😎always sunny cryptoweather in the caribbean. Alles wat ik tweet zijn slechts mijn gedachten en ideeen. Mijn tweets zijn geen beleggings tips of -voorstellen!

Joined June 2017

- Tweets 12,924

- Following 285

- Followers 1,170

- Likes 2,358

1,024 Photos and videos

2 Dec 2025

so everyone is bearish or afraid to say something else ...... interesting.

i am not bearish atm btw

1

40

cryptocaribbean retweeted

2 Dec 2025

🚨 BREAKING

THE EXACT REASON WHY THE MARKET JUST PUMPED:

WINTERMUTE BOUGHT 8,577 BTC

BINANCE BOUGHT 7,658 BTC

WHALE WALLET BOUGHT 6,610 BTC

COINBASE BOUGHT 5,860 BTC

BITMEX BOUGHT 5,818 BTC

BITFINEX BOUGHT 5,778 BTC

THIS WAS A COORDINATED MANIPULATION!

595

955

6,919

514,618

cryptocaribbean retweeted

4 Nov 2025

BREAKING: Almost every whale just opened longs on BTC & ETH in the past hour 🚨

Millions in new positions. Leverage stacked.

Something BIG is coming...

462

411

3,881

450,306

cryptocaribbean retweeted

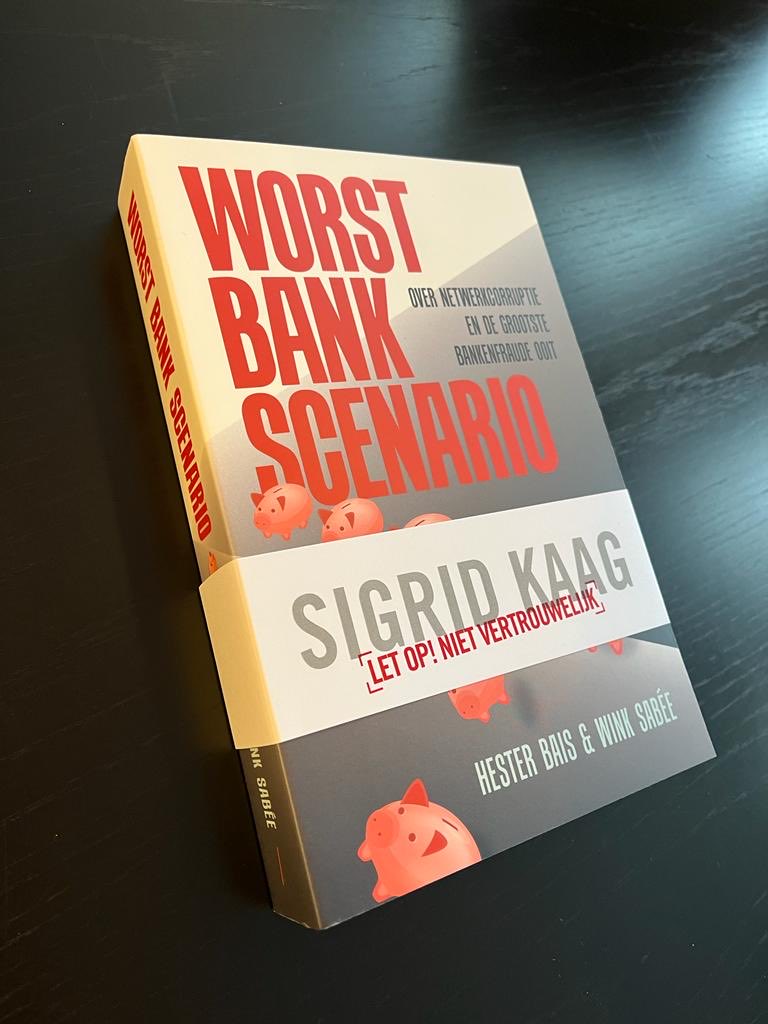

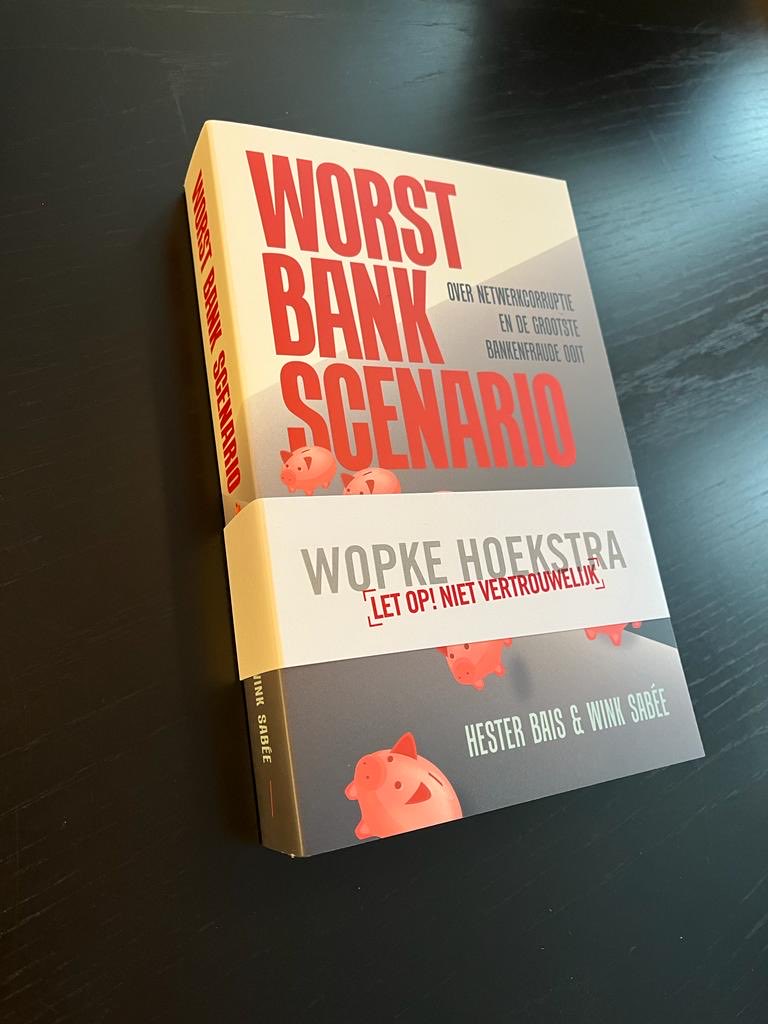

31 Oct 2025

'In 2022 daalde het pensioenvermogen van € 1.917 miljard naar € 1.511 miljard. Deze daling werd veroorzaakt door hoge koersverliezen op obligaties (€ 133 miljard) en op rentederivaten (€ 167 miljard) door de – door de ECB gemanipuleerde – sterk verhoogde rente. Daarnaast daalden ook de aandelen (€ 41 miljard) en beleggingsfondsen (€ 62 miljard) in waarde. [66]

Als gevolg van de liquiditeitstekorten van de banken en de gedaalde rente zijn de pensioendeelnemers daarom sinds de kredietcrisis miljarden aan rendement misgelopen. Bovendien is vanwege het sluiten van OTC-transacties en collateral upgrading het kredietrisico van banken afgewenteld op de pensioenfondsen.'

Fragment uit Worst Bank Scenario

In 2022 werd het Transmissiebeschermingsinstrument door ECB ingevoerd en het Wetsvoorstel toekomst pensioenen ingediend. Ook draaide de DNB de fraude met onderpand terug die de centrale bank vanaf 2018 - na het sluiten van de illegale onderpandcarrousel onder ABP en PFZW - heeft uitgevoerd.

DNB verschoof in 2018 namelijk de datum van waardering van onderpand met één dag zonder toelichting. Deloitte was de accountant. Grapperhaus was toen minister van Justitie en is nu hoofd Juridische Zaken bij Deloitte.

Onderpandbeheer voor CCPs (clearinghuizen) is geen wettelijk mandaat van DNB. Clearinghuizen zoals dat van ABP en LCH SA hebben DNB en dus Nederlands belastinggeld misbruikt voor het uitvoeren van hun eigen agenda. De EU garantieregeling, de onderpandcarrousel van ABP/PFZW en het opkoopprogramma van ECB werden opgetuigd om de enorme onderpandtekorten van OTC derivaten van banken te financieren (in Nederland EUR 200 miljard en in EU meer dan EUR 2000 miljard).

In 2018 werden ook gemanipuleerde rechtsvragen aan de Hoge Raad gesteld door Rechtbank Amsterdam, waardoor sindsdien aangedragen feiten/bewijzen met betrekking tot liquiditeit(sfraude) en verzoeken om getuigenverhoren worden genegeerd. Pieter Omtzigt stelde samen met Eric Ronnes Kamervragen over de enorme balanscorrecties, maar minister Hoekstra verzweeg dat het misbruik van de pensioenpotten de werkelijke oorzaak was.

Inmiddels beschik ik ook over de onderliggende memo van APG aan ABP (met verwijzing naar oa Aegon), de garantieovereenkomst van (bewaarbedrijven van) APG beleggingsfondsen en de statutenwijziging van deze bewaarbedrijven in 2010 en 2016, waardoor ABP gedurende die periode bevoegd werd om de bestuurders van deze bewaarbedrijven van APG te benoemen. Zo werd oa EMIR vrijstelling misbruikt. De hoogte van de garanties werden niet in de jaarrekening van ABP en ABP’s clearinghuis opgenomen.

In 2022 werd NN Investment Partners, de pensioenvermogensbeheerder die in 2014 partner werd van ECB voor de uitvoering van het opkoopprogramma, overgenomen door Goldman Sachs. De onderpandtekorten zijn verschoven naar de UK en de US. Terwijl na deze overname de vrijstelling van EMIR voor pensioenfondsen werd beëindigd, is deze vrijstelling in UK (EMIR-UK) voortgezet.

Collateral is King 👑

13

315

534

35,372

cryptocaribbean retweeted

12 Oct 2025

The Oct 11 Crypto Crash — What Really Happened

TL;DR:

Roughly $60–90M of $USDe was dumped on Binance, along with $wBETH and $BNSOL, exploiting a pricing flaw that valued collateral using Binance’s own order-book data instead of external oracles.

That localized depeg triggered $500M–$1B in forced liquidations, cascaded into $19B globally, and earned the attackers about $192M via $1.1B in BTC/ETH shorts opened on Hyperliquid hours earlier, but minutes before Trump tariff announcement.

It wasn’t a USDe failure!! It was Binance’s design flaw, timed with macro panic (Trump’s tariffs) for cover.

What looked like chaos was actually a coordinated exploitation of Binance’s internal pricing system, amplified by a macro shock and systemic leverage.

1️⃣ The Setup

Binance’s Unified Account let traders use assets like USDe, wBETH, and BNSOL as collateral.

Instead of oracle or redemption prices, Binance valued these using its own spot market - a major vulnerability.

On Oct 6, Binance announced a fix to move to oracle-based pricing, but rollout wasn’t until Oct 14, leaving an 8-day window.

2️⃣ The Exploit

During that window, sophisticated actors manipulated Binance’s order books, dumping ~$60–90M of USDe, driving it to $0.65 on Binance only (still ~$1 elsewhere).

Because the Unified Account marked collateral to internal prices, this instantly wiped margin value and triggered $500M–$1B in forced liquidations.

Then, Trump’s 100% China tariff headline hit, magnifying panic and liquidity stress.

3️⃣ The Profit Engine

The same day, fresh wallets on Hyperliquid opened $1.1B in BTC/ETH shorts, funded by $110M USDC from Arbitrum-linked sources.

As the Binance cascade unfolded, BTC and ETH cratered, those shorts netted $192M in profit before closing out at the bottom.

Timing, precision, and funding paths all suggest coordination.

4️⃣ The Contagion

Binance liquidations dumped BTC/ETH/ALTs into thin books.

Other exchanges mirrored the collapse through cross-market bots.

Market makers hedged across venues were forced to unwind everywhere.

Result: $19B global liquidations, with many alts down 50–70% intraday, all triggered by <$100M of manipulated collateral.

5️⃣ Who’s at fault?

Binance: design flaw delay in oracle rollout = root cause.

Exploiters: executed and timed the manipulation, profited via external shorts.

Ethena (USDe): not at fault - protocol stayed 1:1 collateralized, redemptions normal, peg held everywhere else.

6️⃣ Aftermath

Binance admitted “platform-related issues,” promised compensation for affected margin/futures/loan users, and rolled out minimum price floors oracle integration.

USDe remained operational, and the incident is now a case study in how exchange-side pricing errors can trigger system-wide liquidations.

Bottom line:

A ~$90M dump on Binance and a $1.1B leveraged short elsewhere sparked a $19B bloodbath.

Not a stablecoin failure, but a masterclass in exploiting flawed collateral valuation during peak macro stress.

674

2,104

8,750

2,030,756

cryptocaribbean retweeted

7 Oct 2025

A major milestone for $PAAL as we’re thrilled to announce our expansion to @Solana in collaboration with @chainlink, unlocking a new era of cross-chain AI innovation and growth.

From deploying hundreds of AI agents and chatbots to integrating advanced AI DeFi capabilities, this move opens up new opportunities for holders, deeper utility for $PAAL, and greater flexibility for ecosystem partners.

🌐 Swap on Raydium:

👉 raydium.io/swap/?inputMint=s…

7 Oct 2025

PAAL AI (@PaalMind) is expanding its PAAL token to @solana using Chainlink CCIP.

Already an adopter of the Cross-Chain Token (CCT) standard, PAAL will now be transferable across BNB Chain, Ethereum, and Solana.

Chainlink makes AI smarter.

55

172

821

53,566

cryptocaribbean retweeted

4 Oct 2025

$CELL the quantum narrative is coming, position yourself into a secure blockchain that will easily 100X. Remember AI and AI Agents are nice to have, Quantum level encryption and security are must haves!

2 Oct 2025

Researchers at Harvard built a quantum computer that could run indefinitely.

This might sound "normal," as we're used to using our classical computers for hours a day.

But quantum computers couldn't run for longer than a couple of seconds, if at all—until now.

That's because their qubits (the base unit of a QC—like "bits" in classical computers) lose information REALLY fast due to noise and other external factors that make them unstable, forcing the machines to constantly "restart."

To achieve this breakthrough, the team used techniques that replenish qubits back into the quantum computer as they lose information or get lost—literally escape—overcoming the rate of lost qubits.

In the experiment, the machine ran for two hours straight, and researchers say that, in theory, it could run indefinitely.

"There’s now fundamentally nothing limiting how long our usual atom and quantum computers can run for," said Tout T. Wang, a researcher who works in the lab that designed the machine.

Vladan Vuletić, an MIT physicist that worked in the research alongside Harvard specialists, said that this breakthrough shortens the time frame for building a quantum computer that could run forever in practice, not just theory.

"Before it was believed that this is at least five years away. Now it seems much closer, kind of more on the horizon of two to three years."

3

17

51

1,347

cryptocaribbean retweeted

1 Oct 2025

3

31

127

3,287

cryptocaribbean retweeted

18 Sep 2025

AIOZ Stream Relay: 3 Perspectives on the DePIN Media Infra

Dive into these fresh takes from our team and community, and add yours to the mix.

QRT this post with your thoughts on where DePIN streaming is headed.

Explore how you can build, create, or operate with AIOZ Stream.

38

151

3,631

9 Sep 2025

thats what i mean. Lets do it

8 Sep 2025

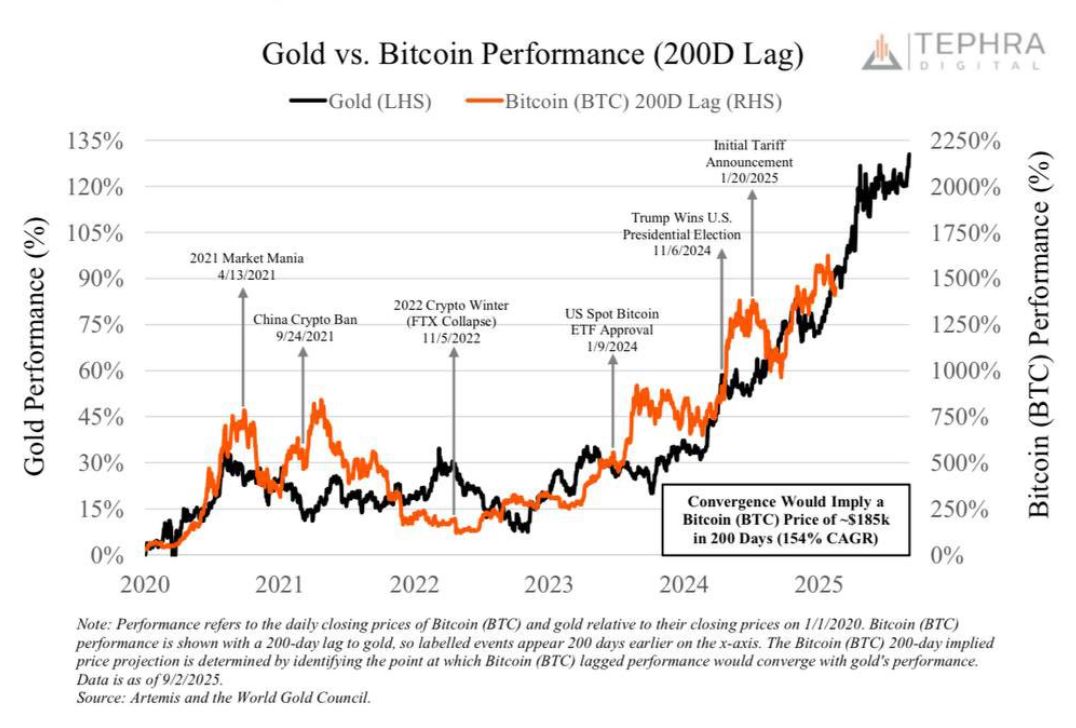

Bitcoin’s gold correlation implies a potential rally toward $167K–$185K in the months ahead. – Tephra Digital 📈

48

9 Sep 2025

$btc again > 113K. Let it be the start to a new ath and surge towards 150-160K in the next 2 months

37

8 Sep 2025

The numbers are correct. Strange we dont see the $btc price go up i.m.o.

7 Sep 2025

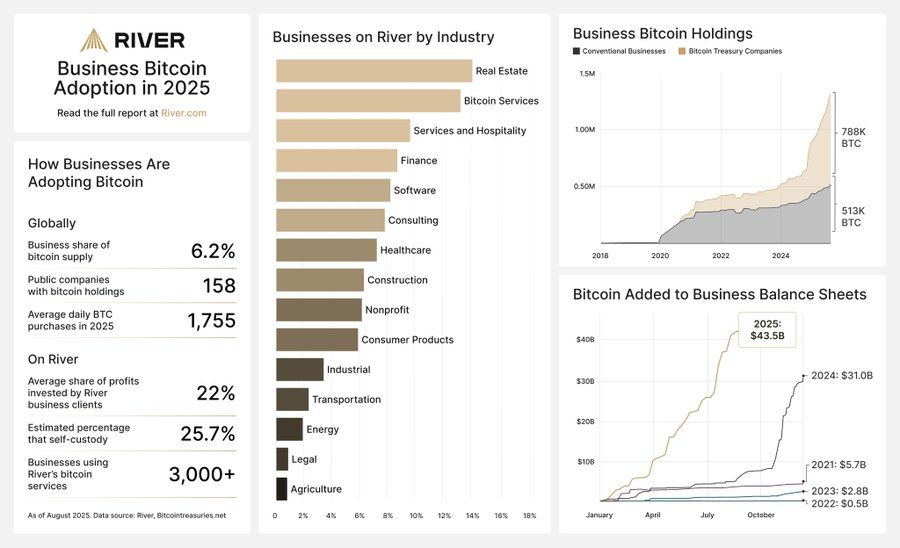

Companies are buying 1,755 BTC per day.

That’s 4x the daily mining issuance of just 450 BTC. 📈

45

cryptocaribbean retweeted

1 Sep 2025

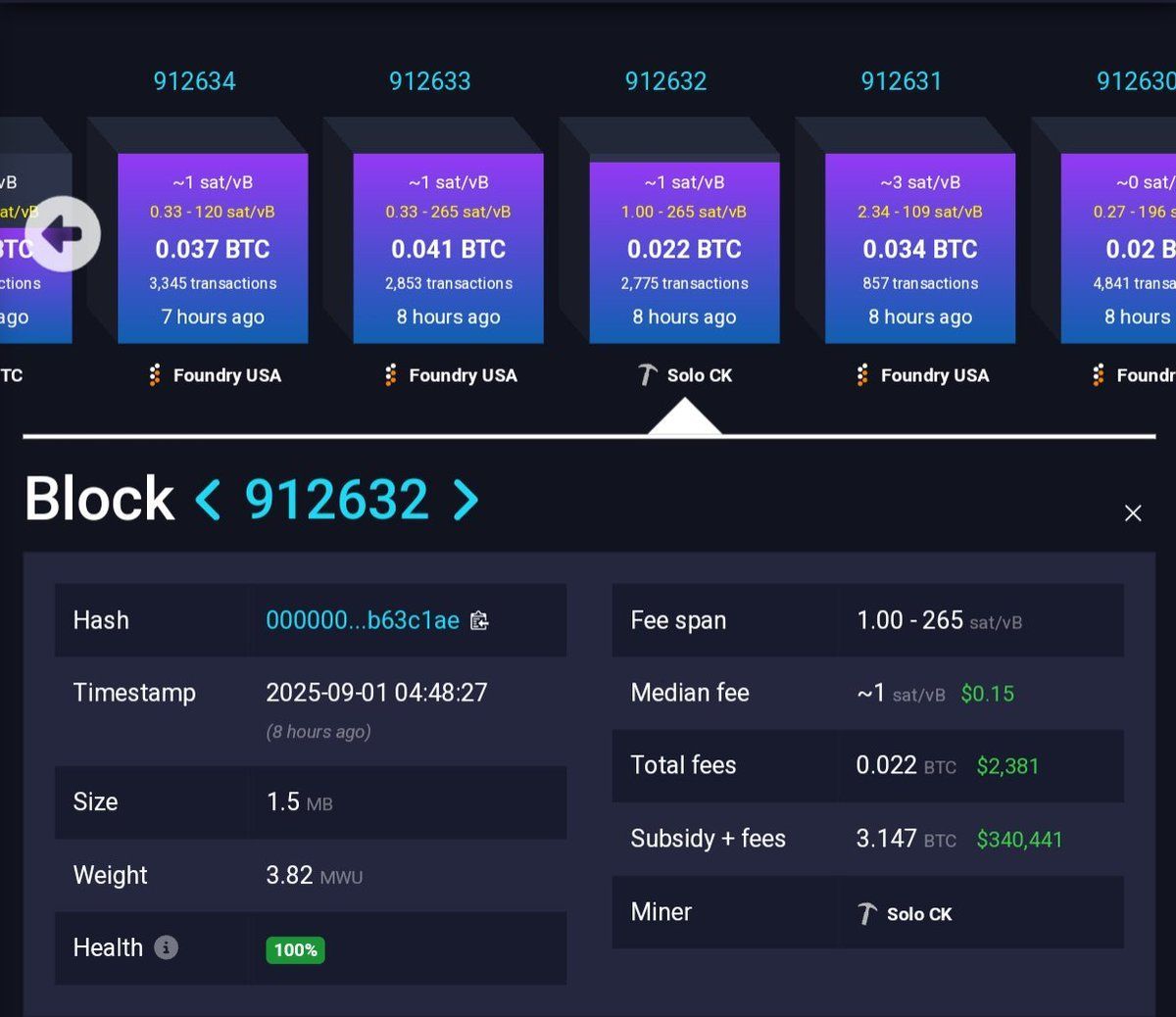

JUST IN: Solo miner mines an entire Bitcoin block worth $340,000.

They won the Bitcoin lottery. 🔥

130

113

1,240

87,288

cryptocaribbean retweeted

31 Aug 2025

Polish CEO Piotr Szczerek (took child’s hat at US Open) & his wife are now viral worldwide.

Instead of apologizing, they threaten lawsuits & call critics poor people without Internet rights.

As a Pole, I despise such behaviour.

To the world listening: that's not how Poles are.

96

61

447

254,453

Als mannen het probleem zijn. Is het dan wel verstandig bootladingen alleenreizende mannen binnen te halen uit landen waar geen posters hangen met #WijEisenDeNachtOp ?

#justasking

153

787

4,050

91,245

27 Aug 2025

saw that before but indeed insane if you place it in a graph. Sol casino is closing

72