Research on Stocks & Investing 📈 Investing Newsletter

Joined January 2020

- Tweets 22,752

- Following 105

- Followers 92,292

- Likes 69,846

3,741 Photos and videos

Pinned Tweet

6 Jul 2025

7 charts that will teach you more about investing than school did:

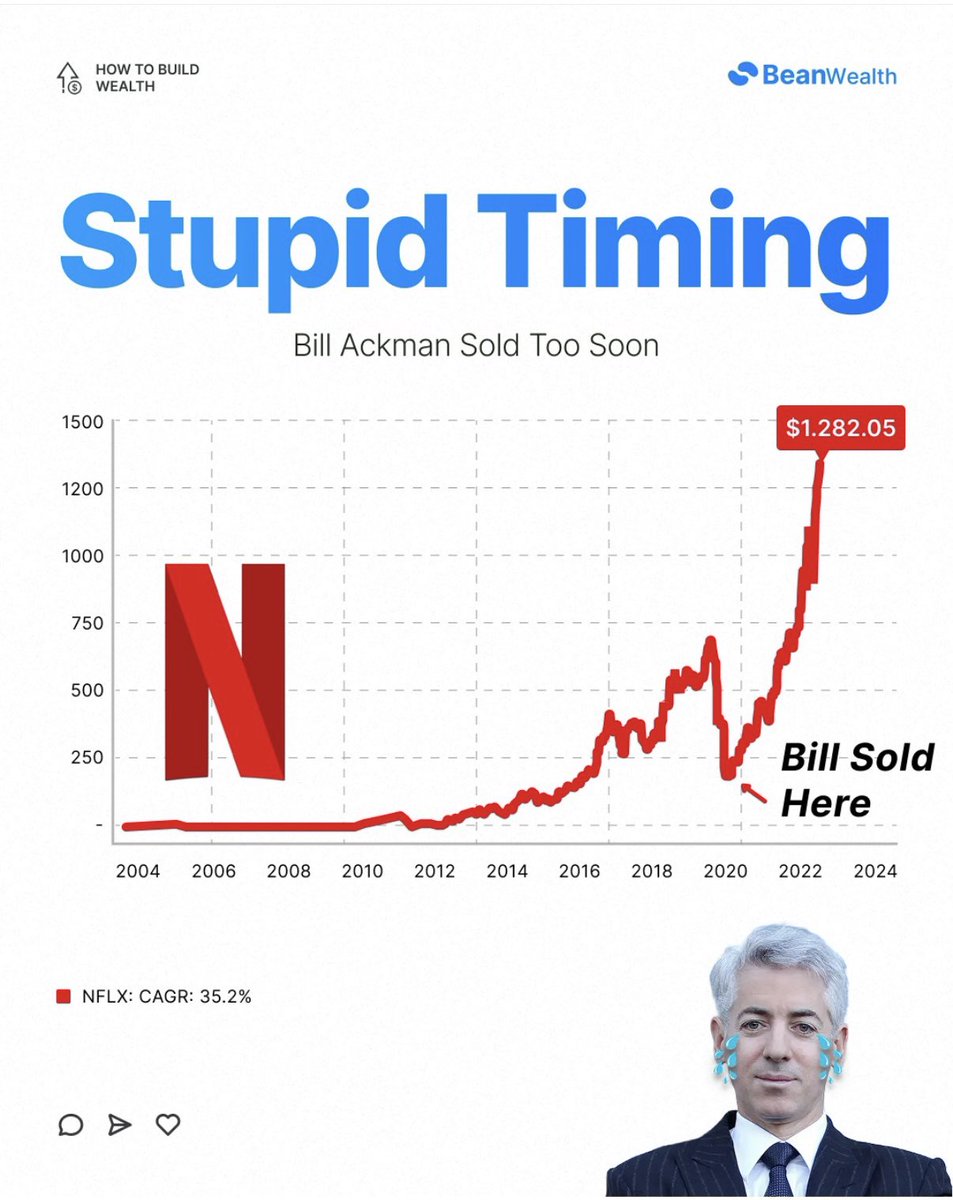

1. Bill Ackman sold the bottom

10

26

80

29,665

$VWAV VisionWave is building around AI-driven defense, RF sensing, and autonomous security systems.

Recent financing, acquisitions, and partnerships continue expanding the platform.

Communicated Disclaimer: tinyurl.com/2ezu68r4

1

1

472

BeanWealth Research retweeted

Jun 9

Most investors still see $MARA Marathon as a Bitcoin miner

The company now has a 2.2 GW power pipeline and exposure to the sovereign AI infrastructure market via Exaion

Power and AI sovereignty are becoming 2 of the most valuable assets in the world

Must watch for investors:

8

15

38

6,539

BeanWealth Research retweeted

Jun 8

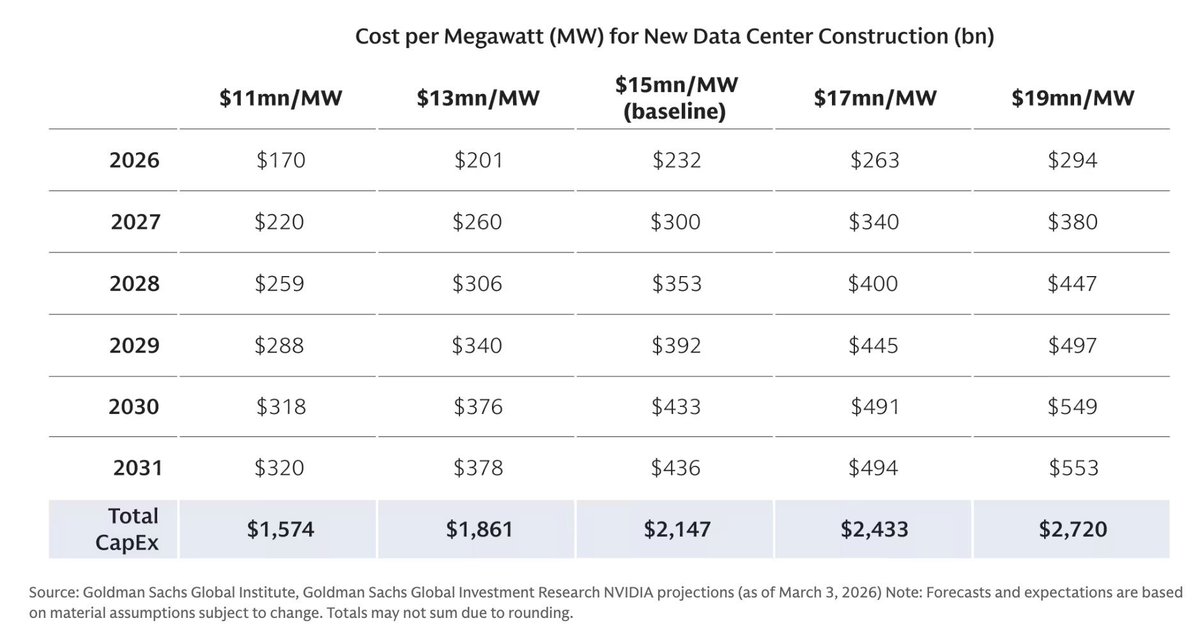

Goldman Sachs projects $7.6 trillion of AI infrastructure capex through 2031

Every new generation of AI infrastructure requires more compute, more power, and more capital than the last

The opportunity for $CRWV $NBIS $MARA and $IREN is still widely underestimated

13

12

46

10,847

BeanWealth Research retweeted

Jun 8

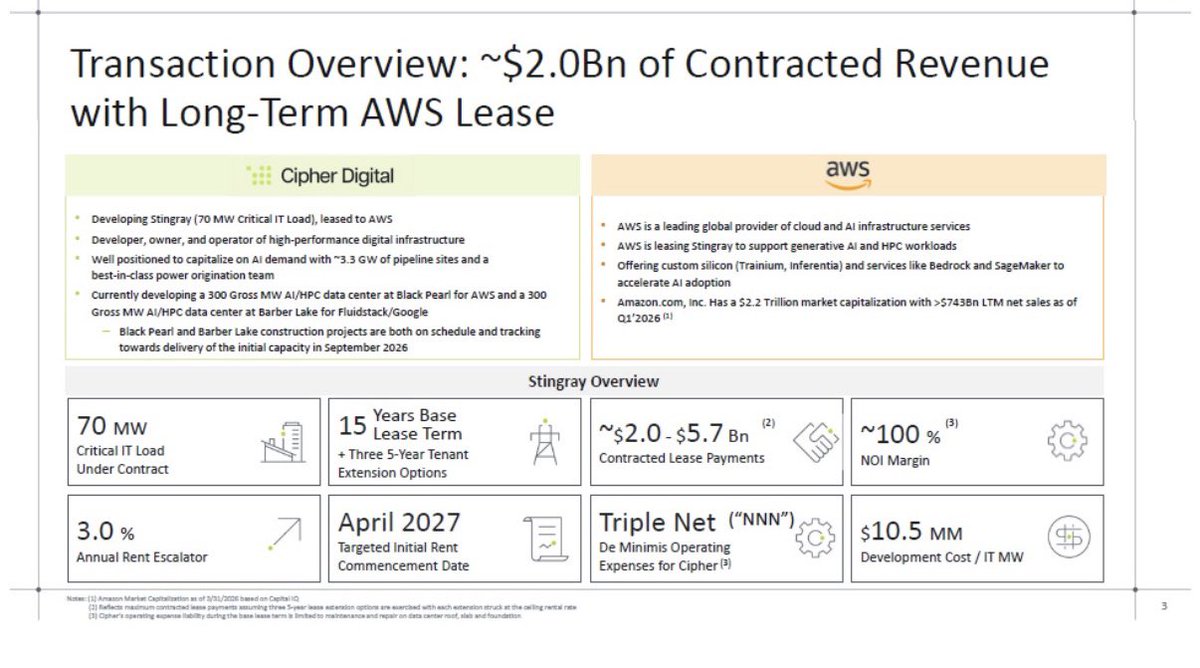

$CIFR Cipher revealed $AMZN AWS as the tenant behind its Stingray data center project

The deal includes a 15-year triple-net lease, nearly 100% NOI margins, and $2 billion in contracted payments

These are some of the strongest AI data center economics we’ve seen disclosed

4

7

44

48,920

BeanWealth Research retweeted

Jun 8

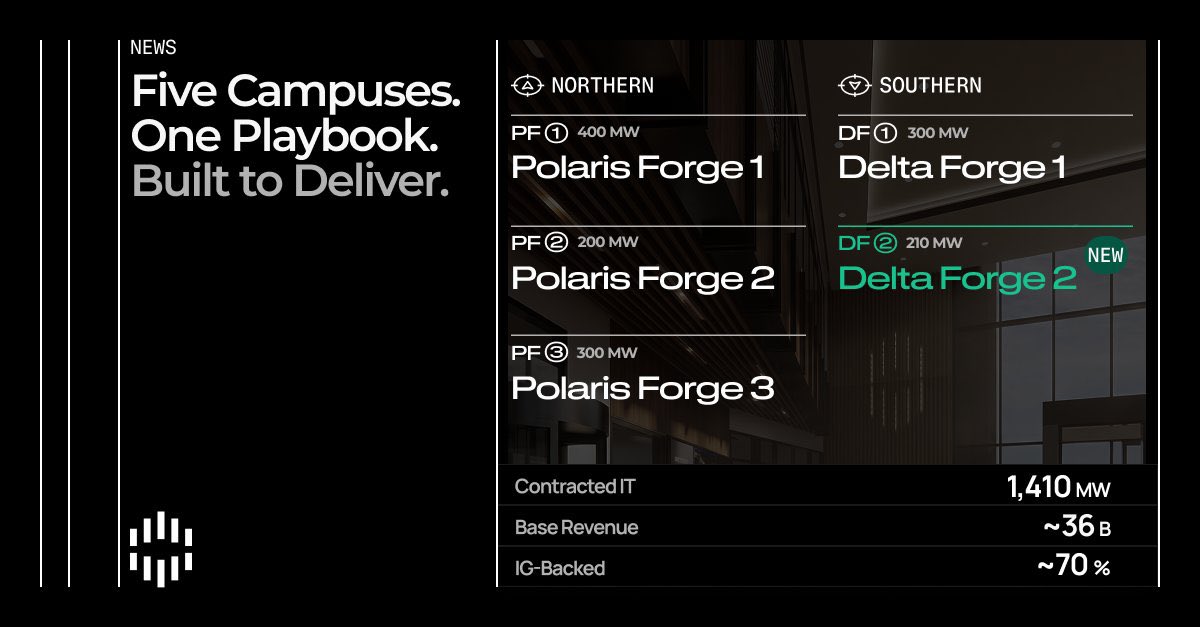

$APLD Applied Digital just signed a 210 MW lease for Delta Forge 2

The company now has 1.4 GW of leased capacity, ~$36 billion of contracted revenue, and ~$86 billion including renewal options

The AI infrastructure buildout is extraordinary:

3

2

9

3,151

BeanWealth Research retweeted

Jun 1

The AI neocloud category is one of the most misunderstood sectors of the AI infrastructure trade:

1. $MARA Mara (AI Sovereignty)

American hyperscalers have a legal problem serving foreign governments. The CLOUD Act means data stored on AWS or Azure is potentially accessible to the U.S. government and foreign nations are not okay with that. MARA acquired a 64% stake in Exaion, a subsidiary of French state-owned energy giant EDF, specifically to serve governments and enterprises that need AI infrastructure their own governments actually control. That is a customer base $AMZN AWS cannot legally compete for. And once its Long Ridge acquisition closes later this year, MARA’s operational and development footprint reaches roughly 2.2 GW. This is no longer a Bitcoin miner but an AI play hiding in plain sight.

2. $NVT nVent (The Vera Rubin Buildout)

nVent is not a neocloud but you cannot build one without it. The entire Vera Rubin generation is defined by one design choice: $NVDA NVIDIA made the NVL72 racks 100% liquid cooled. That single decision turns nVent into a direct beneficiary of every Rubin rack deployed, because each one needs exactly what nVent makes: liquid cooling hardware and rack level power protection. As Rubin ramps through the second half of 2026, that demand flows straight into nVent’s order book, which hit a record $2.6 billion last quarter. It compounds quietly at 20% operating margins while the rest of the market chases the headline names.

3. $CRWV CoreWeave (The Essential Cloud)

When companies build and deploy AI models they need somewhere to run them. CoreWeave is becoming the place the best ones go. Vera Rubin is NVIDIA’s next generation chip delivering roughly five times the inference performance of what exists today and CoreWeave is among the very first to deploy it at scale. That early access is how you end up with nearly $100 billion in contracted backlog from $META Meta, Anthropic and Mistral. They are not signing decade long commitments to a GPU rental company. They are betting on the infrastructure layer the AI economy runs on.

4. $IREN IREN (Energy-to-Compute)

The thing most people miss about AI infrastructure is that GPUs are not the bottleneck. Power is. You can order chips today and wait years for the electricity to run them. IREN has secured 4.5 GW of power globally and needs only a fraction to hit near term targets. Microsoft is already a customer. NVIDIA signed a landmark partnership. And the Mirantis acquisition brought in hundreds of engineers with a decade of enterprise cloud experience across over a thousand customers. The runway here is genuinely difficult to overstate.

28

17

85

62,928

BeanWealth Research retweeted

🔦 Speaker spotlight: @investmattallen, Founder & CEO of @bean_wealth, joins the EIF 2026 speaker lineup.

Matt leads a financial media and investment research platform reaching millions of investors across newsletters, podcasts, YouTube channels and digital media brands.

Through BeanResearch, his team focuses on technology, AI infrastructure and geopolitical investing themes shaping global markets.

As energy demand, AI infrastructure and capital markets converge, retail investors need better ways to understand the opportunity.

That is why this conversation belongs at EIF.

📍Dallas | July 23, 2026

🎟 Use code EIF20 for 20% off tickets

🔗EIF2026.com

#EnergyInvesting #AIInfrastructure #RetailInvestors #CapitalMarkets #EIF2026 #AI #NASDAQ #DataCenter #BitcoinMining #Infrastructure #Energy

2

2

6

3,091

$SUGP SU Group Holdings operates in a niche that doesn’t get talked about enough.

The company provides security engineering, electronic security systems, and screening solutions used across transportation hubs

Disclaimer: tinyurl.com/yvs9h3b8

1

696

BeanWealth Research retweeted

Jun 1

$ONCY Oncolytics Biotech is focused on helping the immune system recognize and attack cancer more effectively.

Its lead therapy, pelareorep, is being studied across multiple cancers including colorectal, pancreatic, and anal cancer, with a strong focus on combining it with existing immunotherapy treatments.

The company recently brought in a new CEO who previously led Ambrx through its ~$2B acquisition by Johnson & Johnson, while upcoming clinical updates and regulatory discussions remain key catalysts.

Disclaimer: tinyurl.com/26m3x87w

3

1

4

1,703

$ONCY Oncolytics Biotech continues to build around pelareorep, its lead cancer therapy candidate.

For investors, the story is increasingly centered around clinical progress and moving toward later-stage development.

Disclaimer: tinyurl.com/26m3x87w

645

BeanWealth Research retweeted

Jun 1

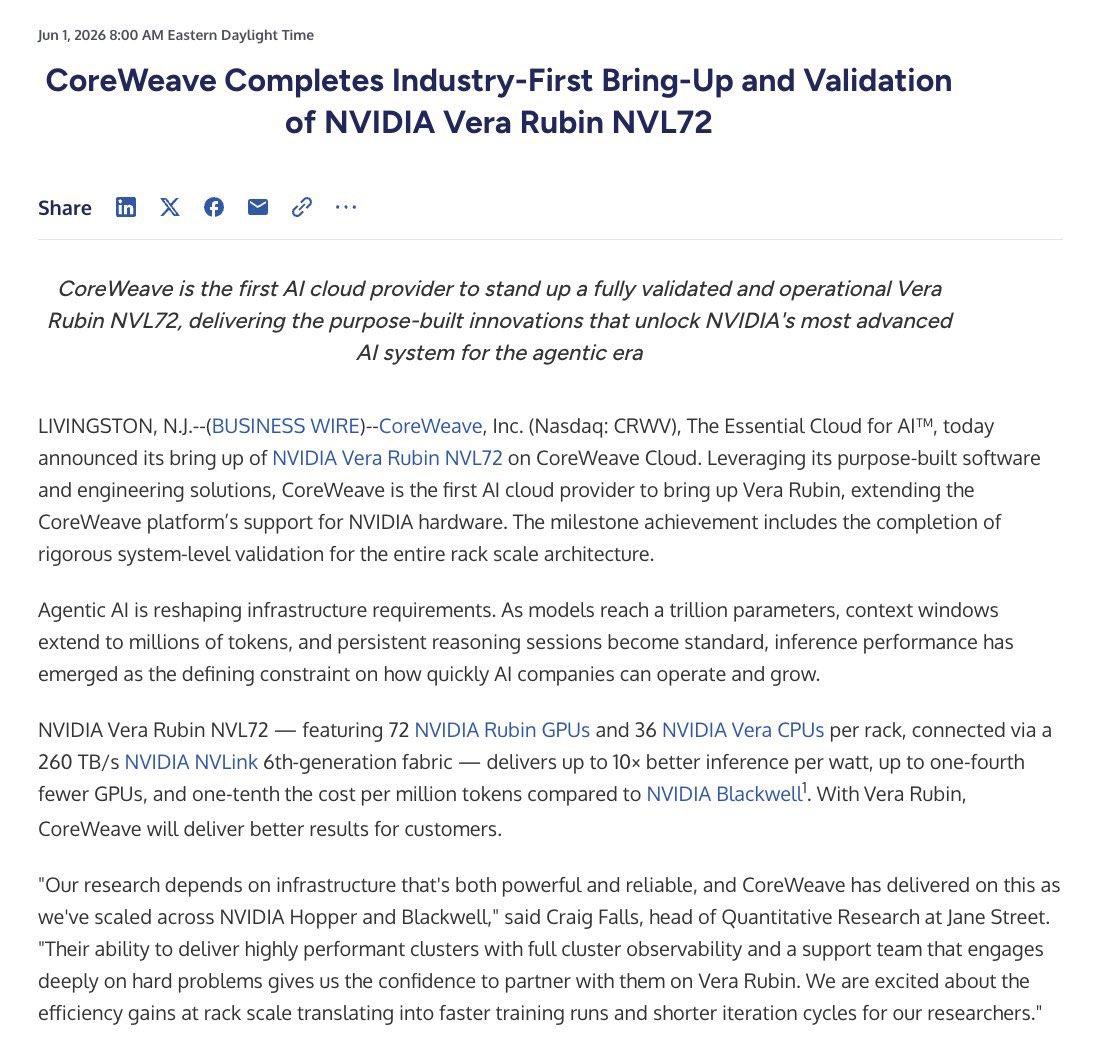

$CRWV Coreweave just became the first AI cloud provider to fully deploy and validate $NVDA Vera Rubin

The fastest path to the newest NVIDIA infrastructure is increasingly running through CoreWeave

This is why the company continues to separate itself from the rest of the market

18

3

28

4,243

$ONCY Oncolytics is focused on advancing pelareorep across the toughest cancer markets, including pancreatic, colorectal, and anal cancer.

They rbrought in CEO Jared Kelly, who previously led Ambrx through its roughly $2B acquisition by $JNJ

Disclaimer: tinyurl.com/26m3x87w

466

BeanWealth Research retweeted

May 31

Dylan Patel: “There are tons of reasons you need CPUs.”

Most investors are focused on GPUs, but CPUs are becoming a critical piece of AI infrastructure

As AI applications and inference workloads grow, demand is accelerating across the entire compute stack

10

3

5

5,395

BeanWealth Research retweeted

May 29

$AMZN AWS CEO: “Compute demand is so excessive that we have never retired old A100s.”

The AI infrastructure buildout is happening so fast that even outdated GPUs remain valuable

Most investors still underestimate how much compute capacity the AI economy will ultimately require

13

10

35

50,741

BeanWealth Research retweeted

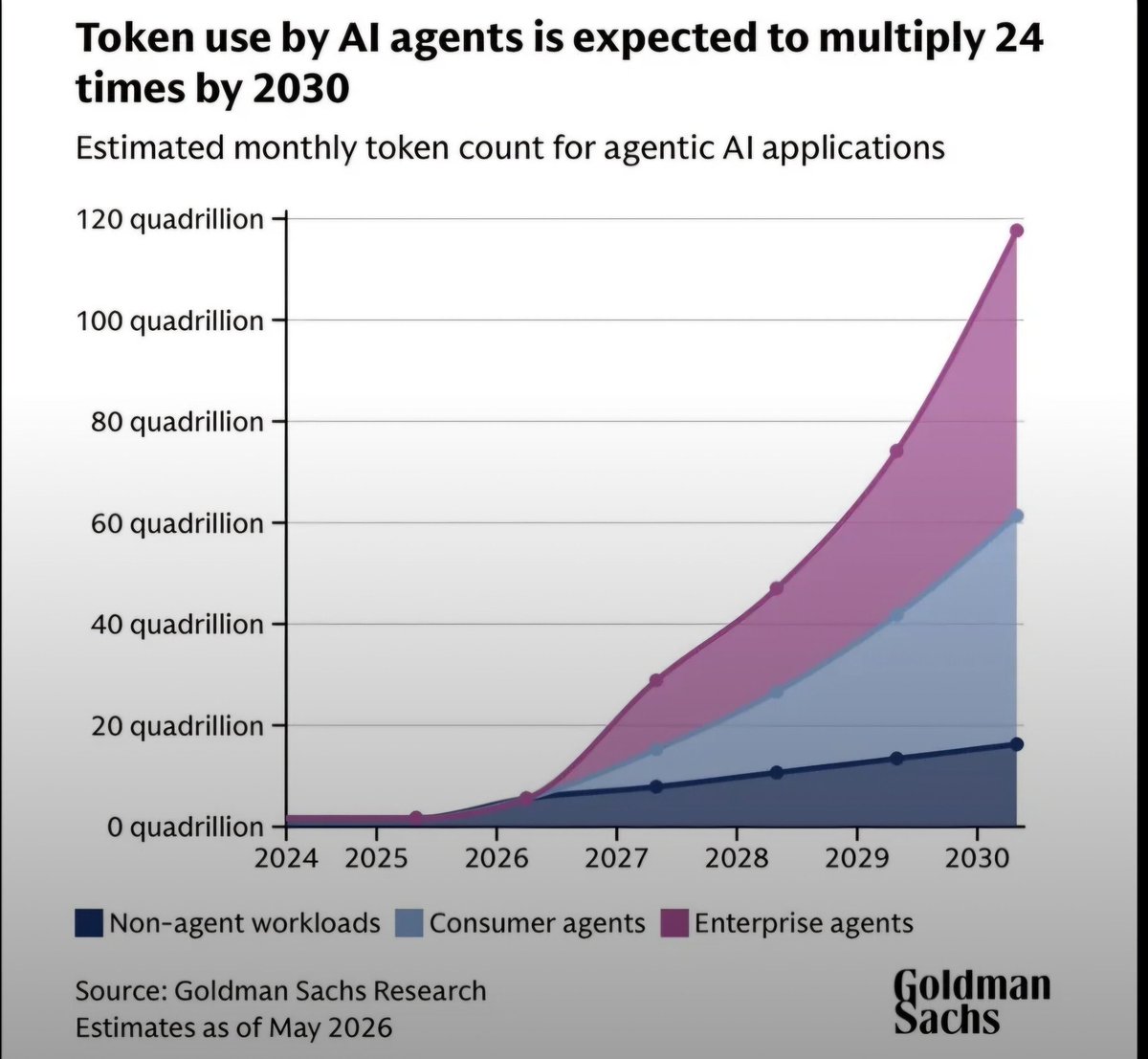

May 28

Goldman Sachs projects token usage from AI agents will increase 24x by 2030

This is massively bullish for neoclouds like $CRWV, $NBIS, $MARA, and $IREN as persistent inference demand drives enormous compute needs

The AI infrastructure boom is still very early

14

12

35

19,017

BeanWealth Research retweeted

May 27

$GRML Greenland Mines is tied directly to one of the biggest geopolitical investment themes developing right now: critical mineral independence.

The company’s Skaergaard project in Greenland has exposure to gold, palladium, rare earths, titanium, and other strategic minerals tied to defense systems, AI infrastructure, energy, and advanced manufacturing.

As the U.S. and Europe push to reduce dependence on China for critical materials, Greenland keeps becoming a more important part of the conversation.

Disclaimer: tinyurl.com/4xs2avzd

3

3

4

1,563

BeanWealth Research retweeted

May 27

Gavin Baker says the neocloud trade is far more durable than most investors realize

“Not all GPU hours are the same.”

He argued companies like $CRWV CoreWeave are operating at a completely different level than low-end providers

Investors need to watch this:

12

5

44

55,522

BeanWealth Research retweeted

May 27

Added 2 new positions in BeanFlagship, our AI infrastructure Autopilot fund:

CoreWeave $CRWV: Every major company in the world is racing to build AI and they all need one thing: computing power. CoreWeave owns tens of thousands of GPUs, the specialized chips that power every AI model being built today, and rents that computing power to the companies that need it. Think of it like owning the power grid during an industrial revolution. Everyone needs what you have and nobody can build fast enough to compete with you.

Demand is so far ahead of supply that prices keep rising and customers are paying upfront just to lock in capacity. That is not a struggling company. That is a company with all the leverage. They are guiding for $25 billion in revenue by 2027 and I believe they get there. This is one of the most important infrastructure buildouts in a generation and CoreWeave is sitting right in the middle of it.

nVent Electric $NVT: Everyone is focused on the GPUs. Nobody is asking how you keep them from melting. nVent makes the liquid cooling systems that sit inside every major AI data center and without them, a $10 billion investment in chips dies from overheating. They grew this business 76% organically in Q1 2026, have a $2.6 billion backlog that has tripled in a year, and fewer than 10% of data centers use liquid cooling today. The runway here is a decade long. This is infrastructure nobody talks about but everyone needs.

8

2

10

3,398

BeanWealth Research retweeted

May 21

Chamath Palihapitiya says AI companies now need three things: “land, power, shell.”

The AI race is a race for power as electricity demand explodes across data centers

The companies securing energy capacity today are positioning for the next decade of AI infrastructure demand

28

10

46

10,416