Joined December 2007

- Tweets 8,154

- Following 213

- Followers 236

- Likes 779

1,620 Photos and videos

Eduardo Llanquileo retweeted

10 Oct 2025

2

52

502

10,811

Eduardo Llanquileo retweeted

6 Oct 2025

341

1,766

11,519

1,551,458

4 Oct 2025

Están jugando una pichanga, faltas innecesarias , empujones, tirones de camisera. #VamosChile

2

254

4 Jun 2025

NVIDIA CEO Jensen Huang shares some insights into the creation of Nintendo Switch 2’s custom processor.

Iwata dreams

youtu.be/ic2ez3ZoKAk?si=g8jp…

79

Eduardo Llanquileo retweeted

21 May 2025

.@SpeakerJohnson warning, you guys are smoking in the dynamite shed.

94

184

1,061

228,415

Eduardo Llanquileo retweeted

20 May 2025

endgame

174

710

5,428

1,397,781

Eduardo Llanquileo retweeted

28 Apr 2025

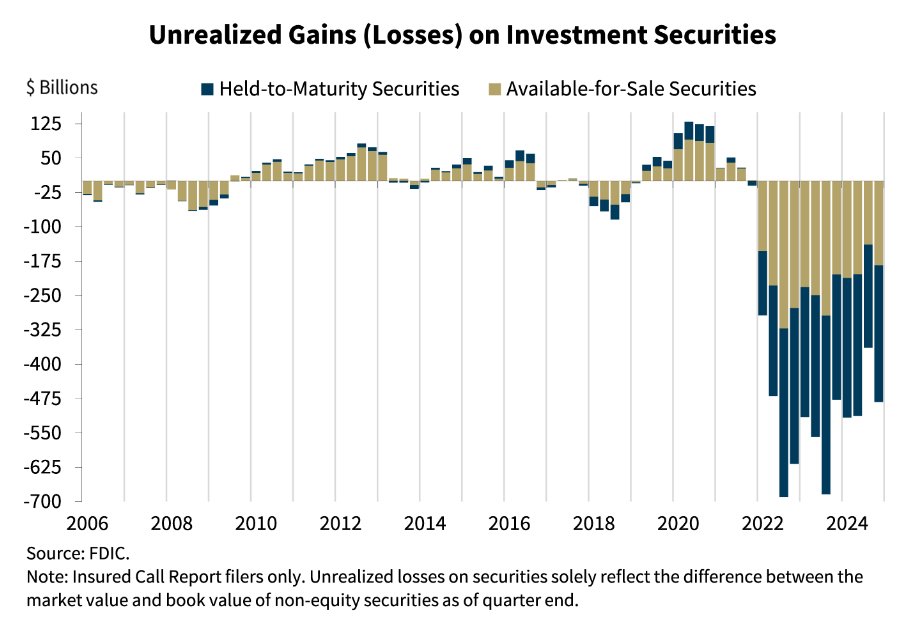

The Silent Banking Crisis: Understanding the $482 Billion Time Bomb

U.S. banks are currently sitting on $482 billion in unrealized losses on their investment securities primarily long-dated Treasuries and mortgage-backed securities bought during the 0% interest rate era. This figure has jumped 33% in just the last quarter, making it the worst paper loss environment banks have faced in modern history even worse than during the 2008 financial crisis.

On the surface, these losses are “unrealized,” meaning banks don’t have to formally recognize them on their balance sheets unless they are forced to sell.

The problem is: what can stay “unrealized” for years can suddenly flip into catastrophic reality under certain conditions.

Here’s how these “paper losses” can become realized losses that ignite systemic problems:

⸻

How Unrealized Losses Can Become Realized

1. Deposit Flight (Funding Pressure)

•If depositors move money out of banks (into money markets, Treasury funds, crypto, or physical cash), banks lose their cheapest source of funding.

•To meet withdrawals, banks may be forced to sell assets even those classified as “Held-to-Maturity” at market prices far below book value, locking in massive losses.

2. Liquidity Crises

•If interbank lending freezes, or repo markets demand higher collateral haircuts, banks could be forced to pledge or liquidate assets under stress.

•Fire sales of long-dated bonds would crystallize the hidden losses instantly, slashing bank equity and trust.

3. Regulatory Pressure

•Regulators could tighten capital adequacy rules (especially if the political optics of another “hidden bailout” grow toxic), forcing banks to raise cash by selling impaired securities.

4. Mergers, Acquisitions, or Liquidations

•If a weak bank is acquired or collapses, its securities must be marked to market during the transaction or liquidation process realizing losses on the spot.

5. Rising Loan Defaults

•If commercial real estate or consumer loan defaults spike, banks need liquidity to cover losses and reserves again forcing them to sell investment securities at fire-sale prices.

⸻

Why This Matters: The Hidden Systemic Risk

As long as banks don’t have to sell, they can “pretend and extend” carrying toxic assets at full value on paper.

But if economic or financial stress forces even a small subset of banks into liquidity-driven sales, it could trigger:

•Equity wipeouts (especially for regional banks).

•Credit tightening (making loans harder to get, slowing the economy).

•Policy reversals (forcing the Federal Reserve back into money printing to stabilize the system).

•Accelerated consolidation (small banks collapse into megabanks shrinking financial competition).

•Loss of trust (depositors shift into money markets, physical cash, gold, Bitcoin, or foreign assets).

The entire post-2020 economic structure rests on the assumption that these unrealized losses stay hidden indefinitely.

History shows that assumption is fragile.

⸻

What Makes This Different From 2008

•In 2008, the problem was credit risk (toxic subprime loans).

•In 2025, the problem is interest rate risk (good-quality bonds bought at the wrong price). Both can destroy banks just through different mechanisms.

This is why liquidity, optionality, and real assets are becoming more critical than ever as systemic risk slowly builds.

⸻

Bottom Line for Followers:

Unrealized losses are invisible until they suddenly aren’t. Liquidity crises, deposit runs, regulatory shocks, or economic deterioration can turn hidden losses into realized catastrophes almost overnight.

Watch the following signals closely:

•Deposit flight speed.

•Small bank equity declines.

•Treasury market dysfunction.

•Expansion of emergency Fed lending programs.

If any of these accelerate, the “pretend” phase ends and the real damage begins.

BREAKING 🚨: U.S. Banks

U.S. Banks are currently facing $482 Billion in unrealized losses, an increase of 33% from the prior quarter

23

73

310

52,322

27 Apr 2025

"Los ciclos del mercado no se revierten por el optimismo de los minoristas, sino porque los regímenes de liquidez sistémica cambian."

27 Apr 2025

Retail Buying the Dip: Strength or Warning Signal?

This past week, retail investors bought $11 billion in cash equities, according to JP Morgan. At first glance, that seems like a bullish sign retail stepping in aggressively during a dip. But if you dig deeper, the picture gets more complicated.

Historically, large retail inflows after a market pullback tend to happen at two distinct points:

•(1) Near local bottoms during healthy bull markets (March 2020, late 2012), when liquidity is abundant and credit markets are strong.

•(2) Just before deeper drawdowns during late-cycle phases (early 2008, late 2021), when market internals are deteriorating but surface indicators (like equities) haven’t caught up yet.

Cross-market signals today suggest we are closer to the second scenario:

•Treasury yields are volatile and unstable, not confirming a clean risk-on move.

•Credit spreads (junk bonds) are widening slightly a subtle stress signal.

•The U.S. dollar remains strong tightening global liquidity indirectly.

•Breadth deterioration across equity indexes is picking up underneath the surface.

•Options flow shows increased call buying often a short-term fuel, but can lead to heavy dealer hedging and fast reversals.

Why does this matter?

Retail buying alone doesn’t drive sustainable rallies. Liquidity conditions and collateral availability do. And while real liquidity hasn’t collapsed yet, the foundation is fragile. Treasury issuance, higher dollar funding costs, and persistent geopolitical risks mean that the window for easy upside is narrowing.

⸻

Key Takeaways:

•Retail strength looks impressive now, but historically signals late-stage risk when liquidity and credit stress are quietly building.

•Short-term stabilization is possible if liquidity remains loose, but the medium-term asymmetry is skewed heavily toward downside risks.

•Missing a small rally is survivable. Absorbing a 30–50% drawdown is not. Capital allocation should respect the growing asymmetry.

•Market cycles don’t reverse because of retail optimism they reverse because systemic liquidity regimes shift.

In short:

Retail buying the dip is a signal but depending on liquidity and market internals, it might be a warning, not a green light.

Stay sharp. Position accordingly.

10

17 Apr 2025

Existirá algún servicio más nefasto que @correoschile ?

Pedido no llega, reclamas, preguntas como va el reclamo y te piden hacer un nuevo reclamo porque el anterior no se cursó. Loop infinito

1

371

Eduardo Llanquileo retweeted

12 Apr 2025

“This is the dream scenario for tech investors,” Dan Ives, global head of technology research at Wedbush Securities, told CNBC. “Smartphones, chips being excluded is a game changer scenario when it comes to China tariffs.” @CNBC 🏆🐂🔥👇

cnbc.com/2025/04/12/trump-ex…

199

183

1,578

236,074

Eduardo Llanquileo retweeted

9 Apr 2025

This is the most bearish my timeline has been since Covid, with no close second 🐻 📉:

People who have never owned a bond are quoting overnight bond futures and swap spreads.

People who have never traded a currency are tracking the pre-market yen and yuan.

People who don’t realize you can’t trade Spot VIX are quoting Spot VIX.

People who don’t understand a real bear market are getting really bearish.

And I think they’re going to be right for a bit longer.

Just long enough for the whipsaw to catch you offsides. You lighten your exposure, but then there’s a monster multi-day rally. Sweet relief, it’s over. You pile back in. Yes, you missed the bottom but you know you’ll get most of the recovery.

So you chase the bounce, only to discover there are lower lows to be plumbed: offsides again.

A Great Bear market doesn’t fall 20% then recover:

It jukes and dodges.

It falls and rallies.

It crashes and rips.

It is head fakes and narratives and bear porn - being negative feels and sounds so fking smart.

In sum, it takes the path of maximum pain, extracting more from you with each jagged move.

It milks you.

Maximum pain means the Great Bear draws you in and kicks you out at all the wrong times. It is raw emotion and you do worse than if you’d done nothing.

You want to give up, so you finally exit and actually do nothing, only to watch it rip again.

But you wise up - this time you don’t chase it, because you have learned your lesson and you know better…

…except you don’t.

It really was over.

If this is a Great Bear, that’s when the bottom is in: when you quit and you’re set back ten years.

Don’t think you can avoid it.

It is your destiny.

48

44

617

143,603

Eduardo Llanquileo retweeted

5 Apr 2025

Tom Lee @fundstrat Calls #Tariff “Liberation Day” a Macro Negative and Explains Why Probabilities Favor Trump Negotiating New Trade Deals With Key Partners

WATCH NOW! 🎥👇

youtu.be/tjHB4M6dJEY?si=ORkO…

DISCLOSURES: GRANNYSHOTS.COM

HOLDINGS: GRANNYSHOTS.COM/HOLDINGS/

STANDARDIZED PERFORMANCE AT NAV AND MKT: GRANNYSHOTS.COM/PERFORMANCE/

BEFORE INVESTING, CONSIDER THE FUND’S INVESTMENT OBJECTIVES, RISKS, CHARGES, AND EXPENSES. FOR THIS AND OTHER IMPORTANT INFORMATION, PLEASE READ THE PROSPECTUS CAREFULLY BEFORE INVESTING. BIT.LY/GRNYPRO

THE PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND IS NO GUARANTEE OF FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE OF AN INVESTMENT WILL FLUCTUATE SO THAT AN INVESTOR’S SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAN THE PERFORMANCE DATA QUOTED. FOR THE MOST RECENT MONTH-END PERFORMANCE, PLEASE CALL (212) 293-7132.

The Fundstrat ETFs are distributed by Foreside Fund Services, LLC.

2

3

15

4,367

Eduardo Llanquileo retweeted

27 Mar 2025

Pro-Trump: Tariffs are a negotiating tool and he’s playing 4-D chess!

Anti-Trump: Tariffs are idiotic and will crush the economy!

Me: I haven’t yet found a way to quantify the effect of tariffs on stock prices so am ignoring the noise and sticking to my investment plan.

7

8

65

10,504

Eduardo Llanquileo retweeted

24 Mar 2025

4

33

1,711

12 Mar 2025

The defining photos of the pandemic — and the stories behind them cnn.com/interactive/2021/03/…

4

Eduardo Llanquileo retweeted

12 Mar 2025

1

3

21

1,131

Eduardo Llanquileo retweeted

1 Mar 2025

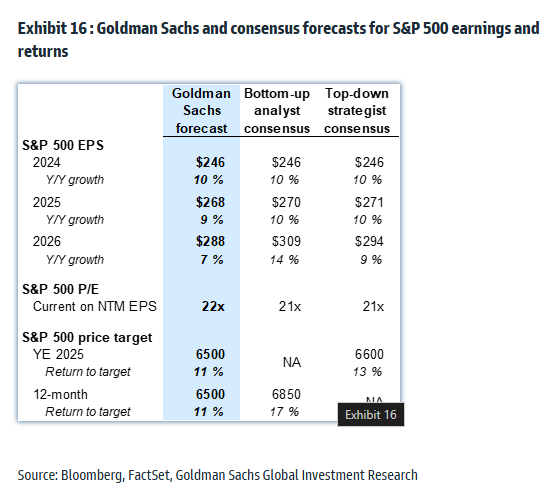

GS: we maintain our year-end S&P 500 price target of 6500

8

44

196

19,039