Content creator 🍭

Joined January 2025

- Tweets 18,684

- Following 7,844

- Followers 9,103

- Likes 17,269

671 Photos and videos

i think one of the biggest lies in crypto right now is that communities are built around belief.

most of them are built around extraction.

people pretend every ecosystem is some kind of movement but the second rewards dry up the timelines go silent and the community disappears overnight.

that is why i stopped trusting engagement numbers a long time ago.

a project with 500 real users who genuinely care is way more valuable than one with 200k followers farming campaigns for points they will dump later.

you can feel the difference immediately when you actually use the product.

real communities complain.

they ask difficult questions.

they criticize decisions.

they stay even when the token is down bad.

farmed communities only know how to post emojis and say bullish under announcements.

honestly i think crypto underestimated how hard real attention is to earn.

money can buy reach for a while.

it cannot buy conviction.

that is also why i find platforms like @RallyOnChain interesting right now.

most projects measure impressions.

very few try to measure whether somebody actually has something real to say.

the next cycle probably will not belong to the loudest projects.

it will belong to the ones people still talk about when there are no incentives left.

6

11

33

3,843

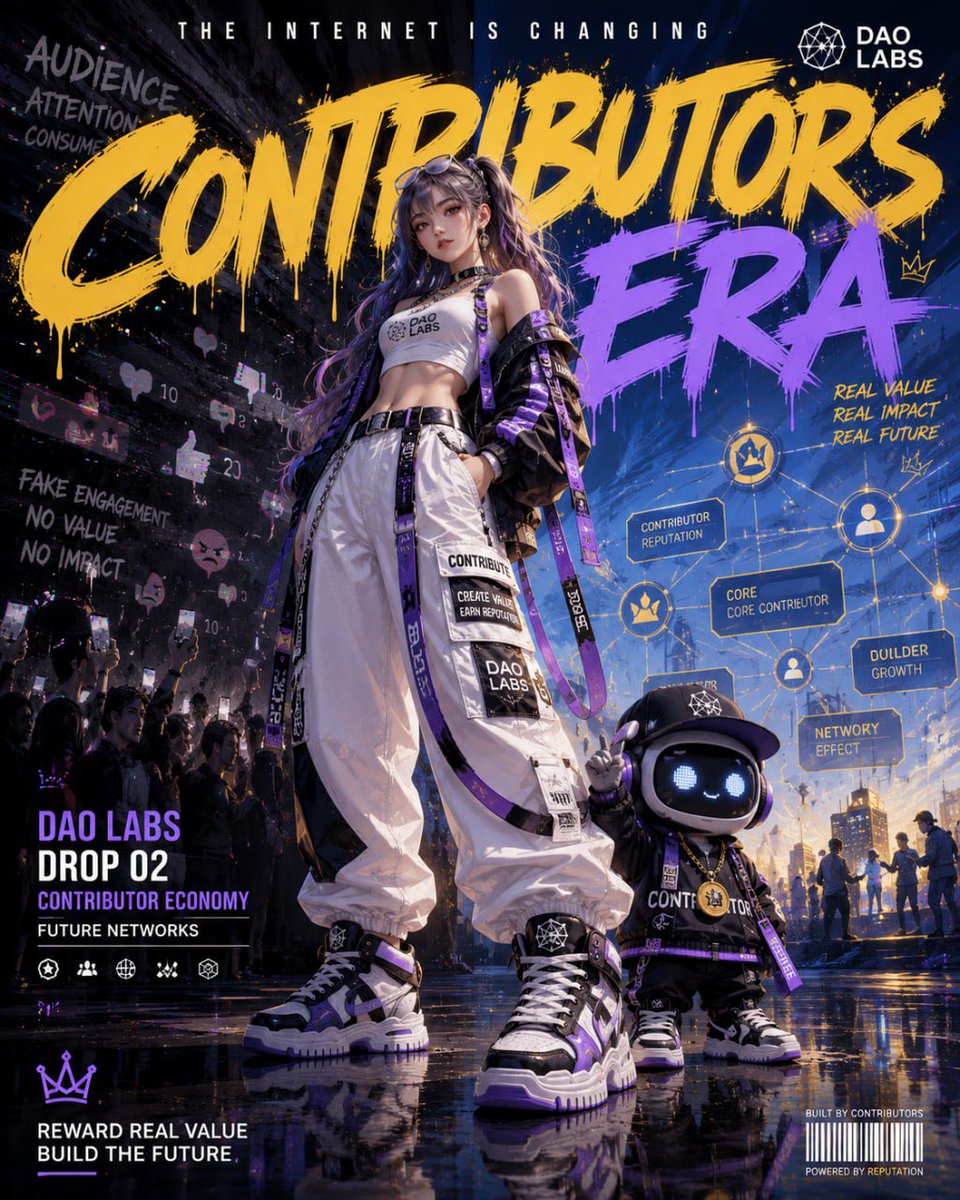

After reading through DAO Labs materials, I keep coming back to one idea:

The future internet probably won’t revolve around audiences.

It’ll revolve around contributors.

That’s a very different model.

Instead of people passively consuming content, communities become active economic networks where participation itself creates measurable value.

AI then becomes the layer that helps coordinate, optimize, and scale those networks.

And honestly, that shift feels inevitable.

Because traditional engagement driven systems are already starting to break under low quality content and attention farming.

The ecosystems that survive long term will likely be the ones capable of rewarding meaningful contribution instead of pure visibility. @TheDAOLabs #SocialMining

I think many people underestimate how difficult decentralized coordination actually is.

Building technology is hard.

But organizing humans at scale is even harder.

Especially online.

DAO Labs seems to understand that future digital economies won’t just need AI tools.

They’ll need AI assisted organizational structures.

Systems that can:

surface valuable contributors

coordinate workflows

reduce friction

align incentives

and improve execution quality

That’s a much deeper problem than simply building another AI application.

And honestly, solving coordination may become one of the most valuable layers in the next era of the internet.@TheDAOLabs #SocialMining

1

7

156

Most people still think institutional adoption is about who launches the biggest pilot first.

I think the more important question is which settlement rails institutions quietly standardize around before the market fully notices.

That is why the current moment around @zksync feels more important than most people realize.

The interesting part is not that institutions are “experimenting” with blockchain anymore. That phase already happened years ago.

What matters now is production architecture.

Deutsche Bank’s DAMA 2.0 infrastructure through Memento is not just another partnership headline. A tier one global bank choosing a ZK based settlement environment for tokenized fund infrastructure says something very specific about where regulated finance thinks the market is heading. Privacy, controlled execution, and Ethereum anchored settlement are no longer optional features for institutions. They are baseline requirements. (zksync.io)

The same pattern appears with Cari Network.

Five U.S. regional banks representing more than $600B in combined deposits are currently onboarding with production rollout planned for later in 2026. What stands out to me is not only the scale, but the coordination effect behind it.

Banking infrastructure becomes stronger when multiple institutions share operational rails. Once treasury systems, compliance workflows, and counterparties begin aligning around the same environment, switching costs rise very quickly.

That dynamic is exactly how financial standards harden over time.

What makes the ZKsync approach structurally different is that the stack was designed around institutional constraints from the beginning instead of trying to retrofit them later.

Most crypto infrastructure works well for open participation but breaks down once privacy requirements enter the picture.

No major trading desk wants its positions visible to competitors in public state. No regulated institution wants compliance logic patched together across fragmented middleware. Privacy is not an extra feature for institutional settlement. It is the gating requirement.

This is where Prividium becomes important.

The architecture combines privacy preserving execution, institutional control, Ethereum anchored security, and composability inside the same environment instead of splitting them across separate vendors and external integrations. (CoinDesk)

I also think people underestimate how important custody integration is in this cycle.

The BitGo integration matters because institutional adoption does not happen when a chain is technically impressive. It happens when compliance teams and operational teams can actually deploy it inside existing frameworks.

Custody is what transforms infrastructure into something institutions can realistically use at scale. (CoinDesk)

Another piece that deserves more attention is timing.

2026 feels like the narrow window where institutional blockchain infrastructure is moving from evaluation phase into standardization phase.

That window does not stay open forever.

The first networks to accumulate regulated deployments gain more than headlines. They gain trust accumulation, operational familiarity, integration gravity, and eventually default positioning for the next institution entering the market.

Technology gaps can close surprisingly fast in crypto.

Network effects inside financial infrastructure usually do not.

That is why this current lead matters.

Not because the race is already over.

But because settlement infrastructure tends to compound around the systems institutions already trust enough to deploy first.

17

24

51

6,377

I think many people underestimate how difficult decentralized coordination actually is.

Building technology is hard.

But organizing humans at scale is even harder.

Especially online.

DAO Labs seems to understand that future digital economies won’t just need AI tools.

They’ll need AI assisted organizational structures.

Systems that can:

surface valuable contributors

coordinate workflows

reduce friction

align incentives

and improve execution quality

That’s a much deeper problem than simply building another AI application.

And honestly, solving coordination may become one of the most valuable layers in the next era of the internet.@TheDAOLabs #SocialMining

One thing I appreciate about DAO Labs is that their narrative feels grounded in real operational problems.

Not just AI will change everything.

But specifically:

How do communities scale?

How do contributors get recognized fairly?

How do organizations coordinate globally without collapsing into chaos?

Those are real problems.

And honestly, most Web3 ecosystems still don’t have good answers.

That’s why reputation systems combined with AI coordination feel so powerful to me.

Because attention alone isn’t sustainable.

Eventually ecosystems need systems that reward people who consistently create value over time. @TheDAOLabs #SocialMining

33

21

61

3,912

My early days in DeFi, a very popular threador gave me this piece of advice Always lock your tokens for the maximum duration if the APY is over 100%. It is literal free money.

It sounded like a flawless strategy. I took my biggest bag at the time and locked it into a 12 month staking vault. I felt like a financial genius watching the dashboard rewards tick up every single day.

Two months later, the market narrative shifted. The protocol's emissions were too aggressive, inflation spiked, and the chart started tanking. I wanted to cut my losses and exit, but my capital was hard locked.

I was forced to sit on the sidelines for 10 more months, helplessly watching the token bleed 95% of its value. That massive 150% APY I was earning did not even cover a fraction of the capital destruction.

The hardest lesson I learned: Liquidity is your most valuable asset in this market. Outsized APY is never a gift. It is the premium you are being paid to take on unseen risks.

You cannot survive in crypto by following generic noise or blindly locking up your capital. You need to verify the mechanics yourself. This is why

I am paying close attention to what @RallyOnChain is building. We desperately need platforms that reward transparent execution and real community value, rather than trapping users in unsustainable hype cycles.

What is the most expensive passive income advice you ever fell for?

Let's hear your horror stories in the replies.

11

13

40

2,940

Dạo này mình thấy nhiều trader crypto bắt đầu nhìn sang Gold với CFD nhiều hơn thật.

Một phần vì market hiện tại chạy theo tin vĩ mô khá nặng. Có những ngày altcoin gần như đứng hình nhưng Gold với DXY chạy rất rõ theo CPI hay phát biểu FED. Nếu trade ngắn hạn thì mấy market này nhiều khi còn dễ tìm setup hơn crypto.

Mình trước giờ chủ yếu trade futures crypto, nhưng gần đây cũng bắt đầu theo dõi XAUUSD nhiều hơn để đọc dòng tiền với tâm lý thị trường.

CFD mình nghĩ không phải kiểu easy money như nhiều người hay shill. Nó vẫn là trading thôi, vẫn cần quản lý risk và giữ kỷ luật. Nhưng cái hay là có thêm market để quan sát thay vì chỉ quanh quẩn BTC với alt.

Thấy Bitget đang mở CFD Championship Phase 5 nên mình có đọc qua format event.

Khá ổn ở chỗ họ chia nhiều kiểu reward chứ không chỉ đua volume:

• Tổng prize pool $90,000

• Leaderboard riêng $60,000

• Top trader nhận tới $4,000

• User mới mở 0.01 lot Gold có 3 lượt Lucky Draw

Ngoài ra còn có daily check-in với blind box nên kể cả không phải tay to vẫn có thể tham gia thử.

Mấy event trading kiểu này thường early phase sẽ dễ tham gia hơn lúc crowd chưa vào đông, anh em nào muốn trải nghiệm CFD có thể xem qua.

Mọi người tham gia even link bên dưới nhé :

bitget.com/en/launchhub/trad…

#Bitget #CFDChampionship

Jun 9

🔥🔥 CFD Championship 5: 0 Fees $90K | Double Win

✅ Complete tasks to unbox Mystery

New users trade 0.01 lot XAUUSD get 3 lucky draws!

✅ Trade vol 50,000$ get 1 credit, share 15,000 USDT

✅ Top trading vol share 60,000 USDT

1️⃣ 4,000$ 2️⃣ 3,000$ 3️⃣ 2,000$

🔗 bitget.com/vi/launchhub/trad…

This information is for reference only and is not investment advice❗️

28

27

741

Chào mng buổi chiều nhé ☀️

Hôm nay bánh bèo 1 bữa nha dạo này bị flop qua mng

Đăng bài dự án thì kh ai tt hết, đăng ảnh thì quá tr reply khong hết 🤣

Ráng active đều xem X có mở lại kt cho mình kh chứ em là em hơi oải r đó

Hôm qua vào check thấy được cộng thêm 12 con vịt 🦆

Cảm ơn @wallchain và mng giúp em có nhiều vịt nhé 🥰

63

62

1,412

ETH mấy hôm nay bị sell khá mạnh, cây nến hôm qua còn quét xuống gần EMA89 làm nhiều lệnh long bị stoploss liên tục.

Mình đang ưu tiên quan sát phản ứng giá quanh vùng này trước khi quyết định long tiếp hay đảo bias short ngắn hạn. Giai đoạn market biến động kiểu này thì volume thường tăng rất nhanh, cũng là lúc mấy event trading race dễ tận dụng nhất.

Thấy bên Bitget đang mở Crazy 48 Hours ETH Special khá đáng chú ý:

• Chỉ diễn ra trong 48h

• Pool thưởng 40,000 USDT

• Chỉ có 256 suất nhận thưởng

• User top có thể nhận tới 2,000 USDT

Điểm mình thấy hợp lý là luật khá đơn giản, chỉ cần trade cặp ETH USDT và đạt đủ volume yêu cầu là có cơ hội share pool.

Nếu ae vốn đang trade ETH hằng ngày thì gần như không cần thay đổi strategy quá nhiều, chỉ cần tối ưu volume và quản lý risk ổn là được.

Mình đang canh thêm volatility để scalp ngắn trong 2 ngày event này, vì ETH hiện tại spread và thanh khoản đều khá ổn cho trader đánh nhanh.

Jun 13

⚡️Crazy 48H (ETH) 256 slots, win up to 2,000 USDT

Trading volume leaderboard battle, share 40,000 USDT

🥇 2,000 USDT

🥈 1,500 USDT

🥉 1,000 USDT

...

⌛ Ends 22:59 14/6/2026 (UTC 7)

🔗 bitget.com/vi/launchhub/trad…

This information is for reference only and is not investment advice❗️

8

7

254

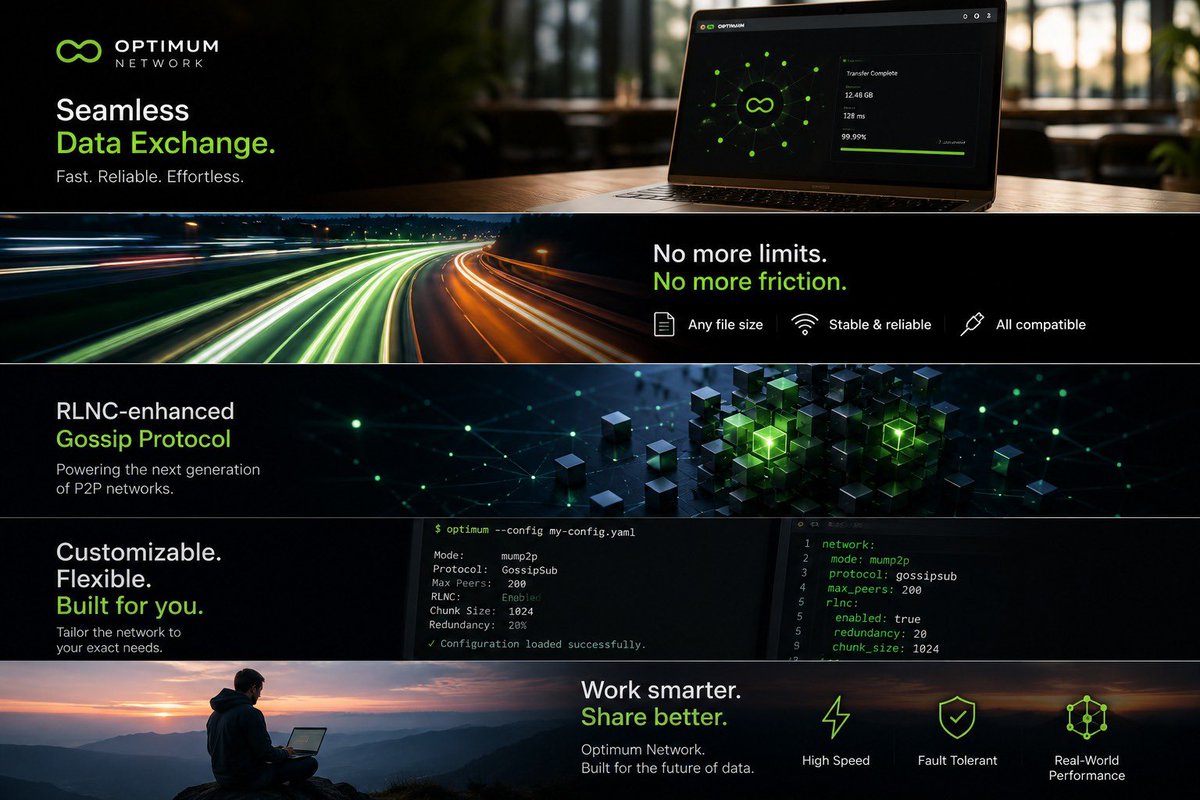

You know the old saying Speed is king, but reliability is queen. This adage holds particularly true in the world of peer to peer (p2p) networks, where both speed and reliability are crucial for seamless data exchange.

@get_optimum's Optimum Network has mastered this balance, delivering high performance capabilities and a robust gossip protocol that enables efficient data exchange. By leveraging this protocol, the network can handle files of any size without worrying about network stability or compatibility issues, making it a game changer for developers, researchers, and anyone who values efficient data exchange.

Imagine being able to share large datasets, collaborate on complex projects, or simply exchange files with colleagues without the fear of network downtime or errors. This is exactly what Optimum

Network provides, streamlining data exchange and opening up new possibilities for collaboration and innovation. Furthermore, the network's reliability also ensures that data is transmitted securely, reducing the risk of data loss or corruption, a critical feature for industries such as healthcare, finance, and research where sensitive data is involved.

The Optimum Network's architecture is designed to adapt to dynamic network conditions, automatically adjusting to changes in network traffic and optimizing data exchange in real time. This ensures that data exchange remains efficient even in the face of network congestion or other challenges. With Optimum Network, users can focus on their work without worrying about the intricacies of p2p networking, making it an attractive solution for organizations and individuals alike.

2

2

81

Most people still think the blockchain race is about users.

It is not.

The more important race is happening inside settlement infrastructure.

Right now, banks, custodians, and clearing institutions are deciding which rails they are willing to build on for the next decade.

And those decisions rarely get reversed once they compound.

JPMorgan’s Kinexys platform has already processed over $1.5T in blockchain based transactions.

DTCC is moving toward tokenized U.S. Treasuries.

NYSE, BNY, and Citi are actively exploring tokenized securities infrastructure.

This is no longer experimentation.

It is architecture selection.

What makes settlement infrastructure different from consumer apps is that network effects compound asymmetrically.

A social app can lose users quickly.

Settlement rails usually do not.

Because every additional institution increases the value of the network for every other participant already connected to it.

If 10 institutions settle with each other, there are 45 possible settlement relationships.

If 100 institutions connect, that number approaches 5,000.

The network becomes harder to replace with every new participant.

That is exactly why systems like SWIFT became deeply embedded in global finance.

Not because they were perfect.

Because coordination matters more than novelty once capital flows depend on the system.

And this is where onchain infrastructure starts becoming important.

Institutions are not simply looking for a blockchain.

They are evaluating whether a system can support privacy requirements, interoperability, compliance standards, predictable execution, and long term scalability.

The technical requirements are higher because the cost of failure is higher.

A retail app can tolerate downtime.

Settlement infrastructure cannot.

This is part of why @zksync is becoming increasingly relevant in this conversation.

zkSync’s positioning has never been only about retail throughput.

The more interesting angle is that zk technology aligns closely with what institutional finance actually needs from onchain settlement.

Scalability matters.

But so does privacy.

So does verifiability.

So does interoperability across different financial environments.

The market is also underestimating how important early institutional integrations become over time.

Infrastructure decisions in finance tend to ossify.

Once workflows, compliance processes, treasury systems, and counterparties align around a rail, switching costs rise dramatically.

That creates a compounding advantage for networks that establish credibility early.

Which is why the next 18 to 24 months matter so much.

This is probably the first real window where onchain settlement infrastructure moves from pilot programs into long duration financial architecture.

And when that transition happens, the winners are usually not determined by hype.

They are determined by who institutions trust to settle value at scale.

16

13

57

6,130

Xem bóng đá nhiều lúc cay nhất không phải thua kèo

mà là cảm giác một quyết định của trọng tài có thể đổi luôn cục diện trận đấu 😵💫

Universal Cup của Bitget cho mình cảm giác khá thú vị ở chỗ:

lần này người xem không chỉ ngồi xem nữa, mà có thể tự tác động vào trận đấu bằng cách sút penalty vào Crypto hoặc Stock target để kiếm điểm cho team mình chọn.

Kiểu concept biến người xem thành một phần của trận đấu này khá khác mấy campaign World Cup mình từng thấy trước đó.

Prize pool tới 250,000 USDT mà còn không cần KYC để tham gia nên entry khá dễ cho người mới.

Mình chọn team Brazil 🇧🇷 rồi, còn mọi người pick đội nào?

Link tham gia nhé cả nhà 👉google.com/url?q=partner.bit…

#UniversalCup

Why trade in separate leagues when your dream team can play on one field?

Crypto, Stocks, ETFs, and Gold are teaming up for the championship this year.

Watch the video to find out each player's strategy behind the lineup.

7

6

220

UEX Futures League vừa mở đăng ký cho khu vực SEA & SA và hiện tại số lượng team tham gia vẫn còn khá sớm.

Đó cũng là lý do mình nghĩ đây là giai đoạn đẹp nhất để vào giải.

Khi lượng đội và thành viên chưa quá đông thì cơ hội cạnh tranh leaderboard và săn reward sẽ dễ thở hơn rất nhiều so với lúc event bước vào giai đoạn crowded.

Tổng prize pool cho chặng Crypto lên tới 120,000 USDT:

• 80,000 USDT cho quỹ giải đấu

• 20,000 USDT cho bảng xếp hạng ROI đội

• 20,000 USDT cho PnL cá nhân

Điểm hay của UEX Futures League là format theo kiểu team competition chứ không đơn thuần là trade solo.

Bạn có thể:

• Tự tạo team và làm đội trưởng

• Hoặc join team có sẵn để leo ROI cùng nhau

Yêu cầu đăng ký:

• Futures net asset tối thiểu 100 USD

• Team cần ít nhất 10 thành viên để đủ điều kiện nhận thưởng

• Mỗi user chỉ được tham gia 1 team duy nhất

Điều kiện tham dự UEX Global Alpha Tournament:

• Những team có ROI cao nhất sẽ được mời vào vòng tiếp theo

• Có thể cần xác minh điều kiện và tiêu chí cân bằng khu vực trước khi tham gia finals

Cá nhân mình thấy những mùa đầu như thế này thường là thời điểm dễ kiếm edge nhất.

Ít team hơn ít cạnh tranh hơn.

Nếu đã từng trade futures nghiêm túc thì đây là lúc khá hợp để thử build squad riêng hoặc tham gia cùng bạn bè trước khi giải đông lên.

Link tham gia ở đây nhé 🥳

bitget.com/vi/events/competi…

Đội này đang top 1 nha mng ơi 🥰

Jun 10

👍 HOW TO JOIN A TEAM

1️⃣ Register

2️⃣ Join a Team ⚡️ Become a Captain

3️⃣ Team Requirement:

- 10 Active Members (KYC, futures asset 100$, 5-day trading)

- 1 KYC = 1 participant

- Team switching is NOT allowed

- Sub-accounts are excluded

➡️ Qualify for the UEX Global Alpha Tournament

✅✅✅ JOIN A TEAM

bitget.com/vi/events/competi…

This information is for reference only and is not investment advice❗️

23

28

509

I've been using @get_optimum's Optimum Network for a while now, and I'm still amazed by how seamless it makes data exchange.

What's even more impressive is how it removes all the friction that comes with it, no more worrying about file sizes, network stability, or compatibility issues.

With its RLNC enhanced gossip protocol and customizable configs, this network has genuinely changed the way I work with files. I've never experienced such reliability and speed in a p2p network.

So, if you're tired of dealing with slow or unreliable data exchange, give Optimum Network a shot. Your productivity and sanity will thank you.

1

1

97

JENNY retweeted

Jun 12

TaigonDAO x Mystic Spirits

Project Overview:

Mystic Spirits (玄灵) is a collection of 2,222 generative Chinese art NFTs, each one a unique fusion of ancient symbolism and Web3 culture. Drawn from the rich visual language of ink wash painting, woodblock print, silk art, and porcelain glazework, every piece features sacred themes dragons, phoenixes, cranes, koi, and more rendered with algorithmically generated auras, inscriptions, and celestial effects. Each token is a collectible relic from a world where classical Chinese artistry meets the blockchain age.

Supply: 2,222

Mint: June 16 4PM UTC

Price: 0.0018 ETH (~3$)

Chain: ETH

We’re GA: 10WL

How to enter:

- Follow @MysticSpirits_ & @TaigonDAO

- Like & Repost x.com/MysticSpirits_/status/…

- Comment your EVM wallet Winners will be picked within 48 hours.

THE WAIT IS ALMOST OVER.

Mystic Spirits is officially launching on @opensea

June 16 at 4PM UTC.

Set your reminders. Tell your friends. The spirits are calling.

Drop your wallets for WL.

22

19

24

328

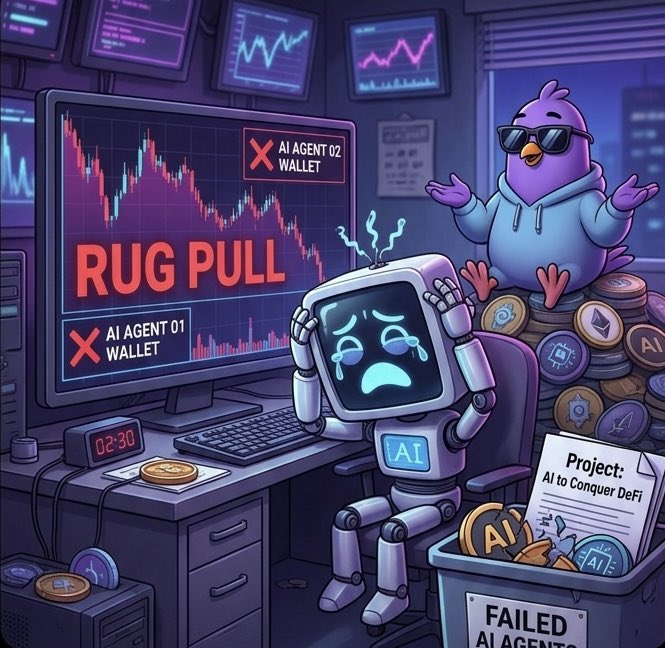

We are building fully autonomous AI agents with sovereign crypto wallets just so they can experience the pure human pain of getting rugged on a random Tuesday @RallyOnChain

15

6

40

1,929

JENNY retweeted

Jun 5

After the apocalypse, ⛩ the Torii Gate will open. Humanity has perished by this point, but their souls still live on in the form of Shinkai Bots.

shinkaijp.com/

心界 — すべてのShinkai Botは、独自の魂と物語を持つ。

109

288

1,164

24,104