Fund manager interviews, stock pitches, fund letters / by @ksmetrics

Joined October 2020

- Tweets 1,790

- Following 2,545

- Followers 6,892

- Likes 2,459

360 Photos and videos

Pinned Tweet

If you’re seeking new ideas make sure to join our weekly Best Stock Pitches newsletter.

Every Monday we email you a curation of the best stock pitches from fund managers and super smart private investors.

JOIN BELOW...

capitalemployed.com/p/stock-…

1

8

3,855

Jun 12

Interview #134 just published.

For this edition we welcome Patrick Rial from TriVista Capital and Hosomichi Fund.

Patrick discusses his background, approach to investing, and pitches two Japanese small caps.

capitalemployed.com/p/2-stoc…

2

4

1,832

Capital Employed retweeted

Best Stock Pitches newsletter just published.

62 ‘fresh-off-the-press’ stock pitches to get stuck into, from Italian tire makers to organ transplants.

Find your next idea >

capitalemployed.com/p/62-qua…

2

3

1,124

Capital Employed retweeted

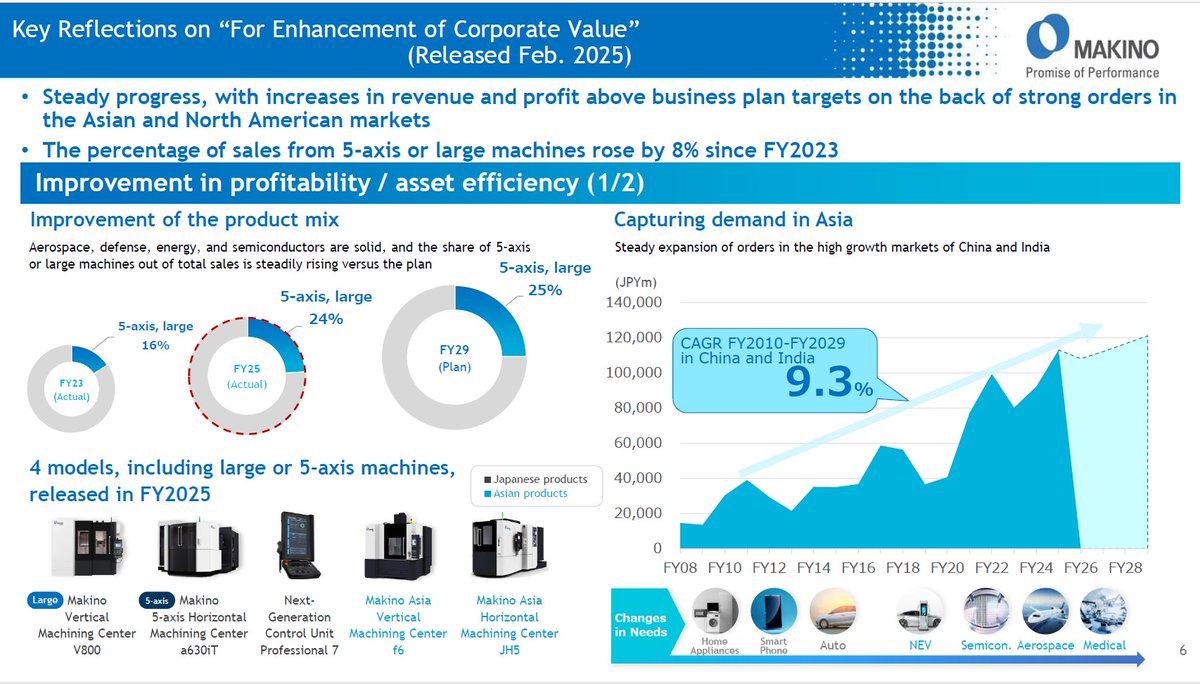

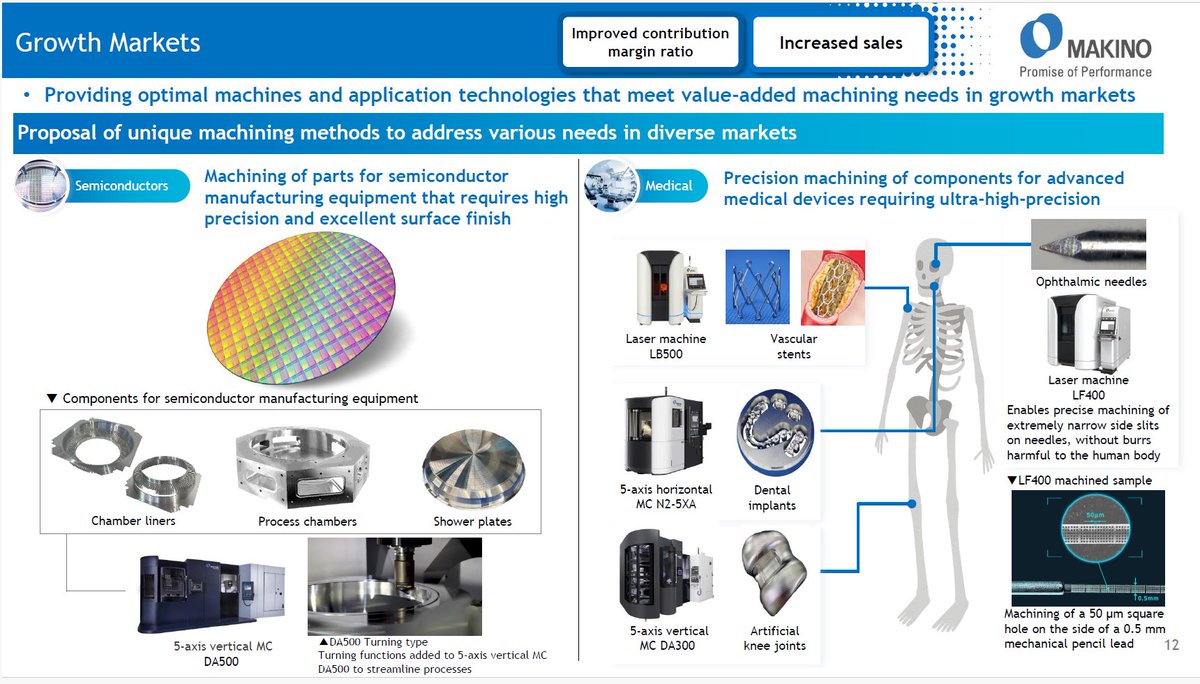

After digging around, I finally settled on my favorite Japanese machine tool producer: Makino $6135.T From giga-casting molds and satellite structures to gas turbine cooling holes and vascular stents, Makino’s tools excel in the toughest machining jobs.

The failed Nidec acquisition in 2025 and the blocked PE buyout in April revealed the company’s strategic value. The Japanese government blocked MBK Partners’ acquisition of Makino on national security grounds, arguing that its machines “are widely utilized by manufacturers of defense equipment in Japan.” I found several examples of Makino machines inside defense manufacturing ecosystems across Japan, Europe, and the US. They are used to make flight-critical structures and propulsion components for F-35 and Typhoon fighter jets, CH-47 and OH-1 helicopter engines, and gas turbines of Japanese destroyers.

Beyond defense, management is also targeting aerospace, energy, semiconductor, and medical markets, where customers need high-precision machining of difficult materials and are willing to pay up for productivity, accuracy, and process know-how. Key applications are aircraft engine parts, gas turbines, semiconductor equipment, and medical devices.

Makino’s opportunity in the emerging space economy deserves a separate post. The US satellite producer Astranis uses Makino MAG3.EX to machine full satellite panels in-house (video linked below). I’m also fairly confident that Makino machines are integrated into the supply chains of SpaceX and Blue Origin.

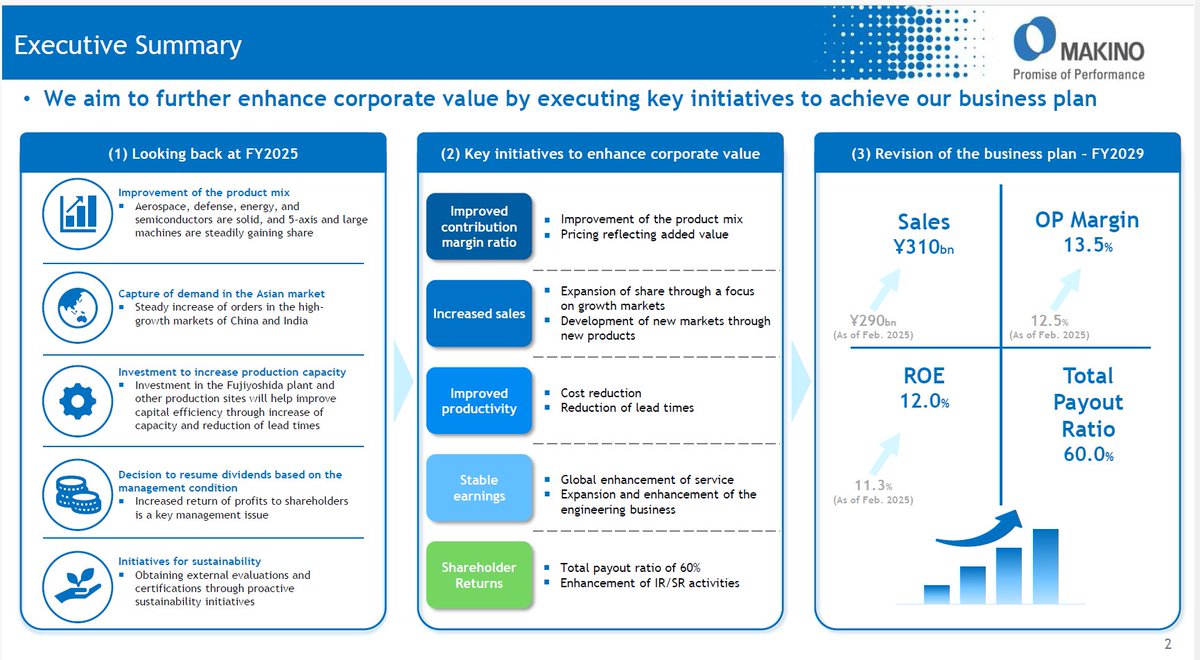

After the acquisition fiasco, management is under pressure to unlock Makino’s true potential. The “Corporate Value Enhancement” plan announced in May focuses on larger and more complex machines, pricing discipline, shorter lead times, higher-margin engineering and aftermarket services, dividends, and buybacks.

The plan is good, but I think it undersells the opportunity. I assume the company will achieve at least 7% revenue CAGR and reach 15% operating margin by 2030. That gets me to ¥21,500 per share or ~50% upside. At ~13 P/E, Makino looks too cheap for its strategic importance, technical depth, and end-market optionality. I took an initial position this week and will be watching for the buyback announcement and continued order build-up.

3

13

87

35,784

Capital Employed retweeted

Interview #133 just published. For this edition we welcome @leevalueroach from The Value Road.

Lee discusses his approach to investing, and shares two stock ideas.

capitalemployed.com/p/2-stoc…

2

10

8,142

Nearly all of the Q1 2026 fund letters have been published now.

The average YTD return was -3.14%

So well done if you're beating that.

capitalemployed.com/p/q1-202…

1

5

616

'Prices fluctuate more than values — so therein lies opportunity.'

Joel Greenblatt

3

11

3,061

Capital Employed retweeted

Best Stock Pitches newsletter just published.

43 ‘fresh-off-the-press’ stock pitches to get stuck into, from beauty devices to Greek shipping.

Find your next idea >

capitalemployed.com/p/43-bes…

2

3

1,058

Capital Employed retweeted

May 30

I was interviewed by @capitalemployed and pitched 2 stocks! One was a previous disclosed position and the other a new one

May 30

Interview #132 just published. For this edition we welcome @HalvioCapital

Anthony discusses his background, his approach to investing, and shares two stock ideas.

capitalemployed.com/p/2-stoc…

1

9

2,885

May 30

Interview #132 just published. For this edition we welcome @HalvioCapital

Anthony discusses his background, his approach to investing, and shares two stock ideas.

capitalemployed.com/p/2-stoc…

4

3,498

Capital Employed retweeted

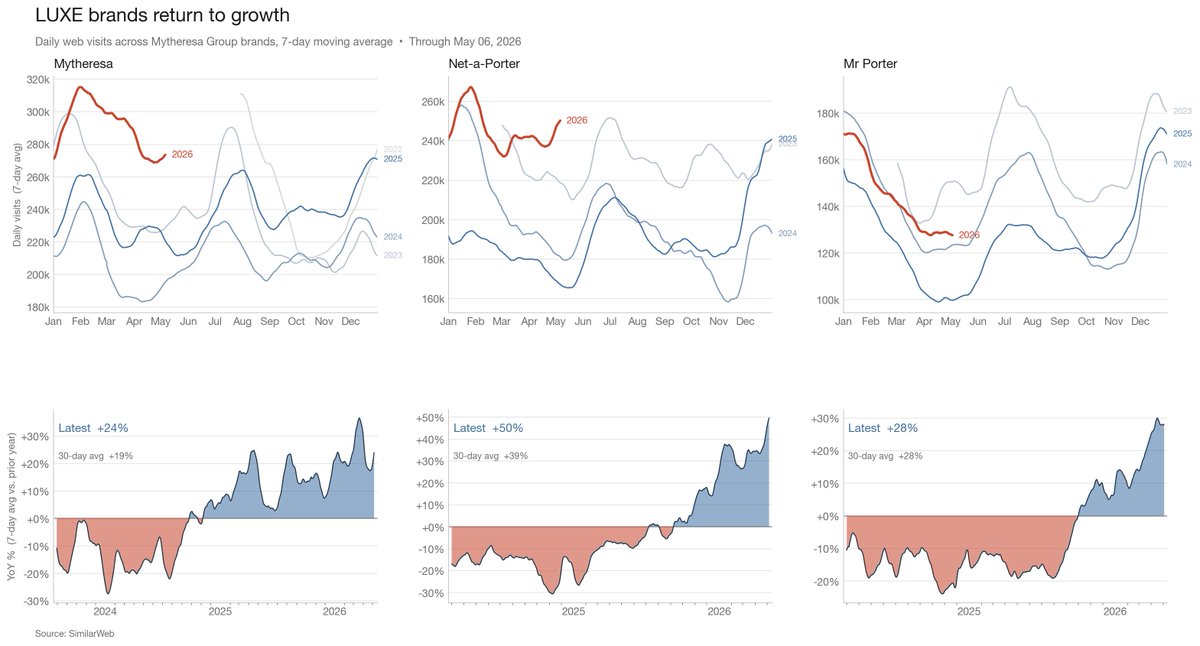

$LUXE could easily be a 1-2x from here. Stock at $7.80 USD -- trades at 0.2x EV/sales and 0.5x EV/gross profit. On FY26 ex-Offprice, it's at ~7x EBITDA.

Run-rate rev at 2.5B EUR, growing LDD -> ~3B in 2 years. At mgmt's 8% margint target, that's like 2.6x EBITDA, and ~160m EUR in net income. About $1.30 per share in EPS.

At a 15x multiple (cheap for a LDD grower) that's worth >$20.

Stock has sold off on inflation fears, but lux consumers are well insulated. Meanwhile, web traffic trends continue to accelerate as LUXE turns around acquired brands Net-a-Porter and Mr. Porter.

4

2

23

21,770

Capital Employed retweeted

May 16

*US meatpackers, cheap enough?*

The US' largest domestic protein producers $TSN $SFD $PPC screen relatively attractively when viewed across the cycle, enjoy defensive demand, and have scale moats.

However, each protein cycle is unique, and we might be approaching a time of great cost inflation at a time of demand disruption.

We have to go over each of the company's segments, capital allocation history, demand/cost drivers, leverage, and arrive at a comment on their valuation

1

1

7

5,514

Capital Employed retweeted

May 18

Best Stock Pitches newsletter just published.

44 ‘fresh-off-the-press’ stock pitches to get stuck into, from a variety of fund managers and investment newsletters.

capitalemployed.com/p/44-bes…

2

3

962

Capital Employed retweeted

May 15

Thanks for having me. Excellent newsletter.

May 15

Interview #131 just published.

For this edition we welcome Wengang Ji from Trigram Partners @TrigramPartners

Wengang discusses his background, launching Trigam Partners, his approach to investing, and shares two stock ideas.

capitalemployed.com/p/2-stoc…

1

1

972

May 15

Interview #131 just published.

For this edition we welcome Wengang Ji from Trigram Partners @TrigramPartners

Wengang discusses his background, launching Trigam Partners, his approach to investing, and shares two stock ideas.

capitalemployed.com/p/2-stoc…

1

2

1,731

Capital Employed retweeted

May 11

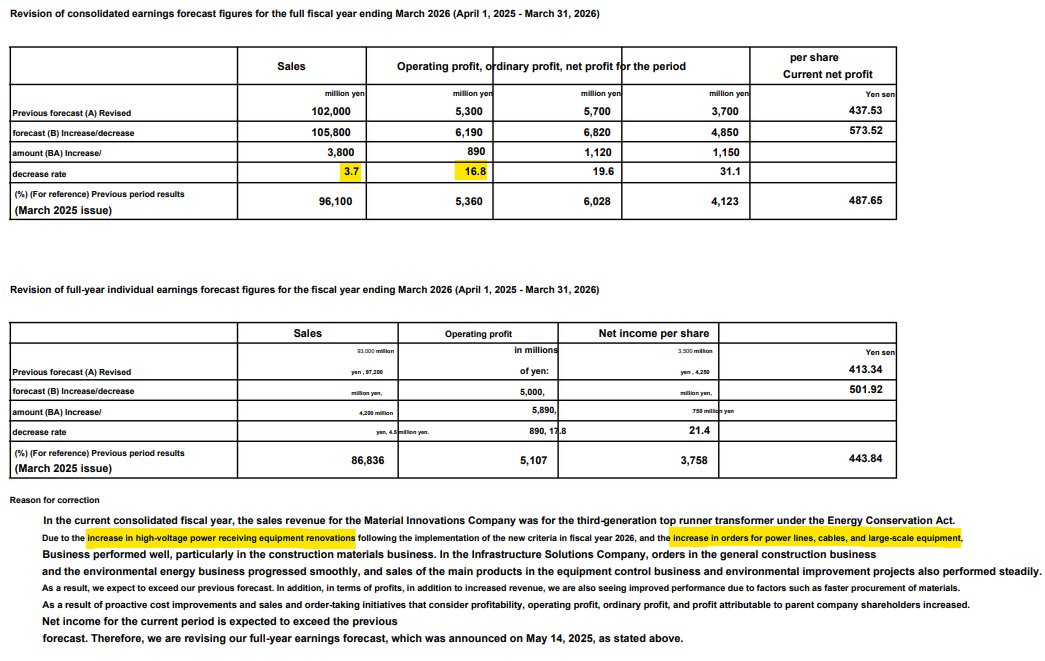

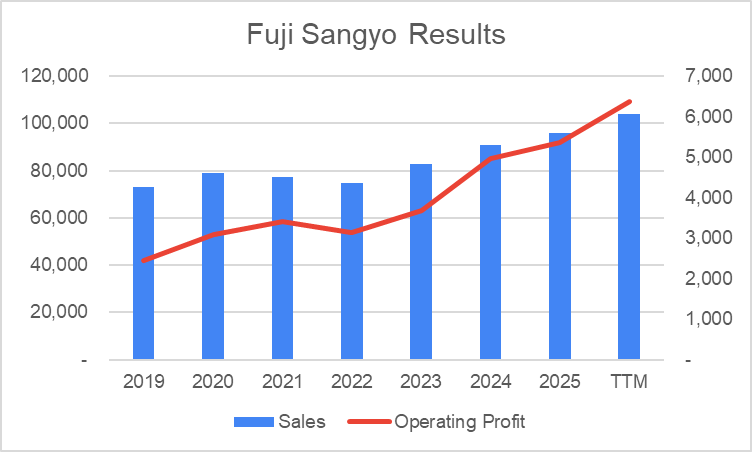

Fuji Sangyo $9906.T raises FY3/26 guidance today, 4% on sales & 17% on OP while bumping their dividend from 130 to 160 (3.7% yield).

Remains awfully cheap at 0.9x TBV, 2.4x EV/EBIT & 7.5x P/E with ~2/3rd of mkt cap in net cash and electric grid tailwinds.

Apr 21

Fuji Sangyo $9906.T is a good activist target. 74% of market cap in net cash with AI tailwinds. Largest ever sale of investment securities happened in 1HFY26 and dividend raise so they appear open to changes but need a nudge. 0.8x TBV, 1.7x EV/EBIT and 6.2x P/E. More below...

3

36

11,735

Capital Employed retweeted

May 11

Best Stock Pitches newsletter just published.

42 ‘fresh-off-the-press’ stock pitches to get stuck into, from a variety of fund managers and investment newsletters.

capitalemployed.com/p/42-sto…

1

3

948