Joined October 2018

- Tweets 21,426

- Following 287

- Followers 5,265

- Likes 8,602

3,201 Photos and videos

Pinned Tweet

1 Mar 2024

For the next time I forget, there is no price too low for value stocks and no price too high for growth stocks.

2

1

29

21,711

If this is the end of the war, and the terms are what's been speculated recently, the TLDR would be: Trump but off more than he could chew and surrendered.

1

2

391

Jun 14

Media is reporting on the draft deal between the U.S 🇺🇸 and Iran 🇮🇷 and the anticipated outcome

3

485

Maybe... $NXR.UN

Looks like it's strengthening?

Discount to NAV

Internally managed

Nice yield.

1

6

450

Trump: There should be no more strikes by Israel in Lebanon, but no further attacks by any group, including Hezbollah, against Israel

1

333

The benefit of the Canadian forced savings (CPP) is that many people are financially irresponsible and would wind up in this position if not protected from their own lack of impulse control.

Jun 12

I am 52 years old. I have been working since I was 15 years old. I have no savings, no retirement, and will never own a home before I die.

And there is now a trillionaire.

3

18

1,859

Basically:

Trump wants: Straight open

Iran wants: Terror by proxy allowed but retaliation not allowed

Israel wants: Safety

1

5

476

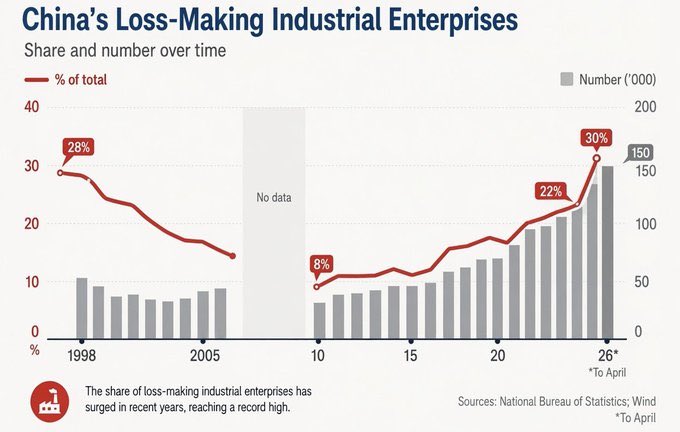

So basically the state is subsidizing 1/3 of the industrial companies in China...

Jun 12

This chart is also one of the clearest visual representations of what Chinese policymakers increasingly describe as “involution” (内卷).

Involution occurs when competition becomes so intense that participants work harder, invest more capital, build more capacity, and cut prices more aggressively, yet everyone earns lower returns. Activity increases, but value creation does not. That is exactly what this chart appears to show.

China’s industrial sector continues to produce enormous volumes of goods, but profitability is collapsing. The share of loss-making industrial enterprises has surged to 30%, while the absolute number of loss-making firms has reached a record high. In other words, more companies are competing than ever before, but a growing percentage of them are failing to earn adequate returns.

This is the classic involution dynamic. Instead of weaker players exiting the market, firms continue operating, often supported by local governments, state-owned banks, strategic objectives, or the simple need to maintain employment. As a result, excess capacity persists. Companies respond by cutting prices. Competitors then cut prices further. Market share becomes more important than profitability. Everyone runs faster, but few move ahead.

The EV sector is perhaps the best example. China has built the world’s most competitive electric vehicle ecosystem, yet pricing pressure has become so severe that many manufacturers struggle to generate sustainable profits. Similar patterns can be observed across solar panels, batteries, chemicals, steel, industrial equipment, and numerous manufacturing sectors.

From a macro perspective, involution is deeply deflationary. When companies are trapped in price wars, they lose pricing power. Falling margins suppress wages, reduce investment returns, weaken business confidence, and ultimately slow household income growth. The result is an economy where supply keeps expanding while demand struggles to keep pace.

This also explains why China’s export push has intensified. Excess capacity that cannot earn adequate returns domestically naturally seeks demand abroad. What China experiences as involution internally is increasingly being exported to global markets through lower-priced goods and rising trade surpluses.

The deeper issue is that involution is not merely a cyclical phenomenon. It is often the consequence of an economic system where capacity creation is rewarded more than profitability. Companies continue investing because competitors are investing. Local governments continue supporting industries because neighboring provinces are doing the same. Capital continues flowing into sectors despite falling returns because strategic priorities outweigh market signals.

The result is an economy that becomes exceptionally efficient at producing things but increasingly struggles to generate acceptable returns on the capital invested.

Viewed through that lens, the rise in loss-making industrial enterprises is not simply a profitability statistic. It may be one of the strongest pieces of evidence that China’s involution problem is becoming more severe. The country is producing more, investing more, and competing harder than ever, yet an increasing share of firms are losing money. That is almost the textbook definition of involution.

3

701

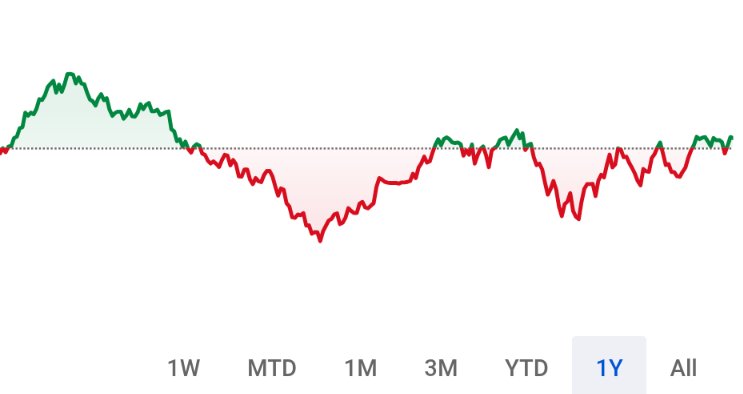

International Growth account flat since late January & YoY

Higher expected returns than where it was a year ago though.

1

4

877

Tough to estimate what might work when but I think the pieces are in place for a 30% ROE to be in the realm of realistic over the next year.

We'll see I guess.

473

If 3i could redeploy 100% of their Action distributions back into increasing the stake (unlikely) it would own the whole company in ~4 years.

If they can't it could mean deployment of capital greater than their current portfolio excluding Action.

2

3

877

This is why I don't think CAPE is a good metric in markets left by secular growers

423

Man... This was really stupid

11 Nov 2025

Sold my CIBC $CM.TO

Too rich for the opportunities in this market.

3

9

3,007

I seem to do this frequently...

Buy ok on a normalization thesis... Sell at normalish average... Company laughs at me and keeps going... Because average is average not expensive.

2

5

339

I hope all the people saying SpaceX is worth more than Canada invest 100% of their portfolio in it...

1

11

926

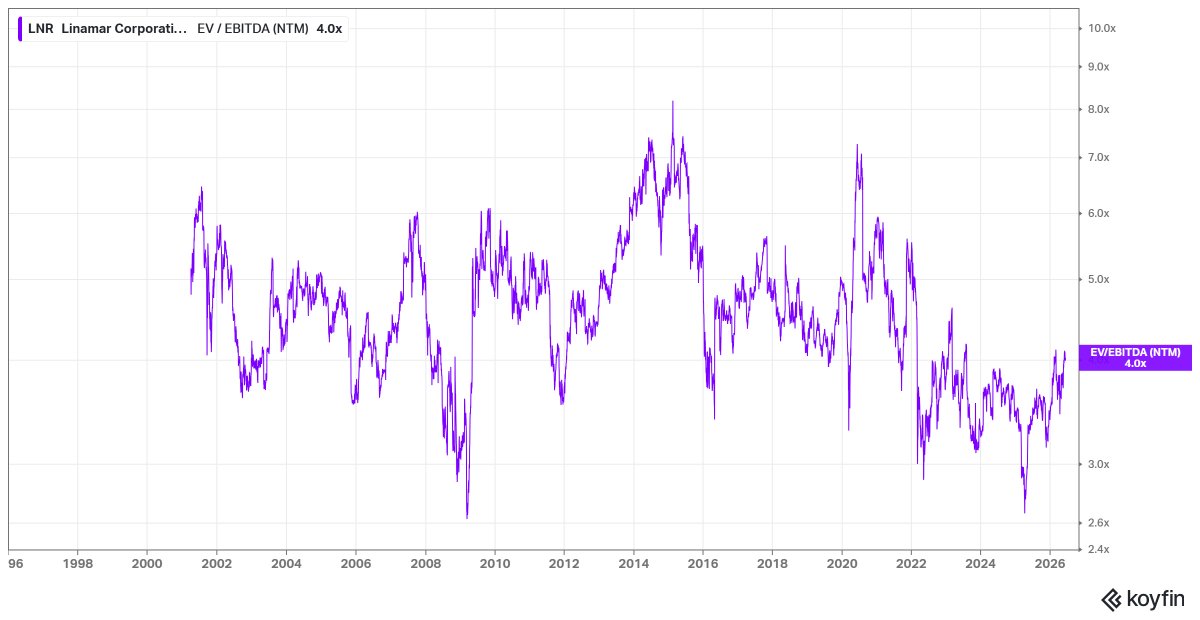

Was reflecting on Linamar: has it moved too much?

While a consolidation is technically healthy at most points, still looks like it's trading near 3.5x year end EV/EBITDA which is basically the multiple they're paying for distressed assets.

2

7

1,957

Prior to 2022 the normal range was 3.5-6x forward EV/EBITDA

At current price, Year end 2026 would be ~3.5

1

225

Not the best metric for capital heavy businesses but an ok one for some rollups that can deploy some leverage into acquisitions where the biz structure includes intangible amortization (~1.50/share)

186

Wouldn't be shocked if the medium term top in the space sector happens within a few days.

Big run up in anticipation. With multiples way up... And fell flat on what was the hype catalyst.

1

348

Top 4 positions account for 53.77%

Next 7 account for 28.56%

Last ~25 account for 17.67%

5

711