Realtime entries and exits from the Dark Pool Vault.

Joined April 2026

- Tweets 167

- Following 37

- Followers 79

- Likes 13

Photos and videos

May 26

Exiting $RDW today @ 22.40. Although it will likely continue to run, this is a 149% gain on shares inside 25 days.

Have a handful of names I am looking to enter new positions in this week. Stay tuned.

May 1

Opening a position in $RDW at 8.98

$GOOGL just told the world that orbital computing is the future. Redwire is one of the few publicly traded companies building the physical layer of that future — solar arrays, orbital platforms, VLEO drones, docking systems — with a $411M backlog, accelerating book-to-bill, and two massive defense programs (Golden Dome SHIELD) coming online.

The broader market hasn’t yet connected orbital compute (Google/Suncatcher) → orbital infrastructure demand (RDW’s core business). Most retail flow is chasing the hyperscaler side of this trade ($GOOGL, $NVDA). The picks-and-shovels layer — power systems, platforms, docking, structural components — that’s where RDW lives.

Redwire is actively bidding on the Golden Dome missile defense initiative, which received $24.4B in initial federal funding and carries a projected lifetime value of $542 billion.

Redwire is forecasting 2026 revenues of $450M–$500M. Q4 2025 revenue was $108.8M — up 56.4% year-over-year — with a record contracted backlog of $411.2M and a book-to-bill ratio of 1.52 for the quarter.

With a $SpaceX IPO anticipated to ignite mainstream capital flows into the orbital economy, $RDW is positioned to catch a significant sympathy bid as retail and institutional investors look for pure-play space infrastructure exposure they can access today.

Risks to note: Earnings May 6th, the company is currently not profitable. Government contract timing delays remain a risk — management has insisted these are timing issues, not lost demand, making 2026 contract flow the pivotal variable for the investment thesis. I still like the risk/reward at this level.

266

May 21

$LITE shares are up ~8% today

To be honest, there is not much utility in trading $NVDA $MSFT $META $AMZN $GOOGL $AAPL in general, but especially earnings. We all know the numbers and guidance will be strong, their reactions are less predictable.

There are subsectors and themes that directly correlate to the commentary coming out of the hyperscalers, which have much cleaner risk/reward profiles.

May 20

Opening a swing trade in $LITE @ 875 ahead of $NVDA earnings

I’ve posted about $LITE before if you are interested in learning more about the fundamentals. I expect commentary from $NVDA to reinforce the AI infrastructure thesis, $LITE could catch a 10% or more bounce on that.

Also expect strong numbers and guidance from $NVDA, unsure how the stock will react.

426

May 20

Opening a swing trade in $LITE @ 875 ahead of $NVDA earnings

I’ve posted about $LITE before if you are interested in learning more about the fundamentals. I expect commentary from $NVDA to reinforce the AI infrastructure thesis, $LITE could catch a 10% or more bounce on that.

Also expect strong numbers and guidance from $NVDA, unsure how the stock will react.

1

14,082

May 15

Ackman buying $MSFT

Not a huge fan of his moves, but it probably catches a bounce here especially if semi’s pull back

May 15

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

177

May 14

As of yesterday’s close, $RDW is up 28% since I alerted opening a position on 5/1.

As the $SpaceX IPO approaches, I expect hyperscaler interest in orbital data centers to continue — $GOOGL x $SpaceX is just the beginning.

The same picks & shovels opportunity that played out in land-based data centers is setting up in orbit. Structural shielding, solar arrays, thermal management, rad-hard compute, laser inter-satellite links, propulsion — all of it needs to be built.

Eyeing a handful of names across those layers. Will be posting the next position soon.

May 12

Exclusive: Google is in talks with SpaceX for a rocket launch deal as the search giant expands its own efforts to put orbital data centers in space on.wsj.com/4nqozpg

331

May 11

Despite these headlines from the weekend, I expect some type of progress this week with Iran ahead of trumps meeting with Xi on Wednesday

May 11

Futures Flat, Oil Jumps After Iran Peace Talks Break Down zerohedge.com/markets/future…

140

May 8

$RDW - Redwire Q1 Earnings Recap

Shares are up 13 % from my alert last week

Yes, they missed. Revenue came in at $96.97M vs. $104.6M expected, and EPS of -$0.40 was well below the -$0.15 consensus — largely driven by a $42.5M non-cash, non-dilutive charge from equity vesting tied to the Edge Autonomy acquisition. Noise imo

Where I am focused is the backlog. $RDW posted a book-to-bill of 1.92 in Q1 and closed the quarter with a record $498M contracted backlog — up from $411M at year-end. Gross margin also ripped from 9.6% in Q4 '25 to 26.6% this quarter. The business is getting cleaner.

Management reaffirmed full-year guidance of $450M–$500M in revenue, and the Andromeda IDIQ ceiling is being flagged to rise above $6 billion.

Revenue was up 57.9% year-over-year.

Post-SPAC names like $RDW carry microscopic floats - SPAC redemptions wiped out the tradeable share base, and locked-up sponsor and PIPE shares mean the market simply can't absorb institutional buying without the stock moving violently. When a narrative re-rating hits - orbital compute as the next phase of AI infrastructure - shorts get squeezed.

I continue to believe capital will chase orbital compute ( $GOOGL adds to this) and with the upcoming $spacex ipo, $RDW is positioned to catch a meaningful sympathy bid as investors look for pure-play space infrastructure exposure.

May 1

Opening a position in $RDW at 8.98

$GOOGL just told the world that orbital computing is the future. Redwire is one of the few publicly traded companies building the physical layer of that future — solar arrays, orbital platforms, VLEO drones, docking systems — with a $411M backlog, accelerating book-to-bill, and two massive defense programs (Golden Dome SHIELD) coming online.

The broader market hasn’t yet connected orbital compute (Google/Suncatcher) → orbital infrastructure demand (RDW’s core business). Most retail flow is chasing the hyperscaler side of this trade ($GOOGL, $NVDA). The picks-and-shovels layer — power systems, platforms, docking, structural components — that’s where RDW lives.

Redwire is actively bidding on the Golden Dome missile defense initiative, which received $24.4B in initial federal funding and carries a projected lifetime value of $542 billion.

Redwire is forecasting 2026 revenues of $450M–$500M. Q4 2025 revenue was $108.8M — up 56.4% year-over-year — with a record contracted backlog of $411.2M and a book-to-bill ratio of 1.52 for the quarter.

With a $SpaceX IPO anticipated to ignite mainstream capital flows into the orbital economy, $RDW is positioned to catch a significant sympathy bid as retail and institutional investors look for pure-play space infrastructure exposure they can access today.

Risks to note: Earnings May 6th, the company is currently not profitable. Government contract timing delays remain a risk — management has insisted these are timing issues, not lost demand, making 2026 contract flow the pivotal variable for the investment thesis. I still like the risk/reward at this level.

7

29,407

May 7

Opening positions in $KTOS and $AVAV

After a meaningful reset on valuation and expectations, both names offer attractive risk/reward at current levels. Daily charts are messy — The weekly and monthly setups are where I am focused

$KTOS

Entry @ $58.25

-FY2025 revenue of $1.35B, up ~19% YoY — with management guiding 18–23% organic growth in 2027 above 2026 levels as program awards accelerate.

-Dominant position in affordable attritable drones (UTAP-22 Mako) — the DoD is structurally shifting toward mass/expendable platforms, and KTOS is best-positioned to capture that budget shift.

-Hypersonic and directed-energy programs (ALTIUS, MAKO, SDT) represent long-duration optionality that the market has been discounting at peak rates. With defense budgets expanding and threat environment elevated, that discount compresses.

-Pullback brings valuation back to a range where risk is well-defined. Weekly structure holds a key support zone, a level that marked accumulation in prior cycles.

$AVAV

Entry @ $171

-FY2025 revenue of $820M, up 14% YoY — Loitering Munitions Systems surged 87% in Q4. FY2026 guidance of $1.9–2.0B (includes BlueHalo acquisition) represents a step-change in scale.

-Switchblade loitering munitions and the small UAS portfolio are seeing real wartime demand validation — Ukraine and peer-threat scenarios have moved AVAV from niche procurement to essential battlefield hardware.

-Production scale is the next catalyst — as unit volumes grow to meet sustained DoD and allied demand, hardware unit economics improve and backlog visibility extends.

-After a significant de-rating, the weekly chart is showing a base worth respecting. Not trying to catch the exact low — looking to participate in the re-rate as execution re-establishes credibility.

4

38,093

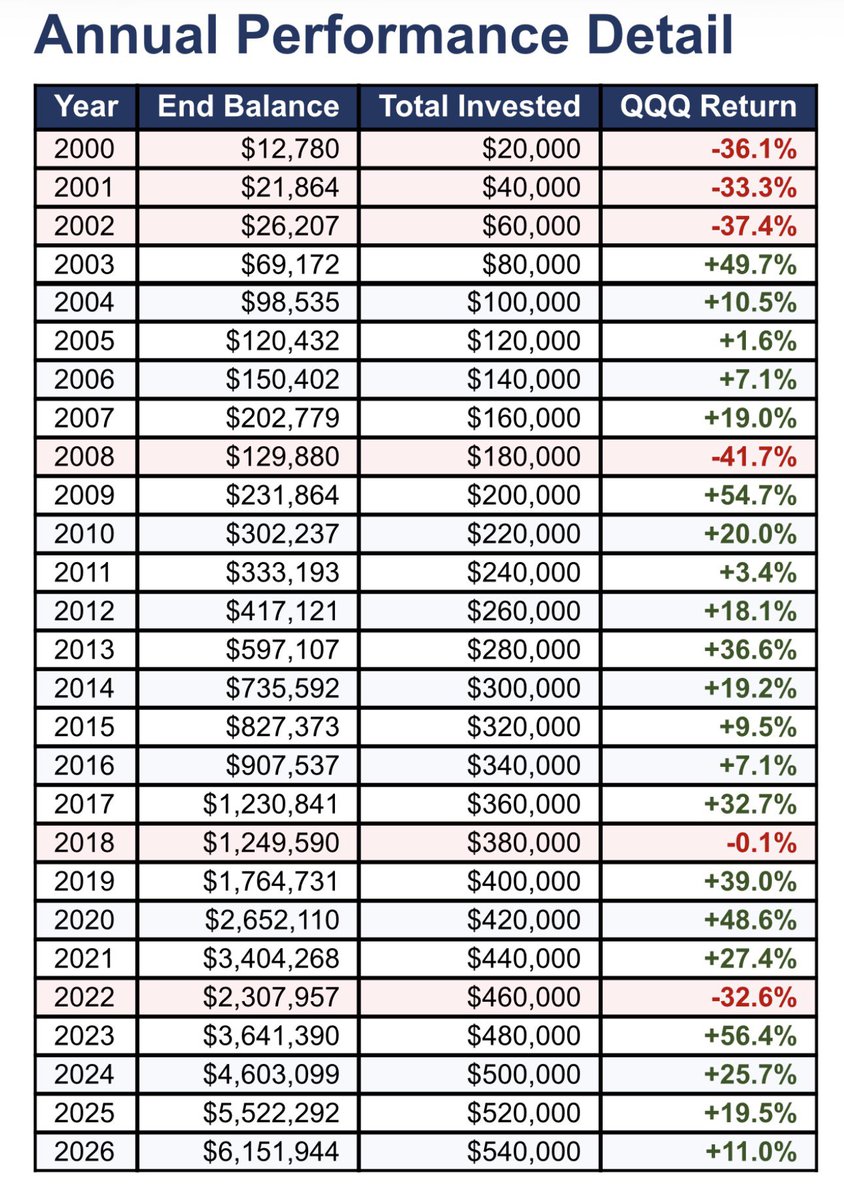

May 7

My feed is loaded with posts about how this is such a horrible time to start your investing career if you’re in your 20s.

This is what it would actually look like if you started your investing career at the worst possible time in the post internet era, experiencing 3 consecutive 30 % down years immediately and then the great financial crisis 40 % down year.

This table assumes you invest 20k per year into QQQ starting in 2000, if you were 25 at inception you are 51 today with a balance of $6,151,944

$QQQ $QQQM

1

134

May 6

$LEU EPS beat with guidance raise — $LEU topped earnings estimates and lifted full-year revenue guidance to $450–$500M, up from the prior $425–$475M range

Execution mode on Oak Ridge expansion — Management signaled a shift from planning to building, with Fluor handling engineering/procurement and Palantir’s AI platform already identifying ~$300M in cost savings with further lead time reductions expected

Strategic partnership network expanding — Geiger Brothers added alongside Fluor and Palantir as day-one partners; an Oklo JV is being explored for HALEU deconversion services

Management pointed to global conflicts and energy security concerns as accelerating the shift toward domestic, non-fossil fuel power — a direct tailwind for domestic enrichment capacity

This is a must own AI infrastructure/energy name that has tremendous upside

2

327

May 6

$LUMN missed earnings expectations but when you look into the numbers the miss is mainly due to the acquisition of Alkira; which in my opinion bolsters their ai capabilities.

EPS (-$0.47 vs. -$0.10 expected), though EBITDA of $1.28B crushed the $791M estimate. Free cash flow guidance was raised.

Strategic business revenue hit $1.246B and crossed 51% of total business revenue for the first time, surpassing Legacy.

The pending Alkira acquisition is framed as capturing a $70B addressable market by enabling customers to design, deploy, and operate the network as software across cloud environments.

I will continue to hold $LUMN as I believe the risk reward is still attractive at these levels.

4

887

May 5

Opening a position in $LEU — Centrus Energy Corp at 203

Centrus is the only licensed producer of HALEU (High-Assay Low-Enriched Uranium) in the US. Foreign, state-owned enterprises currently control nearly 100% of the world’s uranium enrichment capacity. In October 2025, the NNSA notified Centrus of its intent to sole-source certain uranium enrichment activities specifically for national security purposes.

The balance sheet is strong

FY2025 results: $448.7M revenue, $117.5M gross profit, $77.8M net income — with $2.0B in unrestricted cash on the balance sheet.

For a $4B market cap company, that’s extraordinary optionality. Centrus plans to deploy $350–500M in 2026 toward centrifuge manufacturing and industrial buildout at Piketon, Ohio.

Centrus exited 2025 with a $3.8B revenue backlog extending to 2040. The LEU segment alone accounts for $2.9B. These are long-term utility contracts — not letters of intent — because utilities have no alternative domestic source.

Additionally, $2.3B in contingent LEU commitments are tied specifically to Centrus hitting capacity milestones. The demand is real. The supply constraint is the only variable.

Every advanced reactor and SMR being developed for AI data centers, defense, and remote power requires HALEU. There is no other Western supplier. The opportunity is estimated at $8B per year by 2035.

In January 2026, the DOE selected Centrus for a $900M task order to expand Piketon to include commercial-scale HALEU production. Centrus is targeting 12 metric tons of HALEU/year after 2030.

In March 2026, Centrus and $PLTR announced a partnership deploying Palantir’s Foundry and AIP tools across engineering, manufacturing, supply chain, and regulatory compliance for the Piketon expansion.

Since the partnership launched in late January, they’ve already identified nearly $300M in potential cost savings.

The thesis runs through physical infrastructure: AI data centers need power → power increasingly means nuclear → nuclear needs enriched uranium → next-gen reactors need HALEU → Centrus is the only gate. The CEO stated directly that HALEU “will power tomorrow’s data centers and AI technologies.”

$OKLO and Centrus are also exploring a JV to co-locate HALEU deconversion at Piketon alongside enrichment — which would consolidate the entire fuel cycle at one domestic site and reduce shipping complexity significantly.

Key risks:

• Earnings are very volatile, they report today after the close

• Piketon execution risk — large industrial buildouts have a history of cost overruns

• Government funding continuity — much of the growth path runs through DOE decisions

• significant free cash flow generation doesn’t begin until enrichment capacity comes online post-2029

1

877

May 5

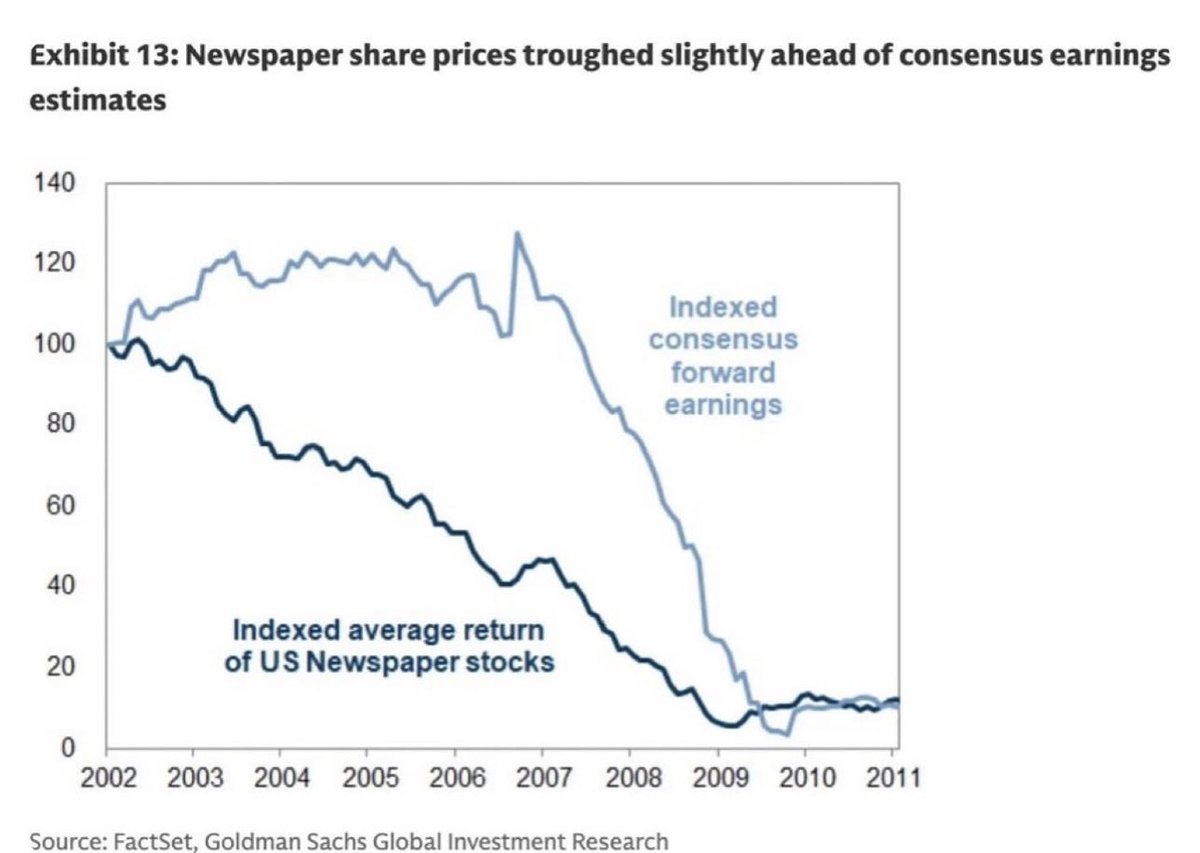

From 2002 - 2009, newspapers stocks went down in a straight line because the market foresaw the disruption of the internet

Yet earnings continued growing for 5 straight years... until they didn't.

I don’t think software and newspapers are the same but we are so early in ai there are more unknowns than knows. That’s why I see more opportunity in the physical/hardware layer. I’ll be opening a new position before the close today.

Do you think this can happen to software stocks?

$MSFT $NOW $ADBE $CRM $ORCL $PLTR $CRWD $INTU $APP $SNPS $DDOG

1

1

28,092

May 5

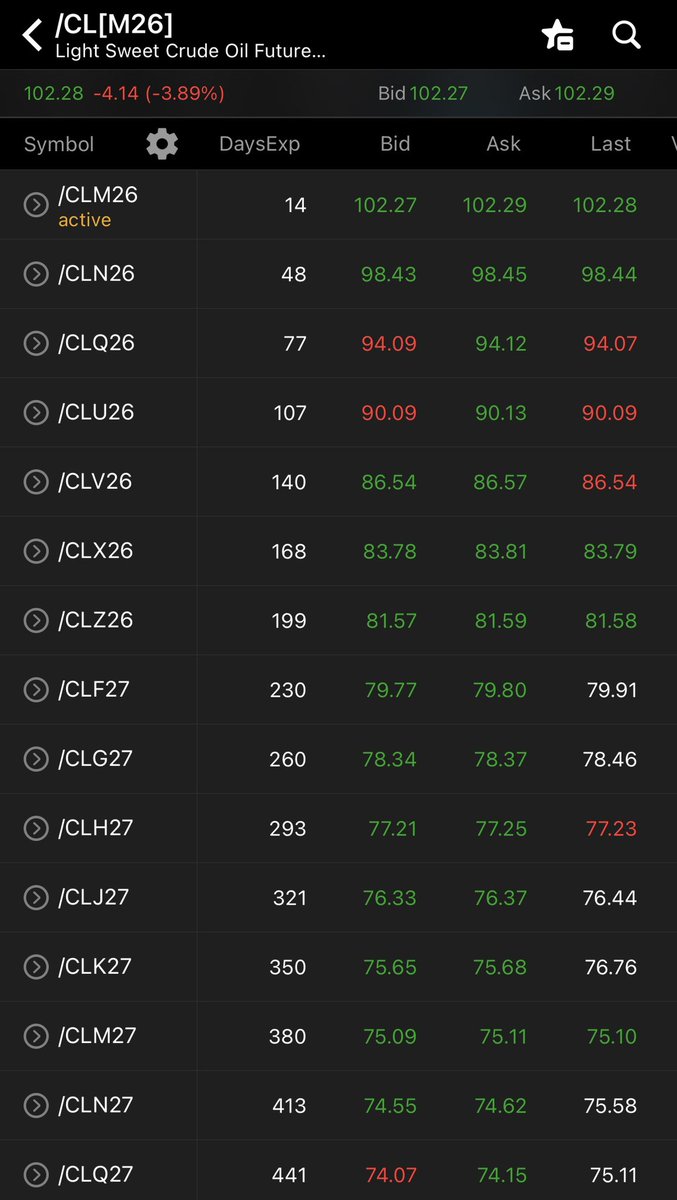

Another day, another seesaw in oil prices.

It’s not until the November (CLX26) futures market that we see crude oil under $85. I feel the conflict in the Middle East will be resolved by the midterms and that this is an overreaction — though that doesn’t mean we can’t go higher before then.

The options market has made it incredibly difficult to bet on either direction while defining risk, forcing you to trade outright.

You can’t trade $USO because when markets are in contango, it actually benefits the ETF to buy the following month’s contract at a cheaper price.

If I’m trading crude oil today, I’m selling $102 calls on the November contract — they’re worth $5.20 today. Size should be proportional to your futures exposure (e.g., sell 1 call per 1 futures contract).

$WTI $CL $OIL $BNO $XLE #oilprices

#iranwar #straitofhormuz #globaleconomy

87

May 4

I continue to believe the best investing opportunities in AI remain in the physical layer / hardware names that are direct beneficiaries of hyperscaler capex $GOOGL $AMZN $MSFT $META $NVDA

$LITE $CLS $AAOI $APH are 4 names I own in the optical & connectivity category - I'd wait for moving averages to catch up before opening new positions but these need to be on your watchlist — they have direct, high-beta correlation to hyperscaler AI infrastructure spend.

The hyperscalers are spending $725B in capex in 2026. A decent chunk of that is physically flowing to these names.

1

1

18

44,149

May 4

$AAOI Applied Optoelectronics: Pure-play provider of high-speed optical transceivers (800G and moving to 1.6T) essential for connecting massive AI GPU clusters.

Explosive bandwidth demand in AI training clusters is shifting away from copper toward optics for scale, power efficiency, and performance.

Multiple large 800G orders in 2026 from major hyperscalers (including upsized deals with a key customer totaling $124M since mid-March, strong $MSFT relationship, and $AMZN exposure via long-term agreements and warrants).

Vertical integration is the structural moat. In-house indium phosphide laser manufacturing cited as a strategic advantage to mitigate industry shortages, with plans to more than triple laser manufacturing in Texas. Most competitors outsource lasers — $AAOI makes their own.

Profitability inflection is imminent. Management targets sustainable non-GAAP profitability beginning in Q2 2026. Still unprofitable today — but the ramp is designed to flip that this quarter

Note that Q1 2026 earnings are Thursday, May 7, so this is a live catalyst

1

160

May 4

$APH Amphenol: Dominant provider of high-speed connectors, backplanes, power solutions, and cable assemblies for AI servers and racks.

Every dense GPU cluster requires massive interconnect content for both data and power delivery.

Primary connector supplier to $NVDA (which powers most hyperscaler AI clusters) direct exposure across $GOOGL $AMZN $MSFT $META

Recent CommScope CCS acquisition strengthens fiber/copper position.

Book-to-bill tells you demand is accelerating. Q1 2026 orders hit a record $9.4B, up 78% year over year, with a book-to-bill of 1.24. That ratio means they're booking more than they're shipping.

The margin profile is best-in-class for an industrial/hardware name. Adjusted operating margin of 27.3% in Q1 2026 — up 380bps year over year. Most industrial/connector peers run in the mid-teens.

Diversification is the hidden edge. Unlike the other 3 which are heavily concentrated in one or two hyperscalers, $APH serves defense, automotive, industrial, and commercial — meaning the AI tailwind is additive, not the whole story. Less upside but more downside protection the others don't have.

3

562