first, keep the answer unclear, then let the market trade the uncertainty.

ambiguous founder signals create speculation. speculation creates volume. volume creates fees. fees become runway.

then the chart collapsed.

after the token was already down heavily from the highs, mac posted an AMA. he said the product had $0 revenue, trading fees were the only way to afford a team, total fees were a little over 6% of supply, and he sold around 2% to get 2-3 months of runway.

that post said the quiet part out loud.

the product was not funding the token. the token was funding the product.

holders were the runway.

and the worst part was not even the first sale. it was the overhang after it. he said he planned to hold the rest unless he needed more to pay the team.

that means every future pump now has a permanent question attached to it: is this a real recovery, or just more liquidity for the next runway sale?

that is why this looked so bad. not because teams never need money. not because founders should build for free. the issue is that the funding source came from a market that had been pushed around by weeks of unclear founder signals.

the clean version would have been easy:

• this is the accepted community token

• i am the fee receiver

• fees may be sold for development

• product revenue is currently zero

• buying this means funding the team through trading volume

• expect sell pressure if more runway is needed

that would be honest. risky, but honest.

instead, the market got ambiguity first and disclosure later.

first, the token was not really endorsed. then it would be acknowledged. then the community had coalesced around it. then it was just a community bankr token. then nothing existed yet. then fees were sold for runway.

that is founder optionality.

when accountability is risky, it is just a community token. when traction is useful, it gets acknowledged. when fees accumulate, it becomes runway. when holders complain, the answer is that the alternative is zero months of funding.

you cannot have it all ways.

either the token is meaningful enough to fund the team, or it is not meaningful enough for holders to expect accountability. picking whichever framing is useful in the moment is the entire problem.

and this is where the “poor comms” excuse becomes too generous.

in a normal startup, bad communication is annoying. in a founder-adjacent bankr token, bad communication is a market mechanism. it moves price, creates volume, generates fees and funds the team.

so even if you give mac the benefit of the doubt, the outcome is still ugly: unclear signals pumped attention into the token, the fee receiver benefited from the trading activity, holders ate the drawdown, and the project walked away with runway.

the less charitable read is worse.

this looked like a volatility farming loop: keep the market guessing, let the chart run, collect fees on the volume, sell part of the stack after the hype, then leave open the possibility of selling more later.

and honestly, i would not be surprised if the next move is a burn, buyback, fee redistribution, new utility announcement or some “community alignment” patch.

not because that would fix the core problem, but because it could restart activity in the book after they had a chance to buy the bottom.

create remorse, show “alignment,” make trenchers feel like the founder learned his lesson, and hope everyone forgets the sequence that came before.

that kind of redemption arc is also a volume event.

and in this setup, volume is never neutral. volume creates fees.

the point is not that SURPLUS is fake or that the product can never work. maybe the team ships. maybe the product eventually starts generating revenue. maybe the money is spent well.

but none of that fixes the core issue: holders were pulled into a market where the founder’s framing kept changing, while the founder side collected fees from the volatility that framing created.

that is not clean fundraising.

that is not community alignment.

it is emotional whiplash engineered around maximum extraction: pull the chair back when accountability is risky, push it closer when traction is useful, let the crowd trade the uncertainty, then harvest the volume.

2

3

9

1,578

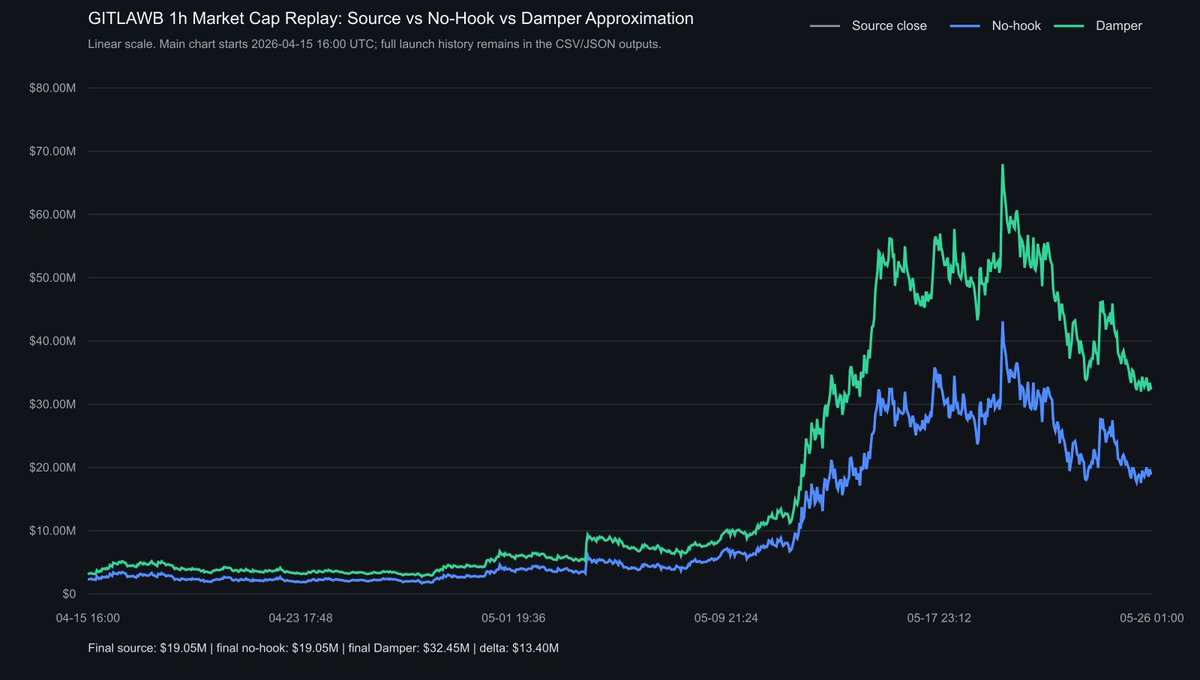

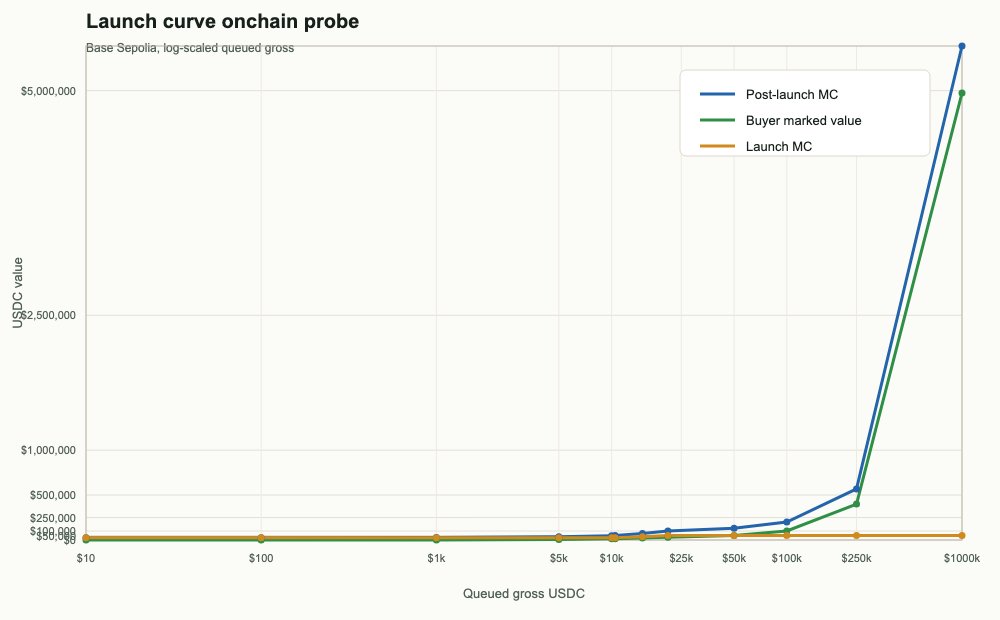

if GITLAWB launched on Damper, the market cap would be $13.40M now and ATH would have been $68.17M

psychological factors not included and real results could be higher

additionally the project would have secured $1.74M worth of extra value at the current price in an OTC desk contract

1

2

9

947

basedfk retweeted

May 21

Given today’s news, reupping this offer to a few more mathematicians!

May 19

ChatGPT Pro seems to be the best of the big models for math research, but many mathematicians haven't tried it

If you are a working mathematician interested in testing out Pro for math research, I'll gift you a month of it

Reply if interested! (I'll probably cap at ~10)

17

2

83

15,365