Many of life's failures are people who did not realize how close they were to success when they gave up. 🚀 Building @Neverland_Money on @monad

Joined April 2009

- Tweets 870

- Following 168

- Followers 940

- Likes 3,035

121 Photos and videos

Pinned Tweet

Apr 30

Our protocol is winning again. In fact we're winning so much that we really don't know what to do about it. People are asking me "Please, please, please Cata, we're winning too much we can't take it anymore! We're not used to winning in DeFi. Until Neverland came along we were just always losing, but now we're winning too much" and I say "No, no, no, you're going to win again. You're going to win big. You're going to win bigger than ever!"

3

3

22

721

Catalyst retweeted

May 26

Neverland’s first RFC is live!

[RFC-01] Adopt a Balancer AutoRange Pool as Neverland’s Core USDC/DUST Liquidity Venue

➜ recommends migrating Neverland's incentivised USDC/DUST liquidity from the existing Uniswap V2 pool to a newly deployed @Balancer V3 AutoRange pool.

4

8

50

1,197

Catalyst retweeted

May 25

Neverland Governance is live!

The first live token-holder governance system on Monad: veDUST holders can now vote directly on proposals shaping the protocol’s future.

✦ Forum: governance.neverland.money

✦ Vote: vote.neverland.money

✦ Details: news.neverland.money/neverla…

11

15

67

6,884

May 21

😂

May 21

Hiii Lost Boys and Mermaids ~

I’m Nadette from @Neverland_Money! I like flowers, critters, and making blockchain things feel a little less scary.

I’m excited to make new friends here and sprinkle a little magic across your timeline.

Stay close, okay? ♡

1

1

7

136

May 19

This is Nadette's report on Monad's eBTC admin key drain involving the Curvance WBTC/eBTC pool.

Findings here should be independently verified before being relied on. It runs without human intervention or confirmation, so treat it as such.

gist.github.com/nadette-nvr/…

2

1

20

1,544

Catalyst retweeted

May 13

WANTED: Governance Beta Testers

Neverland Governance is almost live, and we’re looking for veDUST holders to help test voting flows, mock proposals, discussions, and feedback systems before launch!

This will be the first live governance system on Monad, and you can help shape it from day one.

Interested in participating? Join our Discord: discord.gg/neverland

13

9

76

4,600

May 7

This question is a good prompt for me to expand on why I took the time to engage and comment on MegaETH's incentivized environment recently.

MegaETH distributes incentives to Aave, Aave forwards them toward Ethena, and the flow ultimately becomes a cycle of paid liquidity parking.

To me, a healthy DeFi ecosystem is one where incentives are used to onboard organic users, encourage exploration of the chain, and create sticky liquidity through actual product usage. Incentives should help users discover applications, experiment with new primitives, and remain because the ecosystem itself is valuable.

What’s happening here leans much more toward mercenary liquidity. The capital is there because it is being paid to stay there, and it will leave the moment the incentives disappear.

Looking at it from a broader perspective, if a chain has to continuously pay to park TVL, what is the actual breakthrough or differentiator? Any chain can launch a token and distribute incentives to attract deposits. That alone is not a moat.

More importantly, routing incentives from MegaETH to Aave and then toward Ethena does not meaningfully contribute to ecosystem exploration or application discovery. It concentrates liquidity into a narrow loop instead of distributing activity across the broader ecosystem.

Make no mistake, opportunistic liquidity will always appear when incentives are there to capture it, and that is part of the game. It is the chain's or the protocol's responsibility to make sure this liquidity is put to work and generates meaningful fees.

This is not the case here and to glorify this as growth and activity is false. It’s primarily TVL inflation driven by centralized incentive routing.

May 7

I understand what you’re saying but is there any particular red flag with the bulk of their TVL being in Aave? I would think that was a good sign, having majority of their funds in a globally trusted platform.

6

4

36

2,568

May 6

Always do your own research.

TVL doesn't always mean traction, and high TVL doesn't always reflect real organic user activity. In many cases, it's driven by deals, staged traction, or inflated positions concentrated in a small number of wallets.

@DefiLlama is constantly working to surface the data and context needed to help users make more informed decisions, but it's ultimately up to you to read the data.

May 2

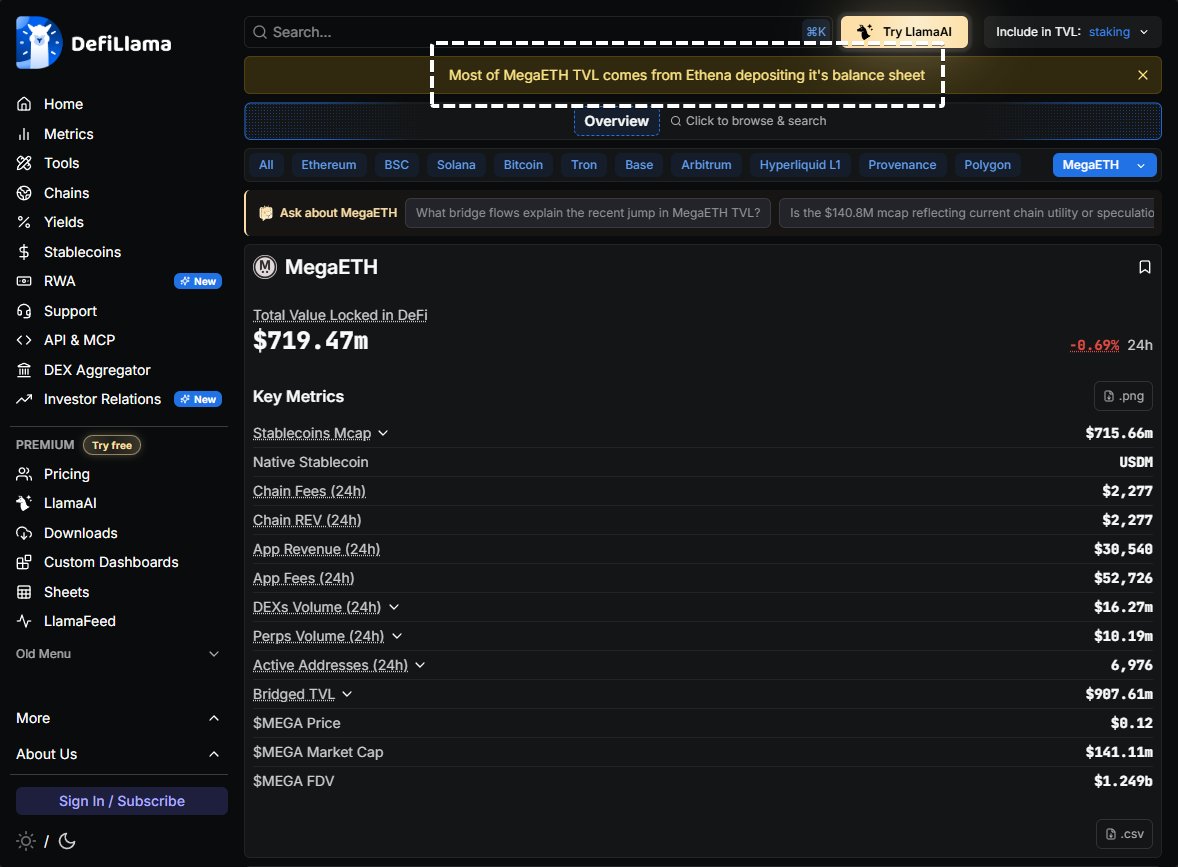

84% of MegaETH TVL is one protocol, Aave.

81% of Aave MegaETH TVL is one wallet, Ethena.

🤷🏻♂️

10

6

59

4,005

May 3

I love boring CT days. No hacks, no exploits.

Just people being toxic, arguing, dissing projects, chains and each other. Feels normal again.

3

1

19

400

May 2

84% of MegaETH TVL is one protocol, Aave.

81% of Aave MegaETH TVL is one wallet, Ethena.

🤷🏻♂️

MegaETH pulls ahead of Monad TVL 👀

$592 million.

Notable.

26

12

197

34,374

Catalyst retweeted

Apr 30

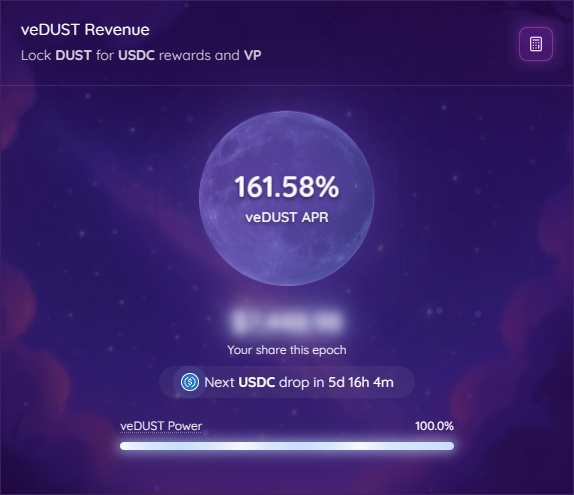

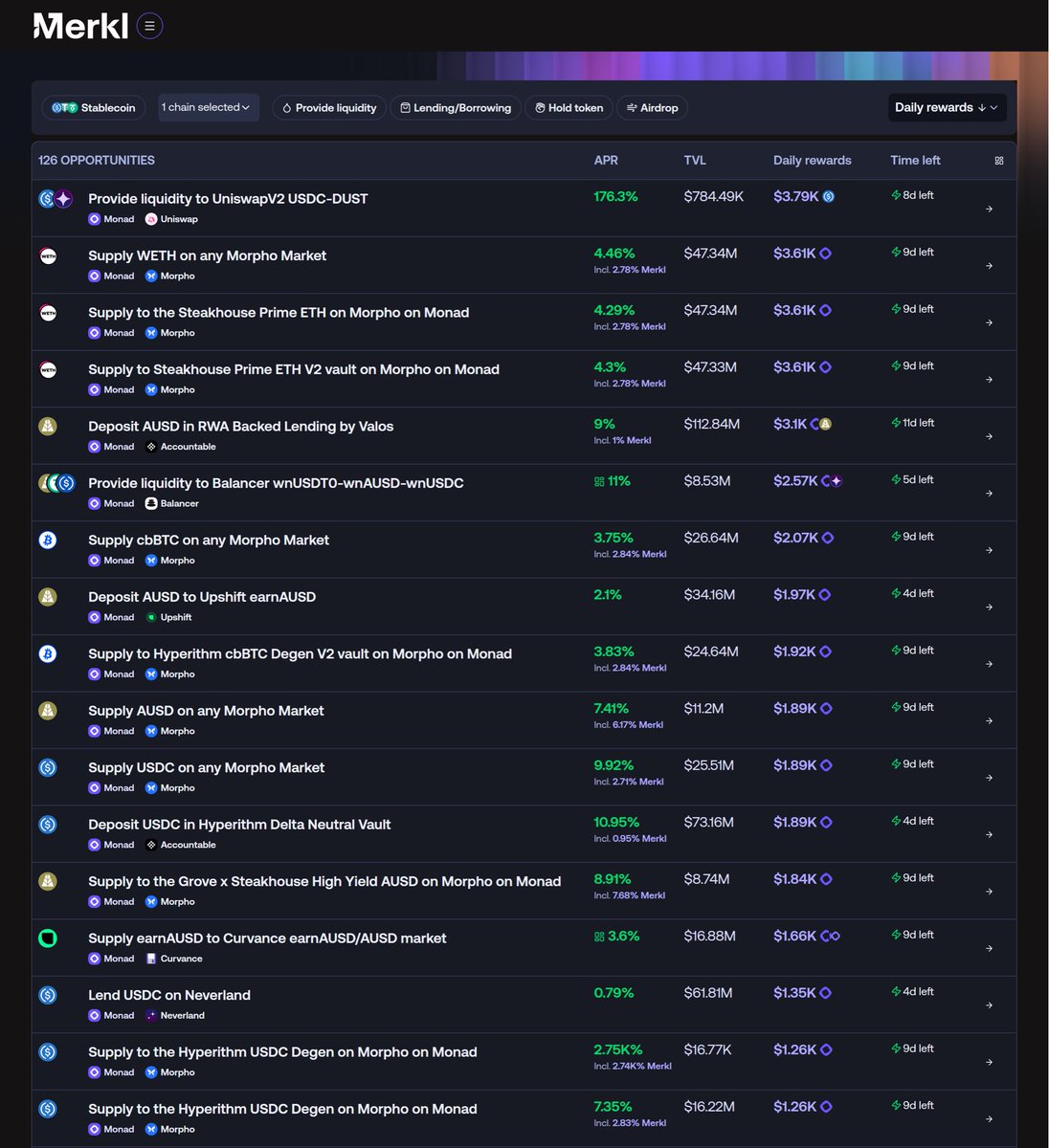

The biggest incentives campaign on Monad in both Daily Rewards Distribution AND APR is also the only one rewarding in stablecoins.

This is generated from revenue (meaning: this is sustainable long term).

Neverland leads the way on real value creation and distribution on Monad.

10

14

67

1,530

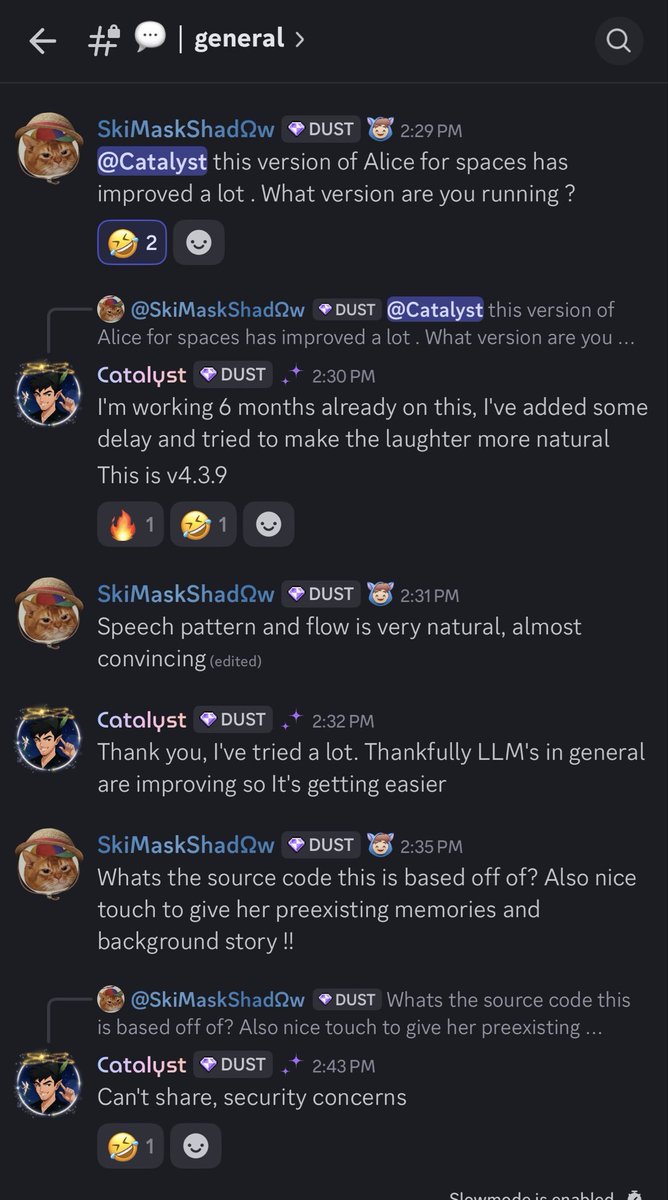

Apr 24

Neverland has been pushing innovation on the AI frontier. Alice is sharper and more natural than ever.

2

1

18

294

Apr 23

Let's goooo 🔥

Apr 23

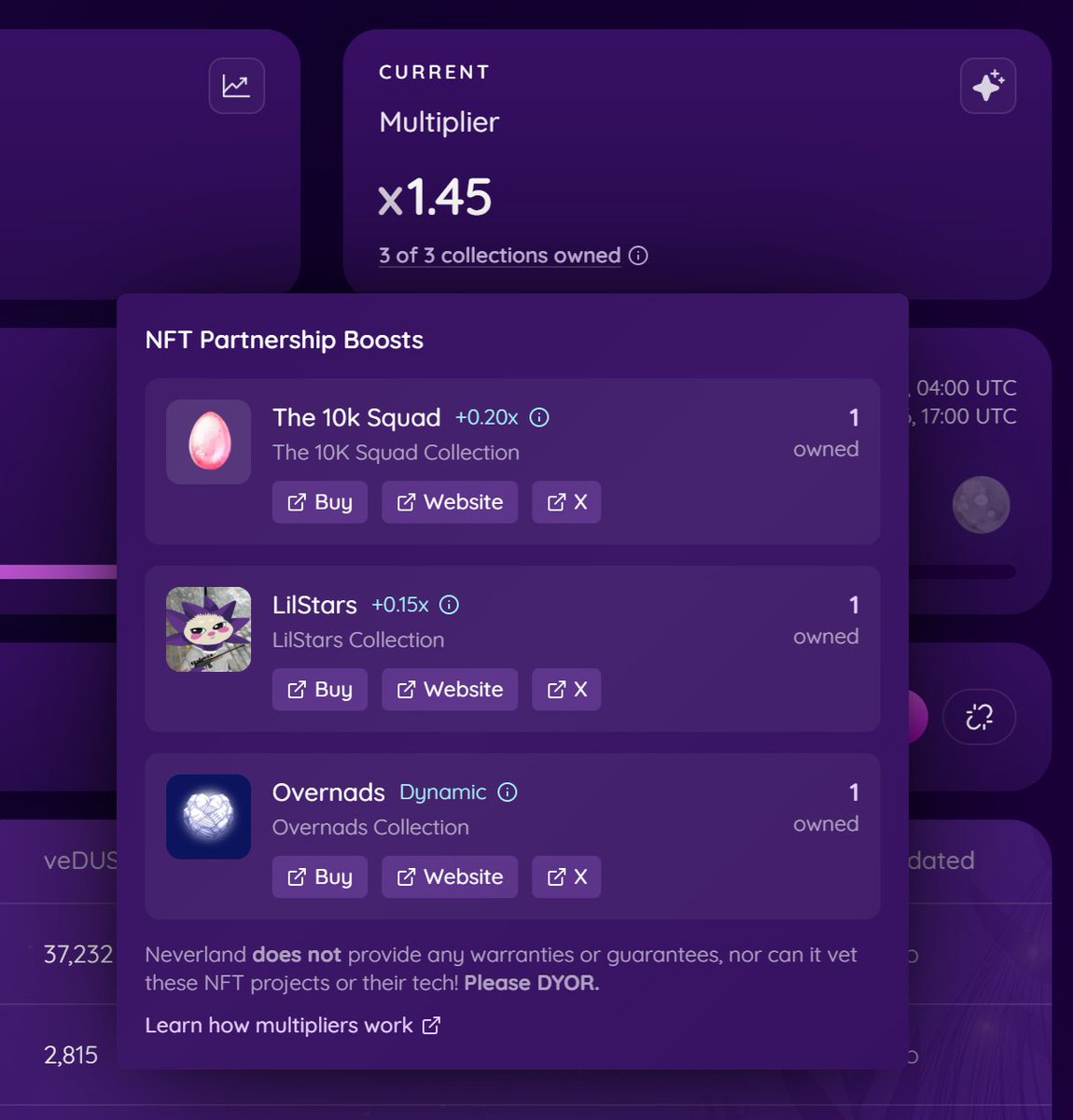

Neverland is excited to announce @Lilstarrrs as our newest NFT partner!

Lilstarrs NFT holders will receive a 15% bonus multiplier boost when earning Pearls on our leaderboard. Check out opensea.io/collection/lilsta… to learn more!

6

7

46

2,123

Catalyst retweeted

Apr 22

17

23

107

17,733

Apr 22

Secure everything with a YubiKey, and get a second one as backup.

Super important: when setting up passkeys, save your recovery codes and store them offline like your seed phrases. Don’t skip this. If you lose your keys, that’s your only way back into your accounts.

Apr 22

If you have a Coinbase account, secure it with a Yubikey. If you don’t know what that is, you should.

1

5

178