💔delta points🐰

Joined February 2018

- Tweets 2,078

- Following 1,175

- Followers 990

- Likes 6,143

154 Photos and videos

May 21

I believe stablecoins earn institutional trust when redemption is boring by design

I believe in @squidrouter

2

36

dyula retweeted

Apr 10

Under-discussed: tokenized stocks may end up representing a larger market opportunity than stablecoins.

Global equities exceed $130T, vs $20T for USD M2.

If tokenization captures a meaningful share of each, the upside for equity issuers is structurally larger.

7

21

65

12,667

Mar 30

They seem to know something 💫

THE ETHEREUM FOUNDATION IS STAKING ETH

The Ethereum Foundation just staked $46.2M of ETH. This is more ETH than they have EVER staked before.

3

87

The Agentic Commerce Market Map

Mar 10

82 companies have been submitted via x402 and added to agenticpayments.artemisanaly… !!

i built this market map in a day and monetized it instantly.

all without needing a merchant account or payment processor setup. anyone can pay to submit a company and it just works.

right now, our interface for interacting w the web is trending toward walled gardens, with leading AI companies whitelisting the apps and services we're allowed to use.

this works great for the top integrations (e.g., google suite, figma, slack, notion)... but what abt everything else?

the alternative future is an open ecosystem where users can discover/test/access hyper-personalized products created by any human or agent. this long tail of useful-but-tiny services only exists if the barrier to becoming a merchant approaches zero.

that's what crypto primitives like stablecoins, blockchains, wallets, and x402 make possible.

18

22

209

23,282

Mar 1

Banks freeze. Exchanges fail. My Bitcoin stays mine.

Just joined the @xverse Card waitlist. Self-custody meets the real world. ₿ 💳

Get in: xverse.app/card/waitlist

45

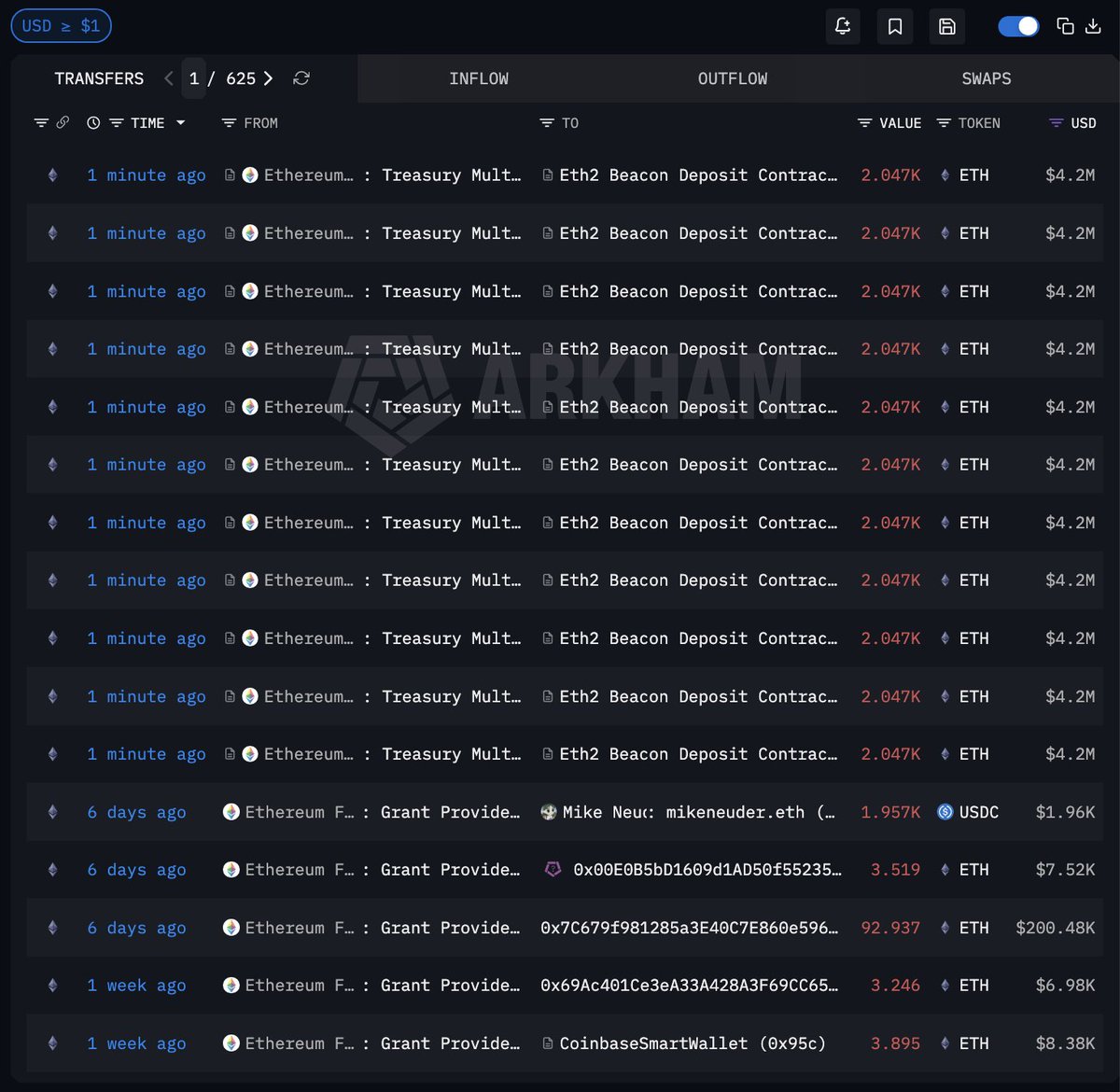

ARKHAM’S MOST UNDERRATED FEATURE

Here’s a feature on Arkham most people don’t know about, but can save you HOURS of research time.

Tag Pages are lists of the largest entities/addresses grouped by theme. Use them to find new entities to track, trace & set alerts on. Here’s how:

10

26

135

19,213

dyula retweeted

Feb 23

85% of all major token launches in 2025 are trading below their launch price.

The median token is down 71% from its TGE. Every single $1 billion FDV launch is in red today.

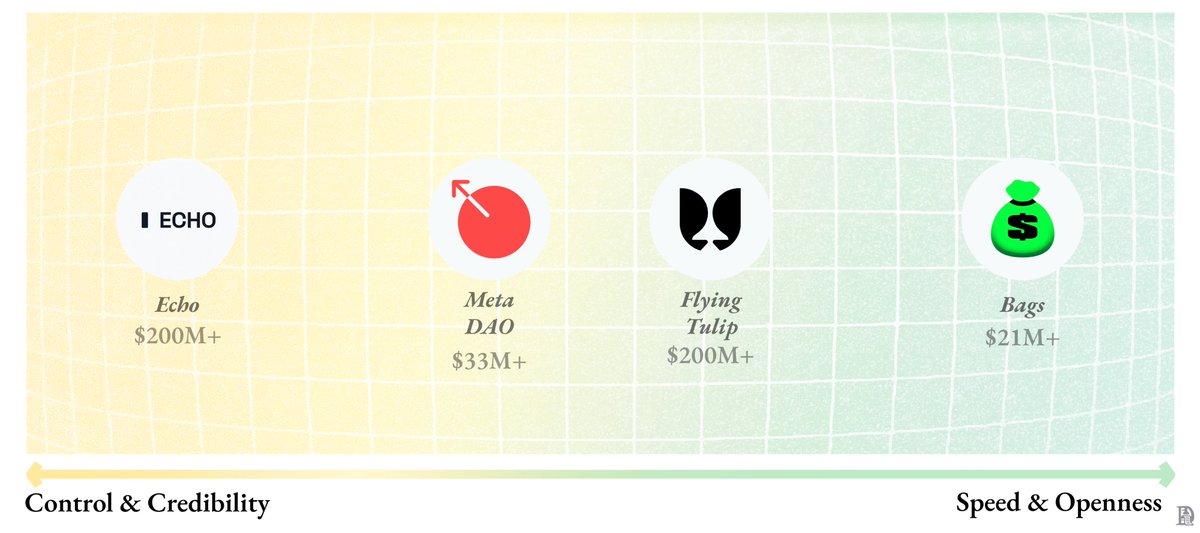

We have been observing how emerging capital formation primitives are tackling the problem. An open internet requires better ways to distribute ownership and coordinate capital. There are four key players, each with distinct approaches to control and openness in today’s market.

1. @echodotxyz

Echo Token launches take place within a regulated, institutionally controlled, and vetted pipeline. Access is gated, compliance is required, and distribution happens through existing infrastructure, rather than permissionless public markets. The upside is credibility and structure. The tradeoff is clear; there is little room to be wrong in public, and failure comes with significant reputational consequences.

2. @MetaDAOProject

MetaDAO focuses on what happens after the capital is raised. It separates the act of committing capital from the act of spending it. The underlying assumption is that raising money is rarely the hard part. The harder problem is ensuring that capital is actually used as intended. Funds committed don’t automatically end up in a founder’s wallet. A futarchy is used to govern how capital flows. This enforces discipline around capital usage, but it does not do well with ambiguity. Early-stage products rarely have clearly defined outcomes upfront, and this structure assumes more certainty than typically exists at that stage.

3. @flyingtulip_

Flying Tulip starts with the problem of irreversible loss. Instead of raising funds and immediately spending them, the capital is parked. Tokens come with a built-in redemption option, allowing holders to always exit at a predefined floor. In simple terms, investors are not forced to rely purely on trust or future execution, and there is a mechanical way to limit downside.

However, this protection comes with constraints. Because capital must remain redeemable, it can’t be deployed freely. Spending must remain conservative, which naturally limits the pace of growth.

4. @BagsApp

Bags removes friction almost entirely, creating a fast and highly permissive version of capital formation. Anyone can launch a token. There is no screening or vetting process. Tokens trade immediately, and the market determines the next steps.

This optimises for speed and access, but it does so by giving up almost everything else. If something doesn’t work, the failure is public and permanent. Capital has no protection. Reputation often has no protection either, and in many cases, it’s simply exploited. Founders still earn fees, but participants and early believers absorb most of the downside.

Asset diversity and the changing nature of tokens require extremely differentiated primitives for capital coordination. There is a reason why the NYSE and Y-Combinator serve different stages of growth in a venture. We are likely to see a similar pattern with on-chain capital coordination primitives.

2

22

21

1,832

dyula retweeted

My predictions for 2026:

The real gold and glory of our generation will be given to a newly emerging kind of person who is truly interested in change and is willing to take more risks with their career betting on technologies whose availability and utility are uncertain.

You need to be clear in yourself to survive the coming period of thought-chaos, because it will make you question your perception, your awareness, your presence... what is natural, what is true, what is real.

People who are distracted now, will be even more distracted later:

Jade Dragon Power Ching Hong Kong Bathouse White Tigress yacht Million Yen Stock Market Pacific Ocean Disappear.

80

78

574

28,029

dyula retweeted

24 Dec 2025

!siht tog eW !lla uoy ot 6202 raeY weN yppaH YREV a dna Merry Christmas !yaw eht lla elgnihC-ahC

185

492

2,409

219,162

dyula retweeted

24 Dec 2025

Cha-Chingle all the way! Merry Christmas and a VERY Happy New Year 2026 to you all! We got this!

2,514

3,080

12,659

4,145,042

22 Dec 2025

I'm eligible for the Espresso airdrop 🥳. Check yours ⬇️ claim.espresso.foundation/sh… via @magna_digital

46

dyula retweeted

18 Dec 2025

We are so back!

The Messari Theses for 2026 is live and available for free.

Jump into the full report now ⬇️

135

228

873

933,465

13 Dec 2025

I've been Making. The. Jump 😌

@jumperapp

Check out my Jumper Wrapped 2025 💜 #jumperwrapped

wrapped.jumper.exchange/2025…

1

41

dyula retweeted

11 Dec 2025

It's time for our annual big ideas.

Here are 17 things that various a16z crypto partners (plus a few guest contributors) are excited about for what’s ahead in 2026.

On topics ranging from agents and AI; stablecoins, tokenization, and finance; privacy and security; to prediction markets, SNARKs, and other applications… to how we’ll build.

Find the full post here: a16zcrypto.com/posts/article…

157

162

895

260,226

dyula retweeted

3 Dec 2025

A new era of Coinbase is beginning.

December 17, 2PM PT, live on 𝕏.

Set a reminder: x.com/i/events/1989118834905…

229

280

1,520

817,008

To be honest, as a simple guy who has nothing to do with VCs or project teams, who has been here since 2018 and has seen a lot, words like the ones here affect me to the core: x.com/hosseeb/status/1988383…

But I will try to be as objective as possible.

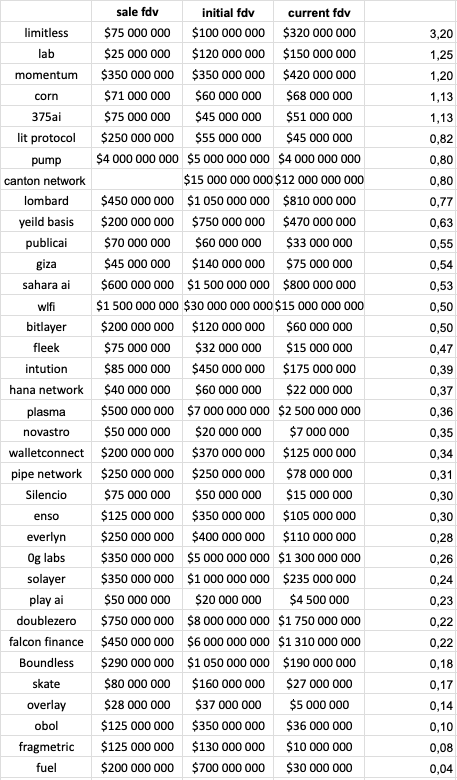

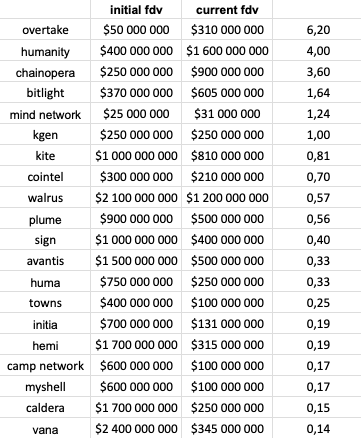

Many have seen these graphs, where the tokens of projects whose teams have conducted airdrops have a perpetually red graph. Before we had enough new data on projects that held a token sale instead of an airdrop, these charts looked impressive and truly convinced us that an airdrop is a problem for a project and brings no practical benefit. But now, it has been almost a year since active token sales began, and we can look at some preliminary results.

First, I would like to explain how the research was conducted.

- All projects conducted their TGE in 2025.

- The projects are divided into two categories: those that had a token sale and those that did not, but had a classic airdrop. It is important to note that some projects, for example, all projects from buildpad, also conducted an airdrop.

- In the "sale" category, I did not include projects that only had a launchpool on an exchange, due to the small supply of tokens being sold.

- The fairness of distribution for some airdrops, such as kgen, is difficult to verify, but I also have no data to suggest that the team distributed tokens to themselves, as was the case with apriori (which I did not include in the selection).

- In most cases, the initial FDV was based on the 5-minute chart and indicates the price at which a retail investor could sell the token. However, the high of the candle is not taken into account; instead, the average price over the specified time period is used. Sometimes, when a project was launched at the beginning of the year, the 1-hour chart was used as the source data.

First, I suggest you take a look at the raw numbers for projects, broken down by various launchpads. Here, in addition to the initial and current FDV, the prices at which the tokens were sold are listed. For retail investors, token sales are generally beneficial. They don't have to think about the criteria the team will use to distribute an airdrop. They are given the terms and they simply buy the token. The last column is the ratio of the current price to the initial price of the token. Many will say, well, that's the market, nothing you can do about it. And they will be right.

Now, let's sort this table from the most successful performance to the worst.

Many evaluate the success of a project based on how much they earned. But I repeat, this is not about retail investors. This is about VCs, who for some reason are trying to prove to us that the entire problem of why project tokens only have a downward movement lies in airdrops. Most of the projects shown here have a clear vertical downward chart. Now let's take a look at how things are with projects that had an airdrop but no token sale.

Doesn't it seem strange to you that out of 36 projects that conducted a token sale, only 5 are trading above the TGE price? 3 of which are relatively small, barely reaching a $150m capitalization, while at the same time, out of 20 projects that conducted an airdrop instead of a token sale, 4 projects are trading above TGE and have a capitalization of more than $300m?

Now, looking at these numbers, tell me: were airdrops the problem?

11 Nov 2025

Late to this, but as a VC, here’s my perspective on airdrop farming:

Farmers are obviously not useful to projects.

@Cobie is right that as a VC, I ignore farming activity. I’m extremely skeptical of easily farmed metrics, and we always dig into the data to try to identify farming. Wherever we see it, we heavily discount it.

Farming is, by definition, people who pretend to use a product and pretend they will be long-term users, in order to get paid via an airdrop.

Let that sink in for a second. Crypto has broken all of our brains on this. If a normal consumer startup paid people to pretend to use their product and pretend to retain, that’d be considered fraud. Airdrops started as an idealistic and egalitarian practice, but the rise of industrial farming has evolved it into something straightforwardly toxic. Farmers try to emulate real users and make it hard for teams (and investors) to identify the difference.

So, no. Farming is obviously bad for startups. If it weren’t bad, farmers wouldn’t try to hide that they're farmers.

But farmers will reply: the value of farming is that farmers pump up metrics of successful projects, and therefore, it’s good for the projects.

This is so wrong it’s hard to even know where to start.

First, if farmers are “pumping up metrics,” who are they pumping them up to? Who is being fooled here by inflated metrics? Is it the VCs? If so, farmers are claiming that founders are conspiring with farmers to dupe their VCs. (And on many heavily farmed projects, VCs are underwater.)

Note: this is incompatible with the theory that VCs are the primary culprit of bad token launches. Either the VCs are dastardly villains conspiring with founders to dump on retail, or they’re stupid fools being duped by founders with farmer-inflated metrics. But it can't be both at the same time.

The other option is that it’s not the VCs who are fooled--VCs see through it--it’s retail who’s being fooled. So maybe farmers are conspiring with founders to dump on retail, and that’s why it’s good for founders. The problem with this theory is that founders don’t get to dump day 1, only farmers do. So by the time the chickens come home to roost, the metrics have already plummeted, the farmers got out by selling their airdrops, and the founder is left holding the bag. Only the farmers profited from retail, not the founder.

But even if we rationally agree with this analysis, to most people, it doesn’t matter. Because we all know that despite this, all good projects get farmed. So if nobody shows up to farm your project, that must imply your project is not good, and therefore you’ll do poorly in the market. Don’t you want to be like all the other good projects? So you need farmers to show up, whether you think they're parasitic or not.

This sounds convincing. But it’s totally wrong, for the age-old reason: correlation is not causation. Yes, good projects get farmed. But the project being good causes the farming, the farming doesn’t cause the project to be good. All big cities have crime, but that doesn’t mean crime is causes cities to get big. The causation is backward. You can have a good project that isn't farmed.

To tell you the truth, I think the actual dumb money here is the exchanges. Exchange listing teams reward farmed metrics more than VCs do. But the market is already correcting on this, and norms are changing. It’s just exchanges tend to be the last to notice, as they’re furthest back in the capital stack.

Now all that being said, there’s nothing morally wrong with airdrop farming. No more than there being anything wrong with running MEV bots or sniping token launches. The game is the game. As long as you’re following the rules, all is fair. So there's no reason to look down on airdrop farmers. They're strategically trying to make money with the resources they have.

But are farmers providing value to founders?

No, obviously not.

(Caveat: “Linear” farming is an exception--if you’re being paid to provide liquidity or an insurance backstop, or some other clear assumption of risk, I’d call that more classic liquidity mining, which is totally valuable. Or if you’re being paid to market make or provide tight spreads, that’s also valuable. This kind of farming is pay-for-performance that contributes to a product moat. But that’s not like the vibes based “pretend to be a user and touch everything" type farming I’m talking about above, which tends to be more common for L1/L2s or for consumer products.)

30

46

195

7,163

dyula retweeted

12 Nov 2025

In our annual guide, we examine the important themes, trends and events that will shape the coming year. Explore The World Ahead 2026 econ.st/3JwJPKx

Illustration: Andrew Rae

367

1,311

3,546

3,776,180