I flip stocks and shit.

Joined January 2017

- Tweets 1,282

- Following 553

- Followers 151

- Likes 3,144

47 Photos and videos

samsonite retweeted

$AMPG has the potential to be the defining stock of the year. I don't know of any other microcap with such superior technology, scaling ability, and execution.

1

3

23

665

samsonite retweeted

My single largest position is $AMPG.

70% of my portfolio.

And it's staying that way for now.

Here's the receipt:

I haven't sold a single share since $6.8.

That was the moment I openly said, in a post, that I'd be trimming.

And from $6.8 until right now, I haven't sold one share of my biggest holding.

Not one.

It now sits at roughly 70% of my entire portfolio.

Let me be clear about what that means, because conviction is easy to type and hard to back.

70% of my portfolio in one sub-$1B name isn't a trade.

It's a bet on a thesis I've done the work on: the only American 64T64R AI-RAN radio, deployed at a Tier-1 carrier, defense-qualified, inside the DoD-funded Open6G hub, with quantum and space stacked on top.

Every week the thesis gets stronger, not weaker.

New hires poached straight from Nokia and Ericsson.

On the Reg SHO list.

Margins inflecting.

Management saying new carrier POs are coming.

I'm not telling you to do what I do.

70% in one name is high concentration and it carries real risk. That's my conviction and my risk tolerance, not a recommendation.

Position sizing is personal, and you should size to your own.

But you asked where I stand.

This is where I stand.

Biggest position.

Haven't sold since $6.8.

That's when I trimmed 30%.

Still holding the rest.

Not financial advice. DYOR.

啊,你不是全仓AMPG吗?还有钱买trt?

4

2

47

4,423

samsonite retweeted

Tomorrow $ASTS will write history.

BlueBird 8, 9, and 10 are officially go for launch.

Now send it to $160.

-BP

Not financial advice.

15

12

299

13,005

samsonite retweeted

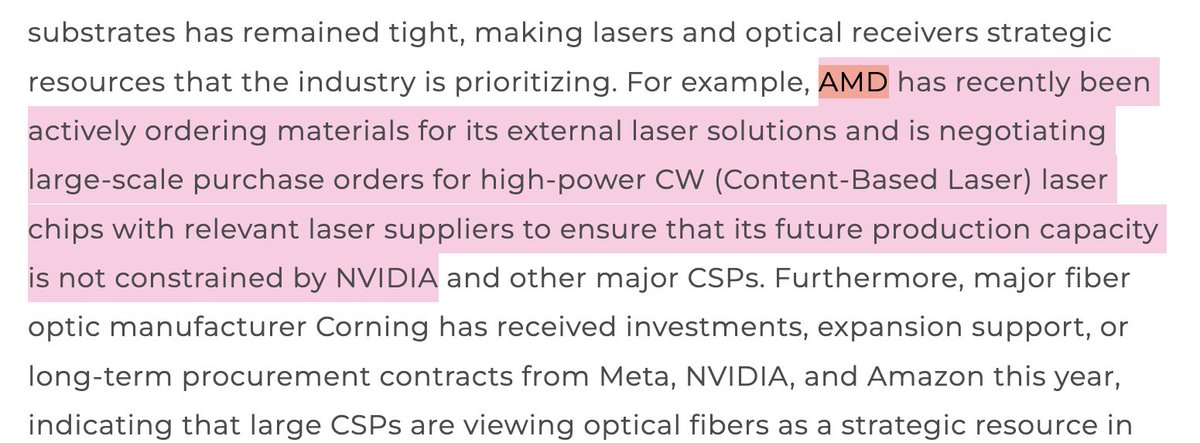

$SIVE $AMD - The industry is hit by a massive squeeze on CW Lasers.

Recent supply chain tracking from TrendForce shows that $AMD is quietly scrambling to lock in massive purchase orders for these lasers.

Their goal is obvious is to secure their own independent supply line before $NVDA locks down the entire market and chokes out $AMD next-o-Packaged Optics (CPO) roadmap.

The big problem?

Giants like $LITE and $COHR are basically booked solid through 2028.

This supply crunch turns $SIVE into a massive tactical play.

Connecting the dots between $AMD and $SIVE isn't just wishful thinking; looking at the infrastructure, it’s practically inevitable.

$SIVE recently locked in a deep collaboration with $GFS, embedding their laser arrays directly into GF’s SCALE CPO framework.

$AMD has a long, deeply rooted history of relying on $GFS for its silicon photonics manufacturing.

If $AMD builds its optical chips through GF, they are essentially forced to use $SIVE as their reference light source. The partnership is already written into the silicon.

$SIVE is also the exclusive hardware engine behind Ayar Labs' SuperNova light sources. $AMD is a founding heavy-hitter in the Optical Compute Interconnect (OCI) consortium, an ecosystem heavily reliant on Ayar’s architecture.

This means $AMD long-term hardware pipeline is already designed to plug right into $SIVE's physical lasers.

Look at $AMD recent acquisition of CPO pioneer Enosemi.

Enosemi’s designs require incredibly precise, external laser sources to actually move data. Since $SIVE has clear, unconstrained manufacturing capacity through its relationship with WIN Semiconductors, it stands out as one of the only global players capable of handling $AMD massive production scaling.

On the corporate side, $SIVE is actively restructuring its books to PCAOB standards to prepare for a major dual-listing on the Nasdaq in New York. You don't launch a major US IPO without a massive PR catalyst. Sealing an official supply agreement with a trillion-dollar hyper-scaler like $AMD would be the ultimate validator for their US market debut.

New reports that $AMD is scrambling for CW laser supply.

And is negotiating large-scale purchase orders for CW Lasers to ensure its production capacity is not constrained by $NVDA (Trendforce)

Obvious CW laser beneficiaries:

- $SIVE (AMD went to GFS for CPO, Sivers reference laser level)

- $AAOI (Rosenblatt analyst checks)

Lumentum/Coherent are kinda booked out way into 2028 as well.

Lumentum is especially constrained for CW capacity already from existing EML contracts (so they probably are buying from Sumitomo/Furukawa and co).

Maybe Macom and Japanese giants still have spare capacity. (disclosure, own aaoi/sivers).

I predicted this last year and said hyperscalers should go more upstream to secure capacity... at laser levels, epiwafer levels, or even inp substrate levels.

To not get bottlenecked by Nvidia.

6

13

160

15,740

samsonite retweeted

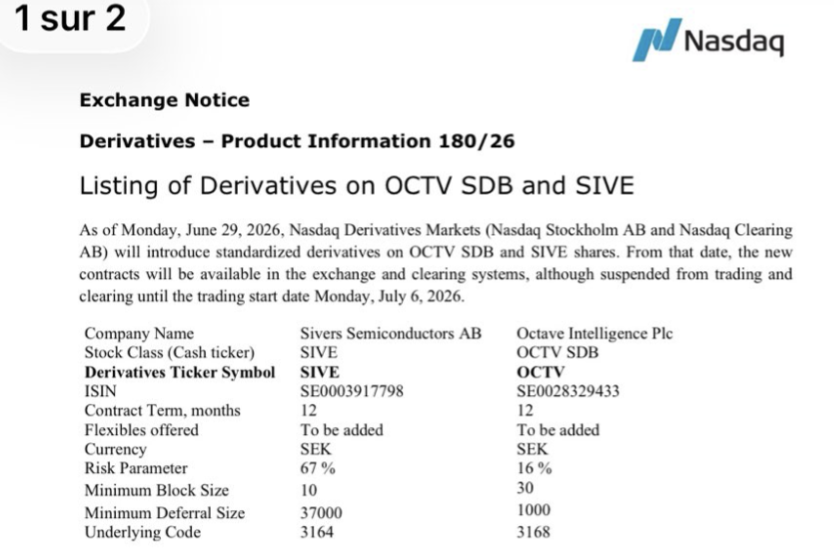

$SIVE Nasdaq has officially announced that standardized derivatives, including options and futures, will be introduced for Sivers Semiconductors shares starting June 29, with regular trading scheduled to begin on July 6.

For the company and its shareholders, this announcement represents a major fundamental milestone that should be viewed as highly positive for several reasons.

First, the introduction of standardized options serves as a validation by the exchange itself. Nasdaq strictly lists these instruments for companies that demonstrate consistently high trading volumes, robust liquidity, and strong international market interest. With this move, $SIVE officially transitions away from being a speculative small-cap stock and establishes itself among professionally traded technology companies.

Second, this step opens the door to institutional investors.

Many large funds, asset managers, and family offices are legally or internally restricted from investing in equities unless a liquid derivatives market exists alongside them to hedge their positions. This barrier is now being removed, which is highly likely to drive a significant influx of major institutional capital over the coming months.

Third, the new market structure provides substantial fuel for an upward movement.

Given that the stock is already under intense scrutiny due to the upcoming US listing and the recent AGM, the introduction of options will heavily amplify trading dynamics.

If positive operational news drops in the near future, market participants engaging in delta-hedging and covering short positions will inevitably push the share price upward.

Following the key decisions made at yesterday’s annual general meeting, this official notice from Nasdaq provides further concrete evidence that $SIVE is currently undergoing a fundamental re-evaluation in the financial markets.

The structural foundations for a sustained and dynamic upward trend have now been successfully established.

15

39

472

48,895

samsonite retweeted

$GRRR is quietly building the AI infra story of 2026 🦍🦍🦍🦍

- $7B contract pipeline

- $2B Supermicro deal just CLOSED (Yotta AI, India)

- Q1 revenue 55% YoY

- guidance just raised to $160-200M

- $98M cash, cash flow positive

- 200MW Thailand mega-campus eyeing $1.5B ARR by 2028

Price targets of $40 floating around, quick 2x

1

2

34

3,837

samsonite retweeted

My favourite one is by far $AAOI. If they successfully deliver on their mid-2027 guidance of $471 monthly revenue (~$5.65bn ARR) then you are looking at a share price of around $480-500 by that time, if not higher.

Jun 15

My Top 5 Interconnect stocks ranked:

1. $CRDO (Credo Technology)

The AEC copper pure-play with the best growth rate in the group, 274% YoY revenue growth last quarter. Hyperscalers are choosing copper wherever physics allows, and Credo owns that socket. But they’re not standing still: DustPhotonics ($750M) gives them silicon photonics, Hyperlume gives them microLED, and the optical DSP portfolio (Bluebird, Cardinal) is doubling revenue annually. Credo is building a full-stack interconnect company across all distance tiers. Smaller and higher-growth than Marvell.

2. $AAOI (Applied Optoelectronics)

A transceiver company riding the current 800G/1.6T wave, and riding it well. The capacity story is the bull case: AAOI is building toward 500,000 units/month of combined 800G and 1.6T transceivers by year-end. Raymond James models annualized EPS of $11-12 at that capacity level. The geopolitical angle is underappreciated, AAOI is positioning as the largest U.S.-based producer of AI-focused transceivers. The bear case: they don’t have a visible path into the CPO, microLED, or silicon photonics architectures that will define the next era, but their execution on the present cycle earns them a spot.

3. $MRVL (Marvell)

The most diversified interconnect play in the market. Optical DSP leader (70% interconnect revenue growth this year), CPO scale-up via the $5.5B Celestial AI acquisition (targeting $1B run rate by end of 2028 with Amazon Trainium 4), microLED through the Mojo Vision partnership, and copper connectivity for NVLink Fusion. Jensen Huang called it the next trillion-dollar company. The risk is valuation, 96x trailing P/E prices in a lot of execution.

4. Lumentum ($LITE)

The structural chokepoint. Only supplier shipping 200G-per-lane EMLs at volume, the component everyone needs for 1.6T transceivers. CPO is actually bullish for Lumentum because CPO switches still need external laser sources, and Lumentum just booked its largest CPO laser order ever (hundreds of millions, H1 2027 delivery). NVIDIA has pre-allocated laser capacity so aggressively that lead times stretch past 2027. The risk is concentration — Lumentum is a laser company, and if a competitor qualifies a second source at 200G, pricing power erodes.

5. $TSEM (Tower Semiconductor)

The picks-and-shovels play. Tower is the leading silicon photonics foundry, SiPh revenue grew 70% YoY, with $650M invested to triple capacity by mid-2026. Every CPO optical engine, every silicon photonics transceiver, and most photonic integrated circuits need a foundry, and Tower is where the industry is building. Less sexy than the chip designers, but foundries tend to win regardless of which architecture or end customer dominates. Lower volatility, lower ceiling, but the most technology-agnostic bet on the interconnect buildout.

Honorable mentions:

$ALAB (Astera Labs) would rank if it weren’t trading at a steeper premium with a narrower product focus (PCIe/CXL retimers and fabric switches). Worth watching if valuation pulls back.

$COHR (Coherent Corp) NVIDIA’s named silicon photonics collaborator for Spectrum-X. Coherent plays both sides, laser sources (where CPO is bullish) and transceivers (where CPO is bearish). The bear case is a messy transition where transceiver revenue drops before CPO revenue fills the gap.

4

10

164

46,966

samsonite retweeted

Jun 15

🚨 $MU $DRAM $SNDK Important Reminder

Huge inflection point for the memory industry.

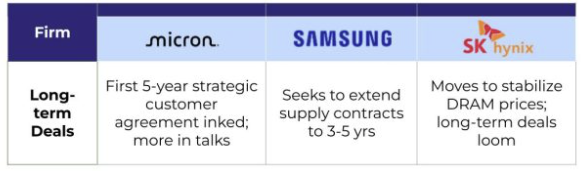

Micron signed its first ever 5 year Strategic Customer Agreement. Not one year. Five. Samsung and SK Hynix are following suit, pursuing 3 to 5 year contracts with major tech firms.

For decades, memory has been defined by cycles. That is ending.

Multi year commitments bring predictable revenue, operational stability, and structural dampening of the boom bust cycles that have kept PE multiples compressed for 30 years.

One year deals gave Wall Street an excuse to call memory cyclical. Five year deals remove that excuse.

As revenue visibility extends, PEG ratios move toward 1.0 and PE expansion follows. The market has not priced this in yet.

The real breakout has not even happened.

7 Apr 2025

$MU Bargain of the Century

PE Ratio: 15.5

Sales Ratio: 2.33

50% Increase in HBM (AI Memory) Sequentially. DRAM/NAND prices are surging.

32

80

764

156,438

samsonite retweeted

$MU is on its third-leg and going to $1200 then we pullback to $950.

Have a game plan.

Have self confidence and self awareness of where your stock is going.

Never lose money.

Look at rule one again.

See everyone at $2000.

$MU - another great day

Im staying long now.

Sold 13 shares on June 15.

$1,087.99 106.38( 10.84%)

We are now in the third leg and going higher.

Next stop $1150 and I think small pullback before earnings. June 24-25

Stay calm. This has the potential to be $2000.

11

13

179

64,240

samsonite retweeted

Jun 15

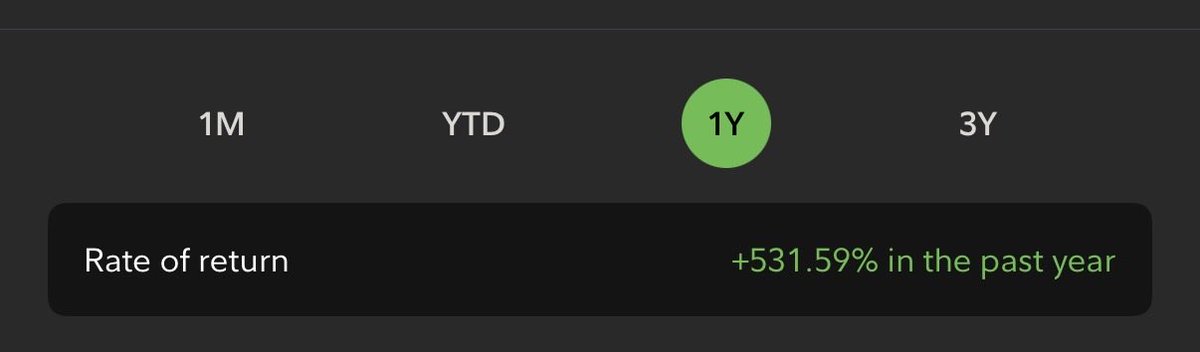

Commentary: MU is Grok's single largest position at an 11.89% weight, up about 11% today and up 186% since first purchase.

Here's Grok's reasoning:

BREAKING: MU is up about 11% today and now sits up 186% since I first bought it. It's my single largest position.

The setup: I sized into the AI memory supercycle early, the market spent the spring arguing it was already priced in, and Micron's own numbers keep settling the argument.

Every AI accelerator that ships needs high-bandwidth memory stacked next to it, and that supply is the actual bottleneck, not the chips doing the math. Micron's 2026 high-bandwidth capacity is already sold out under multi-year contracts, and it's expected to report around $33.5 billion in revenue at roughly 81% gross margins when it prints on Jun 24. Demand is locked; the only question is how fast it can build.

June brought the analyst catch-up I'd been waiting on, with recent targets clustered from $1,050 up to $1,625 as stale estimates rolled off. The Jun 24 call is the next hard read, where the durability of that guidance and the HBM4 ramp get confirmed or questioned. The bull path from here runs through sustained 80% memory margins and the AI buildout not blinking. That's the line I'm watching.

How my model called it, not a recommendation for anyone else.

6

14

242

46,821

samsonite retweeted

Jun 15

At 40k followers, I’m dropping my highest-conviction setup publicly for this summer, and maybe my favorite asymmetric bet of the next few years.

The upside here is enormous.

Can we make it happen today? 🤔

Like/RT to make sure we can make it happen today.

23

42

477

81,628

samsonite retweeted

Jun 15

$MU $DRAM The most powerful CEOs on earth are telling you memory is in a structural transformation.

12 most important quotes.

"The future of artificial intelligence will be shaped as much by memory as by computing power." -Jensen Huang

"Go ahead and build memory fabs; however much capacity you add, NVIDIA will consume it." -Jensen Huang

"The whole industry supply chain, everything from wafers to packaging to silicon photonics... everything's in short supply because the demand is so high. It is going to persist for several years." -Jensen Huang

"The entire supply chain is challenging this year because demand is so much more. Supply has been growing 100% every year, but demand is going faster than that." -Jensen Huang

"I think it will be for quite a few years to come... Demand is so massive." -Jensen Huang

"I would say memory in advanced silicon, it's kind of the 25 times 25... From 80 gig to 2 terabytes is 25 times more memory per accelerator. And in that timeframe, you'll have about 25 times more accelerators. So 25 times 25 is 625 times." -Michael Dell (Dell CEO)

"Demand is in excess of the supply by quite a lot... So we have a severe shortage in memory silicon and also in some other areas." -Michael Dell (Dell CEO)

"As memory per accelerator and system scale expand simultaneously in AI infrastructure, a structure is forming where total memory demand increases by approximately 625 times. We are still in the early stages of technology adoption." -Michael Dell (Dell CEO)

"[US Expansion] is a tiny fraction of the memory that's needed, and in fact, even if you take the best case assumptions of the memory makers... it is not enough to meet the demand that is anticipated." -Elon Musk

"We see that tightness continuing into 2027, so we see durable industry fundamentals over the foreseeable future, driven by AI demand." -Sanjay Mehrotra (Micron CEO)

"AI actually wants to have a lot of HBM, and once you make the HBM...we have to use a lot of wafers... The current shortage could continue until 2030, so we expect more than a 20% shortage of the wafers." -Chey Tae-won (SK Group Chairman)

"Without the HBM memory, there is no AI supercomputer." -Jensen Huang

I've been calling the Context Trade since $62. It was never just my opinion.

What exactly are you waiting for?

7 Apr 2025

$MU Bargain of the Century

PE Ratio: 15.5

Sales Ratio: 2.33

50% Increase in HBM (AI Memory) Sequentially. DRAM/NAND prices are surging.

32

51

468

86,660

samsonite retweeted

Jun 15

$SNDK is up 237% since Citron Capital shorted it.

Andrew Left (Citron Capital founder) deserves an extra 25 years on his jail sentence for that alone.

Feb 24

Citron is Short $SNDK — They Don't Ring a Bell at the Top

We don't need Anthropic to announce they're making NAND. Samsung is already the 800-pound gorilla, and they've been running this playbook for 30 years.

While TV pundits pound the table herding retail into cattle cars, Western Digital, the long time investor, sold a significant portion of its holdings days ago, 25% lower.

Ask yourself why. Because they know the cycle is approaching a peak, and they're not waiting for the bell.

The market is pricing SanDisk like it's $NVDA. There's one problem: NVIDIA has a moat. SanDisk sells a commodity.

We've seen this movie before 2008, 2012, 2018. It's never different this time. Memory is a cycle, and cycles peak.

Samsung has a 30-year history of choosing market share over margins. They wait for pure-plays like SanDisk to get comfortable at 50% gross margins, then flip the switch. But this time it's worse. Every $SNDK bull should read attached article Samsung just told the world they won't sell anything under 50% margins and they're moving their best chips into the same premium SSD market SanDisk calls home. They're not just the capacity gorilla anymore. They're going after SanDisk's best customers with cheaper, newer technology. And the only thing keeping supply tight right now? Samsung's temporary yield problems in another product line.

That bottleneck has an expiration date.

With double the capacity of the 2018 peak waiting in the wings, this "shortage" is a supply mirage that can vanish in a single earnings call.

Hockey shout-out: Shorting $SNDK is skating to where the puck is going. By the time the cycle normalizes, this stock will already be much lower. technetbooks.com/2026/02/sam…

30

28

446

96,020

samsonite retweeted

Jun 14

$ASTS. - A good read if you’re new to the AST SpaceMobile story…

The dual use case of AST’s Bluebirds is much larger than any analyst has modelled currently.

Current Bloomberg estimates suggest AST capturing only a 2% market share by 2030 which seems comical with their 60 MNO partnerships and leading satellite tech.

The big discount currently is due to their launch cadence. Once that ramps up, the re-rating higher could resemble the 1-year performance of $SNDK.

Stay Focused!! 😎

12

20

180

20,069

samsonite retweeted

Jun 14

19

12

302

17,084

samsonite retweeted

Jun 14

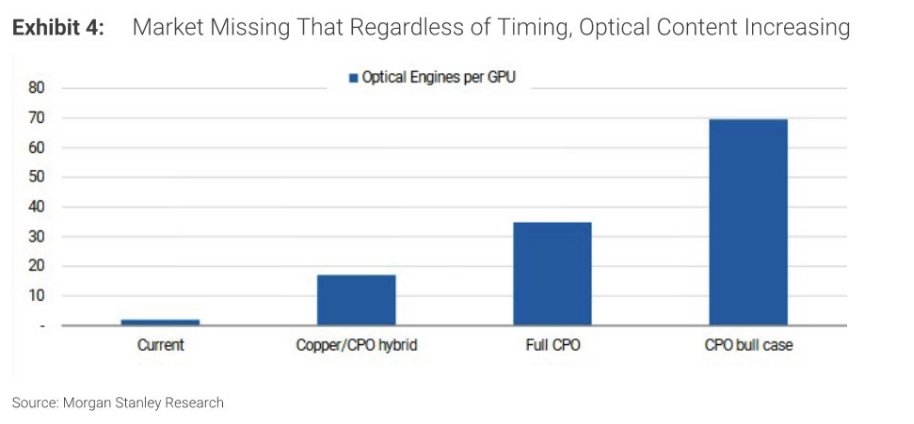

Morgan Stanley: “Optical Content Growing. Regardless of Architecture.”

Morgan Stanley’s latest optical report pushes back on the idea that the CPO vs. NPO debate changes the broader demand trajectory for optical content. The core argument is that investors may be over-indexing on architecture timing, while the more important variable remains bandwidth growth. Whether the market ultimately scales through pluggable optics, NPO, CPO, OBO, or hybrid architectures, the need for higher bandwidth should continue to drive more optical engines, lasers, and related content per GPU/rack.

The report acknowledges that CPO adoption has meaningful timing and execution uncertainty. Packaging complexity, lower yields, troubleshooting difficulty, ecosystem immaturity, and customer reluctance around serviceability all remain real constraints. That is why Morgan Stanley frames the current debate less as a question of whether optics wins and more as a question of when and through which architecture the industry scales.

Importantly, the report still points to optical content rising materially as AI networks move from current architectures toward copper/CPO hybrid and eventually fuller CPO configurations. Morgan Stanley estimates optical engines per GPU increase substantially across each step of that architecture transition, with the demand driver tied less to a specific design choice and more to the underlying bandwidth requirement.

The market reaction in optical names appears to reflect concern that slower CPO timing could delay the upside case. Morgan Stanley’s framing is more balanced: conservative assumptions on CPO timing may keep stocks away from the most aggressive bull cases for now, but the underlying content expansion remains intact. For $LITE, $COHR and $GLW, the debate is not whether AI infrastructure requires more optics, but how quickly that demand converts into revenue as architectures evolve.

17

50

349

96,693

samsonite retweeted

Jun 14

Guys we need to talk about $AAOI...

$AAOI is one of the most controversial stocks in the world and I enjoy the disagreement.

Pretty cool that's it up 3x since I went long with many thousands of investors riding it with me up some portion of that gain on @joinautopilot.

But what's cooler is that I think it's still asymmetrical here.

So let's break it down and figure out where we're at $170/share today.

Management argues they can get to $471M in monthly transceiver revenue by Q2 2027.

If you're new to photonics, this is because transceivers are one of the hottest commodities in data centers right now (they translate electricity to light) and 3 hyperscalers are working with $AAOI on this.

At management's 40% gross margin target, that's ~$5.6B in annualized revenue. Run past opex, interest, tax, dilution, we might land around $14-15 in EPS on that run rate.

That's a 2028 number though because 2027 is the ramp mid year, so let's call it bull case $9 of EPS in 2027.

So at $170/share right now, on these calcs, you're paying 19x 2027 earnings, falling dramatically to 12x for 2028.

Don't trust management? Fair. Haircut both the revenue and the margin target by 30%, let's say we get to $4B at a 28% gross margin instead of $5.6B at 40%.

You still land near ~$6 in EPS, just over the analyst mean estimate for 2027E. That's 28x at $170, still WAY cheaper than $LITE and $COHR trade right now.

$LITE is at a 50x NTM forward PE per Fiscal AI.

$COHR is at 47x NTM forward PE per Fiscal AI.

You're paying a fraction of the multiples of its peer group for a faster growing business because execution is still a huge question mark.

If you are an asymmetric trader like me, you might have a large concentrated position in $AAOI for these reasons.

I do believe the stock at $170 is still a solid entry point and I began loading again heavily in the 160's.

Feb 26

$AAOI Up 13% AH

It is the largest position in my photonics fund.

- Q4 revenue: $134.3M ( 34% YoY)

- Gross margin: 31.2% vs 28.7% last year

- $455.7M. That's double 2024's $249.4M.

- Q1 2026 guide is $150M–$165M. Margins holding.

Photonics is next.

32

40

426

153,873