Joined September 2021

- Tweets 3,776

- Following 276

- Followers 978

- Likes 10,886

749 Photos and videos

Mar 30

tl;dr for those who aren't connoisseurs of concepts like Ontology as I and Gabriel are

## intro

- the "security token industry" has built compliance infrastructure assuming tokens are securities and compliance can/should be smart-contract-rules based

- this is in direct conflict with the core value prop of blockchains: not "same intermediaries, on the blockchain w" but *disintermediation*

- starting from this incorrect assumption about what tokens actually are has lead to a compliance theater cul-de-sac that just adds tech complexity on top (doesn't reduce compliance cost)

## the ontological confusion

- Gabriel outlines 6 relationships tokens can have to securities:

1. chain-as-ledger

2. certificate tokens

3. instruction tokens

4. control agreement tokens

5. synthetic tokens

6. souvenir tokens

- #1 chain-as-ledger means the token is actually the security because the blockchain is the ledger the company uses to track ownership; #3/4 instruction or control tokens direct (with varying levels of legal force) the issuer to update their offchain ownership ledger based on token movement/holdership; #6 souvenirs have 0 legal enforcement structure, may vaguely match an offchain ledger but there's no legal binding that creates consequence for dislocation

- Gabriel argues only does #1 actually make tokens a security, none of the current chains/ERC implementations do so, and because of this they essentially only add complexity and compliance theater vs create meaningful economic value

## the PEB Report and the Token Instruction Model

- the Permanent Editorial Board for the Uniform Commercial Code - the body responsible for monitoring and interpreting the UCC - has been circulating a draft report on the tokenization of securities transfers that primarily analyzes models #3 and 4 above, but also notes #1 (chain as ledger) is an explorable design space

- the PEB report explicitly suggests tokens are not securities but Controllable Electronic Record under UCC Article 12 whose transfer of control constitutes an "instruction" to the issuer directing that the transfer of the uncertificated security be registered

- under this model token transfers are messages to the issuer to "register this person as the new owner" BUT the issuer is not obligated to comply if certain conditions are not met; Gabriel argues this means the smart contract compliance logic is essentially theater because the issuer is still legally required to evaluate the transfer and determine whether to update it's offchain register or not

## why hard coded transfer compliance makes no sense for instruction tokens

- when a token is simply an instruction and not a security, the entire compliance question remains where it has been with offchain securities: with the transfer agents/issuers who decide whether or not to honor the notification; these actors already have very sophisticated systems for tracking ownership and informing decision makers via richer context than onchain data provides, which renders smart contract logic redundant/thinly additive

- Gabriel argues onchain compliance pipelines are worse than current offline implementations for three reasons:

1. onchain pipelines misidentify who bears compliance obligations; securities can trade peer to peer relatively freely, it's issuers, broker-dealers, transfer agents, investment advisors, etc who are subject to regulation; these intermediaries *can not* delegate their legal obligation to infrastructure (smart contract automations) and incorporating controls to attempt to do as much destroy the "marketability" of tokens (composability in defi; if you can't trust you can liquidate a token because the issuer might freeze the txn you can't accept it as collateral)

2. onchain compliance pipelines presume transfer control is the primary modality of securities regulation when it is in fact offering/holding period/resale restrictions for private market securities and broker-dealer/transfer agent/investment advisor activity in the case of public securities; some of the related activity could be monitored/controlled in smart contract functions but current implementations do not do this

3. onchain compliance pipelines are inflexible in a way that is incompatible with how compliance actually works; securities compliance is intentionally risk-based, judgement-intensive, and governed by principles not bright lines because bright-line hard-coded rules are inherently gameable; by hardcoding the compliance at the transfer layer protocols give the false impression that compliance is being handled when it is only being gestured at, which comes at the cost of gas expenses, composability constraints, a false sense of security, and the embedding of today's compliance assumptions into immutable/hard to upgrade code

## the permissioned-ledger variant

- instead of wrapping public-chain tokens in compliance logic, Canton replaces the public chain entirely with a permissioned ledger where unauthorized txns can't even be constructed; Gabriel argues Reg SCI / PFMI / CFTC compliance don't require that unauthorized txns can't be attempted, they just can't be processed (by compliance departments who aren't disintermediated by any blockchain), so Canton trades away public chain competitive advantage while overfitting compliance needs

- in doing this, he argues Canton is essentially isomorphic to existing post-trade infrastructure (DTCC/Euroclear/Clearstream), essentially adding a DAML layer on top of their COBOL, as it still requires all the same institutions, same gated membership, same bilateral opacity as the existing system

- Canton's sub-transaction privacy also kills a concrete legal benefit to transparent blockchains: DGCL §§ 219/220 grant stockholders the right to inspect the stock ledger, and a public-chain architecture makes that automatic; to solve for privacy near-term: issuer-controlled view keys encrypting PII while the ledger structure remains publicly verifiable; longer-term: per-issuer ZK rollups (ZKsync's Prividium, already live with Deutsche Bank) settling to a public chain, gives you transparent settlement encrypted state

## the common thread

- the common failure across ERC-XXXX and Securitize/Canton tokenization standards is that all treated intermediation as a design constraint rather than the problem to be solved; every architectural choice assumes the existing intermediary chain persists and blockchains just add slight efficiency; this produced the false premises: if intermediaries are given, the token doesn't need to be constitutive, compliance can be encoded in the token, and the chain doesn't need to be public

- by reducing the chain to a notification layer for offchain intermediaries (instruction/souvenir/control agreement tokens), these protocols threw away the one structural advantage of public blockchains: settlement finality; when onchain state is a suggestion not a fact, or even where state is authoritative there are god-mode admin powers, tokens become unusable as a DeFi primitive which is why tokenized securities have generated near-zero meaningful ecosystem activity

- the "progressive decentralization" defense (ship instruction tokens now, make the chain constitutive later) has a poor track record: centralized dependencies become structurally embedded, the offchain DB becomes the system of record, admin keys become operationally necessary, compliance modules become contractual obligations to institutional partners, and migration cost exceeds maintenance cost

## what it means to really put securities onchain

- Gabriel argues onchain compliance only does real work when the token is the security, which is why MetaLeX CyberCorps build from DGCL outward; bylaws designate the onchain system as the stock ledger under § 224, each Stock Ledger Entry Token (ERC-721) carries the full legal metadata (holder, class/series, share count, § 202 restrictions, Rule 144 dates, officer auths), and the smart contract's rejection of a noncompliant transfer is the issuer's refusal to register; ownership mutates via metadata updates not wallet transfers so a stolen NFT doesn't change who owns shares

- entry/scrip separation solves defi composability: ERC-721 entry tokens hold the authoritative legal record issuer governance powers, ERC-20 cyberSCRIPs mint against them for fungible liquidity with irreversible admin renunciation capability; lenders get real security interest with no override risk vs. ERC-3643 where agent freeze makes collateral unusable; the scrip layer accommodates multiple legal theories per issuer while chain-as-ledger stays intact underneath

## conclusion

- the corrective isn't a better compliance module but a different question: "what legal architecture makes onchain state authoritative?"; Gabriel argues the answer starts from corporate law: bylaws designating the onchain system as the record, tokens carrying their own legal metadata, compliance doing structural work on the actual stock ledger not theater on a notification channel; a token that doesn't know what it is can't be made compliant by infrastructure that doesn't know what it's protecting

- his argument revolves around what a token actually is as a matter of law: get it right and compliance follows naturally, the blockchain does real work, the intermediary chain shortens; get it wrong and no compliance engineering meaningfully closes the gap

- the stakes are whether tokenization delivers its promise: self-custodied legally authoritative ownership, peer-to-peer settlement, open stock ledgers, programmable full-lifecycle infrastructure; that requires chain-as-ledger (tokens = legal record, chain = ledger, governing instruments fusing both); instruction tokens can't get there regardless of wrapper sophistication

1

11

1,610

Mar 27

nice breakdown of the heterogeneity in "Private Credit Onchain"

re: my post the other day about the sources of wealth at the root of yield

lets trace back top line APY -> source of yield -> fundamental wealth generation

and see if crypto's real advantages = real SAM

Zeus presents 6 different examples of "Machines" behind onchain yield:

1. @maplefinance, direct lender - pools onchain capital, originates lends, collects borrower repayment and delivers back to onchain LPs

2. @centrifuge, @HastraFi capital bridge - routes onchain capital to existing Real World credit needs; he particularly calls out working capital loans HELOCs that earn/provide value via maturity transformation

3. @Securitize, @stokr_io wrapper - tokenizing existing funds/notes that offer yield; here the onchain actor (securitize) is essentially completely hands off of yield generation and adds very little to the risk layering

4. @paretocredit, programmable credit infrastructure/fund of funds - pareto blends two different concepts, one the more classical fintech play enabling third parties to build programmable onchain credit facilities, with a fund layer on top in USP

5. @onrefinance, reinsurance - as Zeus mentions, different in kind to "credit" though like credit it is a source of yield rooted in risk transfer

in my previous post linked in the thread we looked at the sources of wealth generation in the Austrian sense, then the broad categories of financial services that can be provided to support wealth creation to generate "yield"

this gives us a sense of the roots of value creation and how blockchains/defi might meaningfully create net-new or better-in-kind opportunities

we outlined categorical sources of yield:

1. Time value (capital now > later)

2. Roundaboutness Productivity (% share of wealth created by facilitating expansion of existing wealth production)

3. Entrepreneurial Productivity (% share of wealth created by facilitating the discovery of new sources of wealth production)

4. Risk Bearing (absorbing *calculable* variance for others)

5. Liquidity Provision (facilitating immediacy/optionality for others by standing ready to transact)

6. Rent (payment for access granting to scarce factors)

we then examined potential real competitive advantages across these factors blockchains/defi may have, and saw:

2 3 - insofar as technical access to opportunity blocks capital allocation, permissionless defi globally accessible blockchains may genuinely facilitate cheaper/more effective flows to wealth generation

4 - well designed smart contract systems may reduce counterparty, duration, etc risks enough to better facilitate risk transfers across interested parties

5 - perps, AMMs, flash loans are real financial innovations, still testing in prod whether they're value add at scale/for sophisticated actors

6 - globally accessible, permissionless, automated financial infrastructure likely meaningfully reduces network Rent costs (even as we admit there's more to Visa/Mastercard/Swift than simple information sending)

now that we've refreshed the context - do we see anything interesting in a durable sense with our "private credit" yield examples?

direct lender - blends 2, 4; broader capital access better quality/cost risk management through transparency/automation might create genuinely new yield that's delivered to LPs

capital bridge - in the described sense (working capital/HELOC), 2 4 6

wrapper - 5, if we just isolate us treasuries for now (simplicity differentiation from the other examples); broader capital pool access makes existing financial product markets more liquid; perhaps blockchain infra also adds 6 (rent reduction) and for some actors 4 (broader access hedges than local markets provide), though the "yield" from this value add isn't delivered to the RWA holder

programmable credit infrastructure - 6, maybe 2; whether insourced our outsourced a well functioning defi infra should be lower cost than existing alternatives and that may be passed on via yield

fund of funds - in the described sense ("private credit"), 2

reinsurance - if the insurance contracts are moved onchain, with transparent and automated payout mechanisms, 4 (reduces the cost of bearing the risk via better modeling); for now likely just 2 until a lot of legal and BD work is done to bring a meaningful amount of the operational details onchain

thinking across these examples I can see space where the net new elements of crypto can add real world value

though at this level of analysis the question is how much of that value creation will remain endogenous to company equity holders vs be passed on to those allocating onchain capital to these products

1

1

116

Mar 27

Mar 25

nice overview of where the yield is coming from via analysis of one of defi's largest

in exploring the future of onchain yield, I like the first principles approach - what is the essence of "yield" - so we don't get stuck just assuming what will be = more of what is

how do we do this?

I come from bitcoin, so Austrian theory is the base, from which we can parse 2 sources of "wealth creation"

1. Roundaboutness (Böhm-Bawerk) - provide capital to build out a known value-producing process (eg we know people want cars and how to build them; fund a factory expanding it's production capability and you're participating in wealth creation)

2. Entrepreneurial profit (Mises) - successfully addressing misallocations of capital by acting on subjective judgment where no calculable probability exists aka bearing uncertainty to make something new and valuable (eg no one knows the how and how much of ecommerce in 1994, Jeff and his backers took that problem on)

From these sources of new wealth, we can frame "yield" as compensation for services you provide to the structures of production and the exchange of valuable goods and capital.

1. Time value - even in a world of perfect certainty, people want things now more than later and are willing to pay for this

2. Roundaboutness Productivity - looks most like yield on a commercial loan, your portion of the surplus generated by enabling production expansion by providing up front capital

3. Entrepreneurial Productivity - looks like VC investment, your portion of the surplus generated by bearing a share of uncertainty by funding entrepreneurs in their exploration of closing allocation mismatches/creating new goods and services

4. Risk Bearing - absorbing *calculable* variance for others ie Insurance

5. Liquidity Provision - facilitating immediacy/optionality by standing ready to transact when others want to; Market Making

6. Rent - payment for access granting to scarce factors

We can then use these to see how they underpin a few different TradFi Products/yield sources:

Bond Yield = 1 4

Equity Returns = 2 3

Options Premiums = 4 5

So where do blockchains/defi add Real World Value that might indicate future sources of onchain yield?

Perhaps 2 3 - "Internet Capital Markets" of the VC investment and Private Credit kind; the trick of this is that the limit of wealth creation in Roundaboutness and Entrepreneurial Productivity is fundamentally one of information about what is actually productive and who has good entrepreneurial judgement.

There are some structural bottlenecks - part of why Brazilian grain producers pay 20% on working capital loans is terrible infrastructure for accessing funding

But that's a trust and politics question as much as it is a payment/repayment rails one

Most early stage ventures fail as a nature of the game; there is some differential between good founders idea and inability to get VCs to take their call

whether that's a meaningful margin or not is *uncertain*

Risk Bearing - perhaps Smart Contract functionality and blockchain data availability can meaningfully reduce cost/improve quality of underwriting but that is the key, the payout mechanisms aren't the hard problem here though that's the most obvious solution blockchain provides atm

Liquidity Provision - AMMs, perps, flash loans are innovative. Maybe Pendle Yield splitting/Boros approach to IRS are as well; is there any more math to apply here to create genuine innovation?

Rent - ETH as the new Visa, Solana as the new Nasdaq, whether this value add can justify a network token price or not is still up for debate but building more open globally accessible settlement infrastructure remains a core, somewhat tangible value add from blockchains

the two things I'm watching as catalysts for a next wave of experimentation in onchain yield

1. Tradfi on chain - both capital and operational infrastructure; what happens when TF money demand for permissionless, fixed rate, undersecured lending enables billions in net new global loan origination (likely a few million in honest entrepreneurs worldwide who are able to create wealth if they could secure a few thousand dollars in capital at sub 10% rates)

2. Some sort of US safe harbor rules or other legal infrastructure that enable token utility and equity property experimentation that's currently no-go'd by Foundation lawyers; maybe buyback and burn isn't so dumb if that's deemed an allowable mechanism for value accrual without being treated as a must-register equity

37

Mar 26

stellar has been doing a v nice job building out Institutional

cool to see them making moves when ct had written them off, lessons in there

also this very week austin's at war with zach arguing about circle's ability to - on ethereum - freeze funds

x.com/austincampbell/status/…

1

3

267

Mar 26

nice overview of Mastercard's to date crypto related movement

a few thoughts, some recurring some from the article:

* the article does the crypto native meme, focusing on the "stablecoin transfers are cheaper than 2-3%" narrative that doesn't fit the real defensible core of Visa/Mastercard

while also including the lede: Visa/Mastercard don't take 2-3% that's the total cost stack (including issuer/acquirer bank fees)

their take is closer to ~0.13-0.15% and that's for doing a ton of value add with fraud management, guarantees, etc

The article does hint at the actual forward advantage for these networks - "Value Added Services"

They just need to get into crypto payment service provision quickly and smoothly enough to maintain their corporate expertise and big data advantages

And or move further out on the regulatory moat stack - ie buy BVNK and acquire licensing to do cross boarder payments in 130 countries

* ai agents will also want fraud management, guarantees etc. and have selection pressures driving them to demand scale that humans alone wouldn't

"smart contracts fix this" = maybe, but also a persistent CT handwave meme

as we've seen recently with Resolv and every other crypto exploit, the transparent rules of operation in blockchains composability have thus far created a ton of opportunity for adversarial actors to study and exploit the systems

if we view blockchains/crypto on the whole as one large exploration of the farthest reaches of Kerckhoffs' principle - that cryptosystems should be secure even if everything about them is known except the key - then we keep moving in a direction where we assume eventually we'll discover the ruleset that enables the cost asymmetry of gaming blockchains/smart contracts at deca trillion scale is in favor of defense vs offense (aka blockchains/SCs can be trusted rails for the global economy)

this feels like it's still at the very least an ongoing multi year project with real uncertainty that may not *resolve* in crypto's favor, not something we can just assume will get Figure'd out in a codeislaw manner vs one that still requires the opacity and judgement of human intervention

* the article does hedge this to a degree, but $33T in stablecoin volume in 2025 is CT bullposting when talking about payments - the Visa Onchain Analytics . com dashboard isolates "Retail Sized Transaction Volume" at $69.72B last year

that's only txns <$250 and includes cex deposit/withdrawal and defi activity so not a perfect 1:1 for "payments" volume but still tells a much different growth/current state story

1

3

246

Mar 25

nice overview of where the yield is coming from via analysis of one of defi's largest

in exploring the future of onchain yield, I like the first principles approach - what is the essence of "yield" - so we don't get stuck just assuming what will be = more of what is

how do we do this?

I come from bitcoin, so Austrian theory is the base, from which we can parse 2 sources of "wealth creation"

1. Roundaboutness (Böhm-Bawerk) - provide capital to build out a known value-producing process (eg we know people want cars and how to build them; fund a factory expanding it's production capability and you're participating in wealth creation)

2. Entrepreneurial profit (Mises) - successfully addressing misallocations of capital by acting on subjective judgment where no calculable probability exists aka bearing uncertainty to make something new and valuable (eg no one knows the how and how much of ecommerce in 1994, Jeff and his backers took that problem on)

From these sources of new wealth, we can frame "yield" as compensation for services you provide to the structures of production and the exchange of valuable goods and capital.

1. Time value - even in a world of perfect certainty, people want things now more than later and are willing to pay for this

2. Roundaboutness Productivity - looks most like yield on a commercial loan, your portion of the surplus generated by enabling production expansion by providing up front capital

3. Entrepreneurial Productivity - looks like VC investment, your portion of the surplus generated by bearing a share of uncertainty by funding entrepreneurs in their exploration of closing allocation mismatches/creating new goods and services

4. Risk Bearing - absorbing *calculable* variance for others ie Insurance

5. Liquidity Provision - facilitating immediacy/optionality by standing ready to transact when others want to; Market Making

6. Rent - payment for access granting to scarce factors

We can then use these to see how they underpin a few different TradFi Products/yield sources:

Bond Yield = 1 4

Equity Returns = 2 3

Options Premiums = 4 5

So where do blockchains/defi add Real World Value that might indicate future sources of onchain yield?

Perhaps 2 3 - "Internet Capital Markets" of the VC investment and Private Credit kind; the trick of this is that the limit of wealth creation in Roundaboutness and Entrepreneurial Productivity is fundamentally one of information about what is actually productive and who has good entrepreneurial judgement.

There are some structural bottlenecks - part of why Brazilian grain producers pay 20% on working capital loans is terrible infrastructure for accessing funding

But that's a trust and politics question as much as it is a payment/repayment rails one

Most early stage ventures fail as a nature of the game; there is some differential between good founders idea and inability to get VCs to take their call

whether that's a meaningful margin or not is *uncertain*

Risk Bearing - perhaps Smart Contract functionality and blockchain data availability can meaningfully reduce cost/improve quality of underwriting but that is the key, the payout mechanisms aren't the hard problem here though that's the most obvious solution blockchain provides atm

Liquidity Provision - AMMs, perps, flash loans are innovative. Maybe Pendle Yield splitting/Boros approach to IRS are as well; is there any more math to apply here to create genuine innovation?

Rent - ETH as the new Visa, Solana as the new Nasdaq, whether this value add can justify a network token price or not is still up for debate but building more open globally accessible settlement infrastructure remains a core, somewhat tangible value add from blockchains

the two things I'm watching as catalysts for a next wave of experimentation in onchain yield

1. Tradfi on chain - both capital and operational infrastructure; what happens when TF money demand for permissionless, fixed rate, undersecured lending enables billions in net new global loan origination (likely a few million in honest entrepreneurs worldwide who are able to create wealth if they could secure a few thousand dollars in capital at sub 10% rates)

2. Some sort of US safe harbor rules or other legal infrastructure that enable token utility and equity property experimentation that's currently no-go'd by Foundation lawyers; maybe buyback and burn isn't so dumb if that's deemed an allowable mechanism for value accrual without being treated as a must-register equity

4

446

Mar 24

why hasn't this been done yet?

re: Institutional = behavior to model, not simply a capital acquisition target

very cool how anastasiia takes the tradfi CLO/Rating Agency parallel, identifies where the analogy falls apart for Defi in a manner that indicates "testable predictions and measurable parameters"

work like this is how we enable crypto to bring the best of it's unique qualities while maturing through adoption of what's already working in the rest of the world

"The beauty of every high class TradFi model is that it was built to formalise a phenomenon that kept destroying capital until someone built the measurement language to locate it."

@antoniogm complained later in the day yesterday:

"Crypto is going to find out the hard way that it's horribly behind when it comes to risk modeling (I'm a former credit quant...the field is behind what the state of the art was 20 years ago).

It'll learn one blow-up at a time.

Want to make a fortune in defi? Create a dashboard that shows DV01 (to offchain rate moves), JTD (pivoted by underlying asset), correlation delta (for correlation across assets)..."

fair. also, humans repeatedly demonstrate bias towards loss-reactive learning rather than prevention or gain potential exploration (outcome/near miss bias, prospect theory)

the losses will continue until Institutional Behavior improves

I think anastasiia is right to claim Defi is at the inflection point, now, where this can happen

Easy money for retail brought easy money for organized hedge-fund-class operators, loads of stress testing and the easy to exploit opportunities have been captured/mitigated

a protocol operator I spoke with recently said:

"most of the 'institutions' are still figuring out how to engage with on-chain markets and what it means across disparate internal stakeholders.

The newness and lack of clear objectives create ambiguity that kill forward momentum, leaving it to the internal R&D team to figure things out without a clear mandate."

the opportunity in helping those R&D teams figure things out well enough to convince the mandate makers to deploy is close enough CT can smell it

curious to see whether that insustry-wide opportunity can inspire an ISDA/SWIFT/USB/Linux style industry-wide org to develop

or whether a risk curator, data company, chain foundation, defi project will be able to win alone with a proprietary framework

1

114

Mar 23

The exploits will continue as the market matures

Risk curators are some of the clearest actors sitting at the intersection of Institutional = Tradfi and Institutional = behavior patterns under capital-at-scale constraints

Outsized risk/reward opportunities are signals there's value surface area to explore, but trillion dollar asset managers aren't interested when the risk is liquidity getting locked on an asset whose price has collapsed 75%

The asymmetric upside of learning to navigate perils like this is attractive to some actors, though

5-6 years ago, the upside was so quick (days/weeks) and so asymmetric (5-10x) with so many opportunities (dozens of coins/NFTs/yield farms) that the slightly above average retail participant could throw darts and come out ahead

now as @WazzCrypto pointed out in his recent post about "safe" defi yields being lower than IB's rfr, for retail participants it's been nearly all risk and no upside since better capitalized participants have begun operating, and token buy pressure has collapsed the clear upside opportunity for the defi everyman

so for now the game has shifted to those who have/or can attract 8 figure capital pools and make enough from 2/20 to continue on that basis alone, or leverage access gained from that activity to accrue alpha/private market equity access to preserve asymmetric upside

this is a stabilizing force that can enable more capital coming onchain even if it doesn't "democratize generational wealth" for solo participants playing part time at home directly

That stability can create the conditions that enable another wave of that opportunity - Wall Street likes it, Tech likes it, lobby to pass something like a CLARITY act and enable another generation of experimentation onchain

I like what @StreetFDN and @lex_node are working on in equity x token mechanics and legal structures for trust minimization as non-legislative routes that can enable experimentation

the exploits will continue, the market is maturing

Mar 22

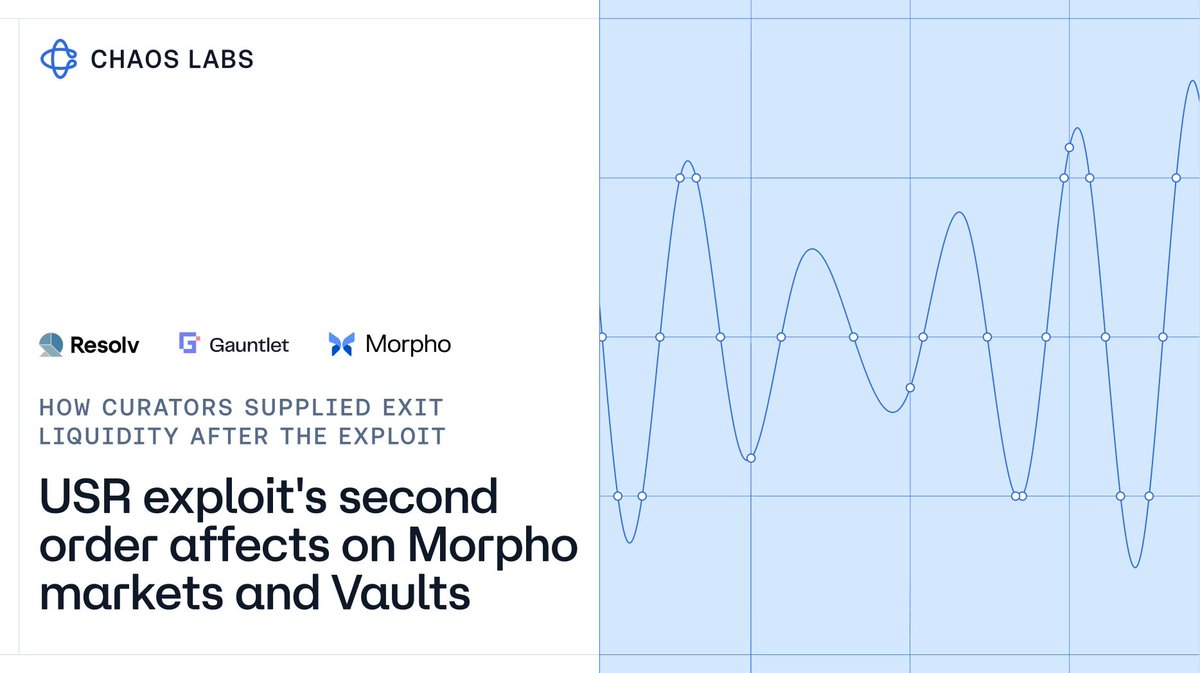

1/ Millions in bad debt, at the time of writing, were created across Gauntlet's Morpho vaults from the Resolv USR exploit.

Almost all of it was supplied ** after ** the exploit.

So why would curators supply millions in USDC to a broken market?

Let’s dive in.

1

147

cryptofreedman retweeted

Mar 3

30

16

140

35,088

Feb 25

have been thinking about this for a while Dante wrote it so he gets the QT

Visa/Mastercard aren't just "slow legacy tech owned by rent seekers" to simply be disintermediated by megaTPS chains and ERC-20s

they bear and mitigate risk that's part of the txn fee

Feb 24

Everyone saying stablecoins magically solve agentic commerce should slow down and read this.

There are two big things people are missing.

1. Card networks are not just “payment rails.”

You cannot replace Visa, Mastercard, and AmEx with “just send stablecoins.”

Visa, Mastercard, and American Express do far more than move money between banks.

They make it possible to transact almost anywhere on earth while solving for:

-Risk (fraud, chargebacks, disputes, etc)

-Security/authentication

-Global acceptance/distribution

Name someone building with agents who does not have a credit card. Distribution matters.

The current x402-style stablecoin stack does not replicate this.

Wallet → wallet sounds clean, but in reality, direct stablecoin transfers introduce real problems at scale:

-Who eats fraud?

-Who arbitrates disputes?

-Who underwrites failed delivery?

-Who manages compliance across jurisdictions?

Card networks have spent 50 years and billions of dollars building these mechanisms. It is boring, operational monotany, but its absolutely mission critical.

If stablecoins are going to power agentic commerce, the industry has to rebuild all these layers (Not just the settlement layer).

2. Micropayment economics are being oversimplified

People imagine it works like this:

Agent A wallet → Agent B wallet.

That is not how it works in practice.

There is almost always a facilitator in the middle handling gas abstraction, routing, pricing, compliance, liquidity, and sometimes credit.

If this market matures, there will be more intermediaries, not fewer. Orchestrators. Risk engines. Liquidity providers. Identity layers.

Each one needs to get paid.

Micropayments have razor thin margins. When you stack multiple service providers in the middle, those margins compress fast.

Stablecoins are more efficient than legacy systems. That is true. But efficiency does not eliminate cost. It just shifts where the cost sits.

Stablecoins are a powerful primitive. They are not a finished payment network.

Agentic commerce will not be won by whoever settles the fastest. It will be won by whoever can combine:

-Settlement

-Risk management

-Compliance

-Distribution

-Sustainable unit economics

Until we solve the unsexy parts, stablecoins are an ingredient - not the full stack.

Great piece by @Trace_Cohen

1

157

cryptofreedman retweeted

Feb 14

Recently I have been starting to worry about the state of prediction markets, in their current form. They have achieved a certain level of success: market volume is high enough to make meaningful bets and have a full-time job as a trader, and they often prove useful as a supplement to other forms of news media. But also, they seem to be over-converging to an unhealthy product market fit: embracing short-term cryptocurrency price bets, sports betting, and other similar things that have dopamine value but not any kind of long-term fulfillment or societal information value. My guess is that teams feel motivated to capitulate to these things because they bring in large revenue during a bear market where people are desperate - an understandable motive, but one that leads to corposlop.

I have been thinking about how we can help get prediction markets out of this rut. My current view is that we should try harder to push them into a totally different use case: hedging, in a very generalized sense (TLDR: we're gonna replace fiat currency)

Prediction markets have two types of actors: (i) "smart traders" who provide information to the market, and earn money, and necessarily (ii) some kind of actor who loses money.

But who would be willing to lose money and keep coming back? There are basically three answers to this question:

1. "Naive traders": people with dumb opinions who bet on totally wrong things

2. "Info buyers": people who set up money-losing automated market makers, to motivate people to trade on markets to help the info buyer learn information they do not know.

3. "Hedgers": people who are -EV in a linear sense, but who use the market as insurance, reducing their risk.

(1) is where we are today. IMO there is nothing fundamentally morally wrong with taking money from people with dumb opinions. But there still is something fundamentally "cursed" about relying on this too much. It gives the platform the incentive to seek out traders with dumb opinions, and create a public brand and community that encourages dumb opinions to get more people to come in. This is the slide to corposlop.

(2) has always been the idealistic hope of people like Robin Hanson. However, info buying has a public goods problem: you pay for the info, but everyone in the world gets it, including those who don't pay. There are limited cases where it makes sense for one org to pay (esp. decision markets), but even there, it seems likely that the market volumes achieved with that strategy will not be too high.

This gets us to (3). Suppose that you have shares in a biotech company. It's public knowledge that the Purple Party is better for biotech than the Yellow Party. So if you buy a prediction market share betting that the Yellow Party will win the next election, on average, you are reducing your risk.

Mathematical example: suppose that if Purple wins, the share price will be a dice roll between [80...120], and if Yellow wins, it's between [60...100]. If you make a size $10 bet that Yellow will win, your earnings become equivalent to a dice roll between [70...110] in both cases. Taking a logarithmic model of utility, this risk reduction is worth $0.58.

Now, let's get to a more fascinating example. What do people who want stablecoins ultimately want? They want price stability. They have some future expenses in mind, and they want a guarantee that will be able to pay those expenses. But if crypto grows on top of USD-backed stablecoins, crypto is ultimately not truly decentralized. Furthermore, different people have different types of expenses. There has been lots of thinking about making an "ideal stablecoin" that is based on some decentralized global price index, but what if the real solution is to go a step further, and get rid of the concept of currency altogether?

Here's the idea. You have price indices on all major categories of goods and services that people buy (treating physical goods/services in different regions as different categories), and prediction markets on each category. Each user (individual or business) has a local LLM that understands that user's expenses, and offers the user a personalized basket of prediction market shares, representing "N days of that user's expected future expenses".

Now, we do not need fiat currency at all! People can hold stocks, ETH, or whatever else to grow wealth, and personalized prediction market shares when they want stability.

Both of these examples require prediction markets denominated in an asset people want to hold, whether interest-bearing fiat, wrapped stocks, or ETH. Non-interest-bearing fiat has too-high opportunity cost, that overwhelms the hedging value. But if we can make it work, it's much more sustainable than the status quo, because both sides of the equation are likely to be long-term happy with the product that they are buying, and very large volumes of sophisticated capital will be willing to participate.

Build the next generation of finance, not corposlop.

925

689

4,940

1,008,803

cryptofreedman retweeted

Feb 6

387

532

3,573

1,153,575

8 Dec 2025

prediction market = knowable, privately held information can be expressed in price (will the US invade Venezuela in 2026)

gambling = unknowable, betting on odds (will football player score xyz points next game)

3

179

The End of the Free Money Era in Crypto

The crypto market didn’t implode in a single moment. There was no spectacular collapse. It just quietly started bleeding out.

Two major shifts reshaped the entire landscape.

First came the political realignment. Trump’s return didn’t just shift the headlines, it fundamentally changed how capital flows. The liquidity that once poured into crypto got rerouted, redirected toward interests that now hold the keys to monetary policy. A manipulated market loses its appeal, especially when it becomes clear the casino is rigged.

Then AI stole the narrative. The smartest money in the world doesn’t announce its exit. It just rotates. And rotate it did. The capital that once inflated JPEGs and yield farms is now fueling data centers, model weights, and infrastructure with measurable traction.

Capital flows to where things are actually getting built. In 2025, that stopped being crypto.

Not a Collapse. A Controlled Deflation.

What we’re seeing isn’t a crash. It’s not a blowup. It’s not Terra or FTX. It’s something quieter and more permanent.

This is a slow leak. The air is coming out of the balloon, and the room is getting eerily quiet. The structure is still intact, but the speculative energy has vanished.

This is what maturity looks like. The circus leaves town, the lights go off, and only the ones with real conviction stay behind to sweep the floors.

Consolidation Is the Next Era

The age of explosive expansion is over. For years, crypto grew by forking itself into a million variants, each one slightly more degenerate than the last.

That playbook doesn’t work anymore.

Now we’re entering the era of consolidation. Projects will disappear. Teams will merge. Entire categories will get wiped off the map.

Layoffs are already hitting high-profile teams. Many of the names you’ve grown familiar with won’t survive the year. Not because they’re scams, but because they simply don’t matter anymore.

The market is cleaning house. It’s long overdue.

Adapt or Get Deleted

This is the cycle where all the excuses stop working.

No one cares about your airdrop anymore. VC backing doesn’t guarantee relevance. Community is just another buzzword if your product doesn’t work.

From here on out, survival depends on three things. You need actual traction. You need a functioning business model. And you need to solve a real problem.

If you don’t have those things, you’re already dead. The market just hasn’t priced it in yet.

The Problem With Crypto’s Inner Circle

Go to any conference and you’ll start to notice a pattern. It’s the same 200 people, speaking on the same panels, doing business with the same insiders.

This isn’t an ecosystem. It’s a clique.

They fund each other. They promote each other. They create closed loops of capital and influence that reinforce their own relevance.

But these loops are starting to break. In a post-bubble world, insulation becomes fragility. These networks of mutual back-patting lack urgency. They lack feedback. And they’ve never had to compete with anyone serious.

That’s about to change. Web2 operators are coming. They understand execution. They know how to build businesses with real users and real revenue. They don’t need to play the crypto social game because they’ve already played the real one, and won.

Crypto-Native Isn’t Enough Anymore

There’s a dangerous assumption in this space that being crypto-native means being ready.

It doesn’t.

Many of these teams have only ever operated in a world with free money, subsidized growth, and infinite second chances. They don’t know how to survive without constant inflows. They’ve never had to deal with competition or scarcity.

That illusion is ending. Quickly.

Having a token doesn’t make you a business. Having a DAO doesn’t make you decentralized. And having a runway doesn’t mean you’re building something that deserves to exist.

The Window Is Open

This is the part of the cycle where the next giants quietly emerge.

You won’t hear about them on podcasts. They won’t be trending on Crypto Twitter. They’ll be building.

The smartest money in every cycle looks boring at first. It looks undervalued. It looks slow.

But if you pay attention, the signs are there. Teams that keep shipping. Founders that say less and do more. Protocols that create value and don’t beg for engagement.

This is the moment to pay attention. This is where asymmetric bets start to appear. And this is the part most people miss because they’re still waiting for a pump.

Conclusion

Crypto didn’t die. It just lost its storyline.

The bubble didn’t pop. The narrative rotated. The tourists left. The VCs stopped pretending.

What remains is the real game. No more hopium. No more ponzinomics. Just a brutally competitive landscape where the only metric that matters is survival.

Most people won’t make it because they’re still trying to replay 2021. But for those who adapt, and actually build something useful, this could be the best cycle yet.

Not because it will be easy. But because it will be earned.

25

7

86

3,552

28 Nov 2025

Devcon bump bby

1

2

147

27 Nov 2025

1. get experience with connections working a job that gives you exposure

2. Open an advisory firm, be very reasonable with your retainers (all cash no % tokens)

3. Grow experience connections even further

4. when you actually know what you're doing, create a proper fund, invest in advisory projects you think have solid RR

Project flow = you get perspective that can be genuinely valuable to individual project teams who will largely be one and done with this work (can critically fail don't have time/access to mitigate that risk even if you're very smart)

The advisory is your investment deal flow generator mechanism to dd beyond what most VCs will be able to do

13 Nov 2025

1

8

182

1/ On Losing Faith

Is it over?

Was it all a fever dream?

Have we run out of steam?

Is it time to pivot to AI for real this time?

2/ Everything is dead?

BTC: DAT premiums down, nobody cares

ETH: Stablecoin

Alts: Crushed

NFTs: Right click saved

Meme coins: As expected tbh

Zcash: Pumping! which ofc means "cycle is over"

3/ This is the worst cryptotwitter timeline I have ever seen relative to the environment.

Nobody is attacking us, USA is being reasonable and rational, no CEX has run away with our money, and yet, dead, dead, dead.

No narrative, no spark, nothing.

4/ Why?

I read the timeline and it tells me:

a/"nobody owns BTC" (odd, I mean someone has to own BTC, there is a ton of BTC)

and

b/ "the gamblers have liquidated themselves (again)" - true, but it was always like this

5/ This TL feels different. This does not feel like

"fuck I got liquidated", it feels like malaise, tiredness.

Like boredom, to be honest.

I know you think it is the price action but the price action is obviously downstream from psychology.

6/ I have a different view of what is going on.

I think almost everyone forgot what matters, chased after things that did not matter and, we are in the process of discovering they don't matter.

7/ What matters? Only decentralization, only permissionlessness. Nothing else matters at all.

Everything else about crypto is WORSE than a centralized database and always will be because that is how computers work.

8/ In my view, basically everyone "major" except vitalik has strayed from the light on this.

Let's start with Team BTC which USED to be very interested in how to build a network that become nation-state resistant.

This was the BTC of Antonopoulos, of Lopp

9/ We are 5 years into the BTC of Saylor and that BTC is 100% about driving price action.

It is about driving flows to BTC, about getting fully integrated with the USA financial system.

10/ It sounds nice, it sounds better than the system beating us with a big stick, but the net effect is that more and more BTC ends up in Coinbase Custody in New York State

Nothing wrong with that, but none of that BTC is nation-state resistant.

It is 100% non-resistant to the US government specifically.

11/ The problem with this is that with permissionlessness off the table, the only thing left to drive purchases of BTC is FOMO.

"there are only 21M, they are going to run out, you need to buy some before others do and it goes exponential"

12/ I mean, maybe that is true.

I am not making price predictions, I still own BTC and always will I think.

But it is cringe, and it is wrong.

13/ You can think about this by taking it to the extreme case and trying to understand which of the two scenarios adds value to the world.

14/

Scenario A: Blackrock owns all 21M BTC, everyone on planet earth owns shares in the Blackrock ETF and Brian Armstrong is in charge of making sure we don't lose Our Precious

Scenario B: Everyone on earth has their own BTC wallet and BTC is distributed in several billion places around the world and it is literally impossible for any government to stop BTC

15/ In Scenario A, BTC is a complete and utter failure. It is just a pet rock. Yes it is "rare" but it is also "100% seize-able by the USA government"

At which point, it might as well be an IOU from the USA government that it pinky-swears is rare

16/ "but it is not like this because other nation-states are accumulating and game theory blah blah blah"

No my brothers and sisters.

The exact scenario where your BTC get seized is a) centralized and b) hyperbitcoinization

Maybe the Strategic Bitcoin Reserve is happening and it is your ETF and $STRATEGY (TM) capital stack all along (thank you for your contribution to our national security)

17/ To be clear, nobody is seizing your BTC (let alone your ETH) now because it is not important enough yet.

But, if it was, I dunno, I would not trust those centralized vehicles.

CEO, Board, shareholders, SEC, US government, state government, custody firm, their regulators all have an angle of attack on a DAT.

18/ If USA seizes BTC, other countries won't save you:

EU: "Thank god our dreams have come true, we can ban it also"

UAE: "grumble grumble, but fine we will go along"

China: "ban. unban. ban. unban. anyway so long as currency is not free-floating, BTC won't be free here"

Russia: "someone falls out of a window"

19/ Of course, BTC in ETFs is by no means the worst of it. The "crypto's main use is a casino" crowd is the worst.

This is not a zero-sum game, it is a negative sum game because it is rigged.

20/ "what about the JPGs huh?" -> I still love them.

The best ones are the best tokens in the world by far, rare, suffused with meaning, with no external dependencies and great to hold on-chain.

And beyond the art JPGs, I think that NFTs can do many more things, but this is on me to "show, not tell"

21/ I want to circle back to BTC because it is the easiest to reason about.

When people explained to me time and time again that it was a ponzi, I had a simple explanation of why it is not.

21/ BTC lets you do some things better than the existing system. "be sovereign over your money" or "send money to anyone on the planet within minutes" or "maintain an insurance policy against the existing financial system"

22/ I could not tell you how much value this had, but I knew it was not zero.

In fact, the value went up the more people used it, the bigger the network was, the more people you could transact with, the more resilient it was to government censorship.

These are the economics of a network system, not of a ponzi.

23/ If you take this away, if you stop building a network but instead just, at the extreme, just sell everyone shares of the ETF, well there is no network, there is no incremental network value being generated by the next buyer.

24/ In this model, BTC becomes more ponzi-like.

If a new participant does not make the network stronger by joining, they are not adding value, therefore there is a fixed pie and it is just value transfer to an existing holder.

25/ Again, take it to the extreme other direction -> assume we managed to move the whole economy to decentralized rails.

I think that world would be better, it would make better decisions, it would take advantage of the wisdom of crowds, there would be more transparency, less rent-seeking and the aggregate value of the world goes up because it is more productive.

Some % of the improved value of the world will get captured by the early participants to the network (which is normal and fair) but some % will be captured by everyone (as a late participant or consumer).

26/ But if we don't make the world better, if the world is exactly what it is, but also we play with a pet rock, this will not happen and, well, eventually playing with pet rocks gets very boring

27/ So what to do?

The same things you always should do:

a/ push yourself, and by extension, the world an inch, a foot, a mile down the pathway of decentralization.

many ways to do this, it is a journey, start today.

b/ remember, you, yes, you in the mirror have no business trading perps or day-trading stupid coins.

you are bad at it and your future self will be mad at your current self.

28/ If you must do it, carve out a budget and test how great you are across the cycle with your budget (1%, 5%, 10%, 20% of your portfolio, not all of it)

I am of course a dinosaur, but my total portfolio % of "putting money into stupid coins I have been FOMOed into it" is less than 1%. It has gone about as well as you might expect.

29/ Other than that, own some BTC, some ETH, some NFTs (good ones, that you like) in a self-custodial wallet, a small number of your favorite alts if you must.

And keep your job. Earn money, don't try to be a pro crypto trader, this is an imaginary job that only cobie and like 5 other people are qualified for.

I have always worked, every single day of my adult life. You should too.

30/ Crypto is a bad way to get rich quick, but a decent way to get rich slowly. In any case, you should have some stake in the decentralized world, in the digital world.

31/ I think in the end, "it" will be OK but "it" it not everything, it is not most things. As it always was, most coins will go to zero, most NFTs will go to zero. These are the rules of the game.

32/ Most of you are young. You have time, you have time into the ASI world, you have the greatest gift and wealth of all. You will be ok.

33/ Don't mope. It does not help anything. If you are bummed out, sad about your outcomes, there is only one sure thing that helps.

Get back to working.

34/ Even if you are young, life is short, your life is the important thing, money is just a game, just a tool, just an information system.

Don't anchor to your wealth, don't anchor to your ATH, it is not real, my ATH wealth has gone down 90% multiple times. Note it and just keep going.

If you are healthy, in a decent country, in a half-decent economic situation, you are better off than almost anyone who has ever lived

35/ If you have an opinion (even a dumb one) about Monad or Grifters, you are in the 0.001% most forward thinking people in the world.

Did you make a "mistake"?

Who cares, everyone makes mistakes - keep going, keep trying, keep making mistakes, eventually you will find your way, you will get a win.

This is how it goes.

36/ use a hardware wallet and even better a SAFE

37/ and to close again with the most important thing. decentralization is the only thing that matters.

if you go in that direction, if we go in that direction, in the end, it will be ok.

i have no doubt about this, i have never had any doubts about this, it matters so much more than you think it does.

/the end

437

514

2,774

553,578

Saylor is a government proxy company.

The United States protects its empire through institutions most people never think about. Treasury is the command center. The Federal Reserve is the engine room. OFAC and FinCEN are the enforcement spine. Together they operate like a financial intelligence agency.

Basically it’s an “Economic Defense Department”.

No press conferences.

Pure control. Shadows.

Bitcoin enters. Not a replacement for fiat. A new reserve collateral that absorbs volatility and legitimizes the debt. USA has no other options.

BTC is a pressure valve. A balance sheet amplifier. A way to run deficits without destroying trust. The government cannot buy it openly. A sovereign nation cannot accumulate a volatile asset on the front page of a newspaper. That is not how U.S. operates. That is not how a reserve currency adapts. Accumulation must be invisible. It must move through proxies. It must move through public entities. It must move through corporate vessels that can absorb dilution and attention. That’s saylor.

This is where MicroStrategy appears. Not as a tech firm. Not as a software company. As a proxy. As a vessel. As a strategic actor in a much larger monetary shift. Issuing more shares. Taking on unsecured debt. Converting every liability into harder collateral. Scaling a balance sheet with no political blowback. That is how a sovereign accumulation campaign looks in the modern world. Loud on the surface. Quiet in intent. A public crusade masking a state-level transition. A single corporate figure acting as a lightning rod so the government does not have to. That is why the optics matter. That is why the narrative matters. That is why the evangelism matters. Satoshi built the tool. Anonymous. Untouchable. Outside the reach of every institution. Saylor built the optics. Visible. Loud. Inside the financial system where it can legitimize itself.

This is not coincidence. This is architecture. Look at it all.

Miners inside America. ETFs approved onshore. Hashpower consolidated domestically. A compute backbone built through industrial miners. A liquidity on-ramp run by BlackRock. A balance sheet proxy run by MicroStrategy.

This is how a sovereign currency evolves without admitting it is evolving. This is how the next reserve collateral rises without ceremony. Quiet. Structured. Strategic.

“Slowly then all at once”

The Hash Dollar.

Satoshi isn’t CIA/NSA

But.

Saylor is definitely running a Bitcoin strategic reserve for the United States government.

-941

How does a sovereign nation accumulate bitcoin? You have a publically traded entity do it. Then have the guy go around like a lunatic telling people to buy it. Our entire monetary system is built on optics and trust. They financially destroyed the hunt brothers. Why? Bitcoin becomes the release valve, governments can’t change its rules the same way they could with COMEX silver. This why BTC miners will be inside America. It’s all the same game.

24

18

355

65,033

cryptofreedman retweeted

21 Nov 2025

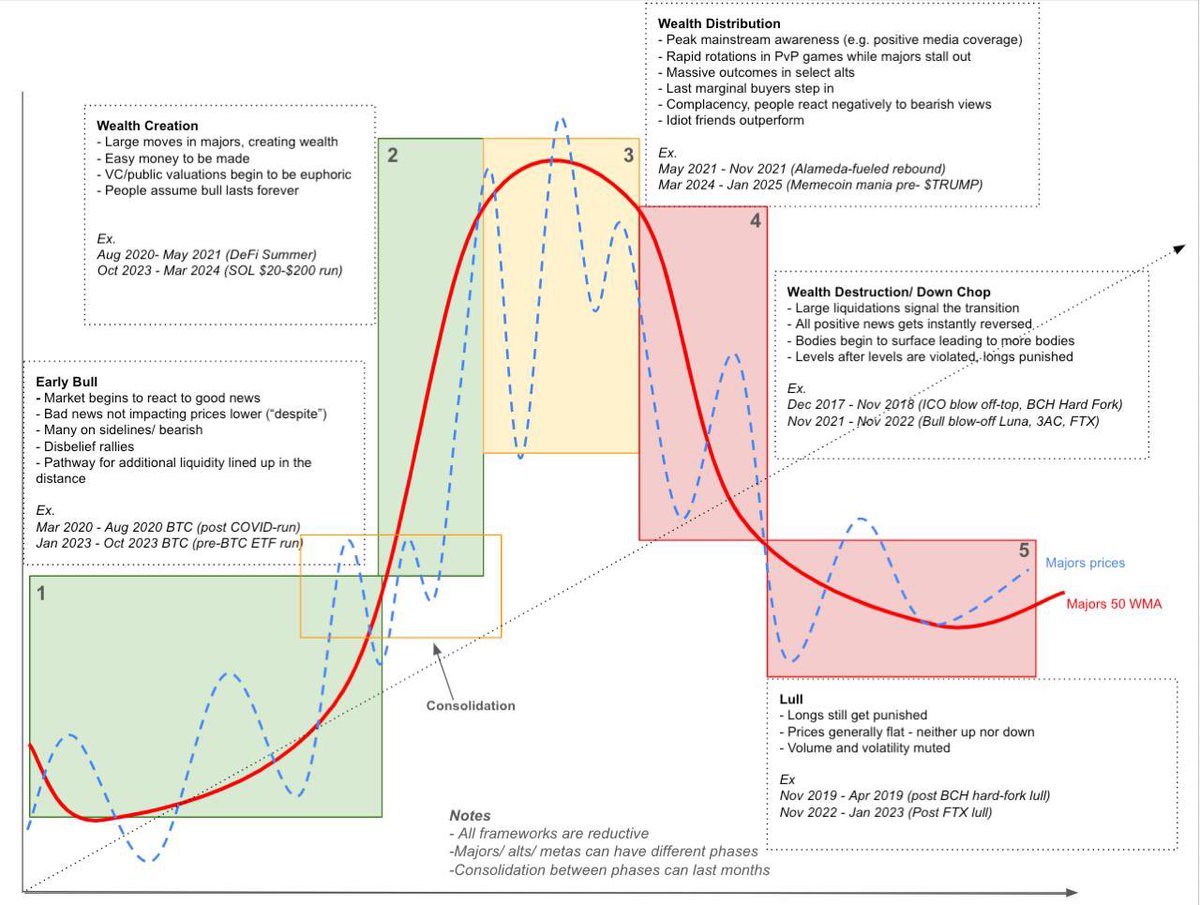

Regime 4 began in earnest on 10/10 imho.

Some heuristics: positive news are getting reversed (eg $UNI fee switch), small bodies started to surface.

This is not a predictive framework (there is no such thing) but only serves to add nuance to the unproductive “bull / bear” talk.

If you’re a crypto founder looking to fundraise, the window for finding price-insensitive bid is likely over for now. Focus on leaning up and surviving.

Many of the fastest growing products across multiple cycles were all built in Regime 4/5s.

5 Mar 2025

Since some of you found this framework helpful, here’s an updated version

All frameworks are by definition reductive but this gives me clarity on navigating time frames and is part of the reason I limited significant drawdowns to 2 (2017 end and May 2021) in the past 7 years in a 100% vol asset class

Thoughtful critiques welcome

48

16

177

44,592