The Shortest Path to Customer Trust 💙

Joined October 2012

- Tweets 1,089

- Following 1,308

- Followers 1,341

- Likes 551

140 Photos and videos

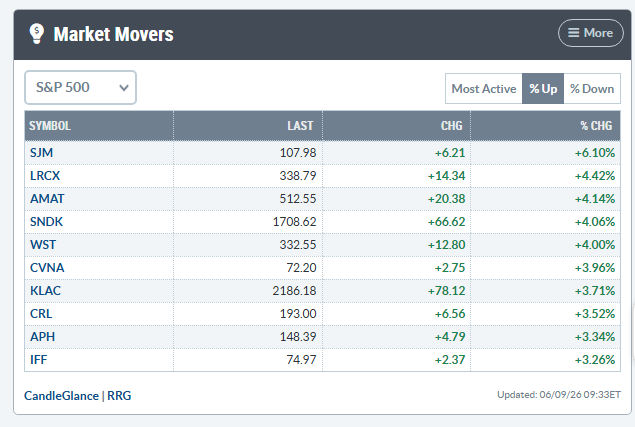

Fun to see former Candid customer J.M. Smucker having a strong day.

Consumer staples are easy to underestimate from the outside.

Coffee, pet food, frozen handhelds, spreads.

Not flashy categories.

But the customer content is incredibly real:

freezer drawers

lunchboxes

pantry shelves

backseat snacks

dog treats after a walk

coffee before the house wakes up

That is where a lot of brand trust actually lives.

Not in the campaign.

In the routine.

1

575

The internet keeps trying to automate authenticity.

Then a few real vacation photos show up and casually do 780K views.

No hook.

No framework.

No “wait until the end.”

No cinematic AI polish.

Just a human moment people believe.

That is still the signal brands are chasing.

1

445

Same primitive.

Very different market.

In 2015, Like2Buy and the early link-in-bio visionaries helped brands turn Instagram attention into ecommerce traffic. We had great success with similar flows at Candid: social post → mapped destination → product/content page.

Useful, but enterprise-shaped.

Stan pointed the pattern at creators selling digital products.

Not “visit the PDP.”

“Buy from me.”

One capability shift, 10 years in between.

Completely different GTM.

Completely different outcome.

The category was never about links.

It was always about converting social attention into intent.

Huge respect to the Stan team. Toronto keeps cooking.

2

633

This is the platform partner bargain.

The partner ecosystem is R&D for the platform.

It fans out, finds pockets of demand, proves workflows, and teaches the platform what should eventually become core.

Then the useful pieces get absorbed into business.facebook.com, Shopify admin, Ads Manager, etc.

Bad for easy IPO dreams.

Still a fun business if you like useful work, sharp customers, and a permanently moving floor.

they are trying to kill cursor and lovable… and every startup and application — as I’ve warned

Infrastructure companies eventually try to win the platform game, then they learn and take out all their partners on the app layer

1

1

704

Shopify turning 20 is a good reminder that ecommerce infrastructure gets valuable by surviving boring things.

API changes.

Theme changes.

Pixel changes.

Mobile shifts.

Social platform chaos.

AI waves.

Another “this changes everything” every six months.

The flashy layer changes constantly.

The useful layer keeps working.

Jun 2

Shopify launched to the public 20 years ago today

1

498

“AI UGC” is such a funny phrase.

It can imitate the format.

It can imitate the camera angle.

It can imitate the awkward pause before the hook.

What it can’t imitate is the actual endorsement:

a real person choosing to be publicly associated with the product.

That’s the scarce part.

430

Today Instagram had this massive exploit where hackers were just stealing rare handles left and right. Hundreds of accounts gone.

People losing handles they’ve owned since 2010, some worth hundreds of thousands.

I own a few rare ones so I was actually stressed watching this happen in real time, which I haven’t been in years.

Obama White House account got hit.

These aren’t some random new accounts, these are verified, locked down accounts and they still got compromised.

The thing is the exploit is so simple it’s almost funny. Attacker goes to Forgot Password, says their account is hacked, turns on a VPN to match the target’s location (which now you can find on the about section of the page).

Instagram’s AI support flow asks them to verify with a selfie.

They grab a photo from the target’s profile, run it through an AI video generator to make an animation of the person’s face moving around, upload that to Meta’s AI as proof.

And Meta’s AI just accepts it because it can’t tell the difference between a real selfie and an AI-generated video of someone’s face

.

Once verified they change the email to theirs. Password reset link goes to their email. They own it now. 2FA gets bypassed somehow in the process but honestly I don’t know exactly how, just that it did.

Point is even locked down accounts went down.

Then you try to recover your account and you’re talking to a chatbot that has zero ability to help.

You can’t escalate to a human. You’re just stuck. Your asset is gone and there’s no one to call.

The whole thing just highlighted how stupid it is to automate account security without any human in the loop.

One AI fooling another AI while there’s literally no person anywhere to catch it.

Meta took hours to even acknowledge it while accounts were getting stolen every minute.

Now thankfully it’s patched but I don’t think it will be the last one. Stay safe!

302

1,627

10,634

2,041,443

Yep.

A great app feature is often just one messy workflow disappearing.

Auto-mapping and publishing content for brands with high-volume owned posts or paid influencer output is a good example.

Sounds boring on paper.

Eyes light up when you see it work.

May 31

Interviewed a founder who charges $299/month for a single Shopify app feature.

Merchants pay without blinking. That one feature saves them 8 hours a week.

If you can quantify the time your app saves, you can charge more than you think.

1

1

737

Public customer content is becoming scarcer, not less valuable.

Meta is still creating more content volume than ever: Reels, AI tools, Edits, recommendations, translation, advertisers.

But casual public posting is moving away from the old feed model and into lower-pressure surfaces: Stories, Close Friends, Notes, DMs, trial reels.

That changes the job for brands.

The value is no longer “put a feed gallery on the homepage.”

The value is capturing the shrinking share of public customer endorsement, clearing rights, mapping it to products, and reusing it wherever buying decisions happen.

Scarcity increases the value of the signal.

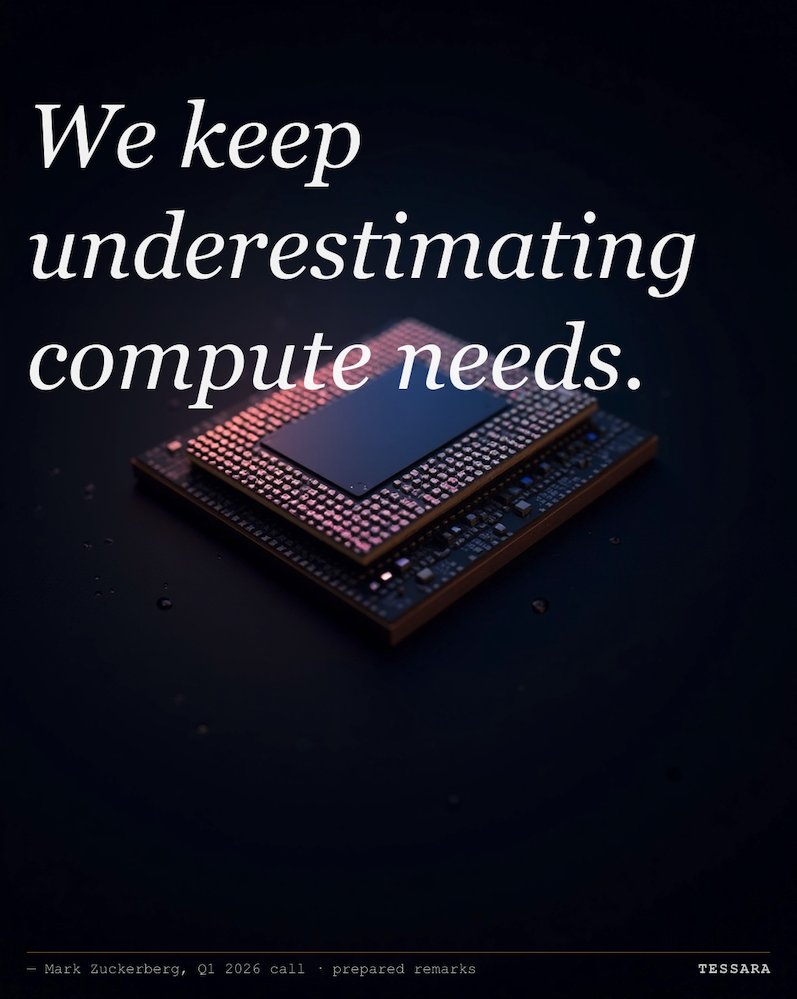

Apr 30

META's Q1 earnings call a few hours ago was important (i listened to the whole hour)

The headline was not the $56.3B revenue or 33% growth. The bigger signal is that Meta raised 2026 capex guidance again to $125-145B from a prior $115-135B... and drove a $107 billion step-up in contractual commitments through multi-year cloud deals and infrastructure purchase agreements in a single quarter.

Management's key line, on Q&A: "we have continued to underestimate our compute needs, even as we have been ramping capacity significantly."

That was paired with explicit commentary that "most of that [capex increase] is due to higher component costs, particularly memory pricing."

The implication: capex tightness is not just a $META story. It is a regime signal. Memory is the binding constraint of 2026, and hyperscalers are pre-paying for capacity years out because they cannot otherwise secure it.

Other signals from the call:

- Q1 capex was light at $19.8B.. well below the ~$32-36B/quarter pace implied by the FY guide. The ramp is back-half-loaded, with direct implications for H2 prints from AVGO, ANET, VRT, ETN.

- Custom silicon hit gigawatt scale: "more than one gigawatt of our own custom silicon that we're developing with Broadcom," alongside "significant amount of AMD chips to complement the new NVIDIA systems." AVGO is now a structural recipient of capex flow; AMD is a confirmed second source on merchant accelerators.

- May layoffs disclosed on the call: "We plan to reduce the size of our employee base in May." Meta is cutting opex to fund capex. That is a multi-year commitment, not a one-quarter narrative.

The bear case is execution: $125-145B capex absorption, FCF compression, and margin pressure if memory prices don't normalize.

1

2,733

Most UGC programs do not fail at the gallery.

They fail at intake.

The content exists.

The problem is everything around it:

Who submitted it?

What product is it tied to?

Do we have rights?

Which project/customer/location is it from?

Can legal use it?

Can ecommerce use it?

Can email use it?

Is it approved, expired, localized, tagged, archived?

A social CMS is not just a pretty display layer.

It is the system that turns messy community content into usable website content.

1,584

Both AI.

One was told to look perfect.

One was told to feel candid.

That distinction matters.

Studio AI optimizes for polish: clean light, clean skin, clean product, clean everything.

Candid AI optimizes for believability: a little movement, a little imperfection, a little “someone might have actually posted this.”

Same technology. Different intention.

And real customer content is still the far end of that spectrum:

no prompt

no art direction

no brand approval before the moment happened

Just someone choosing to be seen with the product.

1

2,144

The point is not “AI bad, real good.”

The point is that commercial perfection and social believability are different creative goals.

A product image can be flawless and still feel empty.

A community signal works because it carries context: taste, identity, popularity, and public association.

1,257

Not all customer content carries the same signal.

A review photo says:

“I bought this.”

An organic social post says:

“I’m willing to be seen with this.”

That difference matters.

The real value of community content is not just showing the product in the wild. Amazon has plenty of that.

The stronger signal is public association.

Someone liked the product enough to put it on their feed, in front of their friends, with their taste and reputation attached.

That is why social content can influence differently than reviews.

It signals trend, popularity, taste, and community support around the brand.

The asset matters.

But the context around the asset is the endorsement.

1,515

Fashion brands now have AI models that are indistinguishable from real ones.

And it turns out viewers don’t consciously notice the difference.

But they feel it. Conversion stays flat. Brand equity quietly erodes. Communities don’t form around synthetic social proof — they form around real people making real choices.

AI fills catalogs. It doesn’t build tribes.

In a world where the default is synthetic, a real human wearing your product has become the scarcer, more valuable signal. Not the baseline. The premium.

Real is now rare.

1

1,844

To be clear — this isn’t anti-AI across the board.

For furniture, home decor, CPG, interior design? AI visualization is better than traditional photography. See it in your room, your colorway, your layout. No model needed. No lifestyle pretense required.

The distinction is whether the product needs identity transfer or spatial imagination.

Fashion sells a self. A sofa just needs to fit.

1,644

The best social proof is placed near the question it answers.

Fit question? Put it near size/variant selection.

Style question? Put it near product media.

Trust question? Put it near reviews or cart.

Usage question? Put it in the gallery, PDP, or post-purchase flow.

“Add UGC” is vague.

Answer shopper doubt.

1,349

Memorial Day weekend is a good reminder that discounting is not positioning.

A sale can create urgency.

It cannot answer:

Will this fit my space?

Will this look right on me?

Do people like me use this?

Is this brand for real?

That is the job of customer proof.

For a lot of B2C brands, the missed CRO opportunity is not another promo bar.

It is making the product page feel less abstract.

1,620

A bit of visual commerce history the internet mostly forgot:

Around 2015, on the IRCE / Shop.org / NRF circuit, Shawna Hausman and the giggle team were already talking about customer content as commerce infrastructure.

They may not have invented the idea.

But they were among the first we saw pitch it from the stage to the broader retail industry: use real customer content across ecommerce, email, social, apps, and ads. Handle rights properly. Treat UGC as more than a social feed.

One pattern from that era has aged especially well:

pushing approved UGC back into the native product media library.

Not just rendering a gallery.

Actually attaching real-world customer content to the right SKU, product, collection, or context so the commerce platform can use it like catalog media.

That unlocks things like:

- clean studio image by default

- “in the wild” image on hover

- richer PLPs and collection pages

- PDP media that feels native

- customer proof without an external display

- storefront performance through the existing image pipeline

Furniture sites later made this pattern feel obvious.

But the insight was already being presented to the industry 11 years ago.

UGC is not just content you display.

Done properly, it becomes part of the product record.

Credit where it’s due: Shawna and the giggle team were early.

One under-discussed pattern: using the social CMS to enrich the native product media library, not just render an external UGC display.

In that setup, approved customer content is pushed back into the commerce platform/CMS and attached to the relevant SKU, variant, collection, or room/style context.

That unlocks a few useful things:

- customer proof can show up inside native product media

- PLPs and collection pages can use real-world imagery, not only PDP galleries

- hover states can swap from clean studio shots to “in the wild” context

- merchandising teams can control the mix without hard-coding displays

- the storefront keeps using its native image pipeline, CDN, and theme behavior

Furniture sites have made this pattern especially visible: white-background catalog image by default, lived-in room shot on hover.

It is still social proof. It is just delivered through the catalog layer instead of a separate widget.

3,478