6,671 Photos and videos

The biggest lie NFT projects told us wasn't about floor prices.

It was the idea that a JPEG alone could be a business model.

For years, we've watched collections launch with beautiful art, ambitious roadmaps, and communities built entirely on speculation.

Then the hype fades.

Because attention isn't revenue.

That's why the new Wingston NFT collection from @RallyOnChain caught my attention.

Not because it's a free mint.

Because it's attached to a protocol that already works.

Think about it.

Most NFT holders are waiting for utility to arrive.

Wingston holders get utility on day one.

• Stake your NFT and earn RLPs daily

• Unlock VIP access to exclusive, higher-paying campaigns

• Receive a Rally Score boost, one of the most important factors shaping creator rewards and opportunities on Rally

This is Rally's first official NFT collection.

A product NFT.

Not a promise.

Not a concept.

A digital asset connected to an ecosystem with real users, real activity, and recurring revenue.

And somehow it's still a FREE mint.

Want a whitelist spot?

Here's the path:

1. Join and submit to any 3 Rally campaigns

2. Finish inside the Top 425 on the weekly leaderboard

3. Follow @RallyOnChain

4. Whitelist Info rally.fun/whitelist

Simple.

The smartest part?

You're earning while qualifying.

Most projects ask you to spend money to get access.

Wingston asks you to create.

That's a very different philosophy.

I think the next NFT cycle belongs to collections backed by products, not promises.

Agree or disagree ?

13

2

51

2,734

Everyone assumes AI will level the playing field so anyone can produce great work fast.

I think it will do the opposite.

The flood of similar sounding output is going to make anything that still carries the texture of one person's real obsessions and rough edges stand out like nothing else.

People who protect their own thinking instead of outsourcing the hard parts to a model will end up with the only work that feels worth paying attention to.

Have you started noticing how samey the AI assisted pieces feel next to the ones with actual friction left in them? @RallyOnChain

7

5

7

1,296

The Future of Finance: Embrace Automation with NomismaNetwork

As the DeFi landscape evolves, the necessity for manual transaction management fades into the past.

Enter automation a revolutionary force that transforms predefined conditions into seamless actions, enhancing efficiency and eliminating delays.

With @NomismaNetwork, we are stepping into a new era where automated financial processes operate natively onchain, creating an optimized environment for both applications and users.

Why Automation Matters:

Minimized Human Involvement: Reducing the risk of errors and freeing up valuable time for strategic thinking.

Boosted Operational Efficiency: Streamlined processes mean quicker transactions and improved user experiences.

Empowered Financial Innovation: Unlocking the potential for more sophisticated applications that can adapt and respond to market dynamics.

The future of DeFi is not merely transactional; it's about intelligent systems that autonomously execute financial activities.

Join us on this exciting journey with NomismaNetwork and be part of the transformation!

Discover more at .

@perx_trade, @quipnetwork @TheARCTERMINAL

20

1

24

126

My weekend plan is pretty simple:

- engage with my mutuals today

-Hit 90k followers on X today

- Make 6 figs on stake or sporty

what about you? what are your plans for the weekend?

Jun 13

my weekend plan is pretty simple:

- engage with my mutuals today

-grab some good food

- get plenty of sleep since i don't have a boyfriend to visit.

what about you? what are your plans for the weekend?

8

2

16

226

In 1970, banks refused to join CHIPS the U.S. large value interbank settlement system until the Fed guaranteed that other participants couldn't see their transaction positions.

The technology worked.

The confidentiality of architecture wasn't there yet. Banks waited.

That's not a blockchain story.

That's a 55 year old constraint that still determines which settlement infrastructure regulated banks actually use.

@zksync thread on why 2026 is when this constraint gets resolved in production and what that unlocks:

The April 2026 GFMA report listed four things institutional onchain finance still needs to resolve: interbank interoperability for tokenized deposits, transaction privacy, RTGS-equivalent settlement, and digital money governance.

These look like parallel problems. They're not.

Privacy gates the other three. No treasury team moves real balance sheet exposure onto shared rails where counterparties can see their positions, strategy, or active trades. Compliance constraints don't yield to good technology in every other dimension. They just block adoption until the specific constraint gets solved.

This is why institutional blockchain deployments stalled at proof of concept for years despite working mechanics. The privacy architecture wasn't there. Configurable permissions on top of transparent infrastructure don't satisfy a compliance requirement that says transaction data must not be visible by default.

The architectural answer to that constraint is not a setting. It's a default.

@zksync runs institution controlled private execution environments. Each institution operates inside its own environment. Only zero-knowledge proofs and state commitments publish to Ethereum. No counterparty sees positions or transaction data.

This isn't privacy as a feature layered onto transparent infrastructure. The network's default state is that transaction data isn't visible. Selective disclosure for auditors and regulators is built in. But the default protects the institution.

That distinction matters for compliance teams in a way that performance improvements don't. A compliance officer can't sign off on "we will hide your data unless someone gets the key." They can sign off on "your data was never visible to begin with."

This isn't theoretical. These institutions are in production now:

Deutsche Bank's DAMA 2.0 tokenized fund platform (Memento) first tier-one global bank live on ZK infrastructure.

ADI Chain live with First Abu Dhabi Bank, Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton.

Cari Network tokenized deposit network for Huntington, First Horizon, M&T Bank, KeyCorp, and Old National Bancorp. $600B in combined deposits. Founded by the 27th U.S. Comptroller of the Currency.

30 institutions in active engagement across U.S. and international banks, central banks, and sovereign currency issuers.

Market context: JPMorgan Kinexys has crossed $1.5T on blockchain rails. DTCC is advancing SEC cleared Treasury tokenization. 93% of tokenized U.S assets settle on Ethereum.

The tokenized RWA market is at $29B and growing.

The first regulated deployments built around architectural privacy become the interoperability baseline the second wave has to meet.

The network effect in settlement is real. 10 institutions create 45 settlement corridors. 100 create nearly 5,000.

But in institutional settlement specifically, that compounding only accelerates once the privacy constraint clears.

Before it clears, each new institution joining shared rails creates counterparty exposure risk for every existing participant. After it clears each new institution adds corridors without adding risk.

That's the unlock that makes 2026 different from 2019-2023. Working technology existed in all those years. Architectural privacy at production scale, with live regulated deployments, didn't.

CHIPS took 4 years from launch to reach critical mass after the Fed resolved the confidentiality question.

11

4

14

3,583

The institutions that joined early shaped how every subsequent participant had to connect.

For people who've worked inside correspondent banking or large-value settlement infrastructure: do you think the privacy architecture or the interoperability standards are harder to standardize across institutions? I think the answer determines which platform the second wave defaults toward.

1

49

The institutions that joined early shaped how every subsequent participant had to connect.

For people who've worked inside correspondent banking or large-value settlement infrastructure: do you think the privacy architecture or the interoperability standards are harder to standardize across institutions? I think the answer determines which platform the second wave defaults toward.

1

48

Dee 🏕️ retweeted

Jun 12

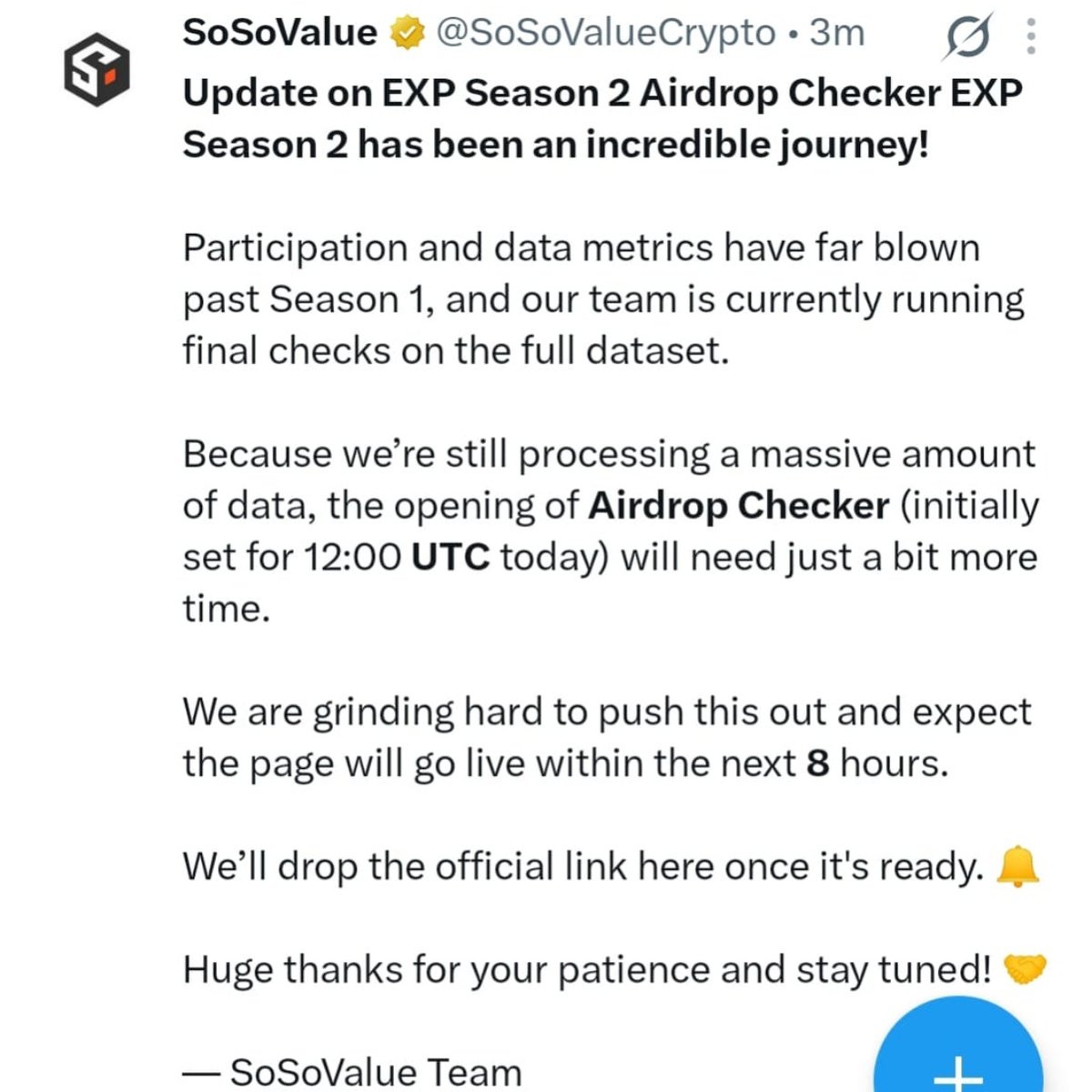

My allocation with over 60M exp. Lol.

just move on from soso, avoid their season 3.

anyone with huge allocation is obviously a partner.

71

7

263

18,653

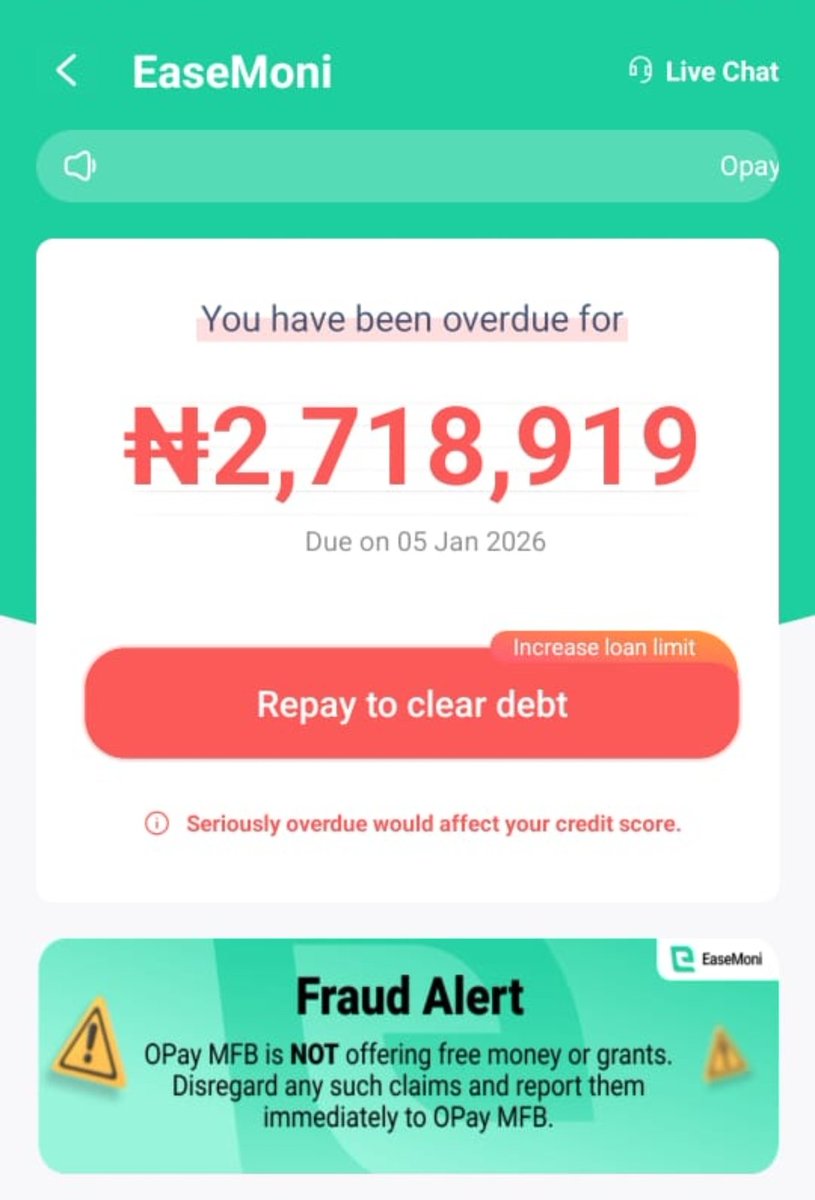

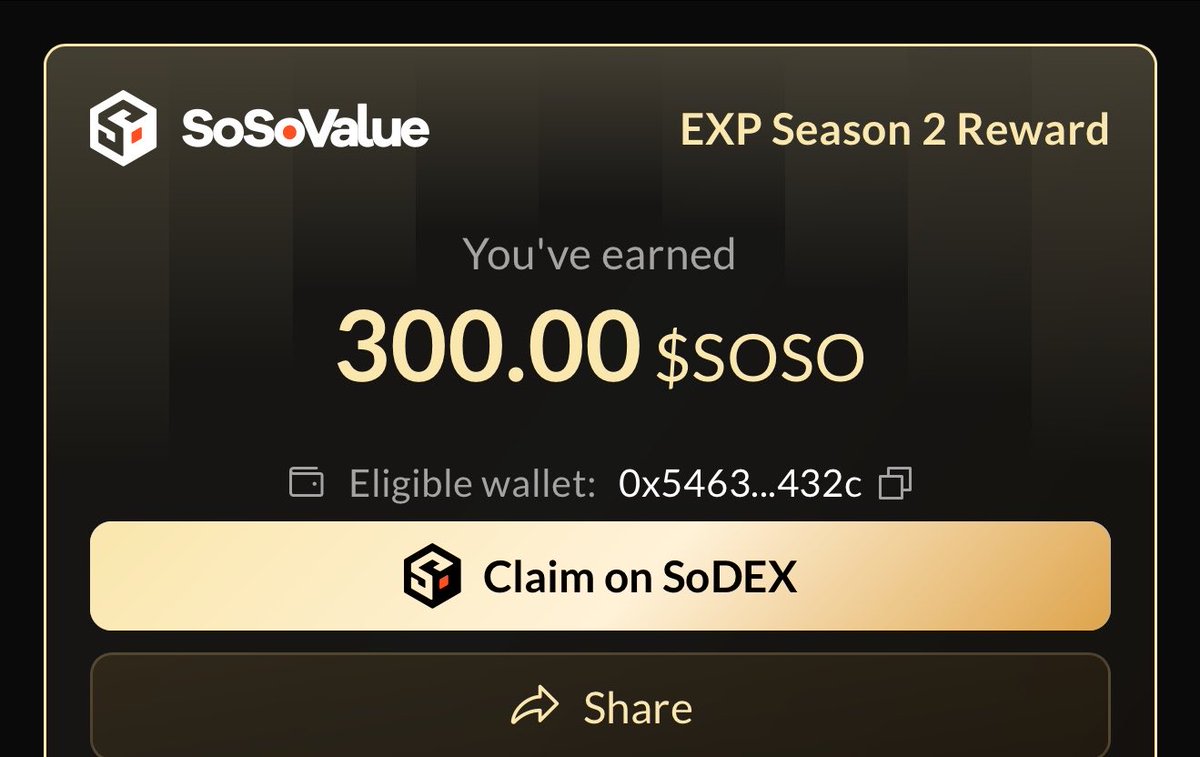

How we won pay debt of 2m☹️with 3$

I don collect loan to make deposits for the car I want to buy.

actively waiting 7 hours for @SoSoValueCrypto airdrop claim so I pay the balance ..

Wish me luck 🙂↔️🤭

2

1

4

148