professional roundtripper trying to survive | tweets are own views and not financial advice | @kuromifnf

Joined November 2021

- Tweets 2,673

- Following 1,177

- Followers 10,370

- Likes 7,857

226 Photos and videos

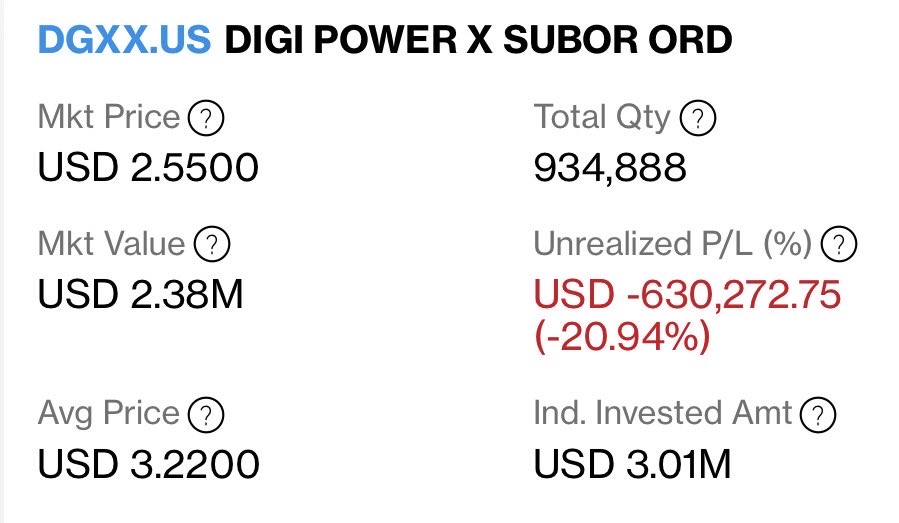

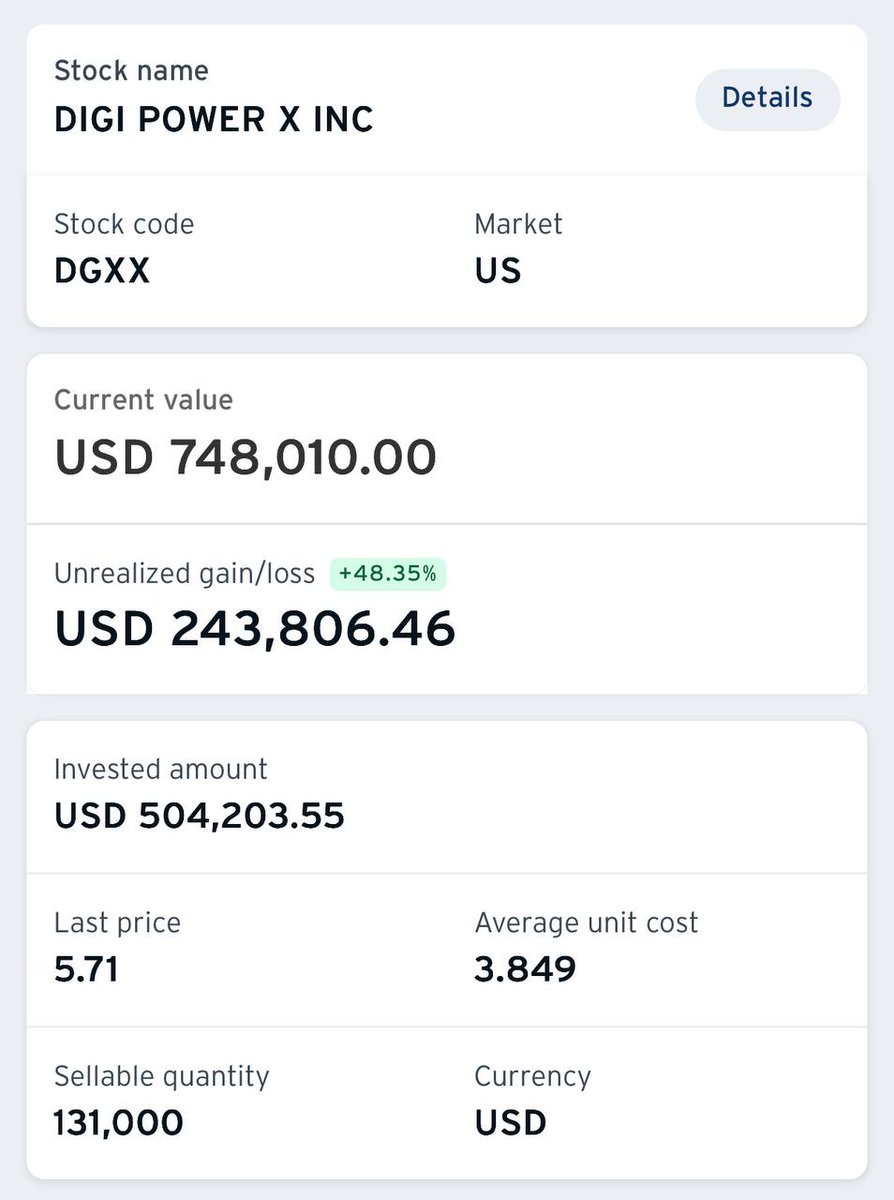

Six months ago $DGXX was a $200M bet on execution.

Today it is a $540M AI infrastructure play with 393MW of secured power and a Cerebras deal worth up to $2.5B, and still the cheapest AI infrastructure name on the board.

The follow up to my original investment thesis is now published and I am more bullish than ever.

x.com/rk8215/status/20650096…

8

14

101

13,891

Ethermonk 📿 retweeted

Jun 10

We’ve got NVIDIA B300s running 🚀

Blackwell, live at our tier 3 Columbiana facility. The frontier, online. $DGXX around the clock!

33

54

207

53,039

Jun 9

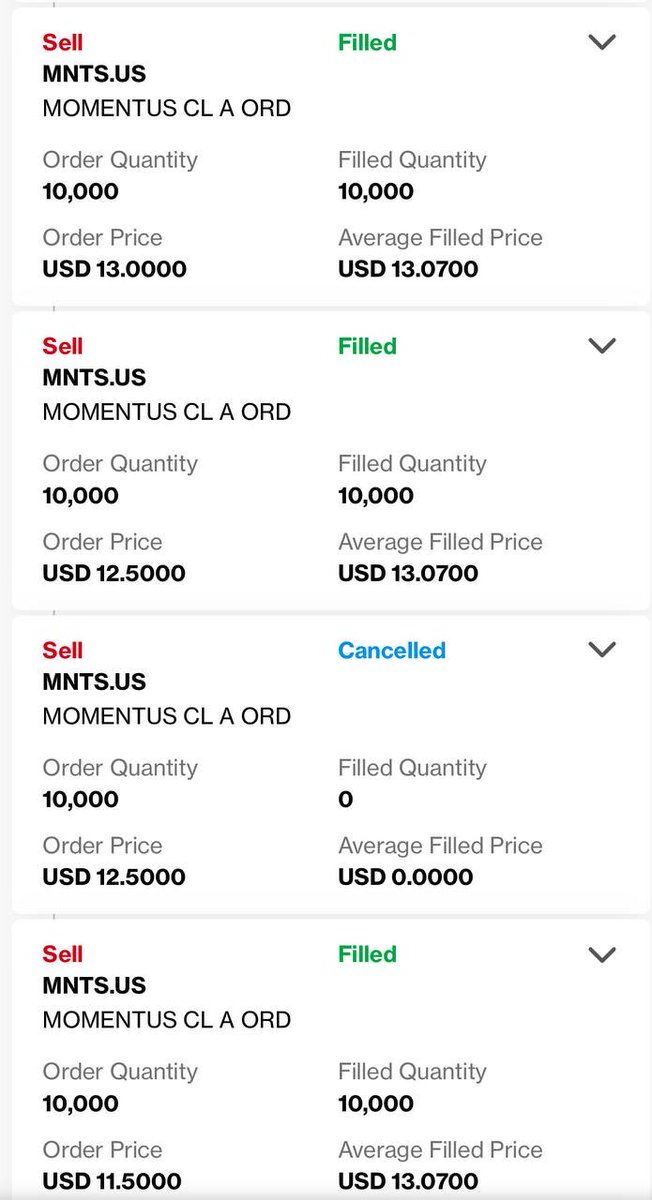

Momentus green in a sea of red tells you all you need to know

I added heavy at $12.28

See you in space 🚀

$MNTS

5

2

20

2,464

Jun 8

All these customers and $AMPG is still a ~$130m mcap penny stock

You do the math

But if @rk8215 tells me to buy, i’m not fading

Got an average entry of ~$5.40

BREAKING: $AMPG LAUNCHES A NEW WEBSITE. AMAZON $AMZN & NVIDIA $NVDA LISTED AS A CUSTOMERS!

Amplitech just released new website and first time ever they are listing $NVDA and $AMZN as their customers.

We were wondering who were the Fortune 50 customers and I guess we just got the answer.

This is absolute game changing news and I do believe the new website was released strategically now before the new contracts which they said they would announce soon.

amplitechgroup.com/

1

6

27

3,455

Jun 8

Biology is the most underappreciated destination for capital to flow into over the coming years.

It's the biggest TAM yet to be materially disrupted.

Two plays I like:

The lower risk 2-3x? $LLY

The higher risk 5-10x? $ABCL

$LLY first.

Most are still pricing this as a pharma company. That's the mistake.

GLP-1s (Mounjaro/Zepbound) aren't the thesis. They're the nearer term funding engine.

$LLY is building the operating system for human biology.

Think of it just like AWS giving developers infrastructure to build software...Eli Lilly is building the infrastructure to build medicines.

-> Discovers targets

-> Designs molecules

-> Learns from every experiment

Here's what it actually looks like:

-> LillyPod: 1,000 Blackwell GPUs. A wholly owned AI factory for biological discovery.

-> Isomorphic Labs: Frontier AI drug design plugged into their pipeline.

-> TuneLab: BioTech partners train on decades of Lilly's molecular data.

30x PE probably seems pricey right now but if this thesis plays out it's not.

Now $ABCL:

Earlier stage. More focused. More niche. Potentially huge upside if AI drug discovery works at scale.

Every company sitting on years of proprietary biological data should get re-rated.

$ABCL is arguably the best one out there for that at $1.7B MC.

3

2

18

4,580

Ethermonk 📿 retweeted

Jun 3

Tenne (the man who helped write drone laws for America and $ONDS from $0.3 to $10 ) didn't just leave Ondas for Draganfly.

→ Jan 2025: He's already CEO of Corlens (metalens)

→ April 2026: Walks away from a $7B platform.

→ May 2026: VP Global Strategy at $DPRO May 2026.

Then DPRO signs exclusive Americas deal with Blitz Corlens Inside.

A 30-day "coincidence" doesn't sign exclusive distribution agreements.

Nothing about this was last-minute.

This is a steak they already cooked for a while.

I'm long Draganfly.

Jun 2

$DPRO - Thank you for the $7.27 dip.

✅ Fully diluted: $300M (USD).

✅ Zero debt with cash.

✅ Citadel owns 5%.

✅ Gov talking about $$ into drones.

✅ Ukraine seeks a major deal with US.

✅ Draganfly been in Ukraine since 2022.

✅ $ONDS goat just joined to surpass $AVAV.

✅ Feeding TMobile with drones, lifting cell towers, etc etc (could be NOK x NVIDIA).

✅ Developing stuff for DEVCOM (army).

✅ 27 years track record.

✅ CEO pretty confident they will meet TTM.

Was easy buy for me.

4

37

20,763

Jun 1

Full size position deployed on $DPRO.

Average somewhere around $7.30.

I highly suggest reading through @chinoalemano’s deep dive on the company. One of the better breakdowns I’ve seen so far.

Furthermore, @aleabitoreddit previously held a position in $DPRO too. If you know his track record, you know he doesn’t randomly touch garbage.

Now add this to the equation:

The US government is actively discussing investments into drone companies and domestic drone infrastructure.

Meanwhile $DPRO is sitting around a ~$300M market cap.

Feels like one of those setups where people only realize the opportunity after it’s already repriced 2-3x higher.

May 28

Started a decent amount of $DPRO position @ $7.25 avg.

With the Trump Administration reportedly in talks to fund U.S. drone companies, the entire drone sector could be gearing up for a major rerate. Historically, these kinds of headlines tend to spark strong moves across drone names even before the real momentum kicks in.

Still a speculative play, but R/R here looks very attractive in my opinion. Feels like one of those themes that can run hard once attention rotates in.

3

4

23

13,823

Ethermonk 📿 retweeted

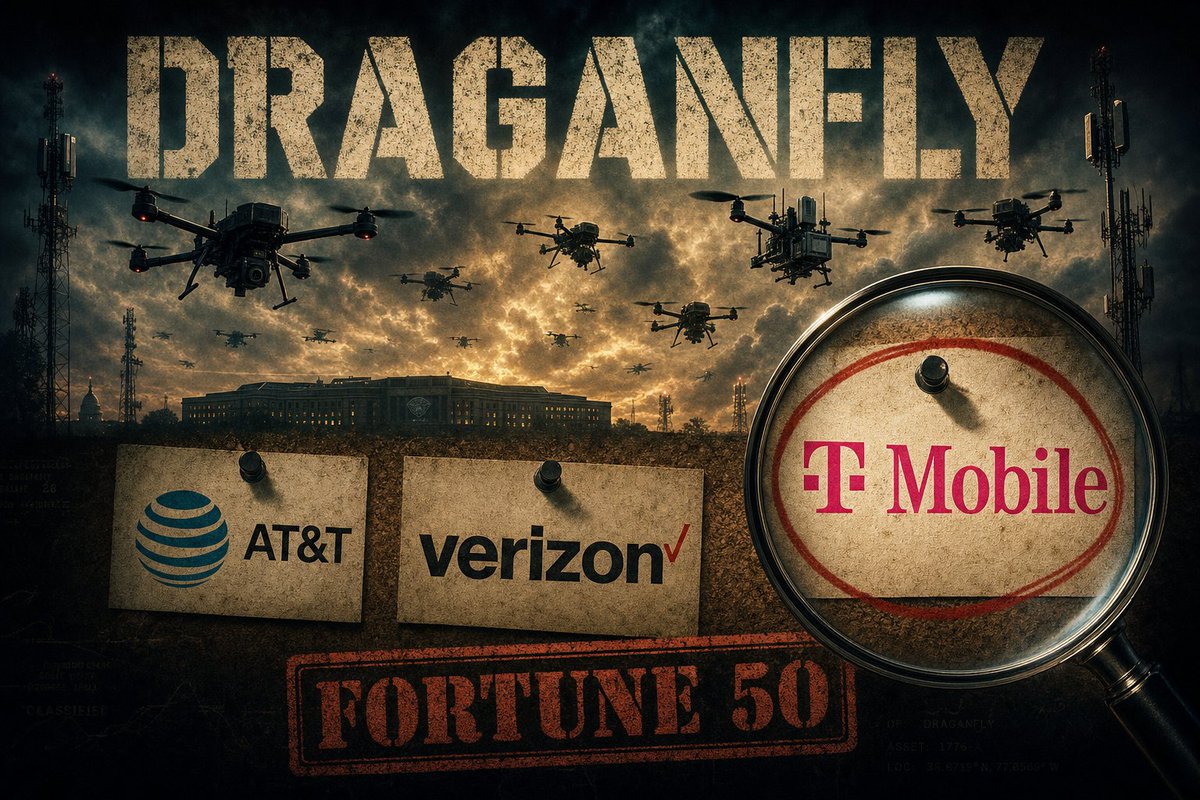

May 30

🚨 A Fortune 50 company is secretly ripping out its ENTIRE Chinese drone fleet… and replacing it with a $300M drone company.

They refused to name themselves.

So I played detective.

And the answer flipped on me at the very end.

The stock is $DPRO. Draganfly.

On the earnings call, the CEO dropped it and clammed up. All he'd say: the buyer is a "Fortune 50 telecom" switching its entire Chinese fleet to Draganfly heavy-lift drones, lifting cell towers, restoring comms when the grid goes down. And they already placed a SECOND order to expand the fleet.

That phrase: "Fortune 50 telecom", was the only clue.

So I ran it down. 🕵️

Step 1: Only THREE telecoms crack the 2025 Fortune top 50; Verizon (#30), Comcast (#35), AT&T (#37).

Step 2: Kill the impostors.

❌ Comcast = cable. No towers to lift.

That leaves AT&T vs Verizon.

I was ready to bet AT&T (FirstNet = federal mandate to dump Chinese DJI drones)…

…until I checked WHO actually closed the deal. 🤯

The sale ran through a tower-services firm, Infinity Communications.

The exec they put on stage, their National Disaster Recovery Director, spent 20 YEARS at T-Mobile, including running T-Mobile's Disaster Recovery program from 2017–2020.

The man who BUILT T-Mobile's disaster recovery is now the one selling these drones.

Salesmen bring their old clients with them. 👀

The catch? T-Mobile is ~#55, NOT technically Fortune 50. So either Draganfly got loose with "Fortune 50"… or it's AT&T/Verizon after all.

But that human breadcrumb?

It points straight at T-Mobile.

And here's the macro bomb that drops on top of ALL of it: this week the Pentagon was reportedly in talks to take direct EQUITY STAKES in American drone makers, actual government ownership, under Trump's "Drone Dominance" push for 300,000 drones by 2027.

The government doesn't just want to buy American drones.

It wants to OWN the companies that build them. 🇺🇸

And obviously, IMHO, getting ground comms back up is a priority if war breaks out.

Stack it:

✅ A blue-chip carrier flipped its ENTIRE fleet to Draganfly (and reordered).

✅ DJI on the path to a US ban → forced replacement cycle nationwide.

✅ Washington moving to bankroll the whole American drone complex.

✅ Draganfly: one of the only NDAA-compliant North American makers shipping today, sitting on ~$100M cash with no debt.

One carrier already flipped.

The government's reaching for its checkbook.

Not financial advice.

Just connect the dots before the crowd does.

ALT Draganfly ($DPRO) customer is probably T-Mobile ($TMUS).

8

8

56

13,723

May 29

Top blasted more $ABCL at $6.

Still early imo and people are trying to get positioned before phase 2 news.

This is relatively longer TF hold for me and will add more on dips

May 12

Bought a lot of $ABCL at an average of ~$4.5

Not the best entry considering it ran off the lows already, but in the grand scheme of things I think it’s still pretty early.

Might take awhile for it to hit multiples, but so far phase 1 results on the earning call yesterday was largely positive which is the main thing I was looking out for.

1

1

20

2,159

May 28

Started a decent amount of $DPRO position @ $7.25 avg.

With the Trump Administration reportedly in talks to fund U.S. drone companies, the entire drone sector could be gearing up for a major rerate. Historically, these kinds of headlines tend to spark strong moves across drone names even before the real momentum kicks in.

Still a speculative play, but R/R here looks very attractive in my opinion. Feels like one of those themes that can run hard once attention rotates in.

3

3

34

12,441

May 26

Insane rally for $MNTS on premarket trading.

Already hit $10, close to 100% in 4 days, volatility swings both ways, and that’s the beauty of smaller caps.

Space theme still running hot so won’t be selling this that early, could easily do another 100-200% from here before $SPCX IPO.

LETS RIDE!

May 21

3

2

16

5,166

Ethermonk 📿 retweeted

May 21

Trading’s the most brutal profession

Someone at rock bottom today will be retired in 2 years

Someone who peaked today will round trip everything in the next 2 years

You made it? They call you lucky

You lost it? They call you gambling addict

178

241

2,843

386,609

May 21

I accumulated about 1% of $MNTS at ~$5.50 for exposure to Space stocks

With the upcoming $SPCX IPO, I fully expect the whole sector to continue front running the hype.

Still pretty under the radar as it’s a micro cap stock of ~$70M mcap, but has the likes of Ken Griffin taking up a 10% position.

11

2

34

18,268

May 15

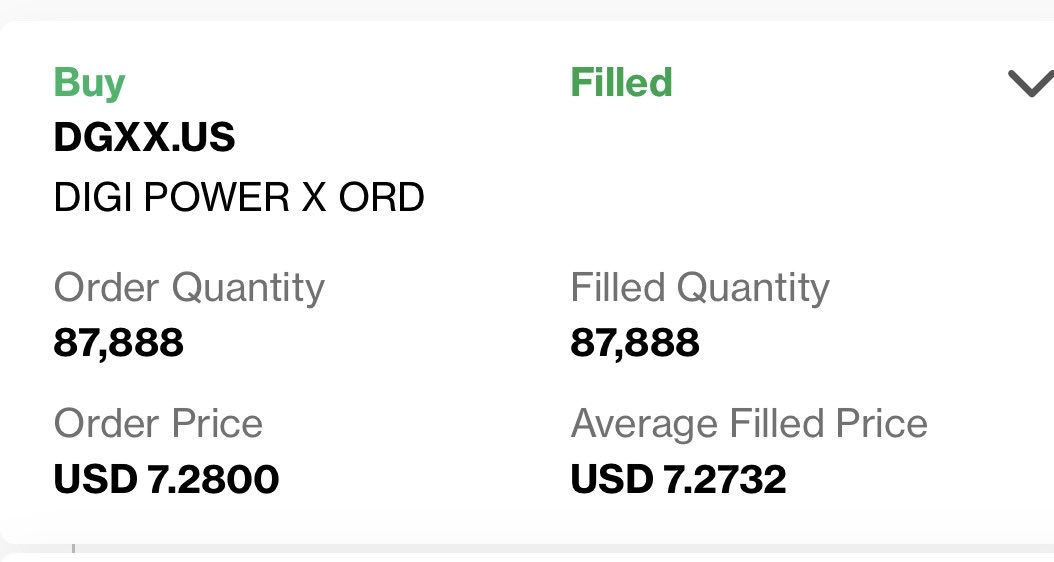

I added more $DGXX today to my already huge bag.

More orders lined up between $6.5-6.8, not sure if we get filled on those though.

Still strongly believe that it is a much better buy here at $7 than at $2-3 a few months ago, simply because there was real execution risk back then and the company has now proven itself with $CBRS & SubQ.

Furthermore, today earnings call was pretty bullish, with @michelamar3 confirming that there will be no further ATM as well as company plans to scale.

I think the strength is pretty telling and we will see this rerate 3-4x minimally from here over the next few months.

21

13

153

9,796

Ethermonk 📿 retweeted

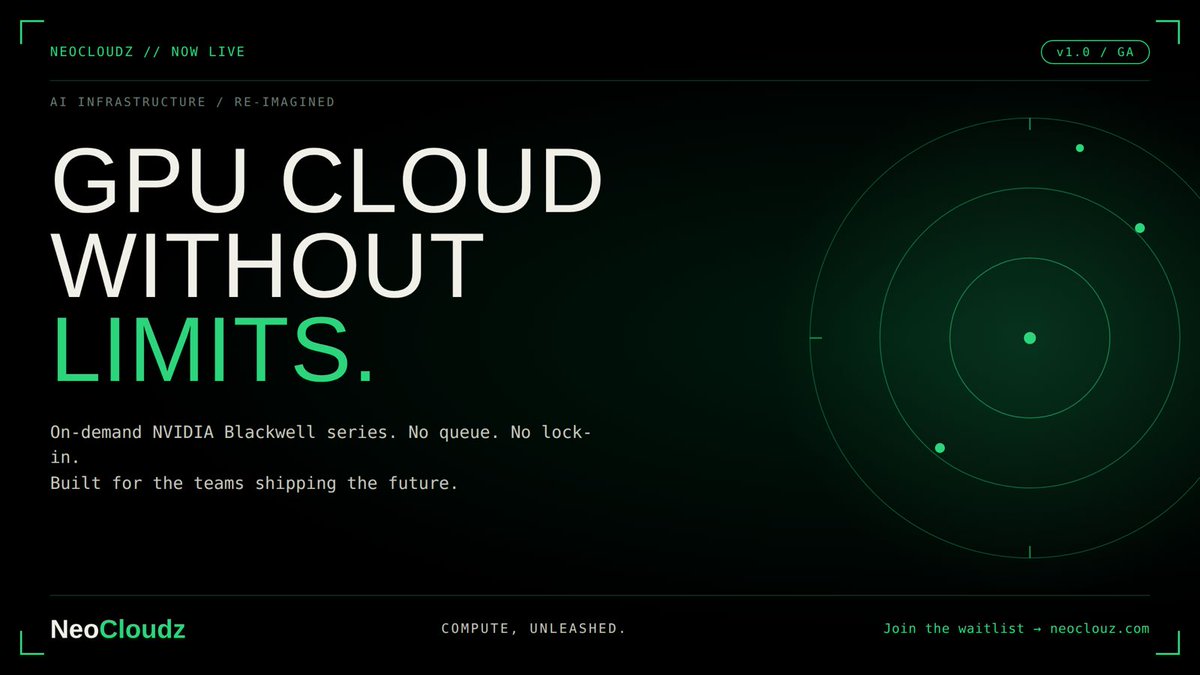

May 13

@Neocloudz is now live — bringing on-demand GPU cloud infrastructure to teams building the future of AI.

As a fully owned AI cloud platform of DigiPower X Inc. (NASDAQ: DGXX), NeoCloudz is designed to deliver high-performance GPU compute with the speed, flexibility, and scalability today’s AI builders need.

Powered by NVIDIA Blackwell series infrastructure, NeoCloudz is focused on removing the friction from AI compute access — no long queues, no unnecessary delays, and no limits on what ambitious teams can build.

From AI labs and enterprise teams to developers pushing next-generation models, NeoCloudz is built for one clear purpose: making powerful GPU cloud infrastructure more accessible, reliable, and ready when demand is moving faster than ever.

This is not just another cloud platform.

This is GPU cloud without limits.

Join the waitlist: neocloudz.com

#neocloudz #digipowerx #dgxx #aicloud #gpucloud #nvidia #blackwell

6

16

81

25,009

May 12

Bought a lot of $ABCL at an average of ~$4.5

Not the best entry considering it ran off the lows already, but in the grand scheme of things I think it’s still pretty early.

Might take awhile for it to hit multiples, but so far phase 1 results on the earning call yesterday was largely positive which is the main thing I was looking out for.

2

4

45

4,599