442 Photos and videos

Pinned Tweet

Protect your crypto! 🔑

Buy a Ledger through my link and get up to $20 in #BTC.🚀

shop.ledger.com/pages/referr…

1

24

CRYPTOCOINFAN 🛡 📜 retweeted

Access the most liquid crypto options in the U.S. soon, powered by Deribit.

10h

Crypto options are coming to Coinbase later this year.

Giving U.S. users access to the full suite of derivatives.

With our Deribit integration, you’ll be able to access some of the most liquid crypto options in the world.

Alongside deep liquidity for spot and perpetuals.

41

55

442

39,428

CRYPTOCOINFAN 🛡 📜 retweeted

$221 BILLION EMIRATES NDB ANNOUNCES IT WILL ALLOW 10 MILLION CUSTOMERS TO BUY #BITCOIN AND CRYPTO

ONE OF THE LARGEST BANKS IN THE MIDDLE EAST

WORLD'S BIGGEST BANKS ARE RACING TO BTC 🔥

42

158

777

25,606

CRYPTOCOINFAN 🛡 📜 retweeted

Jun 12

🚨BREAKING:

MICHAEL SAYLOR SAYS THE U.S. COULD ELIMINATE ITS ENTIRE NATIONAL DEBT WITH BITCOIN

HE CLAIMS OWNING 4-6 MILLION $BTC COULD GENERATE $50-80 TRILLION IN VALUE FOR AMERICA

SAYLOR BELIEVES THE BIGGEST RISK IS ANOTHER COUNTRY BUYING IT FIRST

6

34

164

8,078

CRYPTOCOINFAN 🛡 📜 retweeted

Jun 9

$LINEADAT has already accumulated enough funds for its first BAG.

The treasury is being funded.

The treasury is accumulating assets.

The mechanism is working exactly as designed.

This is no longer theory. The economy is already operating in real market conditions.

Join us. 🚀

$LINEA @LineaBuild

3

7

24

4,853

CRYPTOCOINFAN 🛡 📜 retweeted

Jun 6

The AI buildout is absorbing capital at historic scale, creating temporary pressure across global markets. That does not weaken Bitcoin. It strengthens the case for scarce, liquid, digital capital. Bitcoin remains the premier asset for the long term. $BTC

1,335

1,714

13,935

1,212,062

CRYPTOCOINFAN 🛡 📜 retweeted

Jun 2

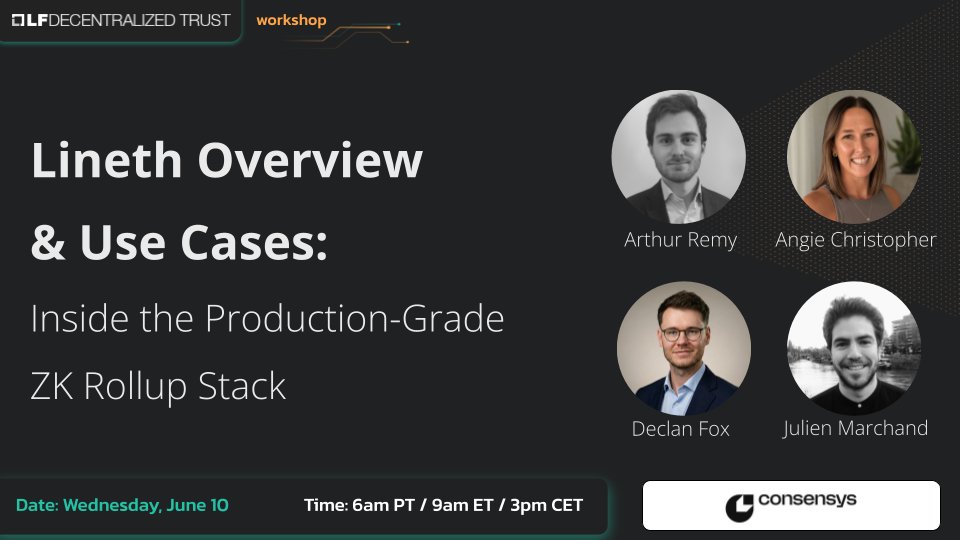

Curious about Lineth?

Join us for an overview and use case session with the team on @lfdecentralized’s Discord.

June 10, 2026: 6am PT / 9am ET / 3pm CET

Register: hubs.la/Q04hh4cS0

22

38

170

25,763

CRYPTOCOINFAN 🛡 📜 retweeted

May 26

🚨 CIRCLE CEO JEREMY ALLAIRE: EVERY MAJOR FINANCIAL INSTITUTION NOW HAS A MANDATE TO IMPLEMENT DIGITAL ASSETS

Not exploring. Not considering. Mandated.

Apr 3

CIRCLE JUST STEPPED INTO BITCOIN 🤯

Circle launched cirBTC, a 1:1 $BTC-backed token designed for DeFi and institutional use.

This puts them directly into the ~$8B wrapped $BTC market, currently dominated by $WBTC. The $USDC issuer isn’t just doing stablecoins anymore -- it’s expanding into #Bitcoin infrastructure.

$BTC isn’t just being held. It’s being pulled deeper into on-chain markets.

9

26

122

9,496

Join me on Kraken Pro and we can both earn rewards. Use the link below or my referral code p8fgfq5t to sign up:

invite.kraken.com/JDNW/hebaq…

1

26

CRYPTOCOINFAN 🛡 📜 retweeted

May 24

If you hold 0.1 Bitcoin:

– Guaranteed top 2.63% globally (21M coins)

– Top 2.13% after subtracting ~4M lost coins

– Only 4.5M addresses hold >0.1 BTC → Top 0.56%

You're ahead of 99.4% of the world.

Let that sink in.

13

38

178

4,393

CRYPTOCOINFAN 🛡 📜 retweeted

May 24

Major areas where the financial system still needs an update:

1. Tokenization of real-world assets - Real estate, stocks, bonds, funds, etc. onchain for instant settlement, fractional ownership & massive distribution.

2. 24/7 Global trading - Pooled global liquidity, every asset, every person, with great leverage and capital efficiency.

3. Next-gen payments - Near-instant, low-cost global transfers using stablecoins, including for Agentic payments.

4. AI-powered risk, credit, compliance, and advice - Better decisions, less fraud, and broader access to capital. Everyone gets access to a great financial advisor.

5. Innovation friendly regulation - Move from one-size-fits-all to risk-based rules that encourage innovation and competition instead of stifling it.

6. Expanded access - Open protocols that reduce middlemen and self-custodial wallets to expand access to everyone with a smartphone.

7. Capital formation - Low cost and turnkey for anyone to raise money for a good idea, increasing the number of startups.

8. Sound money - A refuge from inflation, when discipline is lost in fiat money.

Jobs not done until we get these working for all.

Will require lots of tech innovation and policy work to get there.

701

734

4,629

518,281

CRYPTOCOINFAN 🛡 📜 retweeted

BREAKING: 🇺🇸 THE SEC JUST APPROVED #BITCOIN INDEX OPTIONS ON NASDAQ

WALL STREET NOW HAS OFFICIAL DIRECT ACCESS TO BTC THROUGH U.S. EQUITY MARKETS

WHAT AN ABSOLUTE GAME CHANGER 🚀

72

231

1,052

33,872

1

2

154

Join me on Otomate - Copy trade top Hyperliquid traders on-chain! 🚀

Use my referral link and get 50 bonus points: app.otomate.trade/?ref=5EBWF…

35

CRYPTOCOINFAN 🛡 📜 retweeted

May 7

I spent some time digging into the history of Hyperledger Besu to understand how @Consensys may have monetized it over the past 7-8 years after Besu was moved into open-source / Hyperledger.

Here is what I found.

ConsenSys did not only have Besu core - a free open-source execution client. It also had a commercial version, which was described publicly as a commercial distribution of Hyperledger Besu.

In practice, it was an enterprise package around Besu:

• advanced enterprise features;

• 24/7 production support;

• customized training;

• encryption at rest / RocksDB encryption;

• advanced monitoring;

• event streaming via Kafka / Kinesis;

• group privacy modifications;

• contract permissioning.

It is impossible to know exactly how much ConsenSys earned from this business line, because ConsenSys is a private company and did not publicly disclose separate revenue figures for Besu / PegaSys Plus.

Now let’s move to Lineth / Linea (@LineaBuild).

If we treat Lineth as a kind of “Besu V2”, which is roughly how Lubin seems to position it, then one phrase from the public Linea Stack documentation becomes especially important:

“Reach out to enquire about our rollup-as-a-service or to access our dedicated design team who will configure the stack to your business needs.”

In my view, this phrase gives the clearest indication of ConsenSys’ potential monetization model around Lineth:

• rollup-as-a-service;

• enterprise support;

• stack configuration for specific business needs;

• architecture design;

• integrations;

• support for corporate deployments.

And this is the important point: this does not really look like a direct source of value accrual for the $LINEA token economy.

Most likely, cash flow from these services would go directly to ConsenSys, similar to how enterprise monetization around Besu previously went to ConsenSys / PegaSys, not to any public token.

So the main question becomes:

What real economic value capture models remain specifically for $LINEA?

Based on publicly available information, Lineth can be used to launch several types of networks:

1. L2 Private Validium on Ethereum

2. L2 Public on Ethereum

3. L3 Private Validium on Linea Mainnet

4. L3 Public on Linea Mainnet

In my view, options 1 and 2 do not create direct economic value for $LINEA.

Why?

Because if a company launches a separate L2 based on Lineth and finalizes directly on Ethereum, the economic flow looks roughly like this:

Users pay fees on the corporate L2 -> the L2 operator collects revenue -> the L2 operator pays Ethereum L1 costs for proofs / blobs / settlement -> the remaining surplus belongs to that L2’s own economic design.

In other words, Linea Mainnet may not be involved in this flow at all.

Yes, Lineth as an open-source stack can strengthen the status of Linea / ConsenSys, increase trust in the technology, and attract more enterprise attention. But I do not currently see a direct mechanism that forces such L2s to send surplus fees to buy back / burn $LINEA.

Especially after Lineth was contributed to the Linux Foundation / LF Decentralized Trust, it is hard to imagine ConsenSys being able to require all users of the stack to redirect remaining fees into the $LINEA economy.

❗️But in options 3 and 4, there is already a direct connection to Linea Mainnet.❗️

If a network is launched as an L3 on top of Linea, the economic flow looks like this:

Users pay fees on the L3 -> the L3 operator collects revenue -> the L3 operator pays Linea Mainnet for finalization / commitments / proof-related transactions -> these payments become activity and gas revenue on Linea Mainnet -> after costs, Linea Mainnet surplus goes to 20% ETH burn and 80% LINEA buyback / burn.

This is where real value capture for $LINEA starts to appear.

But there is an important nuance.

Not all fees paid by users inside the L3 will reach the burn mechanism. Only the part that the L3 pays to Linea Mainnet for finalization / commitments / proof-related transactions will reach Linea Mainnet.

So a single L3 may not generate much revenue for Linea Mainnet. But if there are many such L3s, the effect could become meaningful.

Who could potentially need an L3 on top of Linea?

• those who need stronger privacy;

• those who need cheaper finalization because the economics do not work with direct settlement on Ethereum L1;

• banks, fintech companies, payment networks, RWA platforms, and corporate consortia;

• applications that need their own controlled environment, but do not necessarily need maximum L1 finalization for every batch publication.

For example, SWIFT could theoretically choose an L3 model on top of Linea instead of launching a separate L2. But this is not a fact and not insider information, just my own scenario analysis.

To summarize:

L2s built on top of Lineth primarily give Linea status, trust, technology distribution, and enterprise legitimacy. In some cases, they may even become competitors to Linea Mainnet.

But L3s that use Linea Mainnet as their finalization layer can create direct economic value for $LINEA through Linea Mainnet gas revenue and the subsequent ETH / LINEA burn.

So for the $LINEA token, the key question is not simply “how many networks will be built on Lineth”.

The key question is different:

How many of these networks will choose Linea Mainnet as their finalization layer?

In my view, this is what will determine whether Lineth becomes just an enterprise open-source stack for ConsenSys or a real source of economic value for $LINEA.

3

16

366

CRYPTOCOINFAN 🛡 📜 retweeted

Apr 30

JAPAN'S LARGEST EXCHANGE JPX JUST SAID LIVE ON BLOOMBERG IT WILL LAUNCH BITCOIN AND CRYPTO ETFs 🔥

THIS IS MASSIVE

JAPAN IS COMING 🚀

83

396

2,381

144,555

Hej! Dołącz do mnie na platformie Kraken i odblokuj 200 € nagrody kodem q4dbfqs9 lub przez ten link invite.kraken.com/JDNW/l4hm0…

8

CRYPTOCOINFAN 🛡 📜 retweeted

STABLECOIN GIANT TETHER’S CEO SAYS AI AGENTS WILL USE THE #BITCOIN LIGHTNING NETWORK TO TRANSACT ⚡️

HE SAYS AI AGENTS WILL MAKE “TRILLIONS OF PAYMENTS PER DAY”👀

33

66

431

23,449

Exploring the Knidos testnet 🚀

AI agents, on-chain activity, and early ecosystem testing — looks like an interesting place to be before mainnet.

Join here and try it out:

testnet.knidos.xyz/invite?co…

#Knidos #Testnet #AIagents #Crypto #AirdropHunting

18

I joined Knidos testnet and I am exploring autonomous on-chain trading agent.

Join the waitlist now:

testnet.knidos.xyz

#Knidos #Testnet

3