Backing early-stage teams @nascent

Joined March 2009

- Tweets 10,089

- Following 2,277

- Followers 25,156

- Likes 58,773

631 Photos and videos

Dan Elitzer retweeted

May 21

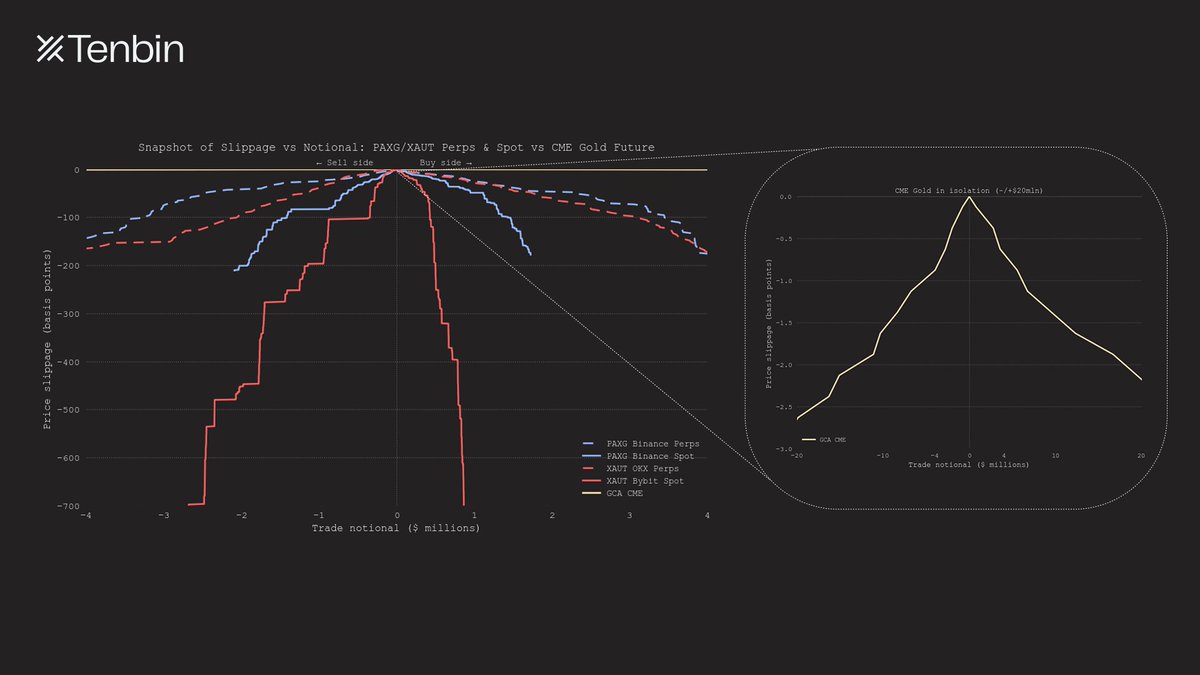

Tenbin's first asset is live.

Introducing Tenbin Gold (tGLD): Liquid, Yield-bearing Tokenized Gold.

Built for instant on-chain liquidity with DeFi utility.

app.tenbinlabs.xyz

46

34

176

35,573

Dan Elitzer retweeted

May 21

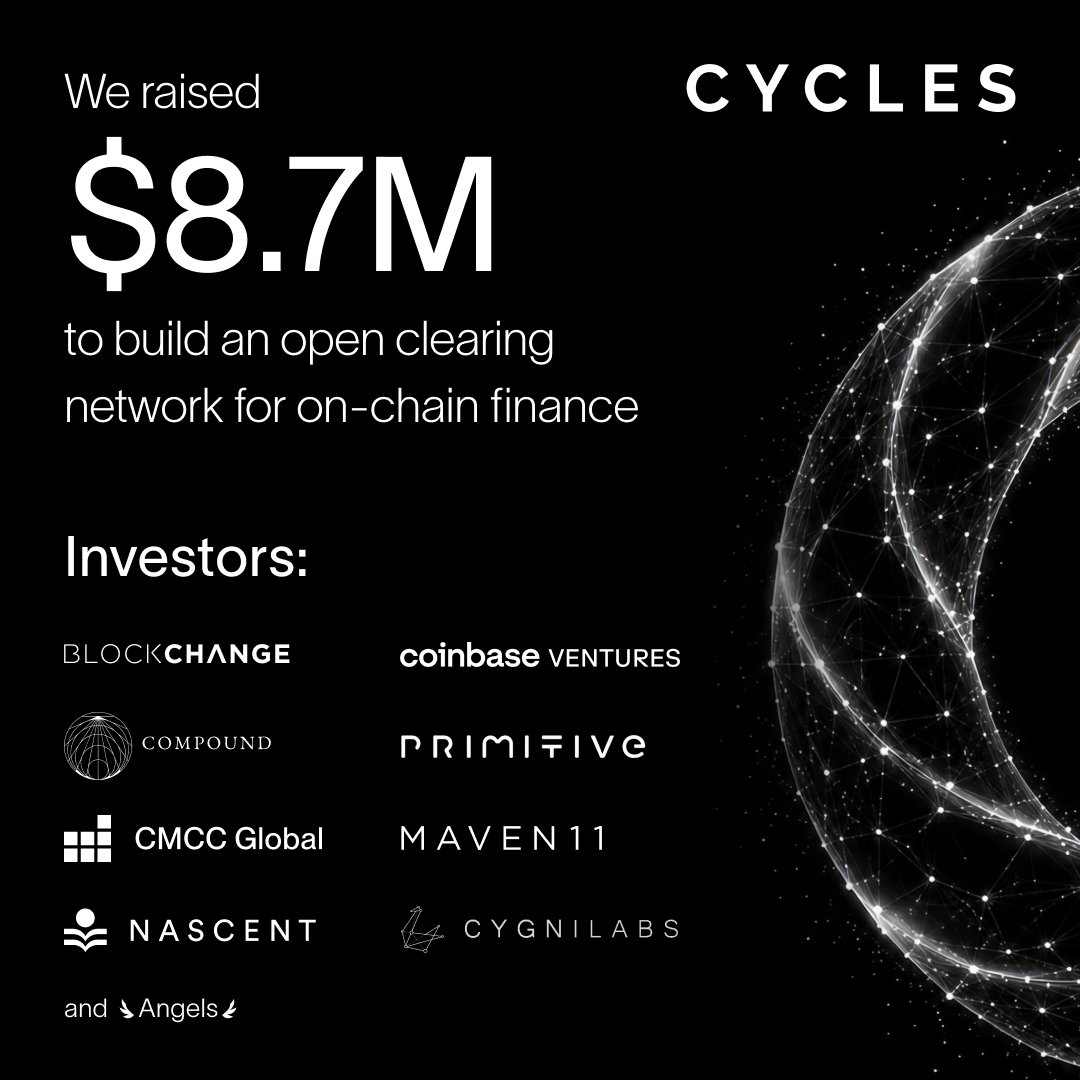

We’ve raised $8.7M to bring clearing to the masses. Our new round was led by Blockchange to work on the most powerful idea in finance.

It’s not just about moving money faster & cheaper; it’s about moving less while doing more.

64

76

531

109,186

May 14

Talking to Paul during diligence on Morpho’s pre-seed in 2021, one of our big questions was what happens if the Optimizer gets so widely used that it effectively drains the underlying protocols.

Paul’s answer at the time: they already knew what they’d build next, and they’d have their own markets underneath. He also understood very clearly back then that the end state for lending was going to be something closer to an order book.

Morpho Optimizer was necessary to bootstrap and get to Morpho Blue. Morpho Blue was necessary to get to Morpho Midnight.

What’s really cool is that, as Paul describes in his post, you can use Midnight and Blue together via the callback feature to get the best of the original Optimizer while still keeping the benefits of the pooled liquidity variable rate model that people have gotten so used to and that’s still genuinely useful in a lot of situations.

Over time, I expect more liquid markets to develop around Midnight loans, and they’ll take a larger and larger share of all lending volume.

Incredible how visionary the @Morpho team has been since Day 1, and what a thoughtful, clean transition to more efficient markets their architecture has enabled.

May 13

Oh wow, lots of memories from Morpho Optimizer. This made me want to share a few stories about the original story, vision, and name of Morpho.

Morpho Optimizer was Morpho’s first version (now deprecated). It grew to $ 1B in deposits and kicked everything off for us.

The idea was simple: we built a peer-to-peer matching layer on top of existing lending pools to optimize rates for lenders and borrowers, while piggybacking their liquidity.

At the time, the vision was to progressively evolve the Morpho Optimizer matching engine so it would rely less and less on the pool model as a fallback, but on active participants, until one day it could metamorphose: from the little caterpillar living inside the apple into a beautiful independent butterfly flying on its own.

That was already in the original 2021 whitepaper. And yes, that is why we are called Morpho (at least the main reason).

That said, we had to pause that vision because we had one big realization: the biggest problem in lending markets was not just capital efficiency. It was resiliency.

As one of the largest integrators of lending pools, we got to experience firsthand what it meant to build a multibillion-dollar integration on top of DeFi infrastructure. And honestly, it felt to risky to support global financial infra.

That is why we built Morpho Blue: immutable and simple code, isolated lending markets, infrastructure that gives integrators control, and a lending stack that can actually scale safely.

BUT: Morpho Midnight brings us back to the original vision of Morpho Optimizer: becoming fully free from legacy constraints and building a true market for credit.

Midnight also has a very powerful feature called callbacks: it lets lenders and borrowers use pools "as they wait for a peer-to-peer match"

This is what I was secretly most proud of in Morpho Midnight: it is both the ultimate vision of both Morpho Optimizer and Morpho Blue at the same time

6

2

101

18,138

Dan Elitzer retweeted

May 13

Apple patched a 13-year-old bug in WebKit yesterday.

Apex, Cantina's autonomous AppSec agent, found it.

It's one of three Apex findings in the same release. Two are CSP bypasses.

Full writeup: cantina.review/ze5

10

514

487

2,238,865

Dan Elitzer retweeted

May 13

Oh wow, lots of memories from Morpho Optimizer. This made me want to share a few stories about the original story, vision, and name of Morpho.

Morpho Optimizer was Morpho’s first version (now deprecated). It grew to $ 1B in deposits and kicked everything off for us.

The idea was simple: we built a peer-to-peer matching layer on top of existing lending pools to optimize rates for lenders and borrowers, while piggybacking their liquidity.

At the time, the vision was to progressively evolve the Morpho Optimizer matching engine so it would rely less and less on the pool model as a fallback, but on active participants, until one day it could metamorphose: from the little caterpillar living inside the apple into a beautiful independent butterfly flying on its own.

That was already in the original 2021 whitepaper. And yes, that is why we are called Morpho (at least the main reason).

That said, we had to pause that vision because we had one big realization: the biggest problem in lending markets was not just capital efficiency. It was resiliency.

As one of the largest integrators of lending pools, we got to experience firsthand what it meant to build a multibillion-dollar integration on top of DeFi infrastructure. And honestly, it felt to risky to support global financial infra.

That is why we built Morpho Blue: immutable and simple code, isolated lending markets, infrastructure that gives integrators control, and a lending stack that can actually scale safely.

BUT: Morpho Midnight brings us back to the original vision of Morpho Optimizer: becoming fully free from legacy constraints and building a true market for credit.

Midnight also has a very powerful feature called callbacks: it lets lenders and borrowers use pools "as they wait for a peer-to-peer match"

This is what I was secretly most proud of in Morpho Midnight: it is both the ultimate vision of both Morpho Optimizer and Morpho Blue at the same time

May 13

Who remembers Morpho Optimiser?

Here's how you'd build a better one on Euler today. 👇

And create an interest rate swap market on top.

What does an Optimiser do?

On most lending protocols there's a spread between the lend and borrow rate. It emerges primarily because of the target 90% utilisation rate, which leaves breathing room for lenders to withdraw, and partly because of the protocol fee on borrower interest (typically 10% if the fee switch is on).

Borrowers pay 5%.

Lenders earn 0.9 * (1 - 10%) * 5% = 4.05%.

An Optimiser matches lenders and borrowers peer-to-peer somewhere in the middle where possible, and reverts to the variable rate pool when not.

Borrowers pay 4.5% (10% cheaper).

Lenders earn 4.5% (11% more yield).

Both are strictly better off if they can lend and borrow peer-to-peer.

Extra yield

It can get even better for borrowers on Euler than on a vanilla Morpho market.

The collateral they deposit sits in an Euler vault rather than idle, and can earn yield via cross-collateralisation when there's demand to borrow it.

For example, a borrower posting WETH as collateral for a USDC loan can have that WETH lent out to wstETH holders looping to capture LST yield. The WETH interest then offsets the cost of the USDC loan.

If that yield runs at even 1%, the effective borrow cost drops to 3.5%, a 30% reduction over regular Morpho market borrowing. 🤯

How to build

So how do you build this on Euler today?

Lenders deposit USDC into an Euler Earn vault. The Earn vault has two strategies: Morpho USDC/WETH (variable rate), and an Euler USDC/WETH P2P vault.

We'll call the P2P vault's shares eUSDC-P2P.

When a borrower takes out a new loan they always borrow from the P2P vault, which pulls deposits just-in-time from the Morpho market.

Similarly, when lenders withdraw, liquidity is preferentially pulled from the Morpho market.

The P2P vault gets its rate (call this the matched rate) by reading the IRM on the Morpho market and splitting the spread between lenders and borrowers.

It can do this because it's designed to be 100% utilised at all times. Effectively a pool of P2P loans. When a borrower repays, the excess deposits are pushed back into the Morpho market.

Parasitic?

The Optimiser and its host have a parasitic relationship. A rational lender or borrower should always migrate to the Optimiser, all else equal including risk. The host becomes wholesale backstop liquidity while the Optimiser captures the prime matched flow. Its economics degrade and the pool drifts towards full utilisation, where it becomes structurally fragile.

Morpho Optimiser was originally built on top of Aave's monolithic pool. Morpho's own isolated markets are now liquid enough to be vulnerable to the same dynamic. I say vulnerable, because parasites can kill their host given a long enough time frame.

When Morpho first built on Aave, the Aave team were delighted they had a new integration. They didn't realise Morpho Optimiser was silently hurting them. Every matched borrower was a borrower whose interest no longer flowed into Aave's pool. Utilisation drifted up, rates got more volatile, and Aave was carrying the tail risk while Morpho Optimiser took the benefits.

It's a vulnerability all variable rate pool models share.

The fix: a secondary market for pool exits

The solution, in my opinion, is liquid secondary markets for pools. You need an interest rate swap market, so people can exit a variable rate pool via a swap instead of a withdrawal, just like exiting a bond early.

Fortunately you can build this on Euler too, thanks to a feature that allows any ERC-4626 compatible vault on Euler to be accepted as collateral for any other.

Introduce a new Euler variable vault, call it eUSDC-variable, that cross-collateralises the P2P vault. You can deposit eUSDC-P2P shares and borrow USDC from eUSDC-variable, or vice versa. Since the underlying asset is identical (USDC on both sides, with eUSDC-P2P just being a yield-bearing USDC claim), the LTV can be set extremely high. 95% is realistic.

The main difference is duration risk: matched and variable rates can diverge, so the share values drift apart.

Two things become possible.

First, anyone stuck in the P2P pool can borrow themselves out without waiting for a withdrawal. They deposit eUSDC-P2P as collateral, which earns the matched rate, and borrow USDC from eUSDC-variable, which pays the variable rate. Net carry per second is matched minus variable. They've swapped an illiquid matched position for a liquid variable one, paying only the spread.

Second, anyone with a view on the spread can take a highly leveraged position on it, going long or short, by swapping into and out of the two pools on leverage. You're trading the interest rate market directly.

Pretty neat, huh?

I left Euler back in January and my understanding is that the Euler team have plenty to be getting on with right now, so I don't expect this to be built by them any time soon.

But if anyone fancies giving it a go, I have a vibe-coded prototype ready to share.

Matched vault, custom IRM, EVC borrow router. About 30 lines of actually novel code on top of existing Euler and Morpho infrastructure.

DM me if you want a look.

The original Morpho Optimiser is what put Morpho on the map. No reason a successor couldn't do the same for someone else.

6

6

98

44,102

Dan Elitzer retweeted

May 4

Stablecoins

Dollars

Gold

Robux

Bitcoin

Birkin bags

Memecoins

Pokemon Cards

Whatever you call money, Blink will let you use it.

Join the waitlist blink.cash

31

23

125

310,517

Dan Elitzer retweeted

Apr 29

For a long time, people have conflated 'DeFi' with 'trustless finance.'

But 'only-up' technology doesn't exist. Claiming you'll never take a loss and will always have liquidity is foolish, if not dangerous.

In 2023, I wrote 'The Two Paths Ahead for DeFi: Decentralized Brokers vs. Protocols.' The core idea: what can be trustless isn't the finance/brokerage part. It's the tech, the infra, the protocol.

Finance is fundamentally probabilistic. When you finance people, risk is the product. The technology, though, can be deterministic.

This is this observation that led to launch @Morpho Blue as permissionless and isolated lending infrastructure.

DeFi is not a product. DeFi is infrastructure. Infrastructure that should empower existing underwriting models and bring them onto an open network, fostering more competitive pricing and better accessibility for end users. That's it.

23

11

148

11,757

Apr 23

Given the increasing prevalence of this type of supply chain attack, starting to feel like users should delay software updates on everything except OS and browser

Apr 23

🛑 WARNING: Bitwarden CLI was compromised in a supply chain attack.

@bitwarden/cli@2026.4.0 included malicious code after attackers hijacked GitHub Actions, stole secrets, and pushed a tampered version to npm.

🔗 Learn how the attack worked → thehackernews.com/2026/04/bi…

3

3

40

12,385

LIVE NOW - The $280 Million DeFi Exploit That Changes Crypto Forever

A $280 Million DeFi exploit exposed the hidden fragility of crypto’s most trusted systems.

@delitzer and @odysseas_eth break down:

- how the attack happened,

- why bridge risk and protocol composability made the damage so severe,

- what Arbitrum’s intervention means for immutability,

- and why DeFi now needs an aerospace-grade security mindset to survive the AI era.

Enjoy the episode.

--------------

TIMESTAMPS

0:00 Intro

0:57 Worst DeFi Hack Ever?

7:01 What Happened?

10:11 How Sophisticated?

11:42 Explaining the Hack to TradFi

16:51 Who’s to Blame?

22:13 L2 Architecture Consequences

28:17 How Does it Get Resolved?

31:46 Circuit Breakers & Rate Limiters

34:05 AAVE V4

34:51 Arbitrum Intervention Implications

42:02 Code is Law vs Human Governance

51:59 Stage 1 vs Stage 2 Rollups

55:29 Post-Hack DeFi

1:03:05 Aerospace Level Security

1:09:49 Will DeFi Survive?

1:14:33 Closing & Disclaimers

8

8

50

9,682

Apr 22

Rate limits, circuit breakers, and clear dashboards like this need to become standard practice across all protocols

Well done @flyingtulip_ @AndreCronjeTech & @DunkingSquirrel!

Apr 22

Circuit Breaker: A rate-limiting safety mechanism that throttles withdrawals and outflows to contain the blast radius of an exploit.

I built a dashboard to track the Circuit Breaker on @flyingtulip_ by @andrecronjetech , a programmatic safety module for DeFi where lenders are protected just as much as borrowers.

ftcircuitbreaker.com/

15

5,474

Dan Elitzer retweeted

Apr 21

Odysseus says DeFi needs circuit breakers like traditional markets have.

"In traditional finance, a hack is a financial event. You have meetings, you fix the ledger."

"In crypto, a hack is a physics event. It happened. You can't drop into a meeting and fix it."

"Circuit breakers are going to be a vital piece of security infrastructure."

Apr 21

TradFi has had rate limits and velocity controls for decades. DeFi hasn't. Rob Hadick says that changes now:

"It makes absolutely no sense for someone to deposit a full port — 300 million — in one shot. That makes no sense."

"Doing things like rate limits — that's gonna be standard from here."

5

12

35

26,707

Dan Elitzer retweeted

Apr 19

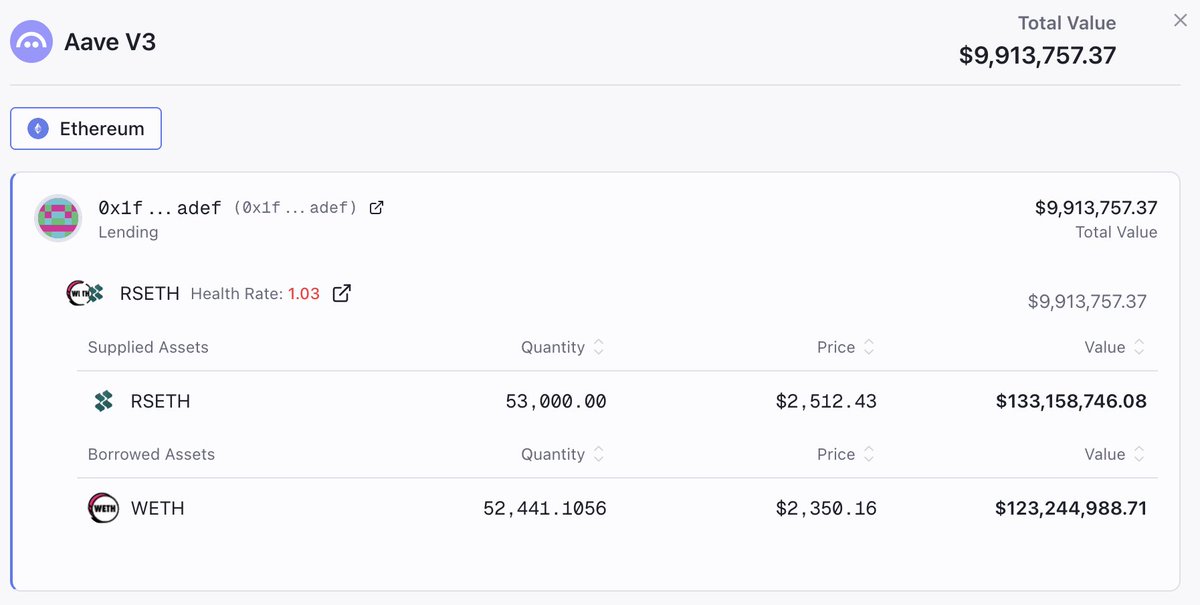

As a follow up to the recent events involving Kelp DAO, I want to reiterate the following:

- Morpho smart contracts are safe and continue to operate as intended.

- The exposure was limited with curators taking preemptive measures immediately.

- Only ~$1M of ETH is borrowed against rsETH as collateral, across two isolated markets out of thousands.

- Of this, only 2 of ~500 Morpho Vaults (with >$10k in deposits) have exposure to these markets, with the final impact dependent on how the situation unfolds.

- Every other vault is not exposed thanks to Morpho’s fully isolated market design.

Although the direct impact to Morpho was limited, there may still be second order effects due to broader ecosystem exposure. Stay safe.

6

21

284

26,621

Apr 18

Ok, so now looking like it comes down to how losses are socialized by KelpDAO, which then impacts backing of rsETH on Aave. This is messy.

Apr 18

Assuming this is correct (and it looks likely from what I see so far), Aave shouldn't have a bad debt situation here:

1) rsETH is still fully backed by ETH

2) The borrower's position on Aave is over-collateralized

Assuming no broader contagion, rsETH should be able to be liquidated gradually and position repaid in full, right?

9

2

54

12,858

Apr 18

Assuming this is correct (and it looks likely from what I see so far), Aave shouldn't have a bad debt situation here:

1) rsETH is still fully backed by ETH

2) The borrower's position on Aave is over-collateralized

Assuming no broader contagion, rsETH should be able to be liquidated gradually and position repaid in full, right?

Apr 18

We are continuing to investigate the L0/rsETH incident, initial reports seem to indicate a private key compromise/bad config allowed ~200m worth of rsETH to be stolen, this was then deposited into Aave to borrow ETH (since rsETH has insufficient liquidity). a) the position is technically backed b) if it wasn't, Aave's token and security module exists to be the first line of defense for bad debt. Aave does not have a way to subsidize losses for users, so it would become a bank run, given Aave has 7b in ETH vs 100m withdrawn vs PUT's 17m exposure, this is all largely irrelevant.

All that being said (just to explain our position) our primary goal is always user PUT liquidity, so we did withdraw all the ETH in Aave to the wrapper itself, this was simply because the available Aave liquidity had dipped below our min threshold.

29

9

156

80,774

Apr 18

I was too optimistic, still could be quite bad x.com/MonetSupply/status/204…

Apr 18

couple things about this tho-

19% haircut could cause >100M of bad debt on aave core market on mainnet (due to high looping LTV), of which only 1/2 might be covered by umbrella

also eth market is at 100% utilization so no liquidations can happen if there is a ETHUSD price drop

16

7,884

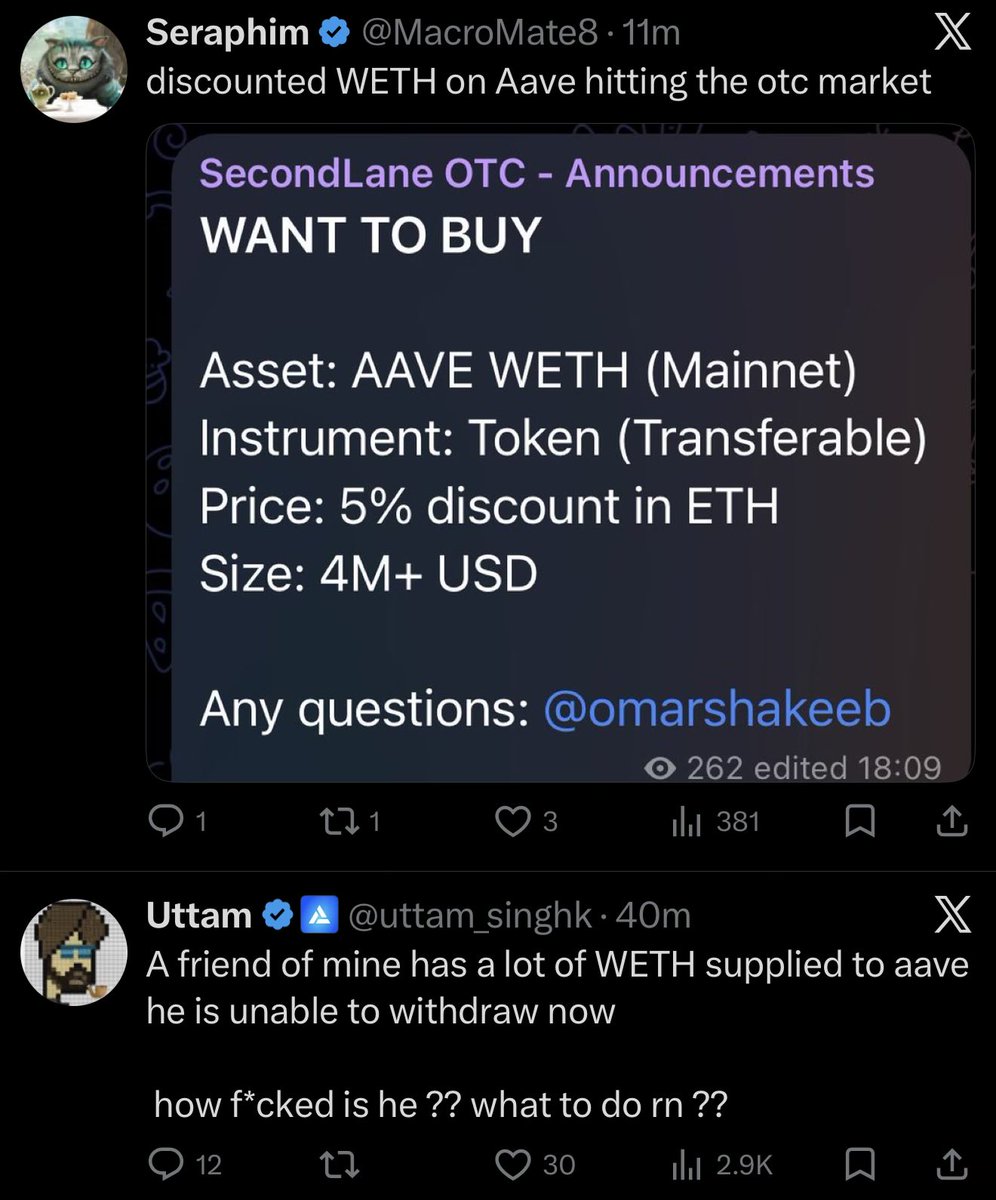

Apr 18

Still good advice until all is clear x.com/Marczeller/status/2045…

Apr 18

If you have WETH on Aave V3 Core, withdraw now, ask questions later.

1

2

4

6,893

Dan Elitzer retweeted

Stop living in fear of losing millions instantly.

There is now a way to overlay checks on top of your business logic to perform runtime enforcement of invariants.

a16zcrypto.com/posts/article…

@phylaxsystems has shipped this. It’s performant, cheap, and also easy to read/write/audit/reason. We are rapidly expanding to more networks.

Get in touch if this kind of thing keeps you up at night.

Mar 12

Earlier today, a user attempted to buy AAVE using $50M USDT through the Aave interface.

Given the unusually large size of the single order, the Aave interface, like most trading interfaces, warned the user about extraordinary slippage and required confirmation via a checkbox. The user confirmed the warning on their mobile device and proceeded with the swap, accepting the high slippage, which ultimately resulted in receiving only 324 AAVE in return.

The transaction could not be moved forward without the user explicitly accepting the risk through the confirmation checkbox.

The CoW Swap routers functioned as intended, and the integration followed standard industry practices. However, while the user was able to proceed with the swap, the final outcome was clearly far from optimal.

Events like this do occur in DeFi, but the scale of this transaction was significantly larger than what is typically seen in the space.

We sympathize with the user and will try to make a contact with the user and we will return $600K in fees collected from the transaction.

The key takeaway is that while DeFi should remain open and permissionless, allowing users to perform transactions freely, there are additional guardrails the industry can build to better protect users. Our team will be investigating ways to improve these safeguards going forward.

8

5

53

12,265