Spine Surgeon to Venture Capital. Trusted resource for MDs on career strategy and healthcare investing.

Joined June 2008

- Tweets 324

- Following 116

- Followers 211

- Likes 607

14 Photos and videos

Healthcare innovation isn't just about technology — it's about vision and courage.

Honored to join @grantzarzour , @DutchRojas and the incredible @BKRBusinessMin Scott Becker on stage yesterday.

Vision. Persistence. Leadership. These are the real foundations of entrepreneurial success.

Disruption in service of physicians and their patients — that's the only kind worth building.

→ @MedMergeco

→ PhyCap Fund

→ Sperity Health

The future isn't coming. It's already here. 🔥

1

3

59

Time is running out... Join us!

May 19

Physicians have been kept at the margins of venture investing. PhyCap was built to change that.

We're hosting our last session before our June 1 final close.

📅 Thursday, May 21 | 2:00 PM ET

🔗 luma.com/fe60nbal?utm_source…

@DutchRojas @drslo

1

56

Take a peek at SF area home prices over past 6 months....just a small preview of the tsunami of wealth soon to be unleashed by theses IPOs. It won't all be parked in real eatate...

May 13

Five percent of US market capitalization is about to enter public markets through three IPOs.

Paul Tudor Jones laid out the structural read on Invest Like the Best. The contemplated IPOs over the next year represent 5-6% of US market cap. Normal IPO issuance runs 0.5 to 1% in active years. The 2026 pipeline runs ten times that ratio.

The mechanism is direct. Buyback capacity has supported equity prices for a decade. The mega-IPO pipeline reverses it. The funding for SpaceX, OpenAI, and Anthropic is already being pulled out of existing technology stocks. Magnificent Seven weakness year to date is the rotation, not a coincidence of earnings cycles.

Standard 180-day lockups place the insider supply wave in Q1 through Q3 of 2027. The 2000 parallel is exact. Supply hit demand at the same moment fundamental concerns began to bite.

For physician allocators, healthcare sits structurally outside this pipeline. That creates the asymmetry worth positioning for.

44

Physician is the word....

May 12

No wonder he doesn’t understand healthcare!

Abdul El-Sayed told a podcast in 2022 that during his only clinical rotation, his job was “to be the, like, worst doctor on the team” and that he was “cosplaying a doctor.”

That four-week sub-internship at the end of medical school is the entirety of his time at a patient bedside.

He is now running for U.S. Senate in Michigan calling himself a physician.

El-Sayed earned an MD from Columbia in 2014, after two years at the University of Michigan Medical School and a Rhodes Scholarship at Oxford where he completed a DPhil in public health. The academic ladder is real.

Two doctorates. “Dr.” is accurate.

He never entered residency.

He has never held a medical license in Michigan, New York, or any other state.

He has never independently treated a patient.

In March 2026, El-Sayed told a group of Teamsters nurses he had “been in enough codes to watch who really does the work.” On a podcast that same month: “I’ve been a doctor my whole career.”

His campaign objects to the Politico report that surfaced these statements.

The spokesperson’s response was that “he has earned the right to be called ‘doctor’ twice over.”

That is true, and it is beside the point. The contested word is physician.

In American medicine, the MD is the beginning. Residency is the apprenticeship, three to seven years long.

State licensure follows residency. Independent practice follows licensure.

The structure exists because patients pay the price when it is skipped.

Every physician in this country surrendered most of their twenties to those steps.

Eighty-hour weeks.

Overnight call. Boards. Maintenance of certification. Malpractice exposure that follows them for the rest of their careers.

Physician is not a credential of the classroom.

It is a credential of the bedside, the licensing board, and the legal accountability of both.

To borrow it without paying for it is to take something from every doctor who did.

El-Sayed knows the difference.

He named it himself.

Excellent reporting @adamwren

politico.com/news/2026/05/12…

2

6

3,934

Already the preemptive shock waves rippling through the SF area...rent and property values are the early indicators...

May 12

5-6% of US market capitalization is about to enter public markets through three IPOs.

Normal run rate is 0.5 to 1%.

The 2026 pipeline is ten times that.

SpaceX.

OpenAI.

Anthropic.

$240 billion combined.

Healthcare sits outside the supply wave.

67

This will be a fantastic event!

Apr 26

We have our Business Leadership Virtual Summit June 22nd. Please join us no charge.

6 Sessions on The Deal Market-PE, VC, Healthcare, Business Services, Real Esate and more. Also sessions on issues facing CFOs, AI use cases, talent and staffing and more. Maybe an added session on the silver tsunami and esops for transactions.

Great speakers include Jeremy Jacobowitz Tom Mallon Paula M. Avenaim Erris Langer Klapper, M.S., ESQ. Dylan Werner Will Conaway Jeff Freedman Chris Lacy Kat Marie Alvarez, RN,MBA BRENT BERGER Kenny Motew Michael Motew Nader Samii Bart Walker Andrea Marin Paul Slosar, MD, MHCDS and Brian Taylor.

For more information reach Lauren Eskenazi or myself. Thank you. Thank you. Thank you.

1

27

We have a lot to talk about!! Join us Wednesday to learn how we harness MDs and healthcare pros insights to make smart investments. #vc

Apr 28

Tomorrow: Patterns from 500 Healthtech Deals

Join @drslo and Tracy Poole as they walk through the signals that build conviction quickly and why some of the strongest looking companies fall apart during diligence.

📅 April 29 | 7:00 PM ET

🔗 luma.com/bamfhwie?utm_source…

@DutchRojas

44

Clinical decision support tools(AI-driven) are growing and will be an important solution helping doctors and frontline health care professionals address the caregiver shortage. VC investments in these is complex.... and requires extraordinary clinical insight. @PhysiciansCap

Apr 21

AI clinical decision support: 70% observed venture failure rate. The segment with the heaviest generalist-VC concentration is the segment with the worst return distribution. Workflow blindness has a price, and the return books show it.

@PhysiciansCap

@drslo

1

55

Unbelievable...

WOW 🚨 Delta Dental is considered a nonprofit but the CEO skyrocketed her pay from $4.5 million per year all the way to $48 million over 4 years

That’s $1 million dollars per month pay for one employee as a nonprofit

“Delta Dental is considered a non-profit, and as such you can be their taxes online. So I got curious in their 2014 filing, the IRS requests for the organization's top accomplishments.

Delta Dental reported that over 95% of claims electronic, online and paper were processed without any manual intervention. That means when your care is denied, there is less than 1 in 10 chance a human reviewed it

— That same year, Delta dished out up to a 30% pay cut on the care that doctors deliver, and for a decade, they did not raise what they pay for your dental care by a single penny.

Meanwhile, their CEO's salary skyrocketed. She went from 4.5 to $15 million a year. From 2014 to 2018, she made off with almost $48 million before leaving her position. That's a million dollars a month. Must be nice. And she's not even a clinician. She's a CPA.

You don't have to be an accountant to do the math. Dr. Pay cuts stagnant reimbursements. They were never about saving patients money on premiums.”

37

Healthcare delivery is a blackbox to most...not us. Seeing around corners in HC investing is a dynamic and nuanced process. Join us tomorrow!

Tomorrow: A Real Healthtech Deal Debate

Join @drslo, @DrVipulKella, and Tracy Poole as they debate a real (anonymized) healthtech deal live.

📅 April 7 | 7:00 PM ET

🔗 luma.com/9sva1xlu?utm_source…

@DutchRojas

1

29

This is accurate...the ACA turbo-charged $$$ to insurance companies (from you the taxpayer) ...the results were predictable and those of us who "predicted this future" were ignored (or worse) as fear-mongering....

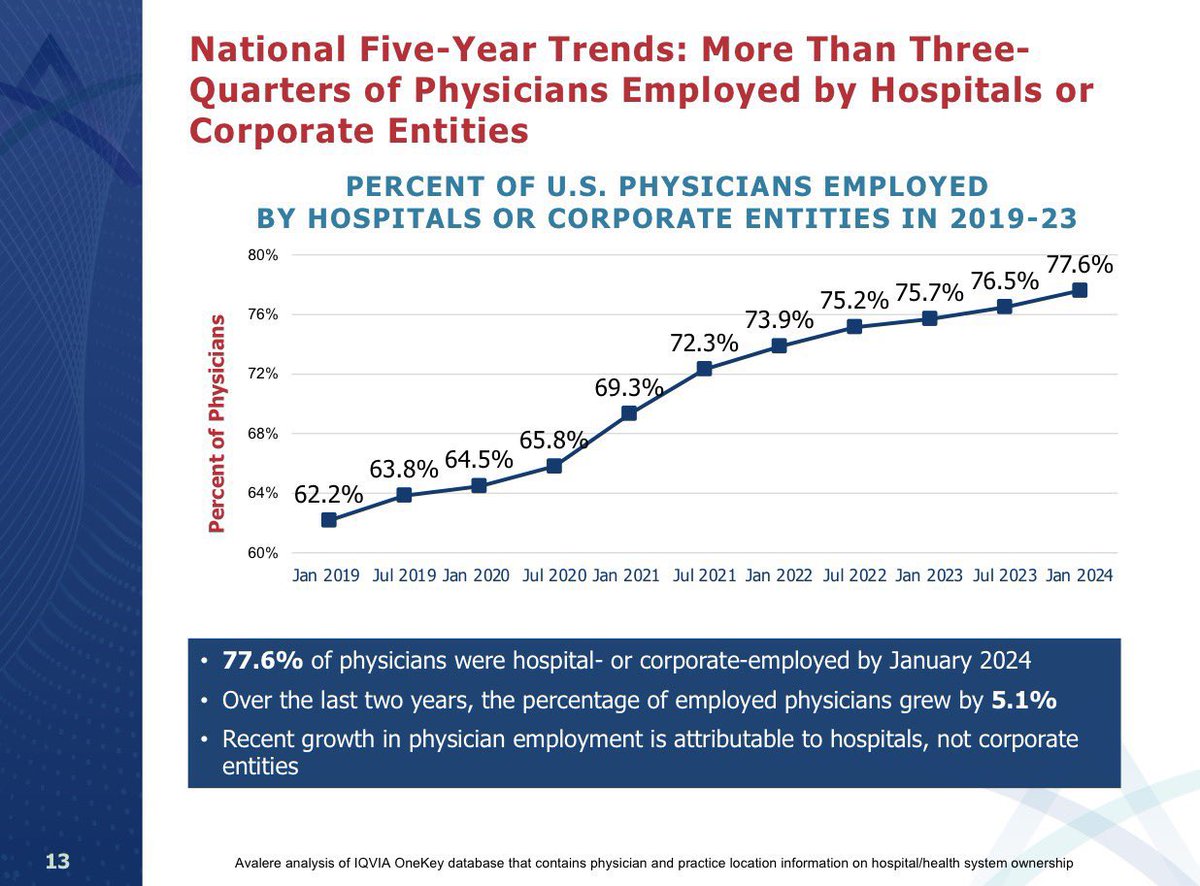

The consolidation engine we aren’t talking about enough - site neutrality

The healthcare consolidation crisis did not begin with hospitals. It began with insurers.

When the Affordable Care Act reshaped the market after 2010, it accelerated insurer consolidation through exchanges, risk corridors, and quality reporting infrastructure that rewarded scale. Larger insurers gained negotiating leverage, tightened network contracting, and squeezed reimbursement margins across the board. Hospitals, facing that margin pressure and the new requirements for electronic health records, population health management, and value-based contracting, responded with the only logical move available to them: get bigger. Acquire other hospitals. Acquire physician practices. Build the scale necessary to sit across the table from a consolidated insurer.

Physicians were the last domino to fall, and they fell fast.

In January 2019, 62.2% of U.S. physicians were employed by hospitals or corporate entities. By January 2024, that number had reached 77.6% — a 15-point shift in five years. Over just the last two years of that period, the employed share grew by 5.1 percentage points, and critically, that recent acceleration is attributable to hospitals, not to corporate entities. Hospitals are still actively absorbing the remaining independent physician workforce. (Avalere analysis of IQVIA OneKey data)

That is not a trend. That is a structural transformation of the American medical profession, driven by a cascading consolidation logic that started with insurers, moved to hospital systems, and is now completing its circuit through the physician workforce.

The mechanism is straightforward. Congress built a payment architecture that rewards hospital acquisition of physician practices. Medicare pays a hospital outpatient department roughly 1.5 to 2.5 times what it pays an ambulatory surgery center and even more than an independent physician office for the exact same procedure, on the exact same patient, with the exact same clinical outcome. A Level 2 office visit in a freestanding physician office generates a professional fee. That same visit, conducted the day after a hospital acquires the practice and designates it a provider-based billing site, now generates both a professional fee and a facility fee — often $500 to $1,500 — with zero change in the care delivered.

That differential is not a clinical premium. It is a billing premium. And when hospitals were already under margin pressure from consolidated insurers, the ability to acquire a physician group and immediately convert its billing to HOPD rates became one of the most reliable capital allocation decisions in American healthcare. The acquisition frequently pays for itself within a year for surgical practices through facility fee conversion alone, not including capturing referrals and procedure volume.

MedPAC has documented this for over a decade. The GAO has confirmed it. What has been in dispute is whether Congress has the will to fix it, because the hospital lobby’s argument is always the same: hospitals cross-subsidize emergency care, graduate medical education, and indigent care, and equalizing the differential will destabilize that model. That argument deserves engagement. But it cannot permanently shield a payment structure that has, in five years, moved 15 points of the physician workforce out of independent practice.

The Cassidy-Hassan site-neutral framework is the most serious bipartisan attempt to correct this differential. This week I will walk through why it is necessary, why it is not sufficient on its own, and what a complete reform package actually requires.

Done wrong, site-neutral reform trades one consolidation crisis for another and the next wave of consolidators is already positioning.

1

48

drslo retweeted

Mar 5

"Payment Reform, Physician Independence, and Rebuilding Healthcare’s Architecture with Dutch Rojas of Bliksem Health 3-5-26"

Listen Here: beckerprivateequityandbusine…

2

1

10

4,582

Making GREAT strides as we aim to complete our Investor pool soon. If anyone wants to join us DM me or @DutchRojas. Www.phycapfund.com.

2

4

621

The data @KyleTMack shows here is stunning...draw conclusions as you see fit but the patterns are highly unlikely absent organizational fraud

Feb 19

HHS just open-sourced the largest Medicaid dataset in history. About $1T in claims data, free for anyone to analyze via @DOGE_HHS. Everyone's looking at what was billed. At @MiddeskHQ, we're looking at who's behind the billing.

Here's what we found 🧵

1

117

I don't know which is worse...the scale of fraud or the sheer ineptitude of simple regulatory oversight????

Feb 13

@DOGE_HHS published a dataset with billing activity for every Medicaid provider; 227 million rows, from 2018 to 2024. I cross-referenced it against the federal NPPES provider registry and @OIGatHHS's exclusion list, and started looking for fraud. It didn't take long to find providers banned for fraud still collecting payments a decade later. Brand-new entities billing $170 million in their first 18 months. A lab that went from 73 claims to 48,000 in a single month. Here are five cases:

1. We Care Transportation, a Kansas transport company, was excluded from federal healthcare programs in January 2010. Their NPI was never deactivated. They kept billing Medicaid for another ten years, collecting $4.4 million through July 2020. As of today, their NPI is still active and their exclusion has not been lifted. They're one of 13 excluded providers in the dataset who continued billing after being banned -- $7.3 million in payments that were improper by definition.

2. Fishing Point Health Care LLC registered in Virginia as a "General Practice" in February 2023. Eighteen months later it had billed Medicaid $170 million, almost all of it on a single attendant care code (S5121). Claims went from 1,213 per month to over 10,000. Toward the end of 2024, it started tacking on ancillary codes -- labs, therapy, E&M visits -- which looks a lot like an attempt to make the billing profile seem more legitimate. There are 20 other entities formed since 2022 that have each billed Medicaid more than $50 million, totaling $1.7 billion.

3. Lifeline Biosciences LLC, an Illinois lab formed in early 2022, has exactly four rows in the entire dataset. In August 2023 it billed 73 claims for infectious agent detection. In December, it billed 48,355 -- a 662x increase in one month, good for $7.3 million. The national trend for that same code was flat. Forty-three providers had similar one-month explosions (10x or more, over $1 million) in the post-COVID period, across 48 separate events.

4. New Life Wellness Center LLC in Phoenix was excluded in November 2024 after a fraud conviction. The billing history tells you everything: 25 patients and $280,000 a month in mid-2021, ramping to 273 patients and $8.7 million a month by March 2023 across 14 behavioral health codes. Community mental health claims alone went from 125 to 5,603 in five months, then billing stopped abruptly. More than 4,200 behavioral health providers in the dataset have a similar growth curve -- peak monthly claims at least five times their trough, with total billing above $5 million -- a $98 billion pool that could use a closer look.

5. C&C Mental and Family Services, a Florida entity formed in April 2023, billed $3.6 million on a single code: H2019, therapeutic behavioral services. The monthly volumes make no sense -- 1,180 claims in October 2023, 804 in February 2024, then 34,760 in July. That's a 43x swing against a flat national trend, which is not what a real clinic's patient load looks like. Over 1,200 providers on behavioral health, attendant care, or waiver codes have the same kind of volatile billing while topping $1 million in total payments, accounting for $14.9 billion collectively.

2

71

"The next two to five years are going to be disorienting in ways most people aren't prepared for..."

76

Great to see others from outside healthcare digging in!

Feb 8

Welcome @WallStreetApes to the discussion. Where have you been for the past 10 years? Insurance companies are vertical (monopolies) with the intent to grow profits and limit spending, or patient service. This is counter-productive to improving patient quality of care.

3

61

Yes we did...stay tuned for more on MedMerge!

Feb 6

70.8% of physicians who sold their practices said the top reason was: “need to negotiate higher payment rates with payers.”

They did not sell because they were bad at medicine.

They sold because they were buying alone.

That part is fixable.

A group of physicians, operators and I built the fix.

59

This is worth a listen....

Jan 16

What looks like medical consensus can actually be manufactured. That’s what’s happened in gender medicine, argues @LeorSapir.

Medical groups like the AAP & Endocrine Society often cite each other’s guidelines as “evidence,” creating a loop of circular citations that gives the appearance of scientific rigor. Internal communications show WPATH strategizing about getting major associations to endorse its guidelines to give them credibility, Sapir was.

Not a single group agreed to endorse them, Sapir says. But none criticized them either. Many organizations actively suppressed dissent from within their own ranks.

Why do such groups keep doubling down, even now? Perhaps it’s too hard to admit they were wrong after endorsing powerful, irreversible drugs and surgeries for kids, Sapir says.

He points to short-term incentives: The heads of these organizations often have a tenure of only one or two years, making it easier to just kick the can down the road.

He also describes “capture by committee”—a small, motivated bloc of activists inside large organizations overpowering a diffuse majority that’s less mobilized (or afraid to stick their neck out). The result? The organized minority wins.

Finally, medicine itself relies on a “chain of trust”: physicians in one specialty defer to the expertise of colleagues in another. When a particular field becomes captured, that chain can break — with far-reaching consequences.

16