Joined March 2024

- Tweets 639

- Following 208

- Followers 2,745

- Likes 3,801

24 Photos and videos

Daniel Barabander retweeted

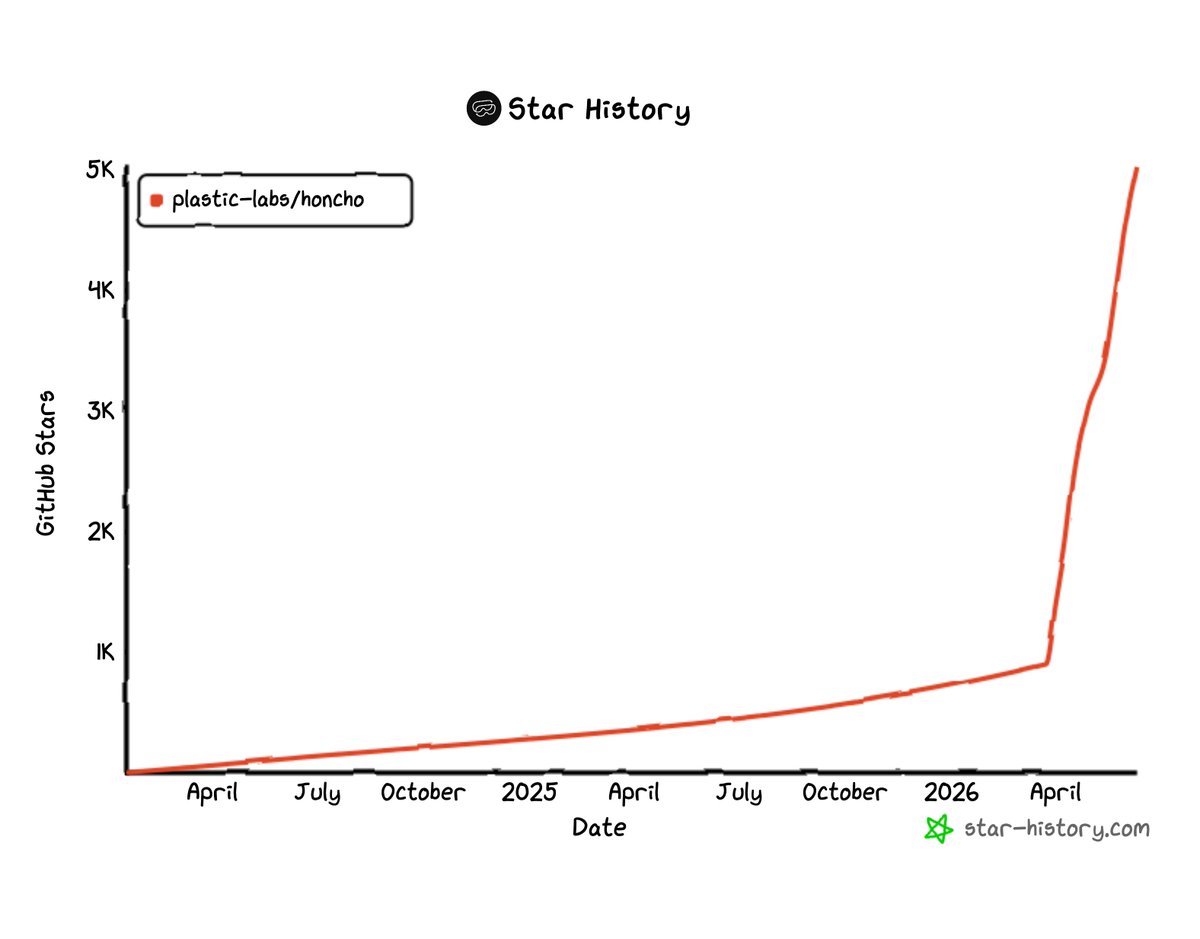

Jun 10

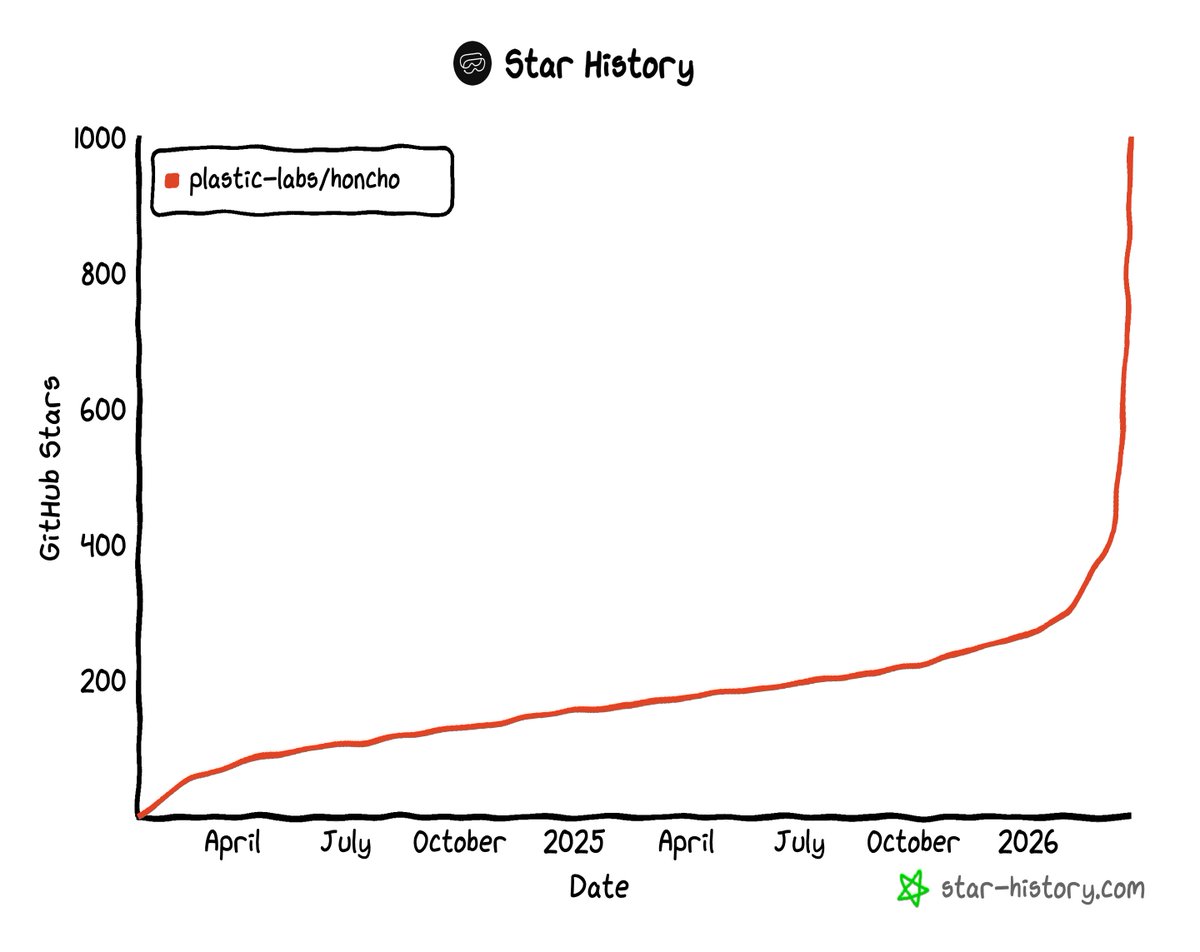

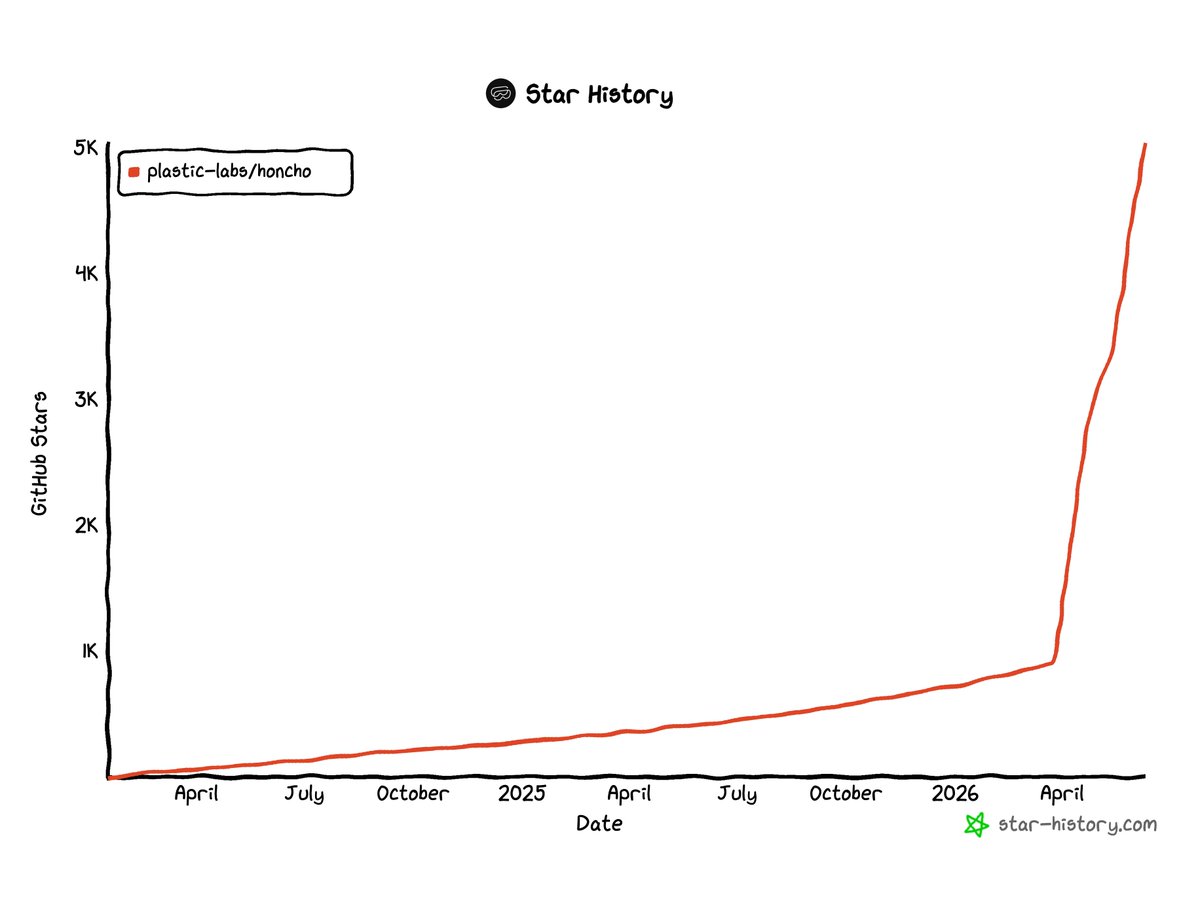

continuing the climb, just passed 5k stars

we'll see you at 10k 🚀

1

2

17

387

Daniel Barabander retweeted

Jun 10

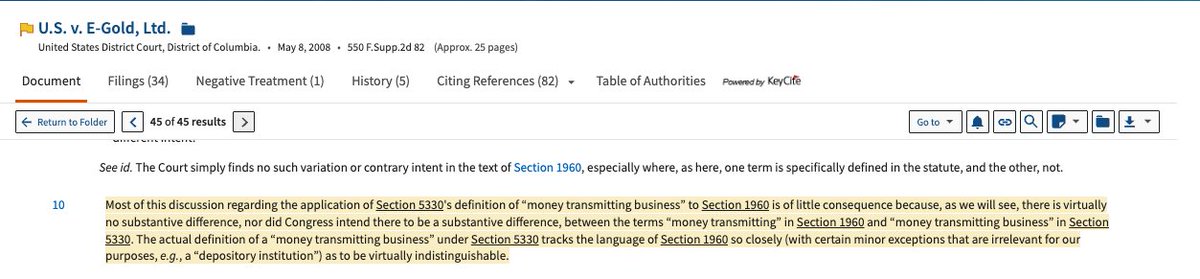

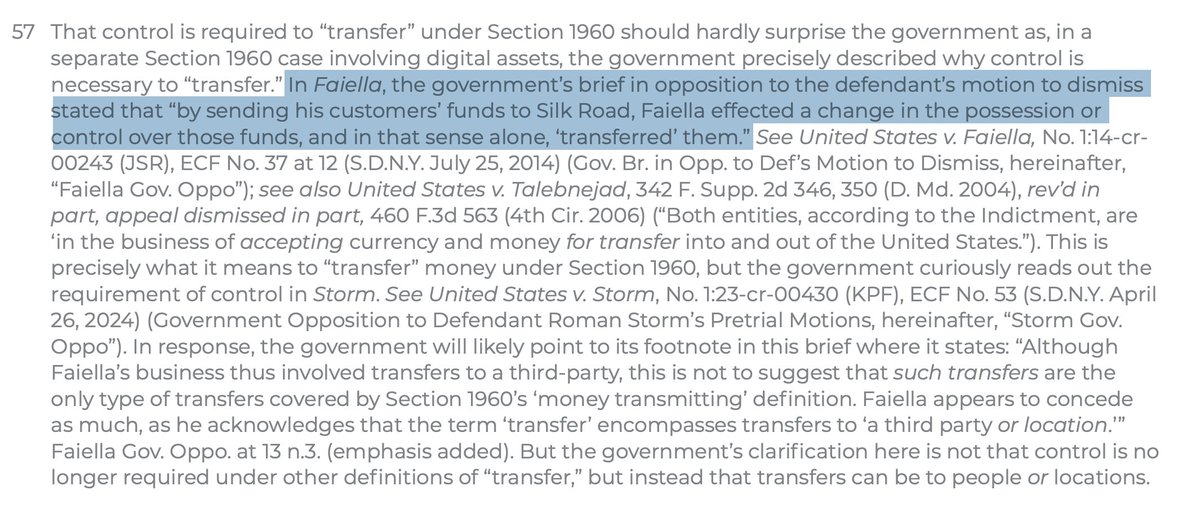

Great assessment of problematic compliance and KYC on-chain which is really a continuation of the same problem faced on-line by regulated transactions and entities (problems of being not present is nearly equal to those of being not permissioned). Using on-device signals and hardware signing (via octet per the article) is a very interesting solves the legal analysis here - some of the larger fintechs and others have been using such signals for security or fraud usecases for decades. Making such technology more available is highly valuable.

1

1

9

2,250

Jun 10

Congrats to the @honchodotdev team for passing 5K stars.

Honcho is the best solution for memory.

6

4

18

913

Bullish.

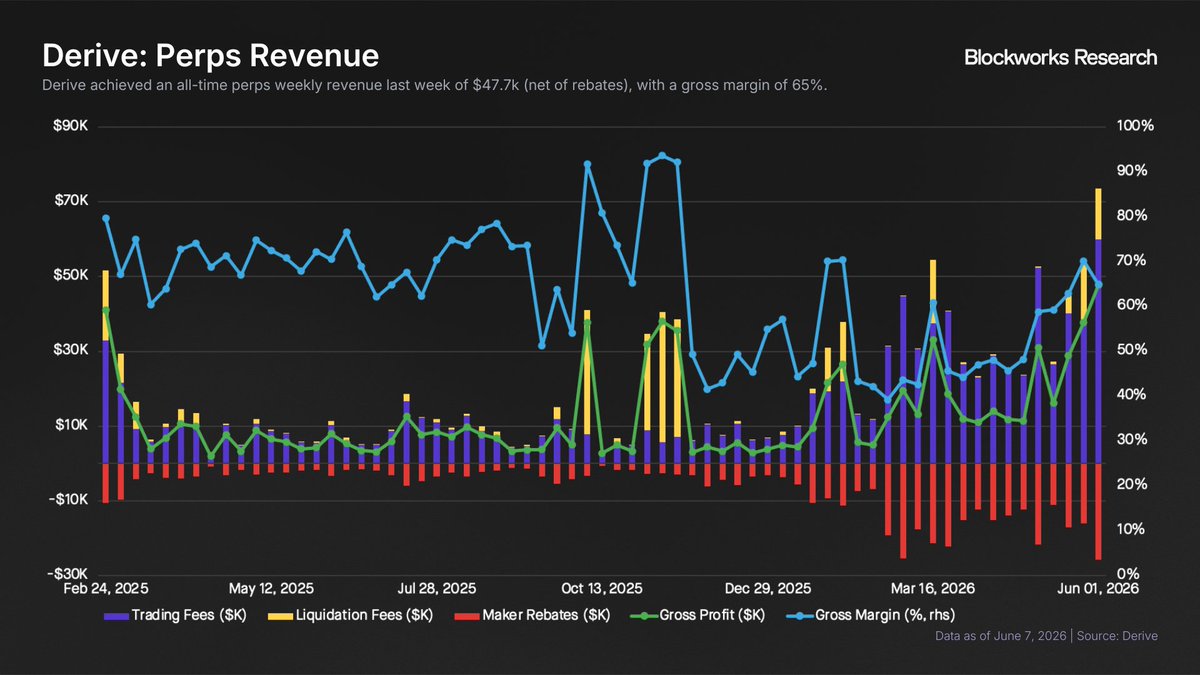

Jun 8

When I wrote about Derive in March, the core thesis was that the protocol was better positioned than at any point in its history: options volumes were reaching new highs, RFQ activity was breaking out, BTC options share vs. Deribit was improving, and HYPE was emerging as proof that Derive could move faster than incumbents on new asset coverage.

The open question was whether that momentum would translate into more durable revenue growth. Last week, Derive generated an all-time high of $110K in weekly revenue, net of maker rebates, across options and perps.

Options remained the most profitable part of the protocol, reaching an all-time high of $62.5K in weekly revenue while maintaining gross margins above 90%. This continues to support the view that options are Derive’s higher-margin product, even as perps become increasingly important to the broader exchange.

Perps also had their strongest week on record, generating $47.7K in revenue net of rebates, with gross margin improving to 65% from below 50% in recent weeks. Some of that was helped by downside volatility, with the past three weeks contributing roughly $35K in liquidation fees.

The volume side tells a similar story. Derive recorded $702M in notional volume last week, its second-highest weekly total over the past year. But the important difference is composition. In March, volume was heavily BTC-led, with BTC accounting for more than 70% of total options and perps volume. Last week, BTC accounted for 46%, followed by ETH at 29% and HYPE at 26%.

HYPE has now become Derive’s most important market after BTC, surpassing ETH in monthly volume in March and accounting for more than 2x ETH volume in May. That said, ETH also saw a notable resurgence last week, breaking $200M in weekly volume for the first time in well over a year.

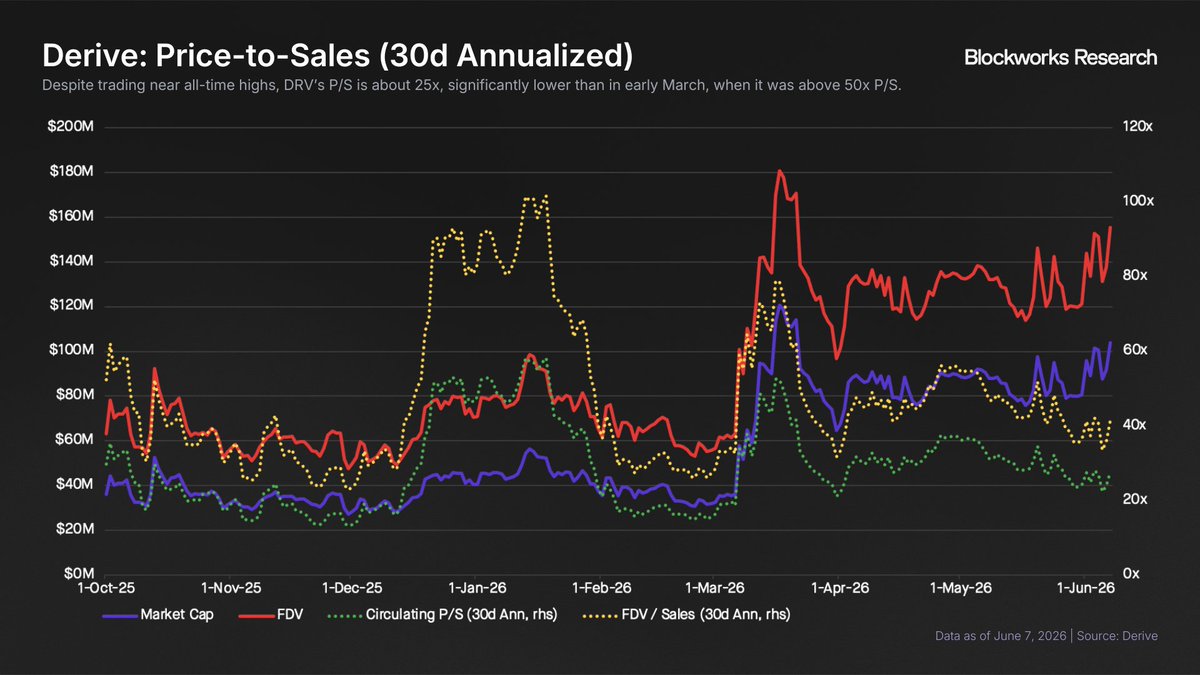

The relative valuation setup has also improved. Despite DRV trading near all-time highs, its 30-day annualized P/S multiple has compressed from above 50x in early March to roughly 25x today. In other words, revenue has accelerated faster than market cap.

There have also been token-level improvements. DRV was listed on Coinbase two weeks ago, improving the asset’s liquidity profile. Derive also completed its B1 token transparency filing in May, further improving disclosure around the token, which remains the only way to gain upside to the protocol’s growth.

Finally, Derive’s late-April governance proposal flipped DRV’s net structural flows from negative to positive. The proposal increased the share of protocol fees used for buybacks from 25% to 35%, while reducing staking emissions from 250K DRV to 100K DRV per week. At current prices, buybacks exceed emissions by roughly $70K per month, more than fully absorbing emission-driven sell pressure.

The case for onchain options remains clear. As crypto markets mature, demand for more sophisticated hedging and structured positioning should continue to grow, and Derive is increasingly leading that charge.

9

584

Daniel Barabander retweeted

Been in these markets for 10 years - today the kind of day which is bearable / high opportunity if and only if you have a fundamentals thesis built from first principles/using your own brain convictions

If you don't have this, take the weekend off and work on one next week

2

3

35

1,163

Daniel Barabander retweeted

Jun 4

For years the tokenized securities permissioning debate has had two unsatisfying answers: whitelisting that breaks UX, or permissionless rails too risk-on for sophisticated issuers. @dbarabander and I have found a third path: proof of location, using onchain geofencing.

1

4

29

1,092

Daniel Barabander retweeted

Jun 4

If you’re building for tokenized securities, you need to read this:

> With an onchain geofence in place, sophisticated issuers could actually issue securities onchain without the whitelist model

6

5

70

21,740

Daniel Barabander retweeted

Jun 4

Really interesting article from @dbarabander and @sabina_beleuz about onchain geofencing - a much-needed technical solution to a really thorny legal problem.

As securities move to blockchains, and a more complicated international legal landscape, we need more onchain solutions.

1

6

23

3,341

Three reasons autonomy is inevitable - not just in crypto.

1. The internet is being rebuilt around agents. Instead of an account with every app, you'll have one agent that acts across services on your behalf. To compose across open APIs, the agent has to hold your assets and identity directly. Self-custody stops being a crypto preference and becomes a structural requirement. Self-custody = autonomy.

2. Technology is solving coordination problems to unlock self-governance. Humans are bad at deciding as a collective, so we've handed decisions to a few fallible people in charge, trading autonomy for efficiency. Technology removes that tradeoff: permissionless markets act as coordination machines that turn participant intents into decisions, and AI can process fuzzy collective context into clean outputs. Self-governance = autonomy.

3. The convenience/control tradeoff is ending. We've always traded relinquished control for convenience - put your cash in a bank so you don’t need to lug it around, sacrifice your privacy for immediate access. But technology is collapsing that tradeoff: clever cryptography can deliver autonomy with no convenience cost. We’ve already seen this with wallets (e.g., Turnkey) and E2EE - it will increasingly be baked in by default, because users will demand it and applications will seek it for faster go-to-market and regulatory arbitrage. More control = autonomy.

1

1

17

1,011

Daniel Barabander retweeted

Jun 2

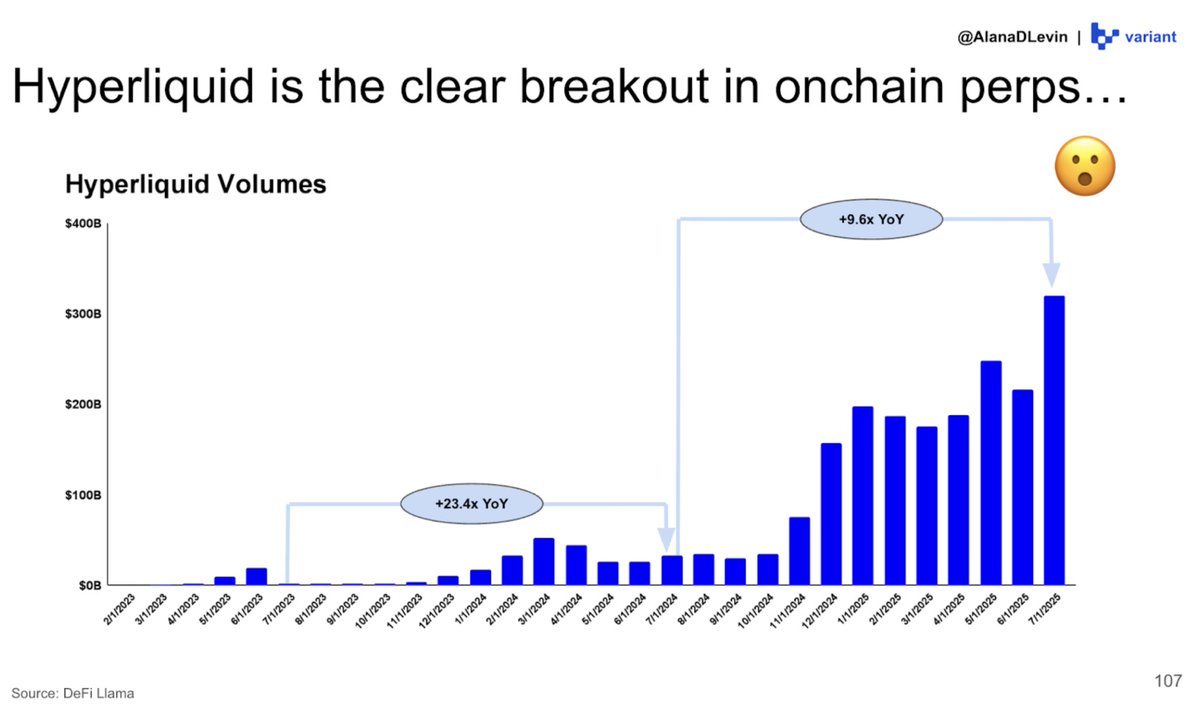

$HYPE continues to cement itself as the leading alt on Derive.

Yesterday:

• $182M notional traded

• 35% of the volume was HYPE

• HYPE surpassed ETH

The dominant alt options market continues to grow.

39

12

115

6,754

May 28

As I've written about before, insider trading = deceptively breaking promises and trading on it.

The promises in this case were formed through standard company polices practically all employees enter into.

That's all the CFTC needed to nail this Google employee.

.@CFTC Charges Google Employee with Insider Trading in Search Result-Related Event Contracts: cftc.gov/PressRoom/PressRele…

1

9

2,100

Daniel Barabander retweeted

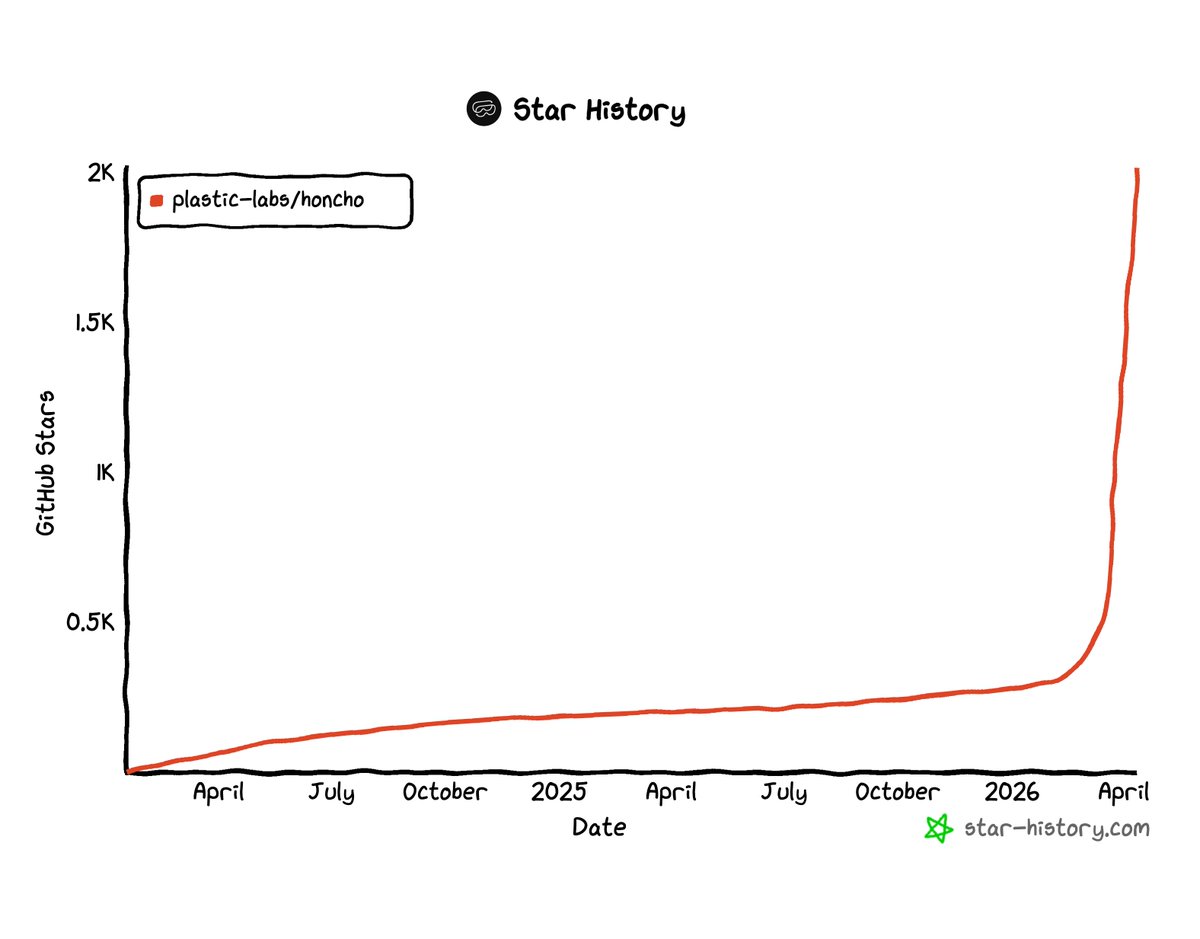

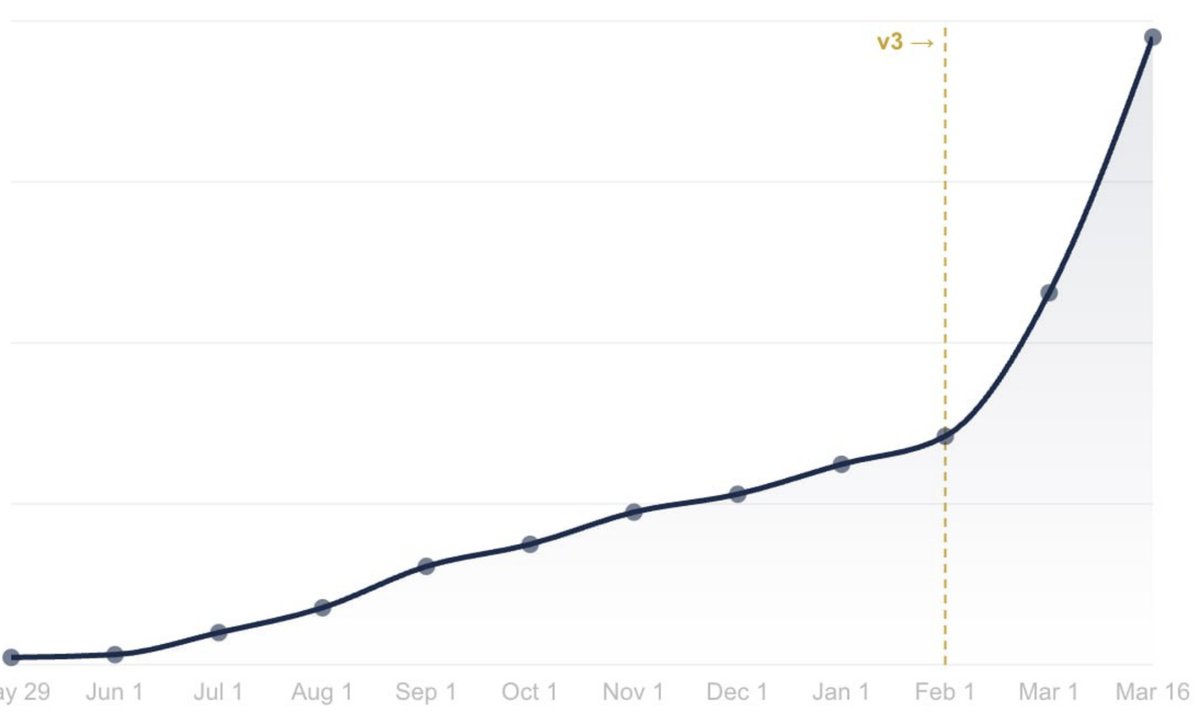

May 26

we went from 1,000 to 10,000 provisioned honcho instances in a month and a half

anyone know killer platform engineers? we can't keep up with the infra demands

4

5

41

5,233

Daniel Barabander retweeted

May 20

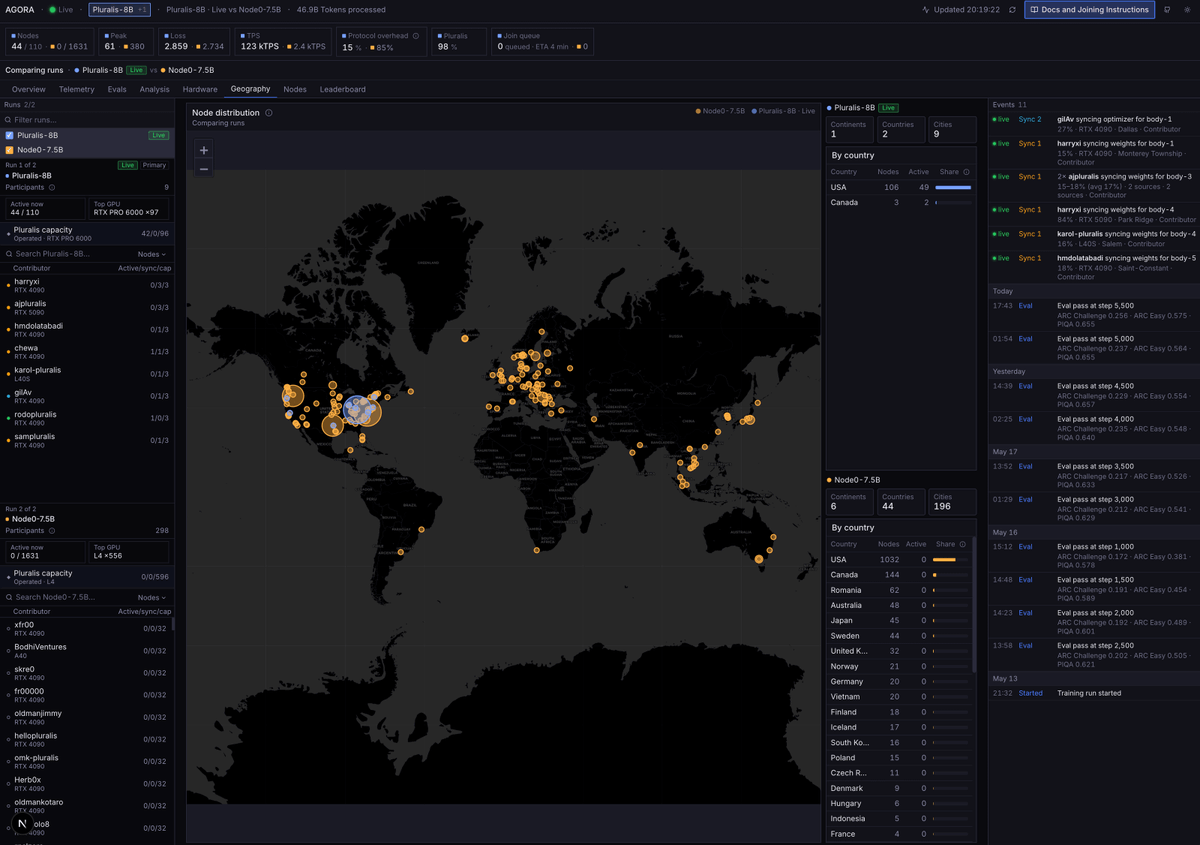

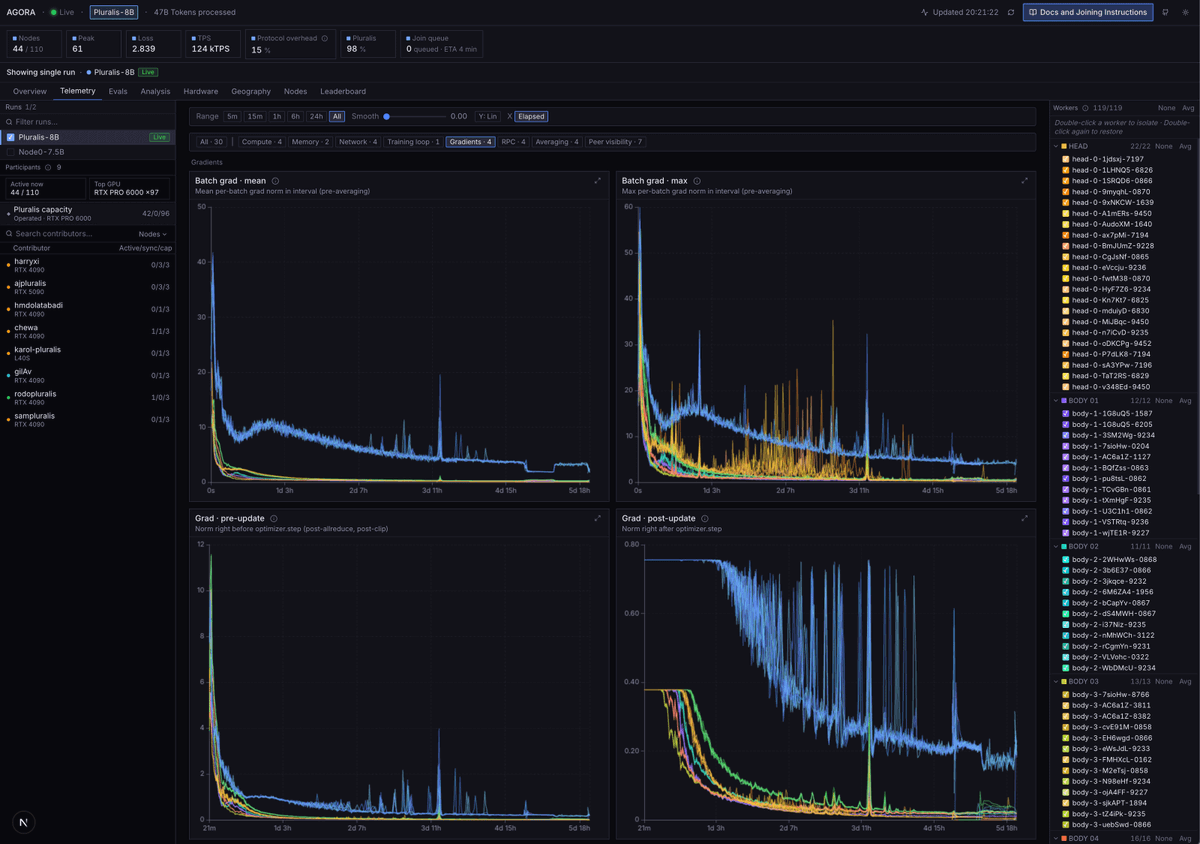

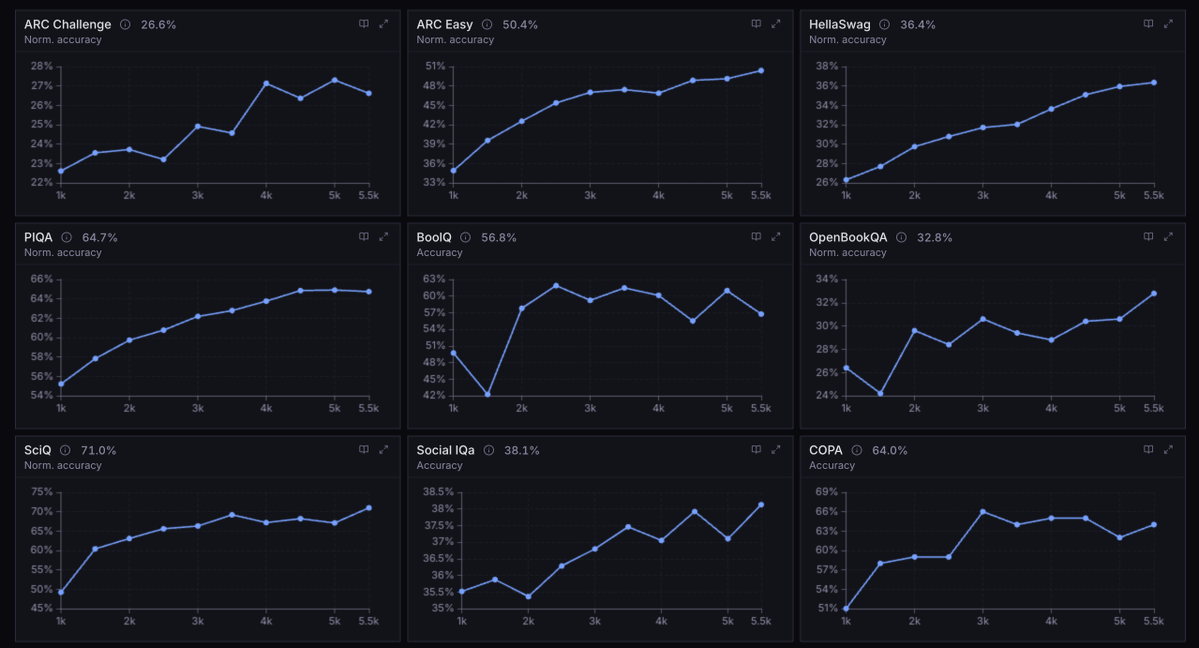

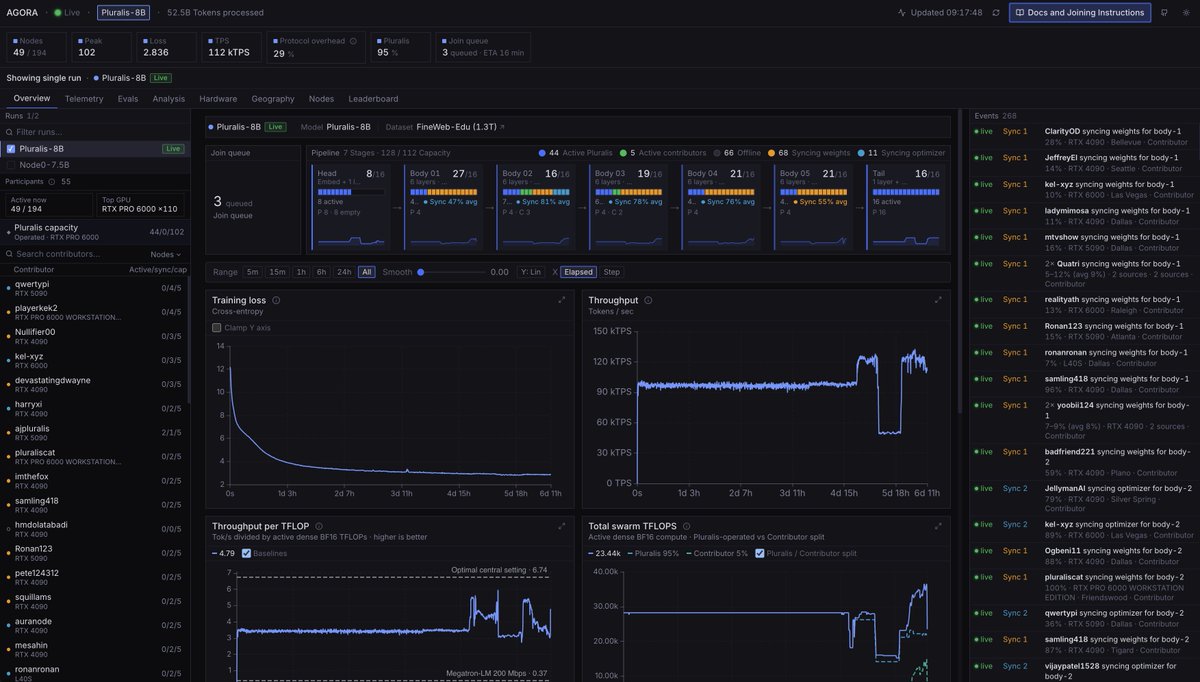

Today we're releasing Agora: the first ever pretraining stack that allows non-collocated consumer GPUs to be competitive with centralized clusters

Agora is 15x faster than Megatron-LM in this setting and is only 1.5x less efficient in terms of tokens per unit compute than TorchTitan on H100s, despite running on devices that have no NVLink or InfiniBand support.

23

42

280

78,440

Daniel Barabander retweeted

May 22

Over the past few weeks I've been using an agent daily

However, it's become increasingly clear that it's not a long term solution. I'm decently suited to hack around, but not to manage hosting and security for an always on, extensible agent

What are the best managed agent services ?

12

1

26

13,797

Daniel Barabander retweeted

May 21

Importantly, a month of 🫡Honcho-powered Hermes usage

Perfect for supplementing the local markdown system

Memory is a reasoning task... and Chuck's just beginning to see the benefits 🚀

May 20

I'm switching to Hermes....

I've been using it for a month.....and I'm sold...moving all of my @openclaw agents to Hermes (@NousResearch)

Why? -----> youtu.be/QQEgIo4Juxg

Thank you to @Hostinger for sponsoring this video!

18

24

489

64,106

Daniel Barabander retweeted

May 21

3

6

28

5,955