Partnering with founders building Africa's intelligent infrastructure. Research-led, early-stage, long-term.

Joined August 2016

- Tweets 2,064

- Following 331

- Followers 5,333

- Likes 2,058

388 Photos and videos

Jun 11

Africa may not win at foundation models, but that’s not the only game. The bigger question is who owns the compute, data, energy, and deployment infrastructure that local AI systems will depend on.

techcabal.com/2026/06/11/afr…

1

51

Jun 3

China's dependence on African critical minerals is raising African governments' leverage, even as debt service and shrinking Chinese lending limit fiscal room for industrial policy.

semafor.com/article/06/03/20…

6

188

Jun 3

MoneyGram launched MGUSD on Stellar, making a Stripe Bridge-issued stablecoin core payments infrastructure across its global remittance and retail network.

coindesk.com/business/2026/0…

1

3

141

DFS retweeted

Jun 1

Spiro raised another $215m in equity. They've now raised over $500m in disclosed capital across equity & debt; $350m of that since my last post.

Compared to other 2-wheeler EV competitors, they have raised from 10x to 90x more.

They have raised a multiple of their peer group combined and now represent ~80% of the core disclosed capital.

When I say we believe African venture is trending towards neo-infrastructure, this is what that might look like. Fundamental solutions, concentrated & blended capital, underwriting enormous platforms.

Forget unicorn valuations, we're talking billion in funding.

22 Oct 2025

Spiro is not an example of a traditional VC play in Africa. It is closer to the OPay 'brute force' playbook.

They might say their competition is gas bikes, but it's been known for a while that they're crushing the competition. How? They were literally built differently:

Spiro was previously M Auto in India, founded in 2019 then bought by parent company Equitane in 2022. Numbers vary, but Equitane had put in ~$65m in equity to unlock another ~$100m in debt.

There is no world where a company that (at the time) had less than 6k bikes on the road and 130 swap stations would raise 9 figures in debt if not for a parent company with $4 billion in AUM and the resulting deep personal network into infrastructure funds.

To put this into perspective, they raised $165m in debt/equity to put 6k bikes out there or ~$25k per bike. But this allowed them to eat enough of the market to now target 100k bikes for $250m capital, a 10x reduction to $2.5k per bike.

Meanwhile, their competitors were trying to do this on $5m seed raises and have 10x less the number of bikes on the road; a gap that keeps increasing as verticalization and economies of scale start to crush the hard asset cost floor even further in favor of Spiro.

Now, what will be built on top of this new infra is a different matter entirely.

4

12

49

7,007

Jun 1

Spiro raised $215 million at a near-unicorn valuation to expand electric motorcycles, battery swapping, local assembly, and clean energy infrastructure across Africa.

bloomberg.com/news/articles/…

1

2

161

DFS retweeted

May 28

It seems to me that we're seeing a new generation of African startup that can only be described as 'neo-infrastructure."

They aren't laying roads or powerlines, but alongside a renewed shift towards sovereignty by governments and industrialization-as-impact by the global development regime, there's a set of AI-native teams out there building the intelligence on top of this next gen of infra.

We've seen several real signals towards this trend. Neo-remittance startups like @NALAmoney growing into full-stack payments with an intelligent treasury layer.

Neo-prime startups like @terraindustries hardening critical infra security across the continent with AI-first hardware during a time of unstable geopolitics.

Neo-procurement startups like @matta_trade stabilizing critical material supply chains with systems-level coordination driven by data discipline.

Like we saw with real-world stablecoin usage, it's very likely that African markets offer some of the most significant wedge opportunities for these kinds of solutions given how existential and unsolved the problems are.

In a world where global trade is increasingly fragile, I am increasingly bullish on teams that bring stability to Africa's industrialization efforts; those who buffer productivity against volatility.

More on this soon.

4

16

42

2,671

May 28

DFS portco NALA secures up to $50 million in credit financing from Liquidity to pre-fund stablecoin payment corridors and scale Rafiki across emerging markets.

liquidity.com/news/nala-secu…

90

May 28

Zipline plans 12 more Nigerian distribution hubs by 2028, aiming to serve 20,000 health facilities and make autonomous medical logistics national infrastructure.

techcabal.com/2026/05/28/zip…

4

5

403

DFS retweeted

May 25

We welcomed H.E. José Bamóquina Zau, Ambassador Extraordinary and Plenipotentiary of the Republic of Angola to the Federal Republic of Nigeria, alongside Defence Attaché Colonel Venutura Miguel and senior Embassy officials, to Terra Industries' Pax-1 facility in Abuja to examine how indigenous defense technology can anchor Angola's long-term security sovereignty.

16

74

339

25,788

DFS retweeted

Jan 12

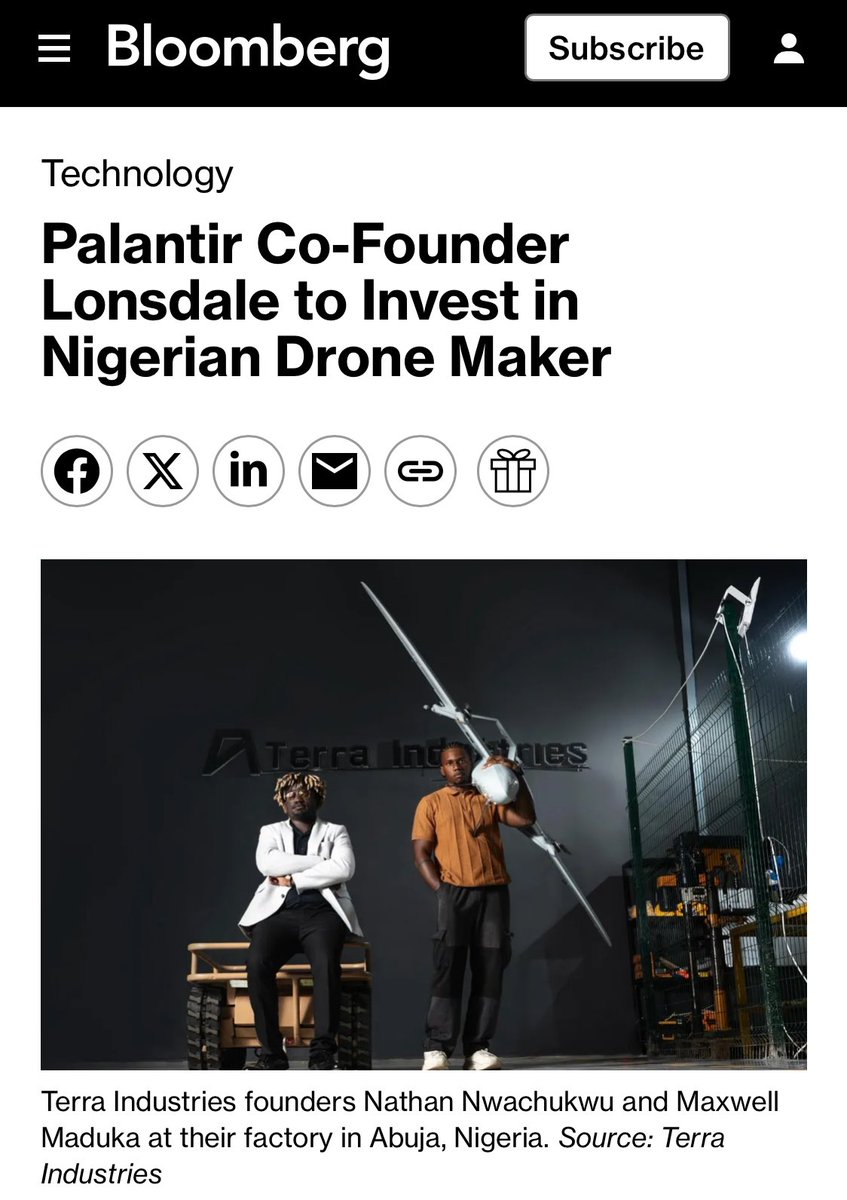

.@terraindustries's seed marks the beginning of a new narrative for African tech.

We're exiting an ecosystem driven solely by the promise of population growth and externally-defined social impact into one where the continent must justify its competitiveness in the AI era.

We believe that @_KingNath @Max_Sengu and team have operationalized a compelling vision to harden Africa's most important infrastructure around energy, critical minerals, and food production.

Excited to have supported this team as one of its earliest investors and to have doubled down this round.

Welcome @8vc @Lux_Capital @novaholdings Valor Equity Partners and others plus a special shoutout to @ulonnaya who's joining the team.

Jan 12

Announcing @terraindustries $11.7M round led by 8VC, the VC by Palantir founder @JTLonsdale

Alex Moore, Board Director at Palantir, also joins Terra’s board

@Max_Sengu & I started Terra to give Africa the technological edge needed for resource protection & counterterrorism

(1/3)

8

38

264

19,674

DFS retweeted

Jan 22

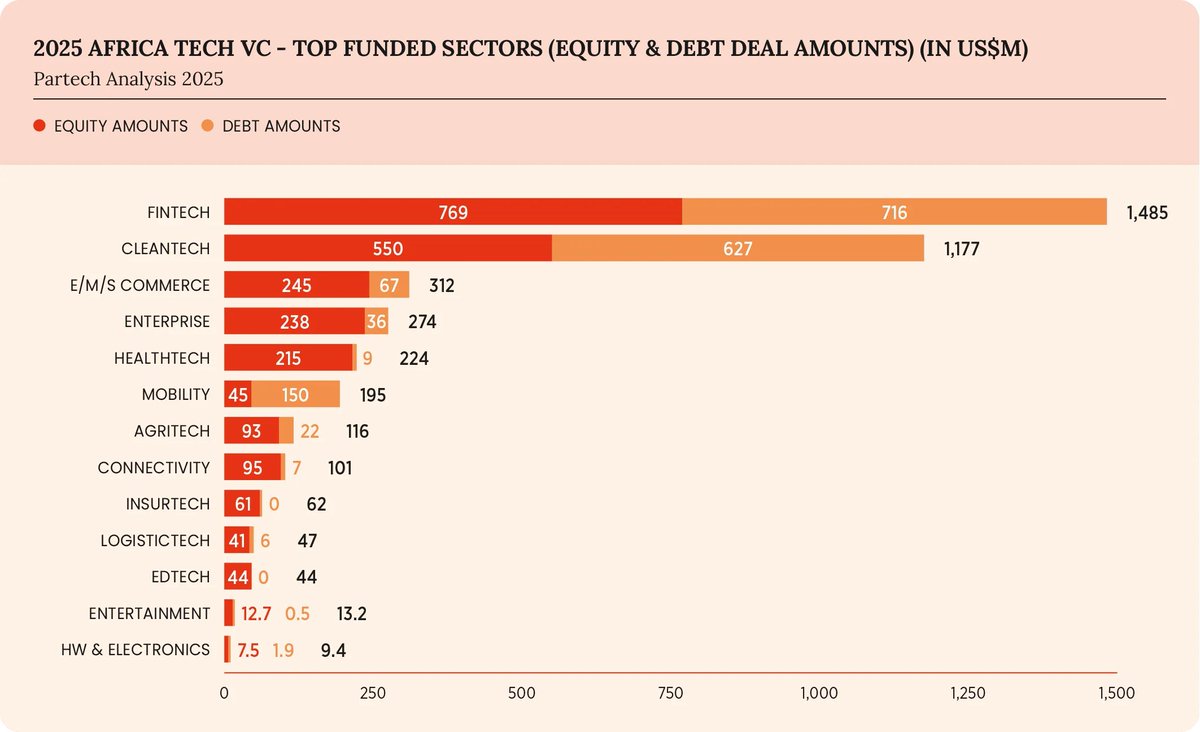

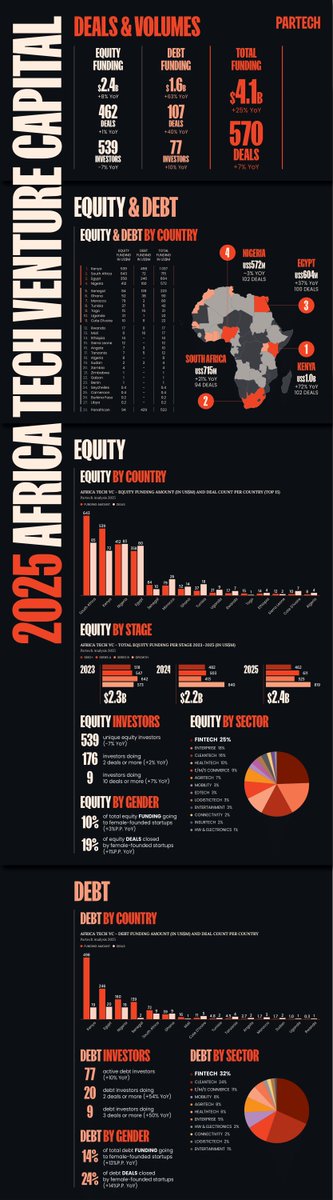

.@PartechPartners Africa's 2025 report is also out - one of the best!

Equity: $2.4b ( 8%)

Debt: $1.6b ( 63%)

Total: $4.1b ( 25%)

> 39% of overall funding is debt; growing at almost 8x the rate of equity.

> Fintech down 12%, Cleantech up 99%

> Renewed concentration into Top4 ( 14% of all funding)

> Seed most constrained (-4%), Series A ( 21%) & Growth ( 29%) are recovering.

> Conversion from early to A has fallen: 2019 vintage (24%; ZIRP), 2020 onward (6.5%), a 73% decline.

My extrapolation is a hollowing out of the early-stage equity pipeline as funds move to bigger fund sizes and tickets. Lower conversion from that pipeline to Series A means we will run into more of a bottleneck this year where it'll be the pressure for funds to deploy vs. the level of de-risking they expect.

The dominance of debt places further signal to de-risk, as our startups will mold their businesses to the shape of available capital.

What I see is an ecosystem that's systematically cutting risk out of its identity. This is a bet against power law distribution and must be discussed hand-in-hand with the exits question.

Jan 22

African tech is charting its own course. 🛣️

In 2025, while global venture capital largely converged on AI, Africa followed a very different path: one shaped by local economic realities and long-term needs.

With the release our 2025 Africa Tech Venture... (1/10)

4

9

39

4,394

20 Feb 2025

See @JakeKendall5 talk about digital trends, cybernetic commerce, and AI in Africa with @julienfanciulli on @France24_fr! Test your french... or read a summary in english of some of his ideas on the Linkedin post.

20 Feb 2025

Yesterday, I joined @julienfanciulli on @France24_fr for #RendezVousAfrique d'#AutourDuMondeF24 to talk #Africantech and AI! See a short summary of my thinking on AI and Cybernetic Commerce in Africa:

linkedin.com/pulse/ai-cybern… via @LinkedIn

6

3,467

5 Feb 2025

The team will be in Nairobi in the coming days leading up to #ATS!

Join us on Tuesday, Feb. 11th by 5pm for a night of networking with founders, investors and ecosystem players!

RSVP here: lu.ma/504vb52p

8

1,762

24 Jan 2025

We’re pleased to have contributed to the CGAP, "Innovative Financing for Inclusive Credit Fintechs in Africa" publication. By interviewing debt investors and fintech stakeholders, we helped uncover valuable insights to provide strategies for reaching inclusive credit in Africa..

1

6

931

24 Jan 2025

... particularly those targeting underserved micro and small enterprises (MSEs).

Curious about what we uncovered? Access the publication below ⬇️

cgap.org/research/publicatio…

3

668

20 Dec 2024

A huge thanks to the entire team DFS Lab, our clients, collaborators, investors and partners for an incredible year!

Catch a glimpse of what we were up to in 2024 ⬇️

medium.com/dfs-lab/dfs-labs-…

1

1

10

2,250

DFS retweeted

23 Nov 2024

Amazing!! Kudus to @fastbuka on of the teams from #StellarSurgeinLagos by @TheDFSLab! #proudmoment and love to see the integration with @Link_IO

2

2

5

1,548

22 Oct 2024

16 Oct 2024

.@TheDFSLab talks "Stellar Surge" - How they building an African dev community

#Stellar #Meridian2024

1

14

1,252

12 Sep 2024

#Thursdaythrowback to #StellarSurge Blockchain Builders Meetup in Nairobi powered by @StellarOrg

It was so much fun meeting builders, founders and blockchain enthusiasts in real time while exploring ways of solving some of the problems faced on the continent through blockchain.

1

4

22

1,073

12 Sep 2024

With over 15 projects pitching for grants and support we had top 5 teams pitching ideas to @BuildOnStellar across Insurance, Finance, E-Commerce, Agriculture etc. These teams will go ahead to exploring further support programs and getting their ideas to user-validated products.

1

3

581

12 Sep 2024

These meetups are a part of our wider #StellarSurge program aimed at building an engaged community of African builders.

@lumenloop

1

4

452