growth & brand strategy @indexcoop · member @safaryclub · advisor @lotusfi_

Joined March 2021

- Tweets 919

- Following 930

- Followers 695

- Likes 9,340

104 Photos and videos

chavis retweeted

Jun 4

Vaults are the ETFs of the crypto world 🌏

They package DeFi’s growing opportunity set into a single product that's accessible to institutions, retail, and everyone in between.

From our conversation with @RasterlyRock, Head of Research at @Bitwise.

1

8

18

6,598

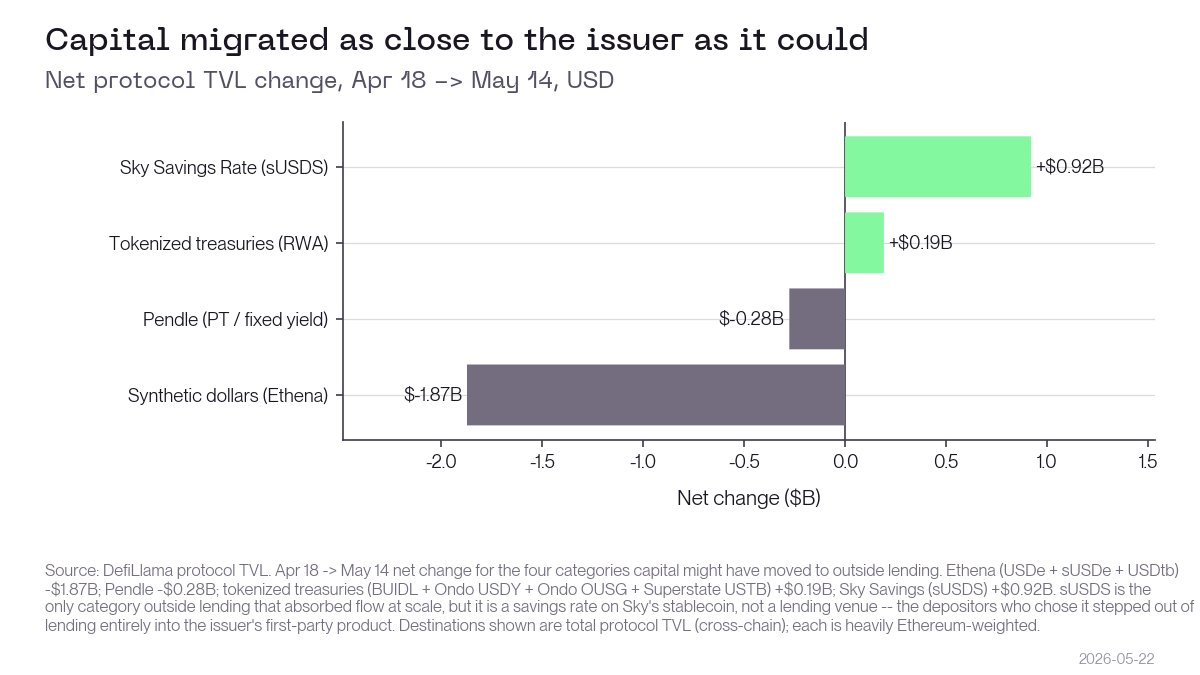

You might imagine capital moved up the stack after rsETH. It mostly didn’t

Not synthetics like sUSDe, not fixed-yield on Pendle, not tokenized treasuries like BUIDL

sUSDS is the closest thing to a counter example. Capital migrated as close to the issuer as it could

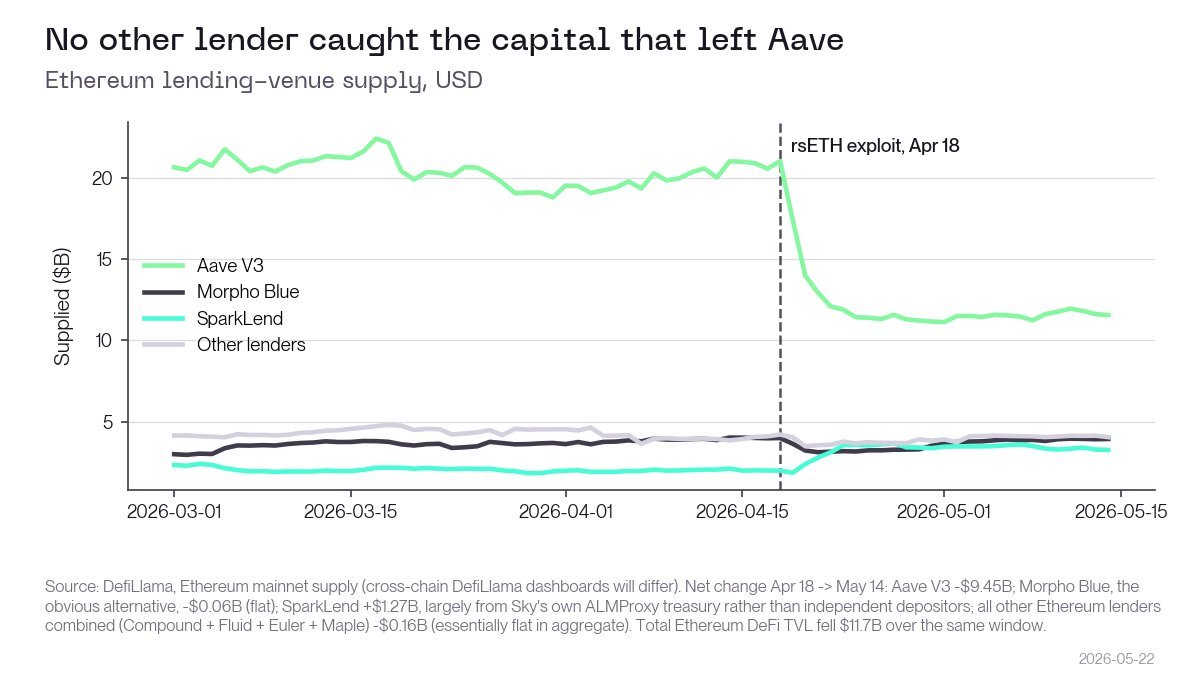

The most interesting thing about the fallout from the rsETH exploit is where the capital fleeing Aave didn't go.

During the event, Aave lost nearly $10B in TVL. Those funds, for the most part, did not move to another lending protocol. Morpho ended the window flat. So did Fluid. Compound fell 13% and Euler lost about 40% of its supply.

The only one that gained was SparkLend.

SparkLend gained $1.27B over the window. The largest single depositor was Spark's own automated treasury contract which net-contributed $437M, roughly a third of SparkLend's total gain. Outside the treasury, the depositor base was top-heavy and focused within a handful of large wallets

In a bank run, people don't go to the bank, withdraw their funds, and then go deposit to the bank next door. The financial system is interconnected. If one bank is in trouble, they all could be.

So, Aave didn't break. They managed to plug the hole and cascading failures were averted. But.. the capital didn't come back. The entire sector remained contracted beyond the event

I think this is because Aave functioned as the trust ceiling for the category - the safest option onchain capital had. When the safest venue is in trouble, there is nowhere safer to run. And if Aave isn’t safe, the logical conclusion is that nowhere is.

In the same month, total stablecoin supply hit a record $320 billion. The capital is here. It just isn't lending.

Aave's USDC supply rate sits at 3.50%. SPAXX, Fidelity's government money market fund, is paying 3.29%.

The premium for DeFi lending's opaque risks is twenty-one basis points right now

Most depositors were likely unaware they had indirect exposure to rsETH until this event. The question now is what else they are unknowingly underwriting

1

6

631

The most interesting thing about the fallout from the rsETH exploit is where the capital fleeing Aave didn't go.

During the event, Aave lost nearly $10B in TVL. Those funds, for the most part, did not move to another lending protocol. Morpho ended the window flat. So did Fluid. Compound fell 13% and Euler lost about 40% of its supply.

The only one that gained was SparkLend.

SparkLend gained $1.27B over the window. The largest single depositor was Spark's own automated treasury contract which net-contributed $437M, roughly a third of SparkLend's total gain. Outside the treasury, the depositor base was top-heavy and focused within a handful of large wallets

In a bank run, people don't go to the bank, withdraw their funds, and then go deposit to the bank next door. The financial system is interconnected. If one bank is in trouble, they all could be.

So, Aave didn't break. They managed to plug the hole and cascading failures were averted. But.. the capital didn't come back. The entire sector remained contracted beyond the event

I think this is because Aave functioned as the trust ceiling for the category - the safest option onchain capital had. When the safest venue is in trouble, there is nowhere safer to run. And if Aave isn’t safe, the logical conclusion is that nowhere is.

In the same month, total stablecoin supply hit a record $320 billion. The capital is here. It just isn't lending.

Aave's USDC supply rate sits at 3.50%. SPAXX, Fidelity's government money market fund, is paying 3.29%.

The premium for DeFi lending's opaque risks is twenty-one basis points right now

Most depositors were likely unaware they had indirect exposure to rsETH until this event. The question now is what else they are unknowingly underwriting

2

2

14

2,894

chavis retweeted

New @Edge_Pod!

Aave compresses risk.

Morpho isolates it.

Lotus clears it.

The @LotusFi_ Founder @Davidareising on why bad debt in DeFi can be better addressed, and how Lotus handles it with new tranched credit markets for better vaults.

Lotus will launch this summer 2026 👀

6

9

27

3,211

chavis retweeted

Apr 30

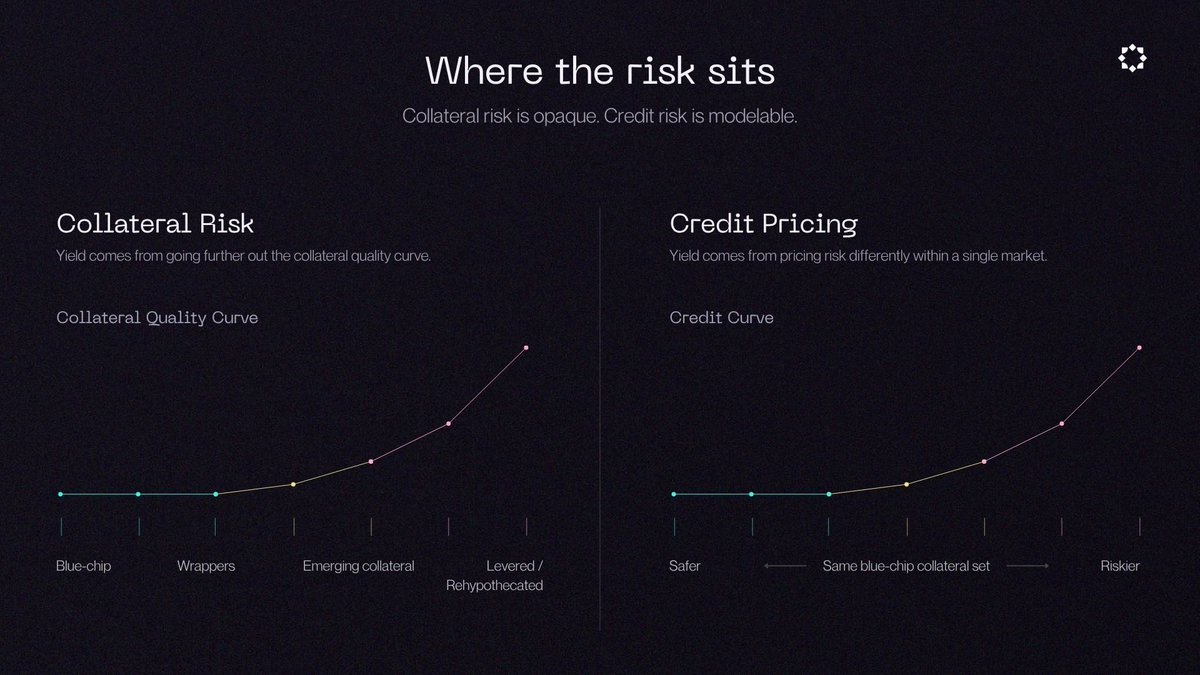

DeFi lending needs a more expressive risk curve.

Rates that match the risk you chose, on collateral you'd actually hold, with transparency you can verify.

First look at the Lotus app.

6

6

28

1,440

idk why but fixed rate borrowing hasn't ever really taken off onchain

@AnthonyBowman43 makes a pretty good case that if you put fixed term loans inside instant liquidity vaults it sets up wonky outcomes

curious if anyone has a clean counterargument

1

8

791

This announcement comes with a model you can try yourself

See firsthand what changes when the base rate is built into a lending protocol: research.lotuslabs.net/#lotu…

Apr 23

On Lotus, lenders earn yield even when no one is borrowing.

We’ve integrated @WisdomTreePrime’s tokenized money market fund into the reserve framework for LotusUSD.

A new model for DeFi lending: productive debt.

2

8

333

chavis retweeted

Regulated yield meets DeFi lending: @LotusFi_ has selected WisdomTree's tokenized money market fund as a reserve asset in their protocol.

Lenders earn yield even when no one is borrowing, first integration of its kind.

Apr 23

On Lotus, lenders earn yield even when no one is borrowing.

We’ve integrated @WisdomTreePrime’s tokenized money market fund into the reserve framework for LotusUSD.

A new model for DeFi lending: productive debt.

4

6

22

2,769

chavis retweeted

Apr 21

Looping is dead. Long live tranching.

Looping has been at the center of DeFi for the last 2 years. It's a great deal at first glance... higher yields while underwriting the same risks (albeit with leverage). If you are confident Ethena isn't going to blow up, well, you might as well loop that to get 15% APR.

But what's happened now is something that most loopers hadn't expected. They're earning -100% APR. Nothing has changed with Ethena. What's changed is the borrowing rates...leaving loopers stuck in deeply unprofitable positions. This is painful!

A single weekend (like this past one) can wipe out months (or years) of returns, from a risk that most folks aren't even underwriting. This all comes from rates being unpredictable... a looper can't know when Aave's rates will skyrocket or when they'll get stuck and be wiped out. You're not just underwriting Ethena. You're underwriting the constantly changing borrowing market.

So what now?

People still want 15% yields, and they're going to get them somehow. But looping as a vehicle is broken.

Tranching is what replaces it. Take any yield source, split it into a secure senior and a first-loss junior, and the junior gets looped-like returns without any borrow-rate exposure. No getting stuck. No negative carry.

This is exactly why Royco is built the way it is.

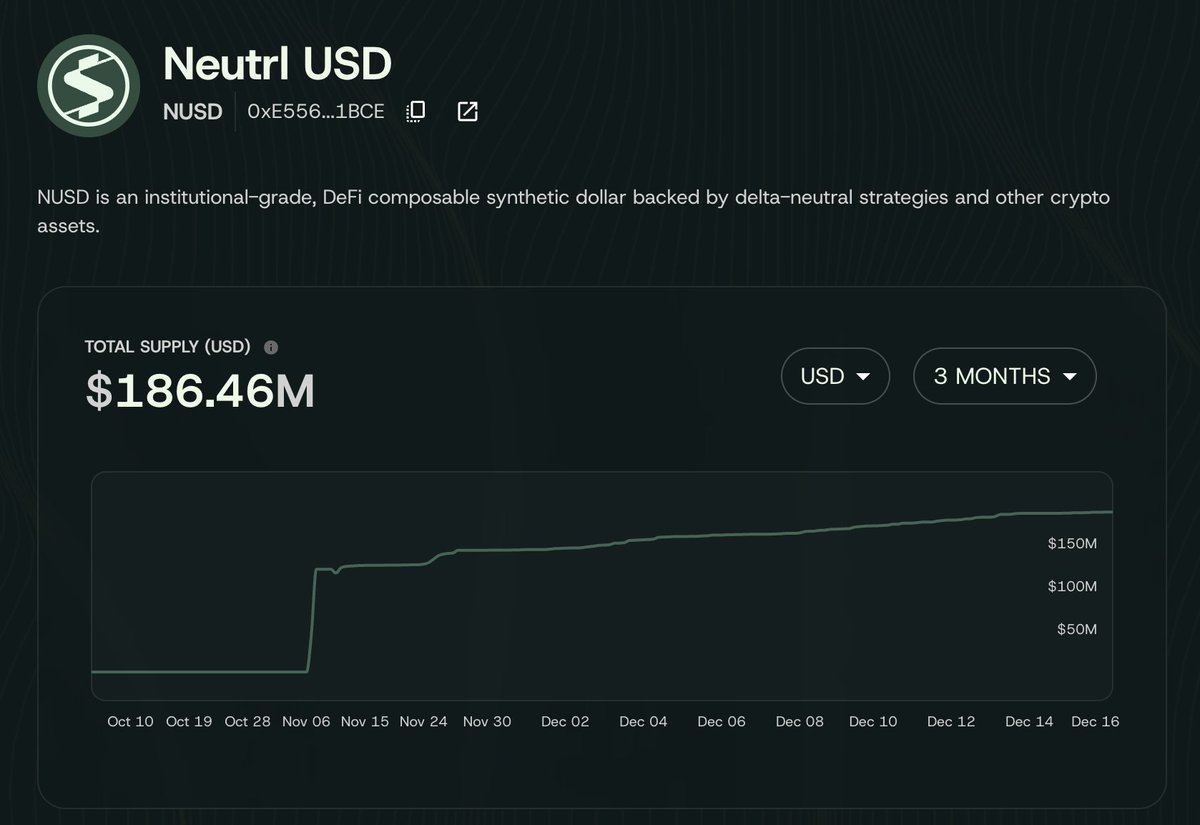

The proof is live. Participants in the junior tranches of Avant, Neutrl, AutoUSD, Smokehouse USDC, SyrupUSDC, and USDai have been earning 1.2-5x the underlying yield source, without the tail risk that just collapsed looper portfolios. And there are a lot more pools going live soon.

For folks thinking about portfolio construction, feel free to DM - happy to chat about the advantages of tranching.

19

11

111

16,131

chavis retweeted

Apr 16

DeFi lending is still waiting for its Uniswap V3 moment.

The breakthrough comes when capital can move along the risk curve, not just between markets.

4

7

31

4,620

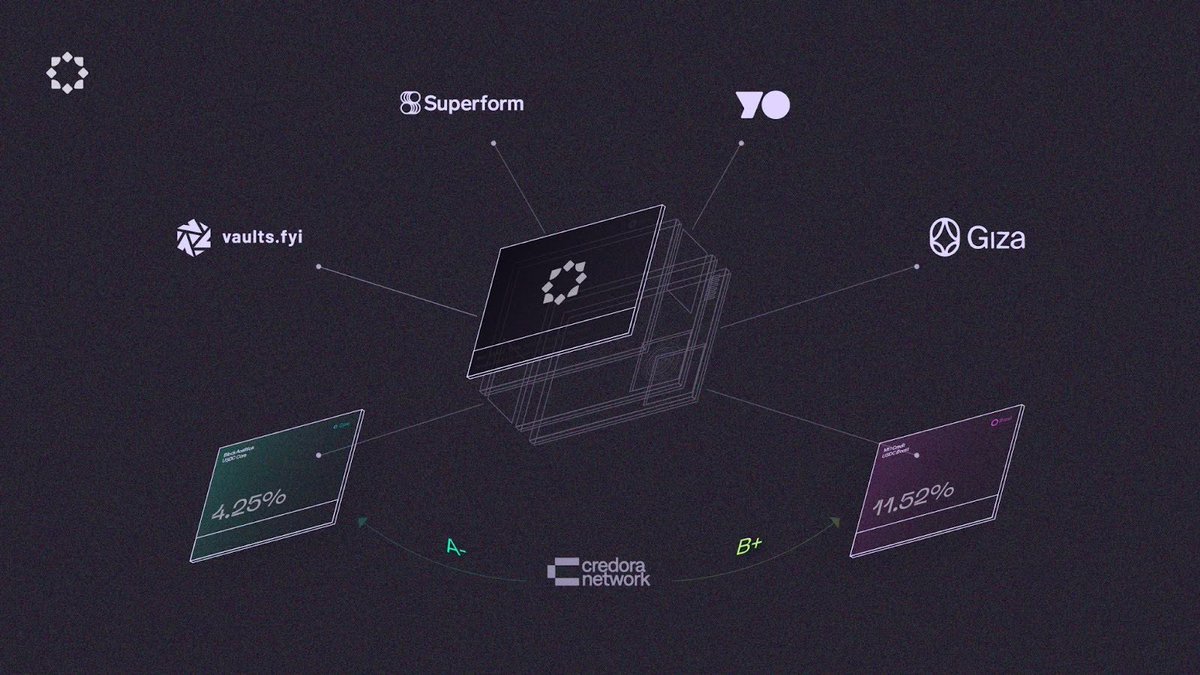

there's a whole ecosystem growing around vaults, but the bottleneck is still upstream

too little clarity around risk, too little control over product construction, and too many vaults that looks the same.

Apr 8

More vaults do not automatically mean better choices.

Better vaults start with better building blocks.

We spoke with @vaultsfyi, @superformxyz, @yield, and @gizatechxyz about what integrators actually need from the next credit engine powering vaults.

1

1

7

522

chavis retweeted

Apr 1

Better vaults start with better market structure.

@Davidareising explains how Lotus enables a spectrum of yield opportunities by pricing credit on connected curves.

The result? Clearer risk, diverse yield, better vaults.

1

8

286

chavis retweeted

Mar 23

Better Vaults need better market structure.

With Resolv, a single issuer-side opsec failure was enough to create losses, illiquidity, or emergency actions across a web of downstream vaults, pools, and credit markets. Last year it was the $93m Stream Finance debacle due to a bad balance sheet.

LPs aren’t being compensated adequately for the opaque risk they’re taking on in many of these assets through diversified vault allocations.

@LotusFi_ doesn’t eliminate collateral risk, but we think our model eliminates much of the incentive to lend against riskier collateral. Lend against blue-chip collaterals like BTC and ETH. Keep liquidity connected. Price credit risk on a curve inside one market.

1

6

20

4,112

you can't help but wonder if the reason you don't see these success stories is that there simply aren't that many people building useful things with AI

Mar 16

Lovable is missing the real growth or “generation influence” outside of the ARR posts they keep sharing and that’s their users.

People actually using Lovable and building companies with it. I mean I don’t even hear about them, not even from Lovable.

Where are the founders who built their first product with Lovable. Where is the person who quit their job after launching something with it.

Where is the team that shipped a startup in two weeks because of Lovable.

Those are the stories people want to see. Lovable is a VC backed company and it seems like they are making good money but the real opportunity is much bigger than posting ARR screenshots.

They could literally create their own version of YC just from people building with their product.

Imagine a cohort of founders launching companies with Lovable. Imagine showing the best products built with it every month. Imagine the stories of people building their first startup using Lovable.

Put those people on billboards.

Put them in ads.

Put them all over social media.

Tell real stories about what people are building.

I love MRR and ARR posts.

But honestly they hit very different when they come from bootstrapped companies.

When a bootstrapped company posts 30k or 100k MRR you know exactly what that means.

Someone sat alone building something.

Someone shipped a product.

Someone convinced real customers to pay.

That revenue is survival.

When a VC backed company posts ARR growth it just doesn’t feel the same.

You raised money to grow.

You have a team, marketing budget, distribution of course the numbers will move.

The more interesting story is not the revenue chart. The real story is the companies being built with your product.

That’s the real influence.

1

4

377