Joined June 2009

- Tweets 8,937

- Following 986

- Followers 1,047

- Likes 36,176

355 Photos and videos

Pinned Tweet

4

7

15

1,737

For anyone who has been puzzled by the (rightly respected) @parkeralewis claiming that the math of BTCTC valuation should imply a discount to BTC, and who were not able to reproduce the same result in their own financial calculations, here @ColeMacro lays out the misconceptions in the framing being used. Be wary when people talk of "the math" but can't or won't show their calculations. Many such cases.

Parker, your framework is still inaccurate, and the conclusion it produces is fundamentally misleading.

To be clear, I do not think you are intentionally trying to mislead people. I think the issue is that the return attribution framework you are using is not internally consistent.

This is also not an isolated issue. Across your commentary on this topic, there has been a consistent pattern of mixing frameworks, comparing unlike metrics, and then drawing conclusions that do not actually follow from the underlying analysis. I do not think that is malicious, but I do think it is a serious analytical problem.

I have done performance and return attribution work for the largest pension fund in the United States, and I have worked with some of the largest and most sophisticated asset managers in the world on exactly this type of analysis. This is not how institutional return attribution is done.

Your claim is that nearly $38 billion of common equity was raised over the period, and that the weighted average price paid underperformed Bitcoin.

But once you introduce a weighted average equity issuance price, every other part of the analysis has to be treated consistently.

That means you also need to calculate the weighted average date of that equity issuance. You cannot take a weighted average issuance price across the entire period, then compare returns from the beginning of 2024 as if all of that equity existed on day one.

By your own framework, most of the equity holders you are analyzing did not even exist at the beginning of 2024. So using the beginning of 2024 as the return start date for that capital is simply the wrong math.

Because much of Strategy’s equity was issued later, and at higher prices, the weighted average issuance date will be pulled meaningfully forward. That matters. A lot.

If you want to build the strongest version of your own critique, the correct analysis would look something like this:

1. Calculate Strategy’s weighted average equity issuance price over the relevant period.

2. Calculate the weighted average issuance date for that same equity.

3. Calculate the Bitcoin price using the same cash-flow-weighted timing.

4. Then compare performance from that weighted average date, using internally consistent assumptions across equity issuance, Bitcoin, and the relevant return period.

That would at least be a coherent, apples-to-apples analysis.

But that is not what you are doing.

What you are doing is taking one metric on a weighted average basis, then combining it with a return period that starts before much of the capital was actually raised. That is not return attribution. It is a mismatched calculation that produces a misleading answer.

The institutional way to analyze this is either to use total return from a fixed start date, such as the beginning of 2024, or better yet, since the inception of the strategy in 2020.

Or, if you want to analyze capital raised over time, use a cash-flow-weighted framework that matches each equity issuance to the correct date, price, and corresponding Bitcoin price.

But you cannot mix the two frameworks. You cannot use weighted average issuance economics on one side of the ledger and a fixed-date return from 2024 on the other side. That is precisely how you get the wrong conclusion.

My view remains that the proper framework is total return over the period, ideally from the inception of the strategy. If you want to use 2024 because that is the period you are focused on, then use 2024 consistently. If you want to analyze equity issuance over time, then cash-flow weight the entire analysis consistently.

Right now, your critique does neither.

That is why I believe your analysis is inaccurate, fundamentally wrong, and misleading. Again, I am not saying that is intentional. I am saying the framework itself is flawed, and the math does not support the conclusion you are drawing.

1

1

109

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 14

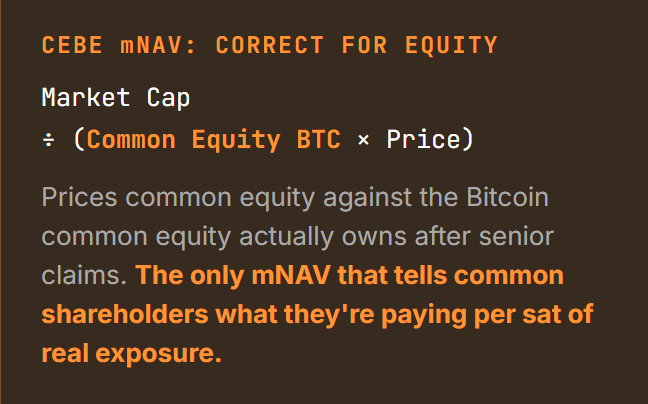

Exactly this. The long run convergence is the fiat claims eroding against BTC. The short run path dependence is why one CEBE reading isn't the whole story, you read it across the price path, not off a single point

Duration tells you how fast the claims converge, but CEBE is the right lens at every point along the way. Appreciate the h/t

1

19

367

Saylor spelling out economic calculation for those who still haven't been able to figure out the complex math of addition and multiplication required for valuation metrics.

Jun 14

BPS measures Bitcoin per common share before senior claims. CEBE BPS measures Bitcoin per common share after senior claims. CEBE is the conservative risk metric. BPS is the common equity growth metric. BTC Yield measures BPS execution.

1

62

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 13

Bitcoin & The Clash Of Two Inexorable Realities zerohedge.com/crypto/bitcoin…

33

51

342

90,416

. @CEBETracker Where can I find the graph of MSTR's CEBE mNAV over time? Thank you

1

3

169

History's first trillionaire is a guy who catches rockets out of the sky with chopsticks and beams internet to every dead zone on the planet.

Same guy ships cars that drive themselves, humanoid robots for the factory floor, brain chips that let paralyzed people move a cursor with pure thought, and an AI running on a supercomputer his team stood up in months instead of years.

And the people crashing out about his net worth are doing it on the app he owns. The same app governments spent years trying to censor.

You cannot legislate a rocket into orbit.

Jun 12

1,893

11,591

70,976

2,374,617

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 12

With all this mNAV talk its important to know where you sit. If you are a common equity holder there is no choice.

5

4

22

3,248

Elon Musk does not own a yacht

Gavin Newsom does

Jun 12

Americans are struggling to pay for groceries and gas while Elon Musk becomes a TRILLIONAIRE.

When the federal government is for sale, the rich get richer and everyone else gets shafted.

The system is rigged.

354

3,899

40,435

722,293

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 10

My bullish/bearish take on bitcoin is that we shouldn’t blame any entity for buying too much of it, because if bitcoin can be killed by an entity buying it, then it wasn’t meant to be.

If all it takes to kill bitcoin is a bullish entity that likes it enough to buy, then go home.

As @LynAldenContact says. If one entity is able to be a problem that kills it, it’s never meant to be more.

205

234

3,436

413,601

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 10

I don't condone any of what I've seen in Belfast. I mean, I'd go to prison if I did, but all the same, it's not my preferred way of doing things. But then my preferred way of doing things (voting and public debate) hasn't made the slightest impact on the decision-making of the state. As such, there was a certain inevitability about this.

Moreover, it's not really my place to judge. I am an extremely fortunate individual who happens to live in a 99% white area, miles from any "diversity" and thanks to my self-employed status, I don't have to self-censor or live a double life at work. I don't have to bottle up my opinions. I actually make a modest income by expressing them.

Most low income working class people, meanwhile, have to live in close proximity to diversity and the squalor that goes with it. Their votes are even more worthless as mine, and they can't speak their minds freely because there'll be some HR ghoul in the mix who will fire them. Ordinary people bear the burden of potentially losing everything for having the wrong opinions.

Meanwhile, they can work hard to carve out a little corner of peace for themselves, just for the local authority to turn next door into a migrant HMO with illegal Deliveroo drivers coming and going at all hours. It's their communities being turned into alien, hostile and violent slums. To then say there is no justification for riots is to tell them they simply have to suck it up - even when they run the risk of an African savage beheading them. What are they supposed to do? Write to their MP? Everyone has a breaking point.

While politicians call for calm, they can only expect to be heeded if they actually do something, but remaining calm when the politicians continue to sit on their hands as people are butchered in the street is absolutely bovine. Ultimately these riots are a consequence of the wilful deafness of politicians, and the blame for what we've seen tonight lies squarely in their shop.

121

891

4,663

101,945

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 10

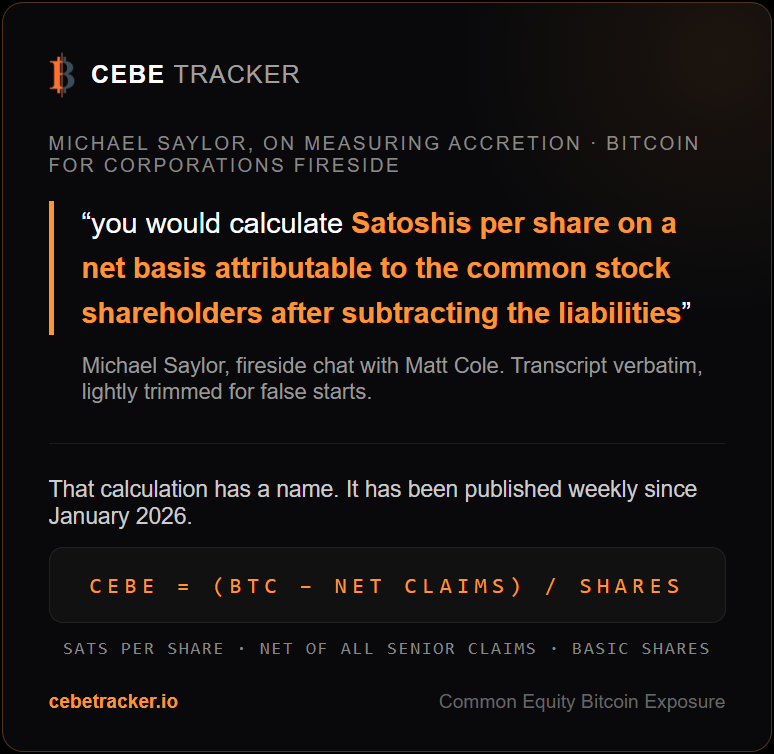

Saylor was asked how to measure whether a deal is accretive. His answer is to calculate satoshis per share, net basis, attributable to common shareholders, after subtracting the liabilities.

That calculation has had a name since January and cebetracker.io publishes it weekly

In the same conversation 'for you to understand whether the company's accreting or diluting, you have to understand all of the tangible assets, the cash, all of the liabilities.'

All of the liabilities, net of cash. That is the entire CEBE methodology in one sentence

He also pushed back on netting preferred, calling it mezzanine capital rather than a balance sheet liability. Fair framing from the issuer's seat. From the common shareholder's seat, the liquidation preference stands ahead of you in every outcome that matters, whatever the balance sheet calls it. CEBE is measured from the common seat. Both views are correct. They answer different question

Another interesting line surfaced, 'there's still a lot of room for debate about what is the right way to value a hybrid credit instrument like STRC.'

Agreed. More on that soon

7

23

126

11,100

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 8

Our statement on the UK government’s demand that all content on all devices sold or used in the country be scanned, on the presumption of nudity, using a dystopian combination of age verification and content scanning. This proposal will not safeguard children. It endangers us all.

signal.org/blog/pdfs/2026-06…

740

8,561

41,368

2,743,459

Something I remember from @saylor's What Is Money series with @Breedlove22: If you could choose one superpower, choose immortality because if you can survive anything, you will eventually figure out how to win. #bitcoin

46

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

Jun 6

It is so wild that the Yookay government is simultaneously trying to lower the voting age to 16, and ban the Internet until age 16.

The Times's weekend read:

* The Labour leadership contest has already begun. In No 10 Starmer is fighting for his political life, putting huge pressure on teh system to bolster his Premiership in face of existential threat posed by Andy Burnham

* Expect a frenzy of activity in coming weeks - the defence investment plan, social media restrictions for under 16s, the Brexit reset. Announcements bogged down in months of bitter internal rows will finally come into public view

* All the announcements are coming before or shortly after June 18th, the date of the Makerfield by-election. Starmer is trying to send a message to Labour MPs that he can deliver

* He isn't the only one. Burnham has began issuing his own national leadership pledges - starting with a £300million cut in business rates for pubs and small businesses

* His press release directly attacked Starmer and Reeves, accusing the government of 'undervaluing' their importance to local communities. This is a *Labour* candidate directly criticising a *Labour* government

* The lines between the Labour Party and Burnham's campaign are increasingly blurred. Team Burnham now has a lot of the party machinery on his side - press officers, officials etc - and also has most of the cabinet out knocking doors in Makerfield. Power is already moving

* Starmer thinks he can fight Burnham, but his allies are unconvinced. One said that he thinks Burnham has behaved 'appallingly'. 'His view is why should he make it easy for him?'

* But there is an acknowledgement that Starmer is on borrowed time. That it is a case of when, not if he goes

* There are divides in Team Burnham over when he should amke a move if he wins Makerfield. The 'go-now' camp say he must seize the opportunity or it could slip through his hands, using the momentum of the by-election to act decisively

* But others think this could be disastrous - that he needs time to build up a proper plan for government and No 10. That if he doesn't he risks repeating Starmer's mistakes all over again

* Then there's what's being billed as the 'battle for the soul of Burnham'. There are those on the left - Louise Haigh, Miatta Fahbulleh and others - who favour a radical break from Starmer. Then there are the centrists - Josh Simons, Jim O'Neill - are are said to be emphasising the importance of fiscal credibility. It is potentially a v unwieldy coalition

thetimes.com/uk/politics/art…

427

1,407

6,418

1,399,955

It's important to realize that much of the slowness one observes in node validation and syncing isn't an inherent limitation of Bitcoin, but an artifact of an inefficient reference implementation-- one that "can't" be significantly changed due to its brittleness in deciding consensus. This is as a result of a belief that "the code is the spec" which results in code that cannot be materially reengineered or rewritten without risk of a chain split. We need to move towards a formal specification of consensus and a multiplicity of modern compliant efficient clients. We shall not trust but verify. hornetnode.org/spec.html @hornetnode

May 31

There are two classes of significant problems that arise from the unnecessarily poor performance. (1) increasing calls to abandon validation (abandon Bitcoin), and (2) increasing calls for censorship (abandon Bitcoin). We have always seen this as existential work.

2

10

1,922

This is why Bitcoin not crypto. Because decentralization means a central authority cannot confiscate.

May 29

JUST IN: 🇺🇸 Treasury Secretary Scott Bessent says the U.S. Government has seized $1 billion of Iran's crypto:

"Just outright grabbed the wallets. Some of them may be typing in right now and might not realize their wallet had been grabbed."

6

1

14

681

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

May 30

Every 50k blocks (almost 1 year) the Libbitcoin team bumps up its sync benchmark. Running on the same (now 10 yo) hardware we work to keep the benchmark milestone sync under 1 hour. After spending the last week implementing a deferred optimization... 950,000 blocks in 56.2 mins!

11

20

109

8,410

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

May 29

This is a 110 IQ take.

The 140 IQ take is that Saylor doesn’t own any bitcoin himself - it is owned by shareholders who have confidence in his ability to acquire more Bitcoin - and that is just corporate adoption of Bitcoin as savings tech, which is a prerequisite for hyperbitcoinization.

The 160 IQ take is that Saylor, by packaging Bitcoin into corporate securities with different risk profiles, has done more to democratize and distribute Bitcoin than any person since Satoshi himself. People who own $STRC are, without knowing it, using bitcoin:native to save, but at a risk profile that is acceptable to them.

Michael Saylor isn’t preventing anyone from owning bitcoin - and he, more than anyone, tells you to do so - but he is opening up Bitcoin to people and pools of capital that previously could not access it.

May 29

Saylor can't sell a substantial portion of his bitcoin without tanking the price.

Networks are meant to be distributed. Liquidity comes from distribution.

Saylor has done nothing to promote distribution.

Strategy is a shitcoin.

125

161

1,610

298,668

Bitcoin Dudebro 3.125 ⚡️🇬🇧 retweeted

May 28

Sorry isn’t good enough.

We need to see the body-worn footage and these officers need to face consequences.

The treatment of this murdered student, in his dying moments, is a national scandal.

1,455

9,523

49,094

538,751