CTO @subyhq | Engineering the payment stack that scales with your business

Joined December 2018

- Tweets 337

- Following 707

- Followers 260

- Likes 882

6 Photos and videos

Suby v3 soon.

Your customer taps Apple Pay or pays by card. You get USDC. Your customer pays in BTC. You receive fiat.

Cards, Apple Pay, Google Pay, stablecoins, crypto and more in. Bank or stablecoins out.

Auto-swap does everything in between.

New app, fully rebuilt.

The gap between cash and crypto just disappeared.

8

15

29

6,473

R1 | Suby retweeted

Kohaku, the gateway to Ethereum privacy, is coming soon to a wallet near you.

35

48

432

80,410

R1 | Suby retweeted

May 22

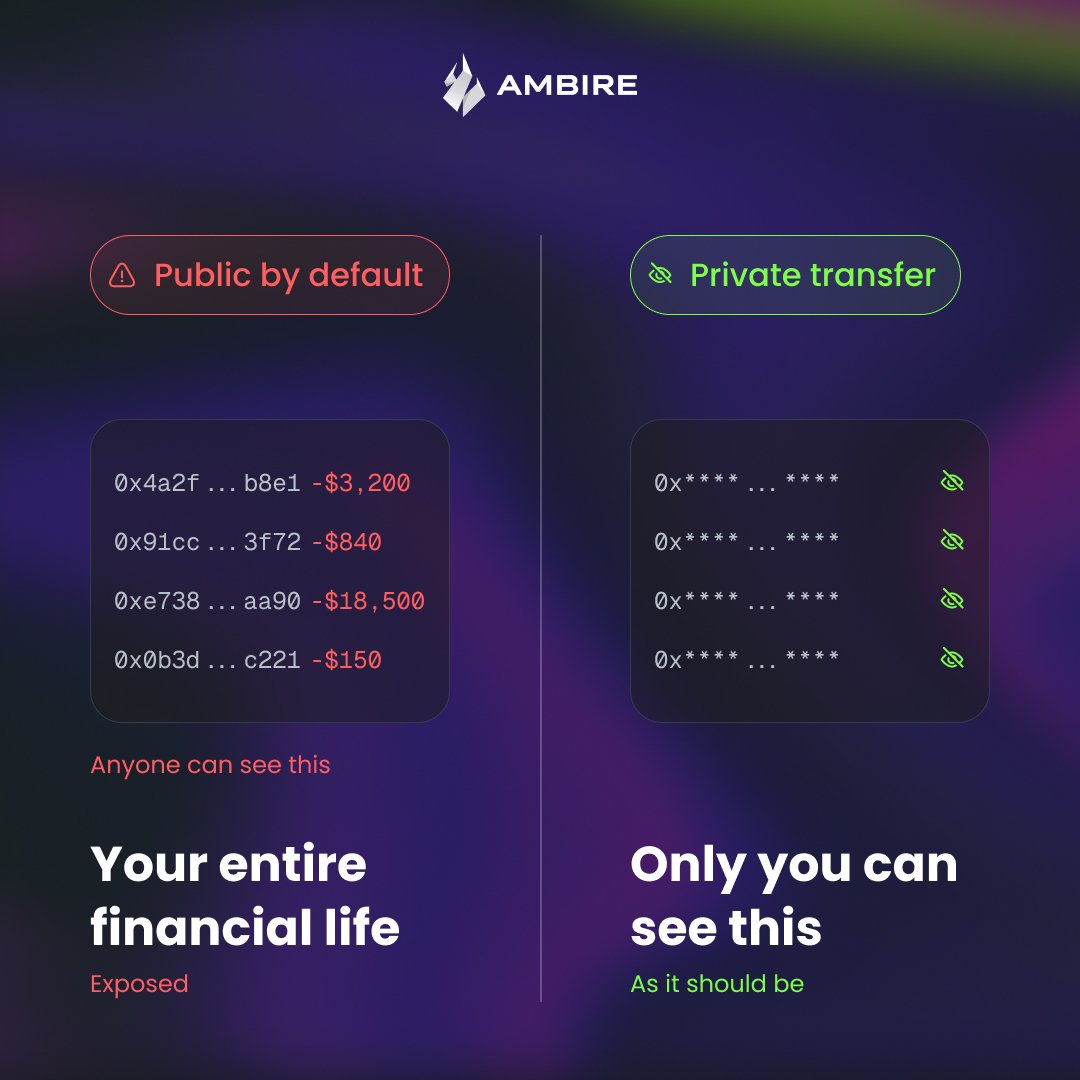

Private transfers are coming to Ambire.

Imagine the power of @RAILGUN_Project & @0xprivacypools built into your wallet.

Study Kohaku.

Mar 4

Every time you send crypto, your entire account history is visible to the receiver.

All public, forever. But that's about to change.

Learn more about private transfers, the missing layer in wallet UX:

8

11

81

12,301

R1 | Suby retweeted

May 18

Real talk: our landing page sucks.

I made it. I'm not a designer. It shows. Shipped it back in January thinking "good enough." then attention started rolling in and I realized good enough wasn't.

So we're redoing the whole thing.

Working with @BoneLLC for weeks now, easily the best agency out there.

Sneak peek attached. Don't mind the copy, that's changing too.

Suby's about to look the way it deserves to.

Thanks @Flexing & @gadzinski_

5

4

28

3,095

May 11

you should read this

60

R1 | Suby retweeted

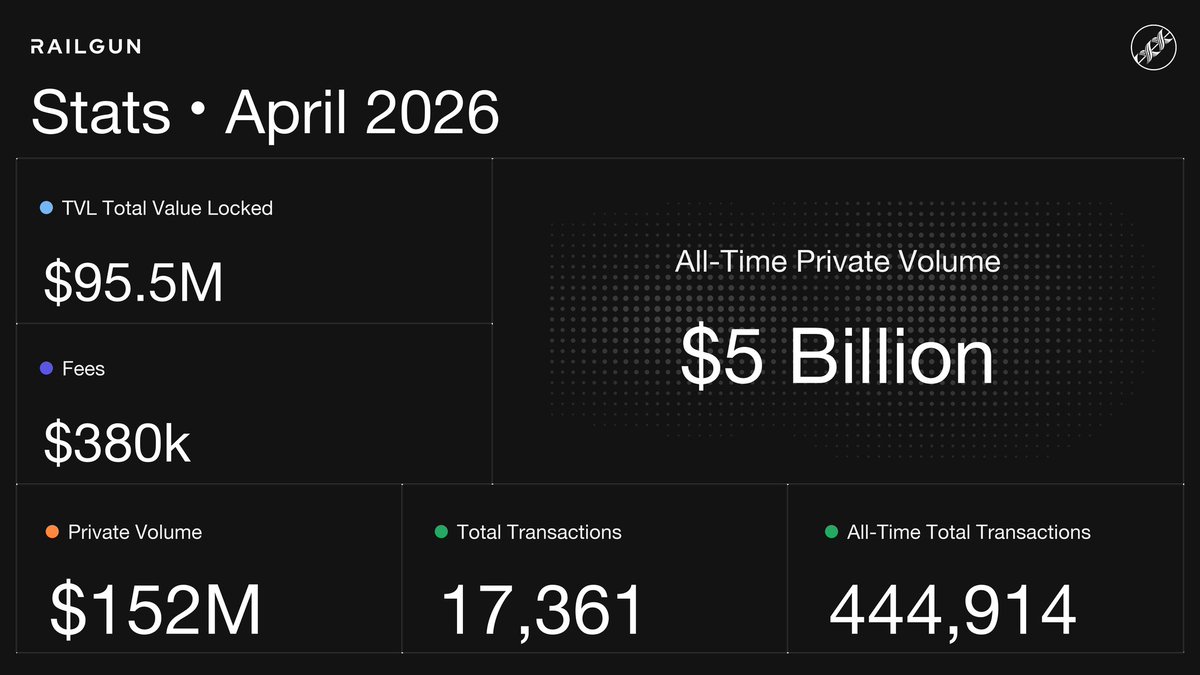

The proof goes on-chain. The details do not.

6

15

107

8,413

Payments are simply better on Base

Apr 23

I sent €5,000 across 8 payment rails. The fastest arrived in 2 seconds. The slowest took 5 days. And the fees? $235 difference on the exact same transfer.

Here's what that experiment taught me about the future of money.

Rail #1: USDC on Base: 2 seconds, $0.01 fee The recipient received $5,882.50.

Rail #8: SWIFT Wire: 5 days, $25 1.5% FX markup The recipient received $5,794.26.

Same sender. Same recipient. Same €5,000 on Monday. One settled before I closed my laptop. The other arrived on Friday.

𝗡𝗼𝘄 𝘇𝗼𝗼𝗺 𝗼𝘂𝘁.

In 2025, stablecoins processed $33 trillion in volume. Visa processed $16.7 trillion. For the first time in financial history, a "crypto" rail moved more value than the world's largest card network.

Most people missed it. The financial press barely covered it. But inside every major payment company, someone is reading those numbers and losing sleep.

𝗪𝗵𝘆 𝗶𝘁 𝗺𝗮𝘁𝘁𝗲𝗿𝘀 𝗳𝗼𝗿 𝘆𝗼𝘂𝗿 𝗻𝗲𝘅𝘁 𝗽𝗮𝘆𝗺𝗲𝗻𝘁

Ask anyone: "Is paying by card instant?" They'll say yes.

They're wrong.

What's instant is the authorization, the 2-second green checkmark that tells the merchant "this card is legit." The actual money? It sits in batch processing queues for 1 to 3 days, hopping between acquirers, schemes, and issuing banks on infrastructure built in the 1970s.

Stablecoins collapse that gap. Authorization and settlement happen in the same transaction. No T 2. No batch windows. No correspondent banks taking a cut.

That's why the fee on my €5,000 transfer dropped from $25 to $0.01.

𝗪𝗵𝗼'𝘀 𝗮𝗰𝘁𝘂𝗮𝗹𝗹𝘆 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝗻𝗴 𝘄𝗶𝘁𝗵 𝘄𝗵𝗼?

Most people frame this as "crypto vs banks." It's not.

The real war is:

- Stablecoin rails vs Visa & Mastercard (the interchange model)

- Stablecoin rails vs Swift (correspondent banking)

- Stablecoin rails vs Stripe (merchant acquiring)

And the incumbents know it. Mastercard added Polygon Labs, Ripple, Solana, and Aptos to its Crypto Partner Program. Visa is already settling USDC through Circle. PayPal shipped its own stablecoin (PYUSD).

They're publicly calling stablecoins a threat while privately integrating them into their stack. Classic frenemy move.

APMs were the first wave. Stablecoin rails are the second.

Huge thanks to Benji Audigé for the great work he put into this during the hackathon I organized 🫡

PS: I post weekly about payments, stablecoins, and the reality of building a payment startup. Follow for more!

89

50

421

34,744

R1 | Suby retweeted

Apr 30

Number 1 thanks to @subyhq

Apr 30

Number 1 and not even close 💙🟦

2

4

22

1,375

Apr 29

true

Apr 29

A founder friend runs a SaaS doing €1M/month. He thought he was paying @Stripe 2.9%. We pulled his last 12 months of statements together. The real number? 7.27%.

That's €524K a year going to fees, on a budget line that said €348K.

Here's what that exercise taught me about how payment processors really make money.

Layer #1: Base rate, what Stripe shows you: 2.9% €0.30

Layer #7: Capital float, what no pricing page mentions: T 2 to T 7 payouts on every transaction

Same merchant. Same customers. Same Stripe dashboard. One line on the pricing page. Seven more underneath.

𝗡𝗼𝘄 𝘇𝗼𝗼𝗺 𝗼𝘂𝘁.

The Merchants Payments Coalition pegs the average Visa/Mastercard interchange alone at 2.35%. Stripe's standard rate sits 0.55 points above that. Stripe's real margin on a vanilla domestic transaction is just 55 basis points.

The other 4 points come from products stacked on top: Stripe Billing for subscriptions ( 0.7%), Stripe Tax ( €0.50/calc), Radar for Fraud Teams ( €0.07/screen), the international card surcharge ( 1.5%), the FX spread ( 1%), disputes (€15 per chargeback, non-refundable), and the float on every payout sitting in Stripe's account for 2 to 7 days.

Most founders never run the math. They see 2.9% on the homepage and budget for 2.9%. Then they wonder why their payment line doubles in the year-end review.

𝗪𝗵𝗼'𝘀 𝗮𝗰𝘁𝘂𝗮𝗹𝗹𝘆 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝗻𝗴 𝘄𝗶𝘁𝗵 𝘄𝗵𝗼?

Most people frame this as "Stripe vs alternative PSPs." It's not.

The real war is:

- Stripe's classic stack (2.9% add-ons) vs Stripe's stablecoin stack (1.5% flat)

- Card networks (Visa, Mastercard) vs onchain settlement (USDC, PYUSD, EURC)

- T 2 batch payouts vs same-block finality

And Stripe knows it. They paid $1.1B for Bridge, their largest acquisition ever. They launched Stablecoin Financial Accounts in 101 countries. They shipped stablecoin subscriptions in October 2025. Their Optimized Checkout now defaults to accepting stablecoins.

They're not defending the 2.9% model. They're migrating off it before someone else does it for them.

Publicly selling the headline rate while privately rebuilding their stack on rails that obsolete it. Classic frenemy move, on themselves this time.

—

For founders done paying for layers they never asked for: dozens of SaaS have already moved their Stripe volume to @Subyhq. 5% all-in. No hidden fees, no add-ons, no FX spread, no float games. Dropping to 4% in the coming weeks.

My friend? He's already on the migration plan.

PS: I post weekly about payments, stablecoins, and the reality of building a payment startup. Follow for more!

3

84

Yesterday: 3D = huge technical barrier, reserved for a niche of designers.

Today with this new tool = total game changer.

Well done 👏

Next step ?

Claude now connects to the tools creative professionals already use.

With the new Blender connector, you can debug a scene, build new tools, or batch-apply changes across every object, directly from Claude.

1

1

81

R1 | Suby retweeted

Apr 24

1 year ago, @etherwan_ and I launched @subyhq.

The rest is history.

2

2

15

1,132

Apr 24

legacy projects moving treasury capital in under a week tells you everything about how real this feels to builders. when DAOs that normally take months to mobilize act this fast, that's your signal

Apr 23

Really grateful to see a donation from one of the oldest DAOs in the Ethereum community. Golem is joining DeFi United with 1000 ETH contribution for the relief effort.

1

4

146

Apr 23

hehehe

Apr 23

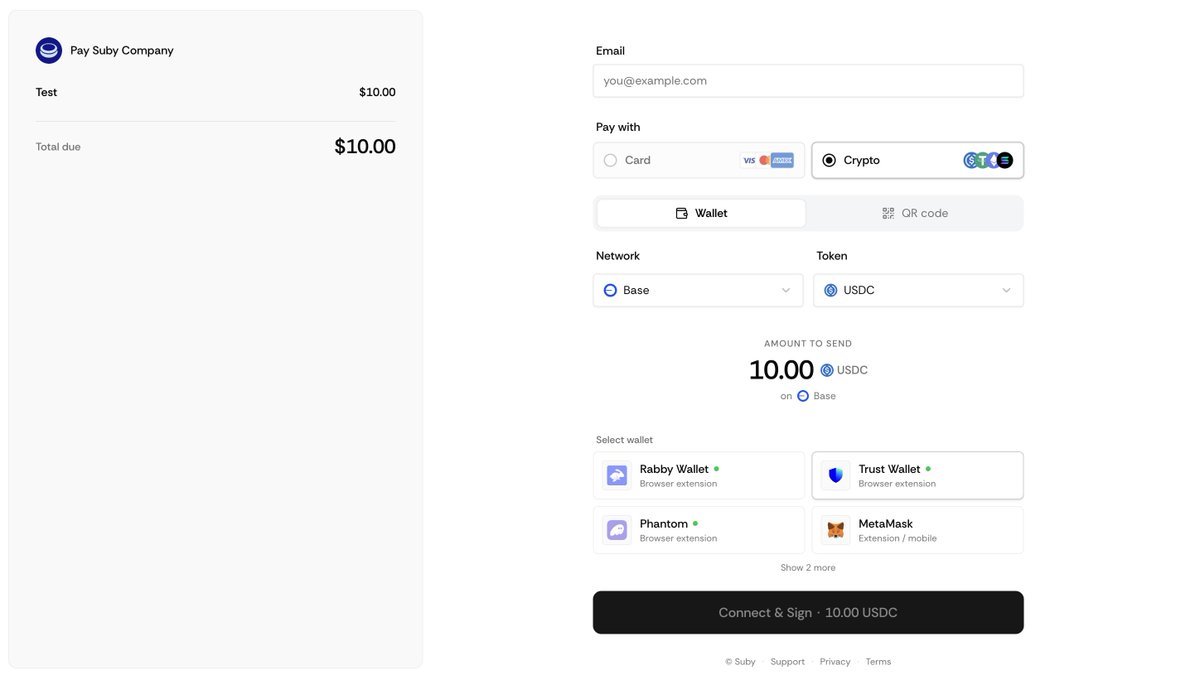

I can finally say it

We have the BEST checkout on the market: card & crypto.

Inspiration design: @nickbakeddesign

Fintech design advice: @privetavdey

Figma design: @pankajstwt

Integration: @etherwan_ & @Ether_MS

Available now at @subyhq

4

118

Apr 22

It’s easier to start an avalanche with multiple snowballs 🏂❄️

Apr 22

I’ve drafted 160 LinkedIn/X post ideas in 1h.

I’ll start scaling content across multiple accounts with @etherwan_ Emil (once his X account is back) and @Ether_MS.

Currently doing 400K views/month alone.

In about 2 months, we’ll be able to hit 2-3M/month (I hope).

3

152

Apr 22

the credential sprawl problem just got visible. before this, every agent integration was a black box of "trust me, it works." now you can actually see what's being passed where. that's the hard part, not the proxy itself

Apr 21

Brex just open-sourced CrabTrap.

A transparent HTTP proxy that sits between your AI agent and every external API it calls.

Okta, but for agents.

AI agents in production are getting real credentials now. API keys. OAuth tokens. Database access. Write privileges to the tools your company runs on.

And nothing in between them and the outside world.

Hallucinated destructive action? Hits production before anyone can intervene. Prompt-injected? Same story. Today's options are "trust completely" or "lock to read-only." Neither works for real work.

How it works:

Every outbound request from the agent gets intercepted. Two checks run:

1. Is this endpoint allowed? (API-level gate)

2. Does this action match the policy, written in plain English? (intent-level gate)

Pass both, through. Fail either, denied. Every request logged and queryable. Blocked agents can escalate for expanded access.

Brex's virtual recruiter Jim is the live example. When Jim tries to email a candidate, CrabTrap checks the policy ("only email candidates who've completed an application") and lets it through or denies it. Same logic for Slack, Greenhouse, anything Jim touches.

---

Pedro Franceschi is an engineer running a financial services company. OpenClaw for personal AI. Now CrabTrap for production agents. He ships the primitives he needs.

Getting value out of AI is an engineering problem first. The CEOs who can think at that layer will pull away from the ones who can't.

2

170

Apr 21

Let’s cook the infra now👨🍳🍳

Apr 21

We've launched a big product update today with @etherwan_ & @Ether_MS.

This is the last one before we start working on scaling the infrastructure to the same level as giant payment companies.

1

2

107

Apr 17

Professor @gaspardlezin is back with another free master class 🤓🙌

Apr 17

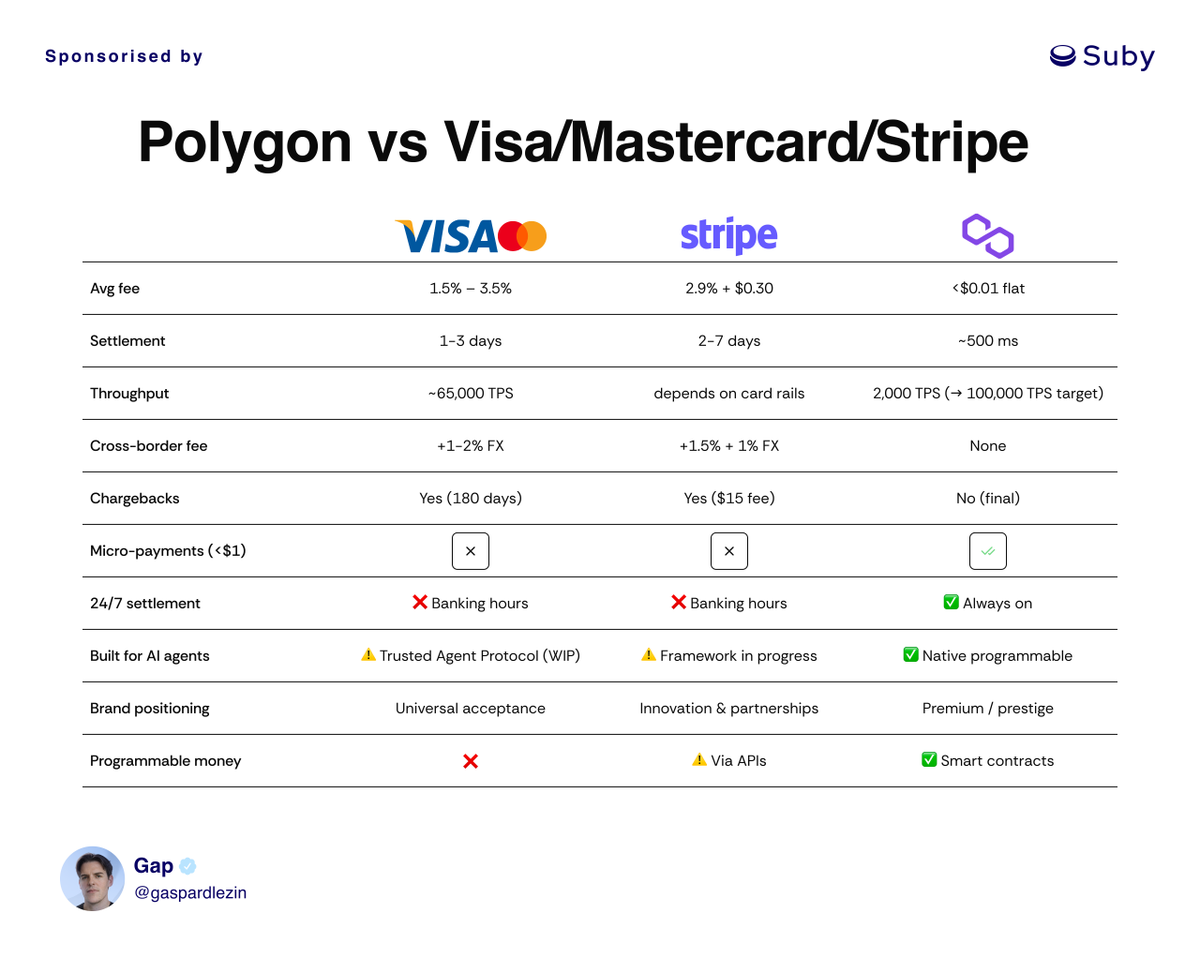

We think crypto competes with banks. In reality, Polygon Labs is going after Visa, Mastercard, and Stripe. And the numbers are starting to prove them right.

@0xPolygon isn't positioning itself as "just another Layer 2" anymore.

Their bet: become the payment infrastructure that directly competes with the biggest web2 payment rails.

The numbers speak for themselves.

Through Paxos, Polygon already processed $1.3B in stablecoin volume with less than $700 in total gas fees. Card networks would have charged ~$32.5M for the same volume at 2.5% interchange.

That's a 99.998% cost reduction.

The "Open Money Stack" strategy

Polygon Labs is raising between $50M and $100M for its new stablecoin payments venture. With $250M already spent on acquisitions, the playbook is clear:

→ Start with institutional B2B payments

→ Pivot to consumer later

→ Build a credible alternative to legacy rails

Marc Boiron (CEO, Polygon Labs) puts it bluntly: today's payment infrastructure was built for humans, not for the agentic commerce that's coming.

The targets are explicit:

- Visa & Mastercard: Polygon's enterprise page literally claims an architecture "that parallels Visa and Mastercard." Near-instant finality, ~$0.001 per transaction, 99.9999% uptime.

- Stripe: Open Money Stack aims directly at institutional payment processing.

- PayPal: already live on Polygon through PYUSD.

The real battlefield: agentic commerce

Deloitte estimates AI-driven commerce could influence $17.5 trillion globally by 2030. McKinsey puts the orchestrated revenue opportunity at $3 to $5 trillion.

Visa launched the Trusted Agent Protocol. Mastercard has Agent Pay. But these frameworks are still built on infrastructure designed for humans: identity checks, settlement windows, fixed fees per transaction.

An AI agent running 1,000 micro-transactions per hour can't operate on those rails.

Frenemies: competing and partnering at once

The paradox: Mastercard just added Polygon to its Crypto Partner Program (alongside Ripple, Solana, and Aptos) in March 2026. Mercuryo Polygon Mastercard are expanding Crypto Credential to self-custody wallets.

Polygon is simultaneously a competitor and a partner of the networks it wants to disrupt.

What it means:

Web2 payment rails aren't disappearing. But their monopoly on institutional flows, cross-border B2B payments, and soon agentic commerce is being directly challenged.

Polygon is betting the next decade of payments won't belong to cards. It will belong to stablecoins running on programmable rails.

And the $1.3B already processed through Paxos is just the start.

APMs were the first wave. Stablecoin rails might be the second.

Thanks to Brian Butler for the data 🫡

PS: I post weekly about payments, stablecoins, and the reality of building a payment startup. Follow for more!

1

4

215

R1 | Suby retweeted

Apr 15

Very raw video to show you all our progress

Already 500 businesses (SaaS, ecom, Discord, Telegram, freelancers) trust Suby and give a lot of feedback every day to improve it

Locked in to beat the Stripe & Whop mafia

7

13

39

2,527